- Automotive

- Industrial Vehicle Market

Industrial Vehicle Market Size, Share, and Growth Forecast, 2026 - 2033

Industrial Vehicle Market by Vehicle Type (Forklifts, Lift Trucks, Automated Guided Vehicles (AGVs), Tow Tractors, Tugs, Container Handling Vehicles), Propulsion (Battery Electric Vehicles (BEVs), Internal Combustion Engine (ICE), Hybrid Electric Vehicles (HEVs)), By Application type (Cargo, Industrial, Others), and Regional Analysis for 2026 - 2033

Industrial Vehicle Market Share and Trends Analysis

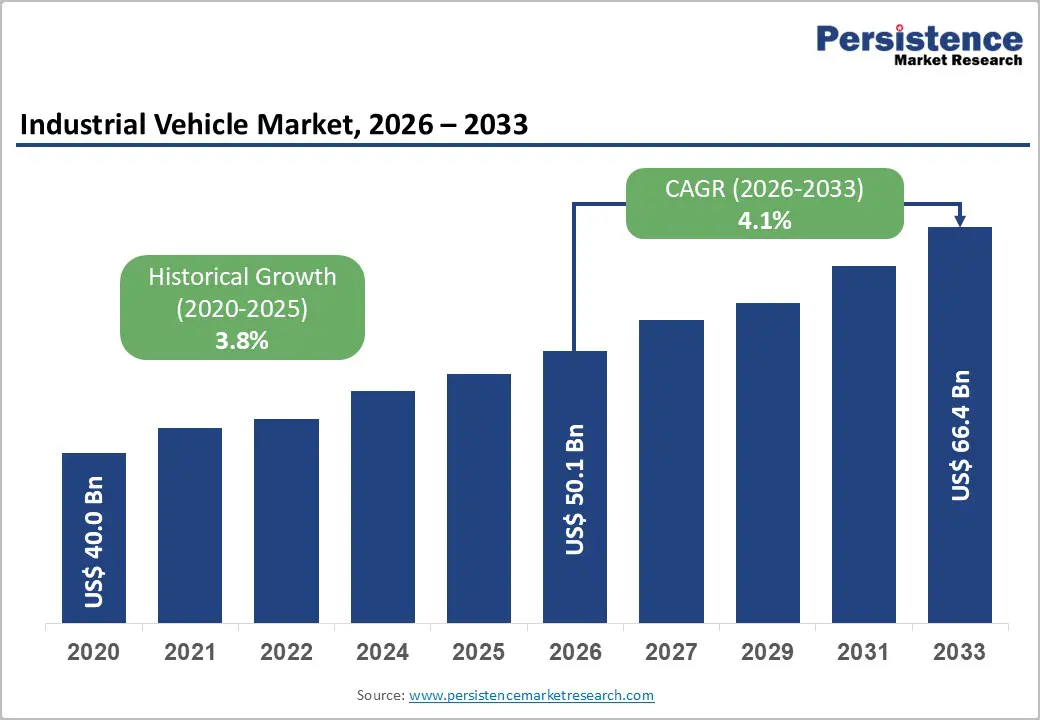

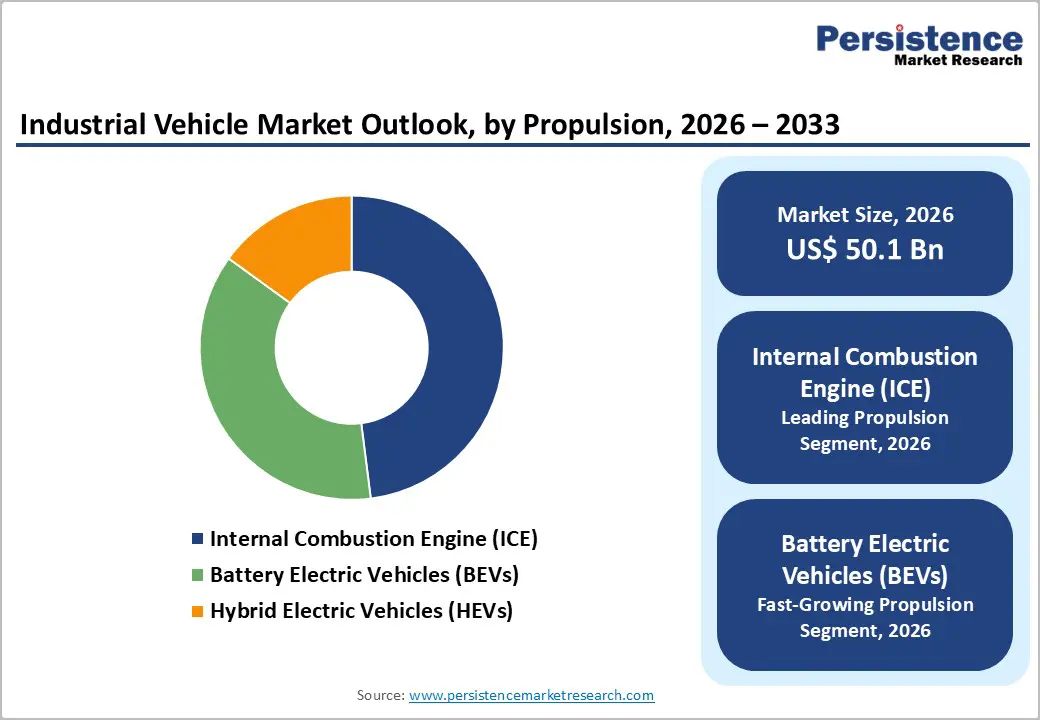

The global industrial vehicle market size is likely to be valued at US$ 50.1 billion in 2026, and is projected to reach US$ 66.4 billion by 2033, growing at a CAGR of 4.1% during the forecast period 2026–2033.

The market is experiencing robust growth driven by increasing demand for efficient material handling and logistics solutions across manufacturing, warehousing, and distribution sectors. Rising adoption of industrial automation technologies, including automated guided vehicles (AGVs) and smart forklifts, is enhancing operational efficiency and reducing labor dependency. Simultaneously, the shift toward electric and autonomous fleet technologies is transforming fleet management practices, improving energy efficiency, and lowering operational costs. Expansion of e-commerce networks, stringent sustainability policies, and advancements in telemetry, robotics, and AI integration are further fueling market momentum. These combined factors are creating significant opportunities for innovation, investment, and strategic growth in the industrial vehicle ecosystem.

Key Industry Highlights

- Dominant Vehicles: Forklifts are set to command around 42% of the revenue share in 2026, while AGVs are likely to grow the fastest from 2026 to 2033, driven by automation and labor optimization.

- Leading Propulsion: Internal combustion engine (ICE) is projected to lead with approximately 48% share in 2026, whereas battery electric vehicles (BEVs) are expected to expand at a 10.2% CAGR through 2033, supported by electrification initiatives.

- Application Focus: Industrial applications are anticipated to capture around 38% of revenue in 2026, while cargo handling is likely to register the highest 2026-2033 CAGR, owing to e-commerce and logistics modernization.

