- Electric Mobility

- Intelligent Transportation System (ITS) Market

Intelligent Transportation System (ITS) Market Size, Share, and Growth Forecast 2025 - 2032

Intelligent Transportation System (ITS) Market By Offering (Hardware, Software, Services), Mode of Transportation (Roadways, Railways, Others), System Type (ATMS, ATIS, APTS, ATPS, V2X, Surveillance & Monitoring), Application, and Regional Analysis for 2025 - 2032

Intelligent Transportation System (ITS) Market Size and Trends Analysis

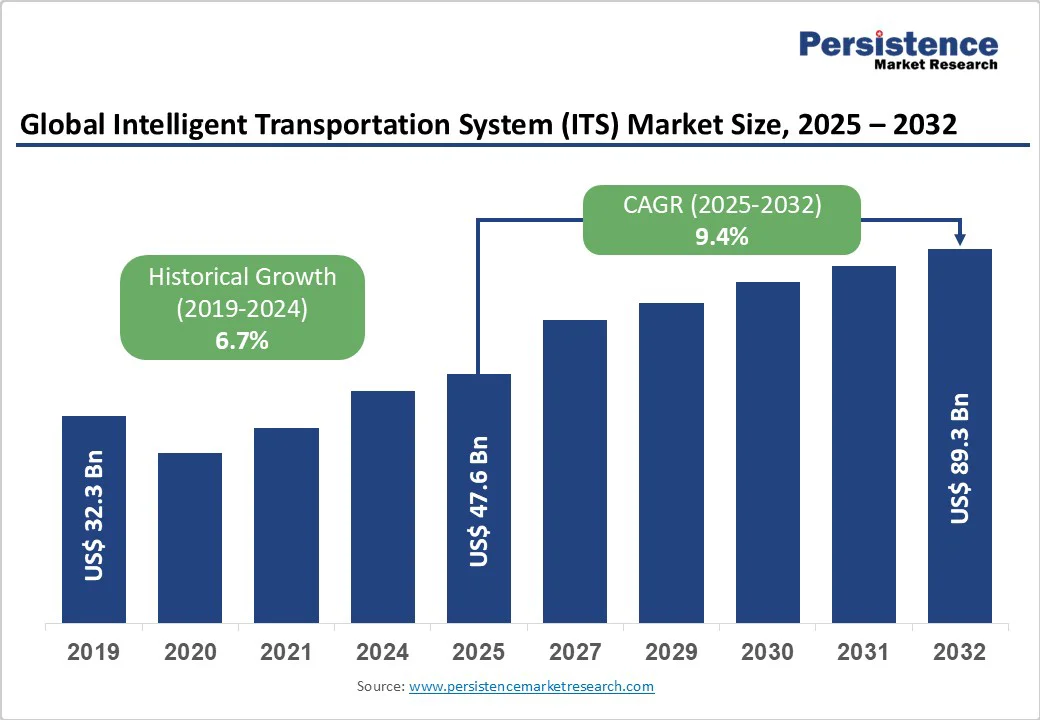

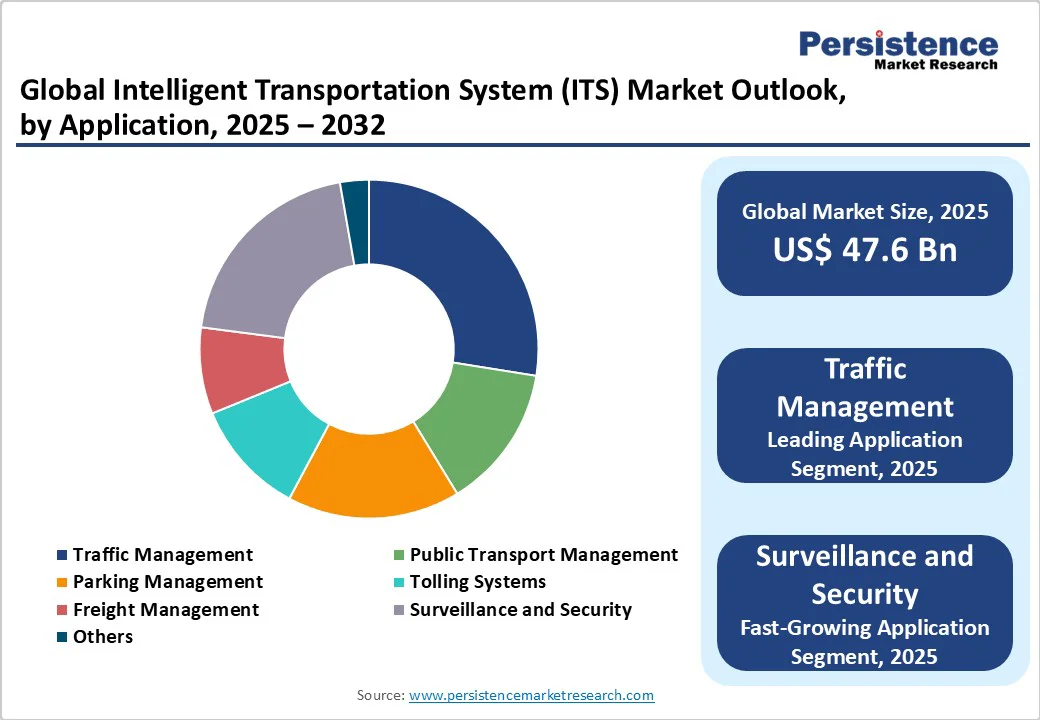

The global intelligent transportation system (ITS) market size was valued at US$47.6 Billion in 2025 and is projected to reach US$89.3 Billion by 2032, growing at a CAGR of 9.4% during the forecast period from 2025 to 2032, driven by rapid urbanization, congestion mitigation, and safety improvement needs, alongside policy-driven deployments, connected vehicle pilots, and AI/video analytics.

Real-world V2X deployments have cut roadside worker collisions by 90%, reduced hard braking by 80%, and lowered travel times by up to 30%, proving strong ROI.

Key Market Highlights

- Leading Region: North America leads ITS adoption with LTE V2X pilots, RSU/OBU standardization, and federal digital infrastructure investments.

- Fastest-growing Region: Asia Pacific is growing fastest, driven by China’s 5G/LTE V2X production, India’s ATMS standards, and AI-enabled smart-city deployments.

- Dominant Mode of Transportation Segment: Roadways dominate ITS due to congestion and safety focus, with ATMS integrating adaptive signals, incident detection, ANPR, and traveler messaging.

- Fastest-Growing System Type Segment: V2X Communication Systems scale rapidly as LTE V2X/5G expands, OEM production increases, and corridor safety/mobility benefits are documented.

- Key Market Opportunity: AI-based incident detection and software-driven optimization reduce reliance on hardware, cut delays and emissions, and enable subscription-based revenue.

