- Industrial Machinery

- Industrial Sewing Machines Market

Industrial Sewing Machines Market Size, Share, Trends, Growth, Regional Forecasts, 2026 to 2033

Industrial Sewing Machines Market by Product Type (Cylinder-Bed, Flatbed, Long-Arm, Post-Bed), End-User (Apparel Industry, Automotive Industry, Textile Industry, Footwear Industry), Operation (Manual, Semi-Automatic, Automatic), and Regional Analysis for 2026-2033

Industrial Sewing Machines Market Share and Trends Analysis

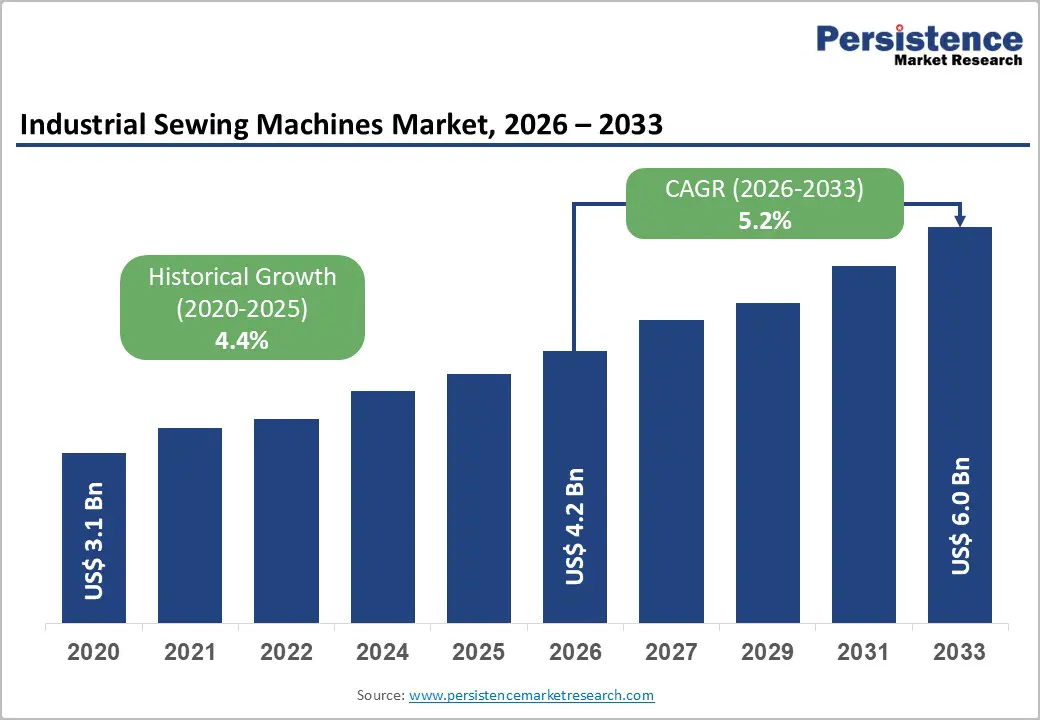

The global industrial sewing machines market size is likely to be valued at US$ 4.2 billion in 2026, and is projected to reach US$ 6.0 billion by 2033, growing at a CAGR of 5.2% during the forecast period 2026−2033.

The booming textile and apparel industry drives growth in the industrial sewing machinery market. Evolving fashion trends and fast fashion demands prompt manufacturers to invest in advanced machinery for enhanced productivity and quality maintenance. Automation delivers quicker turnaround times and higher precision, vital for competitiveness. E-commerce acceleration further boosts apparel demand, spurring machinery adoption. Internet of Things (IoT) and artificial intelligence (AI) integration can further enable real-time monitoring and operational optimization, strengthening market expansion.