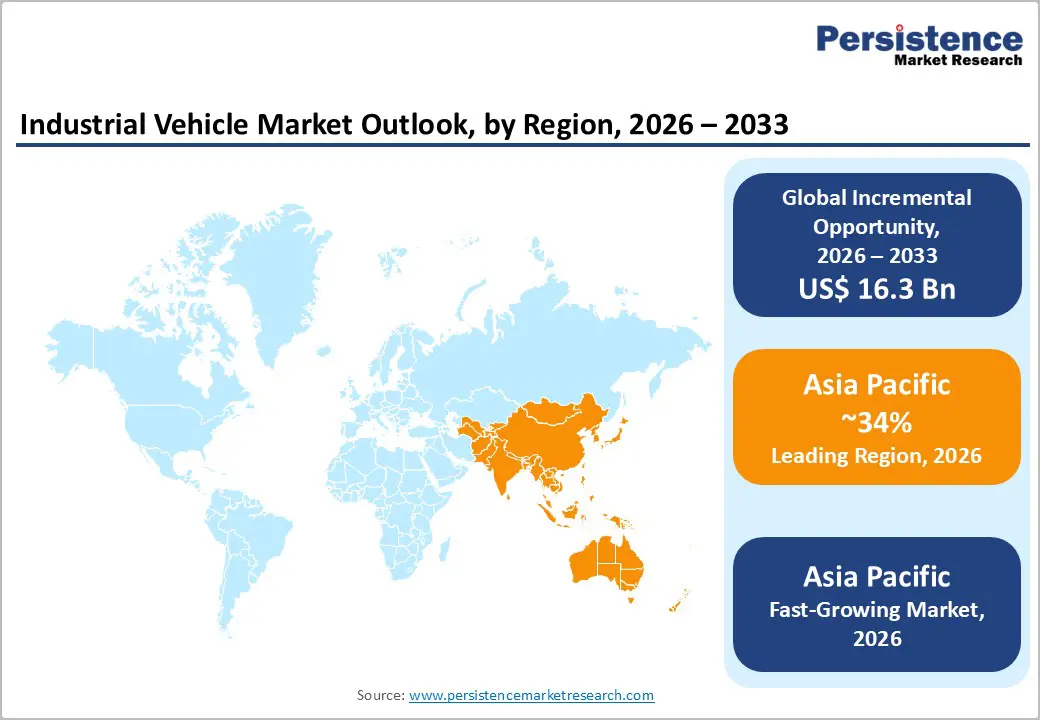

- Regional Leadership: Asia Pacific is set to lead with 34% market share in 2026 and is expected to grow at a 4.5% CAGR through 2033, fueled by electric vehicle (EV) manufacturing expansion.

- Strategic Developments: Key market developments emphasize fleet autonomy, connectivity, and operational optimization, including technology partnerships, product innovations, and geographic expansions.

| Key Insights | Details |

|---|---|

| Industrial Vehicle Market Size (2026E) | US$ 50.1 Bn |

| Market Value Forecast (2033F) | US$ 66.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rapid Expansion of E-Commerce and Logistics Automation

The rapid expansion of e-commerce and logistics automation is driving a substantial increase in demand for industrial vehicles across warehousing and distribution networks. As online commerce continues to grow and supply chains become more complex, operators are investing in modern fleets to boost throughput, reduce labor intensity, and streamline the movement of goods within facilities. These investments also enhance workplace safety, improve order accuracy, and optimize operational reliability in high-volume operations. Advanced fleet management systems, robotics, and automation tools further support real-time monitoring and efficient coordination of multiple vehicles, enabling companies to handle surges in demand while maintaining productivity and operational resilience.

Leading logistics companies in North America and Europe are scaling robotics and automation deployments to meet growing demand. For instance, major U.S. fulfillment centers have implemented autonomous mobile robots for pallet handling and order picking, while European warehouses are integrating AI-driven fleet management systems to optimize workflow. In Asia Pacific, e-commerce leaders are deploying advanced AGVs to handle surges in order volumes. These developments illustrate how automation technologies are reshaping material handling, driving fleet modernization, and enhancing global logistics efficiency.

Electrification and Autonomous Technologies

Government policies and sustainability initiatives worldwide are accelerating the shift toward electric and autonomous industrial vehicles. Zero-emission mandates in Europe and North America, combined with national electrification strategies, are pushing enterprises to adopt battery electric fleets, which reduce emissions and operational costs. Companies are also combining electrification with real-time monitoring systems to optimize energy management, maintenance planning, and fleet utilization. These trends create a strong incentive for modernization and future-proofing industrial operations.

In Europe, several countries are providing subsidies and incentives for electrified industrial vehicles and related charging infrastructure, encouraging fleet upgrades in warehouses and ports. North American companies are piloting autonomous electric forklifts and AGVs to enhance efficiency and meet stringent workplace safety standards. In Asia Pacific, China’s electrification programs continue to support fleet modernization, while India’s PM E-Drive scheme incentivizes domestic production and adoption of electric vehicles. Collectively, these initiatives highlight how electrification and autonomous technologies are globally driving industrial vehicle growth and shaping future fleet strategies.

High Upfront Capital Expenditure

The deployment of advanced industrial vehicle fleets, particularly electric and autonomous models, requires significant upfront investment compared to conventional internal combustion engine units. Costs associated with electrified platforms, charging infrastructure, automation systems, and software platforms can surpass traditional fleet acquisition budgets, making adoption challenging for financially constrained organizations. Even though long-term operational savings are achievable, initial capital outlay can strain cash flow and slow procurement decisions. Companies often require extended approval cycles to balance short-term costs with projected efficiency gains, particularly in cost-sensitive markets where capital budgets are limited.