| Key Insights | Details |

|---|---|

| ITS Market Size (2025E) ITS Market Size (2025E) | US$47.6 Bn |

| Market Value Forecast (2032F) | US$89.3 Bn |

| Projected Growth CAGR (2025 - 2032) | 9.4% |

| Historical Market Growth (2019 - 2024) | 6.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Advancing Road Safety and Efficiency through V2X-Enabled Intelligent Transportation Systems

Demonstrated gains in safety and mobility from Vehicle-to-Everything (V2X) technology and adaptive traffic management are accelerating the adoption of Intelligent Transportation Systems (ITS). U.S. pilot programs show that digital alerts greatly reduce roadside collisions, heighten driver awareness, and enhance overall road safety. Transit prioritization tools, particularly for school buses, have minimized unnecessary stops, improved travel times, and boosted fuel efficiency, proving the tangible value of connected infrastructure.

These proven results reinforce the cost-benefit case for transportation agencies. By adopting standardized communication devices and upgrading signal controllers, cities and highway authorities can implement phased rollouts within budget constraints. This strategy allows them to modernize high-impact corridors first, realize early safety and efficiency benefits, and establish the foundation for scalable, data-driven mobility networks.

Policy Momentum, Mandates, and Electronic Enforcement Accelerating ATMS and ITS Deployment

Mandates and standards are shortening ITS payback cycles and enhancing adoption. The FCC’s prioritization of LTE-V2X within the 30 MHz allocation establishes a national pathway for safety communications and scalable V2X ecosystems. In India, electronic enforcement rules under the Motor Vehicles (Amendment) Act, 2019, recognize ANPR, speed cameras, WIM systems, and body-worn or dashboard cameras for rule enforcement, creating a framework for ATMS integration.