Key Industry Highlights

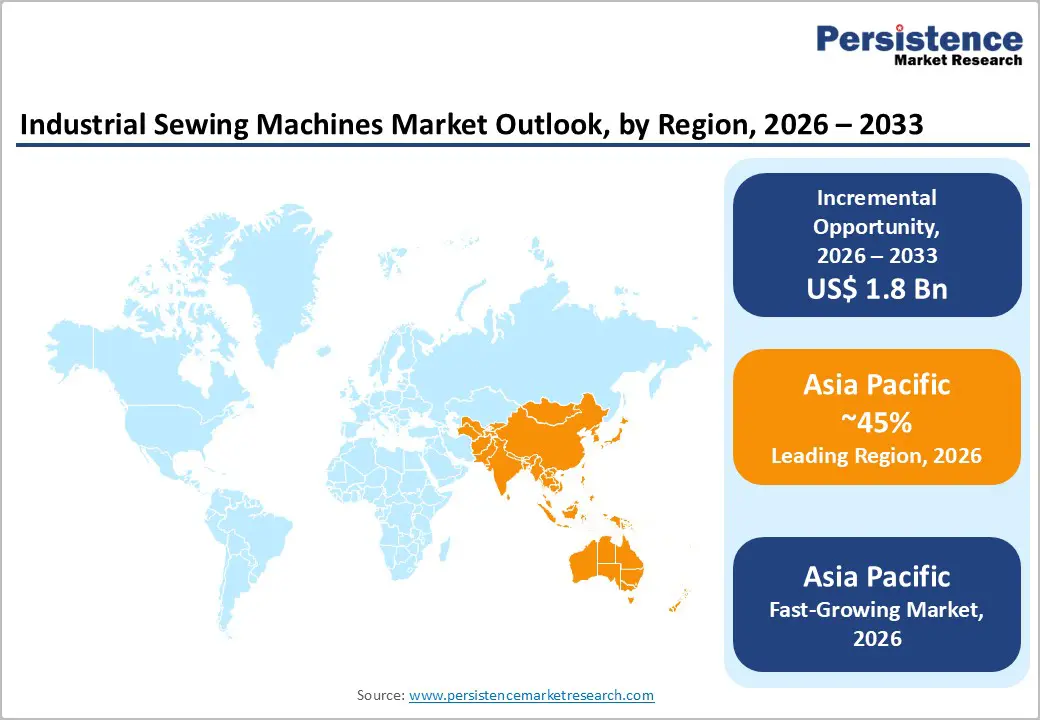

- Dominant Region & Fastest-growing Market: Asia Pacific is likely to be both the leading and fastest-growing regional market through 2033, accounting for approximately 45% market share in 2026, supported by established garment industries and significant exporters of textile products.

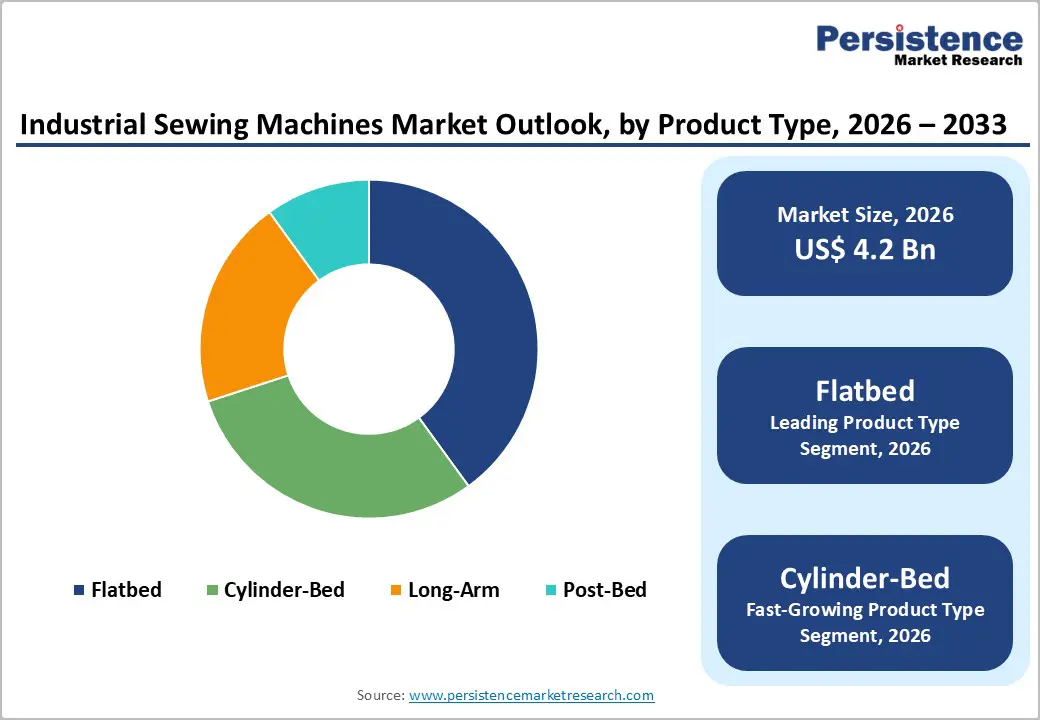

- Leading & Fastest-growing Product Type: Flatbeds currently dominate the product type segment, commanding approximately 40% of total market revenue, with cylinder-bed likely to be the fastest-growing segment during the 2026-2033 forecast period.

