- Electrical Equipment & Services

- Industrial Control Panel Market

Industrial Control Panel Market Size, Share, and Growth Forecast, 2026 – 2033

Industrial Control Panel Market by Component Type (Motor Controllers, Overload Relays, Fused Disconnect Switches, Circuit Breakers, and Control Devices), Form Type (Enclosed, Open), and Regional Analysis for 2026 – 2033

Industrial Control Panel Market Size and Trends Analysis

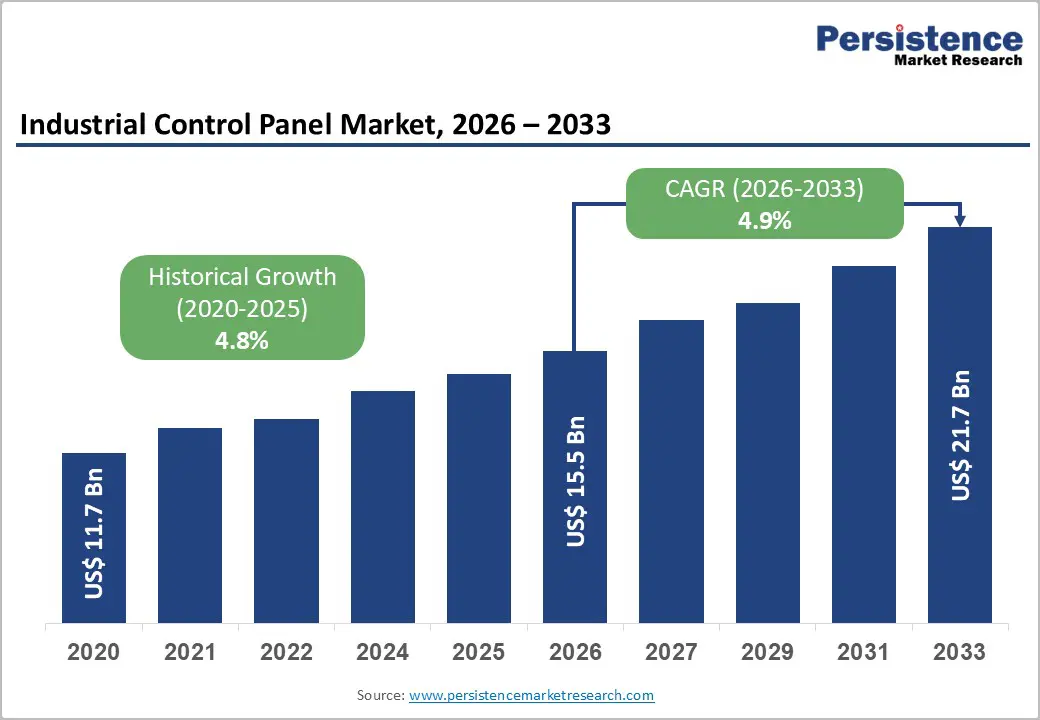

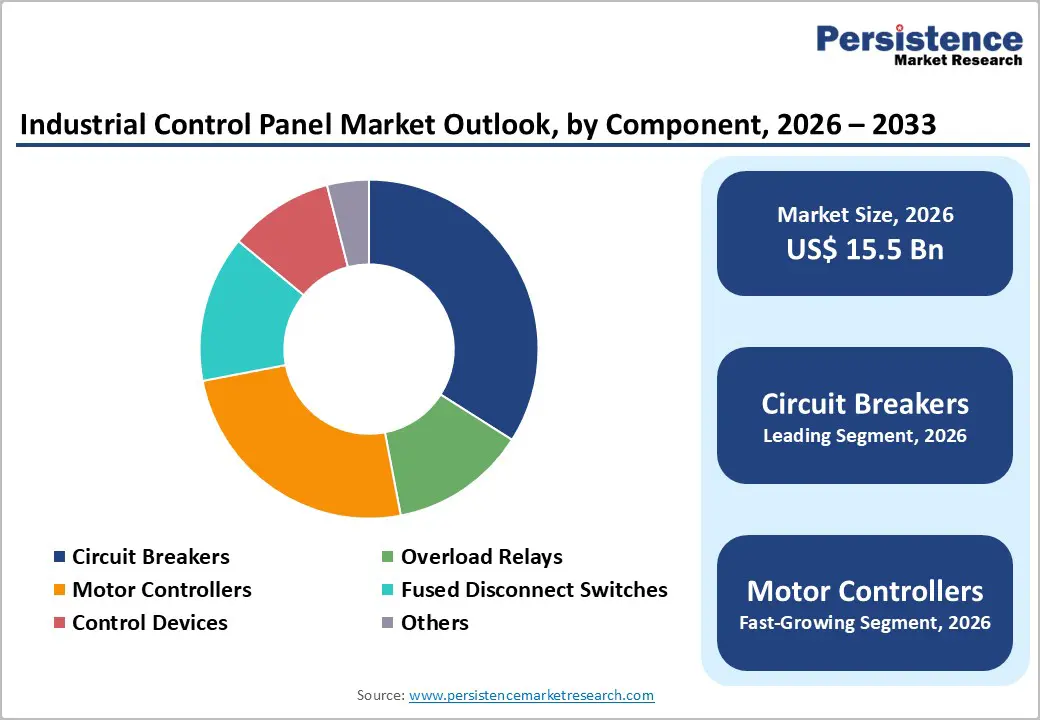

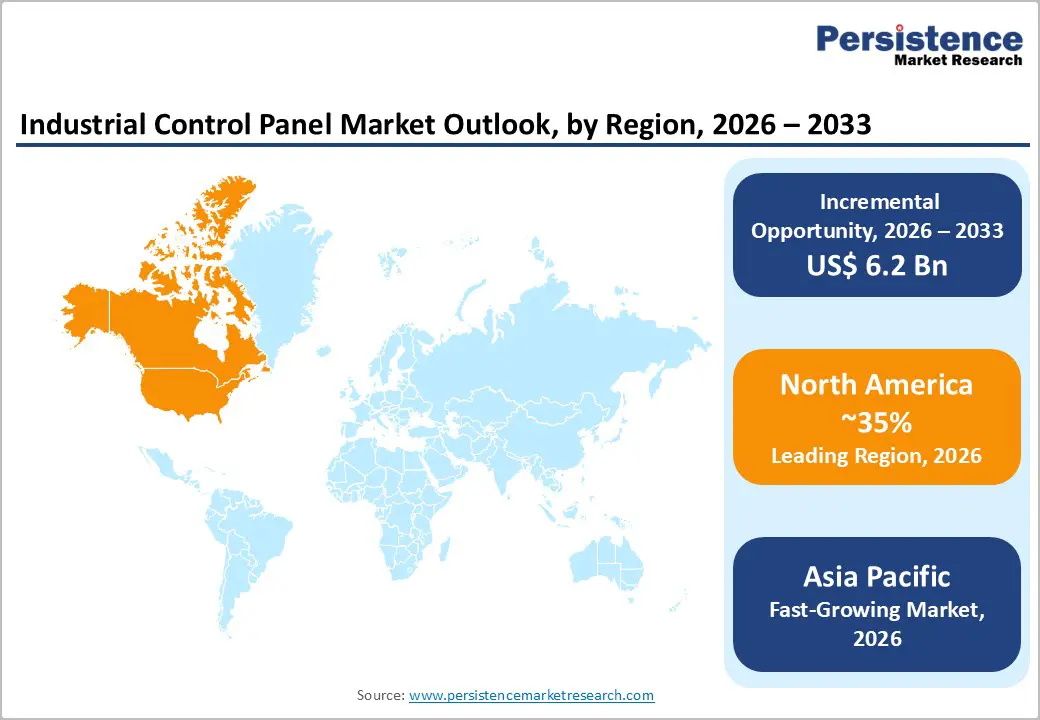

The global industrial control panel market size is likely to be valued at US$15.5 billion in 2026 and is expected to reach US$21.7 billion by 2033, growing at a CAGR of 4.9% during the forecast period from 2026 to 2033, driven by the continued adoption of industrial automation across manufacturing, energy, utilities, and process industries, where control panels are critical for operational reliability and safety.

Modernization efforts in infrastructure, especially within emerging economies, are driving the replacement of outdated electrical systems with advanced, standards-compliant control panels. Technological innovations, including compact designs, modular architectures, and enhanced component integration, are boosting system efficiency and minimizing downtime. Stringent regulatory and safety standards set by organizations such as the IEC and NEMA are also promoting both upgrades and new installations.

Key Industry Highlights:

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 35% in 2026, driven by strong automation adoption, strict safety regulations, and ongoing investments in smart manufacturing.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, driven by rapid industrialization, expanding manufacturing capacity, and strong government support for automation across key economies.

- Leading Component Type: Circuit breakers are projected to represent the leading component type in 2026, accounting for 30% of the revenue share, due to mandatory safety and overcurrent protection requirements.