NHAI’s updated ATMS standards incorporate AI-based Video Incident Detection and Enforcement Systems (VIDES), e-challan APIs, and integration with apps such as Rajmarg Yatra and NHAI One. These codified frameworks drive procurement certainty, lifecycle O&M planning, and sustained budget allocation for ATMS, adaptive signal control, and network-wide incident management.

Barrier Analysis - Cybersecurity, Privacy, and Interoperability Challenges in ITS Deployments

As agencies expand surveillance, telemetry, and connected services, the cyberattack surface increases across vehicles, field devices, TMC software, and cloud back-ends. Reports cite a 25% rise in cyber incidents in highly interconnected environments, necessitating end-to-end encryption, anomaly detection, and zero-trust architectures. Data sensitivity —including location, behavior, and identity —and the risks of deanonymization can undermine public trust without strong governance and privacy-preserving analytics.

Interoperability across heterogeneous data sources and legacy protocols adds technical overheads and can degrade performance unless standardized data models and robust data-fusion architectures are adopted. Agencies must implement rigorous cybersecurity protocols and privacy frameworks to maintain trust while ensuring reliable and integrated ITS operations.

High Initial Capital Expenditure and Integration Complexities with Legacy Infrastructure

ITS programs require significant upfront investments in sensors, controllers, communications, and control centers, along with recurring O&M for devices and analytics. Integrating modern platforms with legacy signals and siloed databases increases timelines, complexity, and costs, particularly for cities with aging infrastructure and limited skilled personnel.

Even when initial capital is supported by smart city programs, ongoing O&M costs —e.g., INR 11.58 crore (US$1.40 Million) annually for a city's ATMs— can strain municipal budgets without outcome-based funding, shared services, or PPP models. Phased procurement, corridor-based rollouts, and modular ITS architectures are essential to avoid vendor lock-in and maintain sustainable, cost-effective operations.

Opportunity Analysis - V2X and Cellularized Corridors Driving ITS Revenue and Corridor Expansion

Mass-market C-V2X is advancing rapidly, with over 10 OEMs producing 5G/LTE V2X warning applications. By October 2024, China’s 5G deployment reached 14.9% and LTE V2X reached 2%, while regulators promoted C-V2X as a “digital seatbelt,” targeting over 60 million connected-vehicle cloud sales by 2034. Equipment benchmarks and validated benefits support scale-ups across snow operations, school zones, and managed lanes.

With FCC LTE-V2X guidance and maturing 5G networks, vendors can bundle RSUs, signal upgrades, and edge orchestration into corridor kits. Partnerships across telecom and cloud ecosystems provide a first-mover advantage, enabling recurring data and software services tied to V2X telemetry, adaptive control, and incident management, establishing V2X as a core ITS revenue driver.

AI-Driven Adaptive Operations, Analytics, and Scalable Enforcement Opportunities

Computer vision and AI are transforming detection, prediction, and enforcement in ITS. Cities in India and globally have deployed AI-enabled CCTV for automated violation detection, queue estimation, and adaptive signal splits, while expressways utilize ITMS for safety and operations. AI-based video incident detection and adaptive signal optimization reduce emissions, delays, and crashes, with studies showing travel-time reductions of 17-30%, waiting-time decreases up to 85%, and meaningful fuel savings.

Software-centric models leveraging connected vehicle data lower reliance on costly field hardware and can reduce OPEX by up to 69% for traffic optimization suites. These innovations create margin-friendly opportunities in SaaS, API monetization, and analytics subscriptions, complementing core ATMS deployments and enabling scalable, high-value ITS services.

Category-wise Analysis

Offering Insights

Hardware leads ITS offerings, with approximately 46-48% market share, driven by sensors, surveillance devices, communications equipment, and upgraded controllers powering ATMs and enforcement systems. Urban networks are scaling CCTV, ANPR, VMS, radar, and loop/ML-based detection across corridors, with documented deployments in India, Europe, and North America. Signal upgrades and RSUs tied to V2X integration, along with known cost ranges, reinforce hardware’s primacy in capex cycles and enable future software layers.