- Leading & Fastest-growing End-User: The apparel industry represents the dominant segment, capturing approximately 52% of market revenue share in 2026, while the automotive industry is expected to be the fastest-growing segment over the 2026-2033 forecast period.

- Main Driver: Smart manufacturing initiatives and Industry 4.0 principles are accelerating upgrades for outdated sewing machines.

| Key Insights | Details |

|---|---|

| Industrial Sewing Machines Market Size (2026E) | US$ 4.2 Bn |

| Market Value Forecast (2033F) | US$ 6.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.4% |

DRO Analysis

Expansion of the Global Apparel and Technical Textile Industries

The textile and apparel industry currently fuels strong growth in the industrial sewing machinery market. Fashion brands actively respond to shifting consumer preferences by adopting advanced equipment that boosts output and ensures consistent standards. Manufacturers invest in these machines to handle larger orders efficiently. E-commerce platforms drive higher volumes of clothing sales, which in turn increases the need for reliable production tools. At the same time, companies integrate IoT and AI technologies into sewing systems. These features allow real-time tracking of performance and fine-tuning of processes, which helps firms cut waste and speed up operations.

Technical textiles will further expand this market in the coming years. Sectors such as medical fabrics, geotextiles, automotive materials, and filtration products demand specialized machinery for precise assembly. Producers will require both high-capacity units for bulk runs and custom-built models for complex tasks. This variety creates fresh opportunities for suppliers to serve diverse clients worldwide. Manufacturers will have perfected equipment that meets these needs, which strengthens global supply chains. Overall, these trends position industrial sewing machine providers to capture sustained demand as industries evolve and innovate continuously.

Automation and Industry 4.0 Adoption in Textile Manufacturing

Smart manufacturing initiatives and Industry 4.0 principles currently accelerate upgrades for outdated sewing machines. Governments in regions such as the, Japan, South Korea, and China actively support these shifts through digitalization programs. Manufacturers adopt computer numerical control (CNC) and electronically automated systems that connect smoothly with manufacturing execution systems (MES). These integrations provide instant quality checks, stitch adjustments, and upkeep predictions. Firms gain efficiency as a result, which lowers operational expenses and minimizes material losses. Producers will soon complete fleet modernizations that transform production lines.

Mid-sized and large operations lead this change by installing connected equipment. Such upgrades enhance oversight across factories and enable data-driven decisions. Workers focus more on oversight tasks rather than manual adjustments, which boosts overall productivity. Suppliers respond by designing versatile machines that fit various scales. This evolution strengthens competitiveness in global markets. Companies position themselves for long-term gains as automation deepens. Industry leaders will capture larger shares through these advancements, while smaller players explore affordable entry options. Overall, these developments reshape workflows and open doors for sustained innovation in sewing technology.

Skilled Labor Shortage and Technology Integration Complexity

The transition to advanced electronically controlled and AI-assisted sewing systems demands that workers acquire specialized skills. Operators now master programmable logic controllers (PLCs) for precise programming, while technicians handle IoT diagnostics to resolve connectivity issues swiftly. Factories in regions such as South Asia and Sub-Saharan Africa struggle with limited access to such trained personnel. This scarcity slows equipment rollout, as teams grapple with unfamiliar interfaces and software. Production lines face interruptions, which inflate initial costs and prolong the path to optimal performance. Manufacturers actively counter these challenges with structured upskilling initiatives that will deliver promising results.