The escalating component and energy costs have added pressure to capital budgets across industrial sectors. Automakers and logistics providers are experiencing tighter margins due to rising input prices, prompting a reevaluation of capital allocation for automation and electrification initiatives. For example, broader industry reports note intensifying cost pressures from tariffs and production inefficiencies impacting vehicle and component manufacturing, which could constrain investment in advanced fleets and infrastructure. These compounded cost dynamics create a challenging environment for upgrading industrial vehicle fleets without substantial financial planning and strategic funding support.

Supply Chain and Component Constraints

The industrial vehicle sector remains highly dependent on critical components such as lithium-ion batteries, semiconductors, and automation hardware, and disruptions in these supply chains can constrain production timelines and inflate costs. Extended lead times for essential parts, particularly semiconductors used in electric powertrains and navigation systems, have delayed deliveries and squeezed production planning. Regions without established local supply chains for these components are especially vulnerable, driving companies to manage risk through inventory buffering and sourcing diversification. Such constraints can slow fleet expansion and delay technology rollout across key industrial markets.

Recent supply chain movements illustrate ongoing component pressures. Lead times for electronics and semiconductor chips have lengthened significantly, with producers in the U.S. reporting extended delivery windows and increased costs for critical parts used in industrial electrification and automation. Automotive and related manufacturers have also faced multiple production halts and operational suspensions due to semiconductor shortages, underscoring the ripple effect of component constraints on broader manufacturing sectors. These persistent supply chain vulnerabilities heighten risk for industrial vehicle producers and buyers alike, emphasizing the need for strategic supply chain resilience planning.

Electrification Focus in Emerging Economies

Emerging markets across Asia Pacific and Latin America are increasingly prioritizing sustainable logistics and modernized manufacturing practices, creating a substantial growth opportunity for electric industrial vehicles. Rising energy costs and tightening environmental regulations are encouraging companies to adopt electrified fleets that offer operational cost advantages and compliance benefits, especially where industrial growth coincides with sustainability goals. Investments in green technologies are becoming central to strategy as regions seek cleaner logistics and lower emissions.

Public policy actions are reinforcing this trend. For example, Kenya’s National Electric Mobility Policy introduces comprehensive incentives, including tax exemptions and support for charging infrastructure, to accelerate electric vehicle adoption across transport sectors, signaling strategic intent to modernize fleets and cut emissions. The policy also prioritizes EV procurement in government fleets and expands charging infrastructure along major corridors, strengthening the case for electrified industrial vehicles in new markets.

Upmarket Shift towards Intelligent Fleet Solutions

The growing adoption of smart telematics, predictive analytics, and autonomous functions is enabling industrial vehicle manufacturers to offer advanced fleet solutions bundled with software services. These digital solutions help companies optimize asset utilization, enhance uptime, and improve operational efficiency through centralized data insights. By shifting from pure hardware sales to value-added operational services, manufacturers can generate recurring revenue streams and deepen customer engagement while addressing complex logistical needs.

Major logistics firms are investing heavily in warehouse automation and robotics to streamline operations and support e-commerce growth. For instance, a leading logistics provider announced a £ 550 million investment to expand robotics and automation across its U.K. and Ireland operations, deploying over 1,000 additional robots aimed at boosting efficiency and meeting demand in high-volume facilities. Such large-scale automation investments exemplify how fleet technologies are evolving into integrated, intelligent systems that combine hardware, software, and analytics, further expanding opportunities for digital fleet-oriented industrial vehicle solutions.

Category-wise Analysis

Vehicle Type Insights

Forklifts are likely to command an estimated 49% of the industrial vehicle market revenue share in 2026, due to their essential role in material handling across manufacturing, warehousing, and logistics operations. Their versatility, ability to handle varied load types, and compatibility with multiple applications reinforce their importance in modern supply chains. In late 2025, Kalmar secured a contract to supply a fleet of medium forklifts with next-generation lithium-ion batteries to ArcelorMittal, supporting efficient and sustainable handling in demanding steelmaking environments. Meanwhile, Hyundai Material Handling’s B-X Series high-voltage electric forklifts received a major product honor in 2025, showcasing advancements in electrified heavy-duty lift technology designed for rapid charging and extended uptime, highlighting the modernization of traditional forklift platforms.