Software and services follow, expanding through AI/analytics, visualization, and cloud O&M models. Government advisories specifying AI-based VIDES, V2X, and surveillance institutionalize hardware baselines, which software orchestrates, underpinning hardware’s current spend leadership while opening annuity streams for software and services across the lifecycle.

Mode of Transportation Insights

Roadways dominate with an estimated ~47% market share due to congestion-relief priorities, safety mandates, and the prevalence of urban signalized intersections that require modernization. National and city programs deploy ATMs, adaptive signals, and electronic enforcement on highways and urban corridors, including the Delhi-Meerut Expressway, the Eastern Peripheral Expressway, and city programs in Mumbai, Goa, Pune, and Ujjain, supported by integrated command centers and sensor networks.

Railways rank second as Europe and Asia modernize signaling, surveillance, and passenger information with centralized control. Structured rollouts first target road networks where congestion and safety challenges are acute, delivering visible ROI through adaptive control and enforcement of violations, justifying roadways’ leadership in ITS investments.

System Type Insights

Advanced Traffic Management Systems (ATMS) lead with ~38-40% share, integrating detection, signal control, incident response, and traveler messaging. Current deployments embed AI-based incident detection, enforcement APIs, and integration with national platforms, making ATMS the core of urban and highway ITS orchestration.

V2X communication systems and surveillance/monitoring are the fastest-growing complements, linking vehicle telematics with infrastructure analytics. FCC LTE V2X policies and multi-city pilots accelerate adoption. Revised standards explicitly prioritize ATMS and VIDES, incorporating e-challan integration, corridor management, and multi-agency interfaces, cementing ATMS as the largest system type in the ITS ecosystem.

Application Insights

Traffic Management is the dominant application (~41-42% share), encompassing adaptive signal control, journey time management, incident detection, and dynamic operations. Real-world outcomes include travel-time reductions of up to 30%, reduced crash risk, and improved compliance in school zones and during winter operations.

Surveillance & Security and Tolling/Enforcement are expanding through ANPR, RLVD, and integrated ticketing pipelines, supported by clear legal frameworks. City and highway programs prioritize congestion relief, safety, and enforceability, placing traffic management at the center of ITS deployment value chains and establishing it as the leading application.

Regional Insights

North America Intelligent Transportation System (ITS) Market Trends

North America is anticipated to be the leading region with 43% market share in 2025. The U.S. is a leading ITS adopter, combining federal research, pilot evaluations, and state DOT deployments across corridors. National pilots demonstrate tangible V2X benefits, including reduced collision conflicts, improved compliance in school zones, and travel-time savings.

FCC’s LTE V2X selection clarifies technology pathways and spectrum usage, while ITS JPO and NTIA tests guide agencies on device densities and performance thresholds. Transparent RSU and OBU costs support capital planning and corridor-scale upgrades, including snow operations and connected school bus priority, reducing crash rates and severity.

Momentum also comes from public-private collaborations, university testbeds, and metropolitan expressway deployments. Interoperability and cybersecurity are standardized workstreams, while innovation ecosystems across automakers, telecoms, and cloud providers enable scalable software services, AI-driven incident detection, emissions reduction, and predictive maintenance in TMCs.

Europe Intelligent Transportation System (ITS) Market Trends

Europe emphasizes regulatory harmonization and safety- and sustainability-led ITS roadmaps. Cities deploy next-gen traffic control software, public transport intelligence, and automated incident systems for bus networks. Rail modernization advances with digital surveillance and control centers, increasing throughput and safety. Regulatory initiatives reduce fragmentation, encouraging harmonized digital markets and strategic infrastructure investment, enabling cross-border ITS integration.

EU member states prioritize privacy-by-design and data governance for scalable analytics, enforcement, and multimodal traveler information. Connected corridors and 5G V2X rollouts, along with AI-enabled adaptive traffic systems, help cities meet climate commitments by reducing congestion and emissions. Select OEMs are already shipping ITS G5 or C-V2X-equipped models, accelerating system adoption.

Asia Pacific Intelligent Transportation System (ITS) Market Trends

Asia Pacific is the fastest-growing ITS region, driven by infrastructure modernization and large-scale smart-city programs. China’s automakers achieved mass production of 5G/LTE V2X vehicles, with deployment rates of 14.9% (5G) and 2% (LTE V2X) by October 2024.