Companies collaborate with vocational institutes to deliver hands-on curricula focused on modern machinery. Equipment vendors provide customized workshops, both in-person and virtual, that simulate real-world scenarios. These programs reduce idle time dramatically and accelerate seamless integration into daily workflows. Employees build expertise in troubleshooting, which enhances stitch accuracy and minimizes defects. Firms achieve cost savings over time through fewer breakdowns and efficient upkeep routines. Leaders establish credentialing systems that match global benchmarks, fostering talent retention. This strategy converts skill deficits into strategic strengths, enabling faster innovation cycles. Ultimately, targeted education drives reliable adoption of cutting-edge technology and equips businesses to thrive amid rapid industry changes.

High Capital Cost and Financing Barriers for SMEs

Advanced industrial sewing systems demand substantial upfront investments, which challenge small and medium-sized enterprises (SMEs) the most. Owners hesitate to purchase CNC and fully automated units due to their high price tags. Basic mechanical options cost far less and suit tight budgets better. Firms in developing regions struggle to secure loans or leases for upgrades. Banks often view textile operations as risky, so they deny funding requests. This financial hurdle blocks access to tools that boost speed and accuracy. Manufacturers will overcome these obstacles by offering flexible payment plans by the decade's close.

Vendors introduce leasing models and installment options tailored to cash flows. Governments step in with subsidies and low-interest programs for key sectors. Partnerships with financial institutions ease approvals for equipment deals. SMEs gain entry to superior technology, which raises their output levels. Owners see quicker returns through reduced labor needs and fewer errors. Leaders craft modular designs that scale with business growth. This openness expands customer bases in underserved areas. Suppliers build loyalty as clients upgrade over time. Smart financing strategies widen market reach and fuel steady demand across all sizes of operations.

Medical and Technical Textile Manufacturing Requiring Specialized Equipment

Demand for medical-grade textiles grows steadily worldwide. Producers create items such as surgical gowns, wound dressings, cardiovascular implants, and filtration media. These products require sewing machines with exact stitch control that meet International Organization for Standardization (ISO) standards. Manufacturers design units with anti-contamination features and cleanroom readiness. Companies prioritize sterile environments to prevent defects in critical applications. Suppliers focus on durable seams that withstand sterilization processes. This niche pulls advanced equipment from general markets into specialized production lines. Firms will secure lucrative contracts by investing in research and development (R&D) for tailored solutions in the coming years.

Healthcare giants seek reliable partners for long-term original equipment manufacturer (OEM) deals. Vendors earn higher margins through custom builds that match strict regulations. Producers gain repeat business as facilities expand globally. Innovations like touchless interfaces and self-cleaning mechanisms set leaders apart. Clients value machines that integrate with quality tracking systems for compliance audits. Suppliers form alliances with medical firms to co-develop next-generation tools. This focus opens doors to stable revenue streams beyond the apparel sector. Businesses position themselves as trusted experts in high-stakes fields. Medical textiles drive premium demand that rewards forward-thinking manufacturers with enduring partnerships and market advantages.

Integration of Advanced Technologies such as IoT, AI, and ML in Sewing Machinery

IoT and AI technologies currently transform sewing operations by providing instant oversight and fine-tuning. Machines track thread tension, speed settings, and fabric feed in real time. Operators receive alerts for adjustments that ensure even seams and minimal flaws. Factories achieve smoother workflows as systems self-correct minor issues. Predictive maintenance schedules service before breakdowns occur, which extends equipment durability. Teams focus on value-added tasks rather than routine checks. Manufacturers integrate these features to meet demands from clients who seek flawless outputs in competitive environments. Industry 4.0 principles will propel connected automation to new heights by decade's end. Producers invest heavily in R&D to embed smart capabilities into core designs.

Vendors create platforms that link seamlessly with factory networks for centralized control. This connectivity supports data analysis that reveals patterns in production trends. Companies gain an edge through customized solutions that adapt to specific materials or styles. Suppliers partner with software firms to enhance machine intelligence over time. Clients benefit from lower running costs and faster order fulfillment. Leaders launch modular upgrades that evolve with client needs. Such innovations attract buyers in sectors beyond apparel, such as technical fabrics. Businesses secure loyalty by delivering tools that scale with expansion plans. Overall, these advancements position forward-looking firms to dominate as smart factories become standard, unlocking sustained expansion in a digitized landscape.