Automated guided vehicles are estimated to be the fastest-growing vehicle type, set to record a CAGR of roughly 9.5% between 2026 and 2033, driven by automation, labor optimization, and flexible material handling needs. They improve throughput, reduce manual handling risks, and support agile operations in fulfillment centers and industrial parks. In 2026, Oshkosh Corporation demonstrated expanded autonomy and AI-based capabilities in industrial and construction equipment, reflecting original equipment manufacturer (OEM) integration of autonomous technologies across product lines. Supporting this trend, Addverb unveiled a wheeled humanoid industrial robot at LogiMAT India 2026, signaling the convergence of AGV and robotics technologies to enhance efficiency and operational effectiveness in complex logistics and warehouse environments.

Propulsion Insights

ICE is poised to lead in 2026, capturing around 42% of the industrial vehicle market share, particularly in outdoor, heavy-duty, and high-load applications where long runtimes and established refueling infrastructure are critical. Their reliability, familiarity, and robust service networks make them indispensable in construction, port, and industrial operations. Terex completed a strategic merger with REV Group, creating a diversified industrial equipment leader with a strong portfolio of ICE-powered vehicles, underscoring continued reliance on conventional powertrains while integrating newer technologies. This approach allows enterprises to maintain operational continuity and fleet readiness during gradual transitions toward electrification.

Battery electric vehicles are anticipated to be the fastest-growing propulsion segment, with a 9.2% CAGR supported by sustainability mandates, total cost of ownership advantages, and regulatory momentum. They are increasingly preferred for indoor operations, where zero emissions and reduced noise enhance safety and air quality. In early 2026, BYD held its Global Forklift Product Release Summit, unveiling its latest lineup of electrified forklifts, demonstrating OEM commitment to BEV innovation. Additionally, Vision Battery showcased high-performance lithium solutions for forklifts and AGVs at CeMAT Asia 2025, highlighting modular battery systems that enable longer runtimes and faster charging, positioning BEVs as a key driver of future industrial vehicle growth.

Regional Insights

North America Industrial Vehicle Market Trends

North America accounts for a significant share of industrial vehicle demand, with the United States leading the region as logistics, manufacturing, and warehouse modernization accelerate adoption. The region’s advanced logistics infrastructure and e-commerce networks support investments in electrification and automation, with fleets increasingly prioritizing electric, zero-emission solutions to enhance efficiency and reduce operating costs. Heavy-duty electromobility is gaining traction, with Volvo Trucks reporting over 700 battery-electric VNR Electric trucks operating across the U.S. and Canada, highlighting corporate leadership in fleet decarbonization efforts and CO2 reductions.

Leading industrial fleets are also advancing electrification at scale. Orange EV’s electric yard trucks have surpassed 10 million operating hours across more than 1,600 vehicles deployed in the U.S. and Canada, demonstrating real-world performance, high uptime, and measurable fuel and maintenance savings for major logistics and industrial operators. Partnerships supporting sustainable logistics are also expanding; Lazer Logistics and Orange EV have deepened collaboration on yard electrification, further embedding zero-emission fleet solutions into core logistics operations across multiple facilities. These company-level advancements illustrate how heavy-duty electrification and yard transformation are strengthening North America’s market leadership while driving regional innovation.

Europe Industrial Vehicle Market Trends

The Europe industrial vehicle market is anchored by leading industrial nations such as Germany, France, Spain, and the United Kingdom. Harmonized EU emissions regulations and sustainability mandates are directing fleet investments toward electrification and automation, which are becoming essential criteria for procurement across logistics and manufacturing sectors. Electrified medium and heavy commercial vehicles are increasingly visible on European roads, and infrastructure initiatives such as expanded megawatt charging demonstrations in Germany in 2026 showcase how OEMs and public-private partnerships are accelerating charging ecosystem deployment to support zero-emission fleets.

In addition to hardware upgrades, European fleets are expanding autonomous and connected solutions to address labor challenges and digital transformation goals. Automotive and logistics players are testing autonomous commercial vehicles and AI-enabled fleet systems that integrate advanced safety and operational technologies for intraregional freight applications. These developments support deeper industrial vehicle penetration into advanced logistics operations. Operators are strengthening supply chains by coupling electrification with automation, aligning with decarbonization pathways, and improving long-term operational performance and sustainability outcomes.