Policies project connected vehicles as a safety backbone. India standardizes ATMS across high-density corridors and urban networks, deploying AI-enabled CCTV, adaptive signaling, and integrated command centers, with O&M models, device inventories, and enforcement API integration.

Southeast Asia and Japan scale digital infrastructure with 5G rollouts, data center expansion, and metro upgrades, enabling multimodal ITS integration and dynamic network operations. Agencies prioritize sustainability, leveraging software-driven adaptive optimization, cloud analytics, and connected vehicle data to reduce congestion and improve safety efficiently.

Competitive Landscape

The global Intelligent Transportation System (ITS) market is moderately fragmented, with strong global incumbents and a dynamic tier of regional integrators. Leading players differentiate through integrated ATMS platforms, AI-based incident detection, tolling and ticketing systems, and V2X-ready solutions.

Key competitive advantages include demonstrated safety and mobility improvements, alignment with standards such as LTE V2X, and the ability to offer modular upgrades to legacy signals and controllers, allowing agencies to modernize infrastructure without complete replacements.

Emerging business models focus on software subscriptions for analytics and optimization, managed services for O&M, and PPP frameworks to fund OPEX-heavy enforcement and surveillance systems. Strategic partnerships with telecom and cloud providers are enabling corridor-scale deployments while generating recurring data and software revenue streams.

Key Market Developments

- In July 2025, Kapsch TrafficCom launched a barrier-free tolling system for multi-lane free flow traffic on National Road 4, north of Oslo, in collaboration with Vegfinans AS. This system aims to improve traffic flow and reduce congestion by eliminating traditional toll booths.

- In August 2025, the Greater Visakhapatnam Municipal Corporation (GVMC) launched "Project SARTHI," a pilot of an AI-based integrated traffic management system. The initiative, in collaboration with the traffic police, uses technologies such as automatic number plate recognition, red-light violation detection, and facial recognition to enhance traffic flow and safety.

- In September 2024, Cubic Corporation introduced Umo ScanRide, a fare payment solution enabling transit agencies to adopt account-based fare collection without installing additional onboard hardware. This innovation aims to streamline fare collection processes and enhance the passenger experience.

- In October 2024, Toyota Motor and Nippon Telegraph and Telephone (NTT) announced a joint investment of 500 billion yen ($3.27 billion) by 2030 to develop an AI infrastructure platform to reduce traffic accidents. The platform will leverage extensive data to enhance driver-assist technology, with plans to deploy by 2028.

Companies Covered in Intelligent Transportation System (ITS) Market

- Siemens AG

- Hitachi Ltd.

- DENSO Corporation

- Cubic Corporation

- Kapsch TrafficCom AG

- Thales Group

- IBM Corporation

- Huawei Technologies Co., Ltd.

- TomTom International BV

- Garmin Ltd.

- Iteris Inc.

- FLIR Systems

- GMV Innovating Solutions

- EFKON GmbH

- Cisco Systems, Inc.

- Indra Sistemas S.A.

- SWARCO

- Q-Free ASA

- NEC Corporation

- Teledyne Technologies Incorporated

- HERE Technologies

- ST Engineering

Frequently Asked Questions

The Intelligent Transportation System (ITS) market is valued at US$47.6 Billion in 2025 and is projected to reach US$89.3 Billion by 2032, at a 9.4% CAGR during 2025-2032, following historical growth of 6.7% during 2019-2024.

Proven safety and mobility benefits from V2X and adaptive operations, formalized electronic enforcement under national acts, and standardized ATMS with AI-based VIDES are driving adoption.

Advanced Traffic Management Systems (ATMS) are leading the way by integrating detection, adaptive control, incident management, and enforcement interfaces, increasingly enhanced with AI-based detection and national e-challan capabilities.

North America leads in documented V2X benefits and policy clarity (LTE‑V2X) in the Intelligent Transportation System (ITS) market.

Software-forward adaptive optimization and AI incident detection layered on capex-funded ATMS deployments, leveraging connected vehicle data to deliver double-digit delay, enabling scalable subscription revenues.

Key players include Siemens AG, Hitachi Ltd., DENSO Corporation, Cubic Corporation, Kapsch TrafficCom AG, and Thales Group.