Category-wise Analysis

Product Type Insights

Flatbeds currently dominate the product type segment, commanding approximately 40% of total market revenue, due to their exceptional versatility and ability to manage diverse tasks. They excel in the apparel sector, where operators use them for stitching garments like shirts, pants, and dresses with straight and curved seams. This broad applicability ensures high demand in mass production settings. Ongoing technological upgrades, such as automated tension controls and digital interfaces, further solidify their position. These enhancements boost functionality, simplify operations, and reduce setup times. Manufacturers favor flatbeds for reliable performance across fabric types, securing their top market share through consistent innovation and user-friendly designs.

Cylinder-Bed is likely to be the fastest-growing segment during the 2026-2033 forecast period. The segment has strong growth potential, tailored for tubular and curved items that flatbed models handle poorly. They serve the automotive and furniture sectors by stitching upholstery, car seats, and similar components with ease. As these industries expand, demand for such specialized units rises steadily. Operators value their ability to access tight spaces without fabric bunching. Technological upgrades drive this segment's rapid adoption. Features like automated feed systems and precision sensors minimize manual adjustments and boost seam accuracy. These enhancements cut production errors and speed workflows. Manufacturers target cylinder-bed models for high-value applications, positioning them as the fastest-growing type amid rising automation needs.

End-User Insights

The apparel industry represents the dominant segment, capturing approximately 52% of market revenue share in 2026, propelled by dynamic fashion trends and fast fashion expansion. Producers adopt advanced sewing machinery to satisfy surging needs for stylish, budget-friendly garments. They prioritize high output to match quick market cycles. Automation and computerized controls transform operations by sharpening efficiency and elevating output standards. Factories achieve faster cycle times with fewer defects, which strengthens their edge in competitive arenas. This reliance on cutting-edge tools ensures apparel makers scale production seamlessly amid rising consumer expectations.

Automotive industry is expected to be the fastest-growing segment over the 2026-2033 forecast period. Industrial sewing machines play a vital role in the automotive sector by crafting durable interior parts such as seats, airbags, and upholstery. Producers demand exact seams and robust construction to meet safety standards. This need pushes the adoption of sophisticated equipment that delivers consistent results under high stress. Emerging markets fuel segment growth as vehicle production ramps up worldwide. Factories seek reliable tools for complex assemblies. Innovations like automated stitching and multi-needle systems heighten output while trimming labor expenses. These advances position automotive applications for rapid expansion amid rising global demand.

Regional Insights

Asia Pacific Industrial Sewing Machines Market Trends

Asia Pacific is likely to be both the leading and fastest-growing regional market for industrial sewing machines in 2026, accounting for approximately 45% of the market share. Major hubs such as China, India, and Bangladesh host vast textile and apparel operations that export goods worldwide. Factories produce everything from basic garments to technical fabrics, which sustains high equipment demand. Low-cost labor keeps operations competitive, while governments offer incentives for factory expansions. Producers invest in machines to handle surging orders from international brands. Local suppliers thrive by delivering reliable tools tailored to regional needs. This concentration creates economies of scale that benefit machine makers.

The region will solidify its dominance through infrastructure upgrades and skill enhancements by decade's end. Policymakers promote clusters with modern facilities that integrate automation. Companies shift toward high-value outputs, such as performance wear and home textiles. Skilled workers adopt advanced systems that boost precision and speed. Trade agreements ease exports, drawing more foreign investment into production bases. Manufacturers explore sustainable practices to meet global standards. Suppliers respond with eco-friendly designs and financing options for upgrades. This evolution attracts premium clients and fosters innovation hubs.

Europe Industrial Sewing Machines Market Trends

Europe maintains a strong presence in the industrial sewing machinery market through its robust manufacturing foundation. Producers prioritize top-tier textile and leather goods, such as luxury apparel and automotive interiors. This focus spurs demand for sophisticated equipment with automated functions and digital interfaces. Countries such as Germany, Italy, and France lead with established factories and heavy investments in R&D. Companies craft machines that deliver exact seams and flawless finishes, which meet stringent client expectations. Skilled engineers refine designs to handle premium materials without compromise.

The region advances steadily as sustainability shapes future strategies. Makers develop energy-saving models and eco-conscious features that comply with strict environmental rules. Governments back green initiatives through grants for low-emission tech. Firms integrate recycled components and smart controls to cut waste during operations. Clients shift toward suppliers who align with carbon-neutral goals. This trend opens doors for hybrid systems that blend power with responsibility. Manufacturers gain loyalty by offering upgrades that extend machine life cycles. Europe will pioneer balanced growth that pairs innovation with planetary care.