Asia Pacific Industrial Vehicle Market Trends

Asia Pacific is anticipated to the fastest-growing regional market for industrial vehicles, projected to expand at a CAGR of around 4.5% through 2033, driven by China’s expansive manufacturing base, rapid e-commerce growth, and strong logistics modernization initiatives. Across the region, adoption of electric freight and electrified industrial vehicles is accelerating: in the first half of 2025 alone, nearly 90,000 electric cargo trucks were sold, with China accounting for about 80,000 of those sales, a clear signal of battery-electric vehicle preference for industrial and logistics applications. Rising urbanization, government-supported green logistics programs, and the development of integrated industrial parks are further reinforcing fleet modernization across multiple sectors.

This shift toward electrified freight is strengthened by infrastructure and commercial initiatives targeting cross-border logistics corridors. For example, GreenSpace E-Mobility announced the Americas’ first binational electric freight route between Texas and Nuevo León, planned with ultra-fast charging stations tailored to heavy-duty electric vehicles, a model that could inspire similar deployments in Asia Pacific logistics hubs. Domestic players in the region are actively scaling electrified vehicle offerings tailored to local conditions and industrial demands, fortifying Asia Pacific’s role as a hub of electrification, automation, and fleet modernization. Investment from both regional and global OEMs continues to expand production capabilities, battery supply chains, and smart fleet deployments across the region.

Competitive Landscape

The global industrial vehicle market structure is moderately consolidated, with top players such as Toyota Industries, Kion Group, Jungheinrich, Hyster-Yale, and Mitsubishi Logisnext capturing a significant portion of overall revenue. These established manufacturers leverage extensive OEM networks, long-standing client relationships, and comprehensive service ecosystems. They continue to invest heavily in R&D for electric and autonomous vehicle platforms, fleet telematics, and predictive maintenance technologies, ensuring leadership in smart and sustainable material handling solutions.

Regional and niche competitors, including Doosan Industrial Vehicles, Godrej Material Handling, and Addverb Technologies, are focusing on specialized applications, automation solutions, and geographic strongholds. Market entry barriers such as high capital expenditure, stringent regulatory standards, and complex integration requirements limit new entrants. However, digitalization and software-driven fleet management solutions are creating opportunities for smaller technology providers to collaborate through integration partnerships. Industry consolidation is expected to progress gradually as leading OEMs pursue strategic acquisitions to enhance geographic presence, technological capabilities, and electrified fleet offerings.

Key Industry Developments

- In January 2026, DF Automation & Robotics expanded its presence in India and dispatched 40 domestically made AGVs and autonomous mobile robots (AMRs), supporting local industry automation efforts. The initiative strengthens regional production capacity and reflects growing demand for intelligent material handling solutions in the Indian manufacturing sector.

- In December 2025, Hyundai’s high-voltage electric forklift earned Product of the Year award, a top industry honor, for advancing material handling efficiency with zero tailpipe emissions and robust performance. The recognition highlights growing demand for sustainable, electric industrial vehicles in logistics and warehouse operations.

- In December 2025, Yale Lift Truck Technologies unveiled a new series of electric forklifts featuring integrated lithium-ion battery technology designed to deliver all-terrain capability and extended operational uptime. The launch reflects growing industry momentum toward electrified material handling solutions that combine durability with lower emissions and reduced total cost of ownership.

Companies Covered in Industrial Vehicle Market

- Toyota Industries Corporation

- KION Group

- Jungheinrich AG

- Crown Equipment Corporation

- Mitsubishi Logisnext

- Hyster Yale Materials Handling

- Komatsu Ltd

- Caterpillar Inc.

- Doosan Industrial Vehicle

- Clark Material Handling

- Nissan Forklift

- Crown Equipment

- JCB

- Manitou Group

- Yale Materials Handling

Frequently Asked Questions

The global industrial vehicle market is projected to reach US$ 50.1 billion in 2026.

Growth is driven by e-commerce expansion, automation adoption, and electrification of fleets across logistics and manufacturing sectors.

The market is poised to witness a CAGR of 4.1% from 2026 to 2033.

Opportunities include fleet electrification in emerging markets and intelligent, software-enabled fleet management solutions.

Toyota Industries, Kion Group, Jungheinrich, Hyster-Yale, and Mitsubishi Logisnext are some of the key players.