North America Industrial Sewing Machines Market Trends

North America sustains a vital role in the industrial sewing machinery market through its cutting-edge production sites. Factories serve demands for technical textiles and automotive parts, such as reinforced upholstery and safety components. Operators rely on state-of-the-art equipment to achieve superior strength and uniformity in seams. The region excels in technological breakthroughs, where firms push automation boundaries with smart interfaces and robotic aids. Makers prioritize systems that link directly to digital factory floors for seamless oversight. This innovation culture draws clients who seek top performance in diverse applications. E-commerce surges reshape operations as brands ramp up output for online apparel sales.

Producers upgrade to high-speed units that handle varied orders with speed and care. Sustainability gains traction, with companies crafting energy-efficient designs and low-waste features. Governments offer rebates for green upgrades that lower emissions. Manufacturers integrate recyclable parts and power-saving motors to align with consumer values. Firms will master hybrid models that balance output with environmental care. Suppliers gain an edge by providing retrofit kits for older fleets. Clients favor vendors who deliver reliable, future-proof solutions. This blend of tech prowess and mindful practices fuels consistent progress.

Competitive Landscape

The global industrial sewing machines market structure is moderately consolidated, dominated by leading players such as JUKI Corporation, Brother Industries, Ltd., Jack Sewing Machine Co., Ltd., and Pegasus Sewing Machine Co., Ltd. These players collectively capture 45-55% of the market share. Companies drive the competitive landscape through relentless innovation and heavy investments in R&D. They launch advanced sewing machinery that boosts efficiency across production lines. IoT and AI integrations set key differentiators, enabling smart automation that tracks performance and cuts labor expenses.

Manufacturers gain an edge by delivering connected systems that predict issues and optimize workflows in real time. Firms also respond to varied industrial needs by crafting specialized models for unique stitching demands. This focus on tailored solutions strengthens market positions and meets client expectations in sectors such as apparel and automotive. Overall, these strategies fuel rivalry and propel industry progress.

Key Industry Developments

- In March 2026, Brother Industries completed its acquisition of Mutoh Holdings, integrating its imaging and CAD/CAM technologies to strengthen sewing and industrial printing capabilities. The move is expected to drive innovation in hybrid sewing machines with built-in printing and design features, enhancing product offerings and competitive positioning in the global manufacturing tools market.

- In January 2026, Hikari, a leading Chinese sewing machine manufacturer, launched its new generation of AI-powered intelligent sewing machines in Dhaka, Bangladesh, marking the first such rollout in the country. The event drew over 500 RMG industry representatives and highlighted features like smart thread tension control to boost garment production efficiency, cut costs, and simplify operations for factories.

- In October 2025, Sokkar Mecca, Egypt's official agent for China's JACK sewing machines, launched the AI-powered JACK A5E-B AMH2 model to advance the local garment industry. This machine features advanced stitching and a semi-dry motor for uninterrupted operation across various fabrics, boosting productivity and quality.

Companies Covered in Industrial Sewing Machines Market

- JUKI Corporation

- Brother Industries, Ltd.

- Jack Sewing Machine Co., Ltd.

- Dürkopp Adler GmbH

- Pegasus Sewing Machine Co., Ltd.

- PFAFF Industrial

- Singer

- Sunstar Co., Ltd.

- Zoje Sewing Machine Co., Ltd.

- Bernina International AG

- Union Special Corporation

- Siruba Machine Co., Ltd.

- Typical

- Toyota Industries Corporation

Frequently Asked Questions

The global industrial sewing machines market is projected to reach US$ 4.2 billion in 2026.

The market is driven by skyrocketing global demand for apparel, technical textiles, and automotive upholstery.

The market is poised to witness a CAGR of 5.2% from 2026 to 2033.

Major opportunities lie in IoT-enabled smart systems, AR/VR integration, and aftermarket services in Asia Pacific and near-shoring jurisdictions.

JUKI Corporation, Brother Industries, Ltd., Jack Sewing Machine Co., Ltd., and Pegasus Sewing Machine Co., Ltd. are some of the key players in the market.