- Leading Form: Enclosed control panels are anticipated to be the leading form type, accounting for over 60% of the revenue share in 2026, supported by superior protection against environmental hazards, enhanced safety compliance, and adherence to NEMA and IP standards.

| Key Insights | Details |

|---|---|

| Industrial Control Panel Market Size (2026E) | US$15.5 Bn |

| Market Value Forecast (2033F) | US$21.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Adoption of Industrial Automation and the Growing Demand for Advanced Control Panels

Manufacturers and process industries strive for higher productivity, precision, and operational efficiency; automated systems have become essential. Industrial control panels serve as the central hub for automation, integrating programmable logic controllers (PLCs), sensors, relays, motor controllers, and circuit breakers to monitor and control machinery. Automation reduces human intervention, minimizes errors, and ensures consistent output quality, which is critical in sectors such as automotive, pharmaceuticals, food and beverage, and electronics. The ongoing shift toward smart factories has increased the demand for advanced control panels capable of supporting real-time data monitoring, remote operation, and predictive maintenance.

The rising adoption of industrial automation is particularly pronounced in emerging economies across the Asia Pacific, where rapid industrialization, urbanization, and cost-effective manufacturing have created significant demand for advanced control solutions. Countries such as China, India, and Japan are investing in automation technologies to improve productivity, reduce labor costs, and maintain competitiveness. Industrial control panels in these regions are increasingly integrated with smart sensors, IoT connectivity, and AI-driven analytics, enabling real-time monitoring, predictive maintenance, and optimized energy consumption. Opportunities for retrofitting and upgrading existing manufacturing facilities contribute to market growth, as companies replace outdated panels with more reliable, modular, and compact designs.

Cybersecurity Vulnerabilities

Modern industrial control panels are often integrated with IoT devices, SCADA systems, cloud-based monitoring, and remote access features, making them susceptible to cyberattacks. Threats such as malware, ransomware, and unauthorized intrusions can disrupt industrial operations, damage critical equipment, and compromise sensitive operational data. Industries such as power generation, oil & gas, manufacturing, and water treatment are especially vulnerable as control panels manage essential processes, and any breach could lead to production downtime, safety hazards, financial losses, and regulatory penalties. With industrial processes becoming more digitized, the attack surface for cybercriminals expands, forcing companies to re-evaluate their automation strategies.

Addressing cybersecurity vulnerabilities increases the implementation and operational costs of industrial control panels, creating a financial restraint on market growth. Companies must invest in advanced security measures such as firewalls, intrusion detection systems, encrypted communication protocols, and secure authentication to protect sensitive equipment and data. Small and medium-sized enterprises often face challenges in adopting such measures due to limited budgets and insufficient cybersecurity expertise, which may delay modernization and the adoption of smart or connected panels. Frequent security audits, compliance checks, and updates are required to maintain system integrity, increasing maintenance overheads and reducing the attractiveness of fully automated solutions for some organizations.

Emerging Markets and Infrastructure Development

Countries, including China, India, Brazil, and Saudi Arabia, are experiencing extensive development in sectors such as power generation, renewable energy, water treatment, transportation, and manufacturing, all of which require advanced control systems for reliable operations. Industrial control panels, which centralize the management and monitoring of equipment, play a vital role in these automated and semi-automated industrial processes. Rising investments in smart infrastructure projects, including industrial parks, smart grids, and automated manufacturing facilities, are increasing demand for modular, energy-efficient, and IoT-enabled panels.

Infrastructure development in emerging economies not only creates opportunities for new installations of industrial control panels but also for retrofitting and upgrading legacy systems. Many industries in developing regions still rely on outdated or manually operated control systems, which often fail to meet modern efficiency, safety, and regulatory standards. The replacement of these legacy systems with advanced, modular, and digitally connected panels provides opportunities for manufacturers to offer scalable, flexible, and standardized solutions. Sectors such as renewable energy, electric vehicle manufacturing, and industrial automation facilities are particularly investing in smart control panels that support predictive maintenance, remote monitoring, and real-time operational analytics.

Category-wise Analysis

Component Type Insights

The circuit breakers segment is projected to dominate the industrial control panel market, accounting for approximately 30% of the total revenue share in 2026, owing to its essential role in ensuring safety and protecting power systems. Circuit breakers prevent overcurrent conditions, protect equipment from damage, and ensure operational continuity in industrial settings. Regulatory standards from organizations such as UL and IEC mandate proper overcurrent protection, reinforcing the essential role of circuit breakers in industrial systems. For example, Siemens’ 3VA molded case circuit breakers are widely used in manufacturing plants to safeguard electrical systems while supporting efficient load management. Industries such as automotive, pharmaceuticals, and heavy machinery rely on circuit breakers to maintain safety and prevent costly downtime.

Motor controllers are likely to represent the fastest-growing segment in 2026, driven by rising automation adoption and the use of variable frequency drives (VFDs). Motor controllers regulate the operation of industrial motors, ensuring precise speed, torque, and direction control while optimizing energy consumption. As industries expand and modernize their manufacturing facilities, demand for efficient motor management rises significantly. For example, Schneider Electric’s Altivar variable frequency drives are integrated with motor controllers to enhance operational efficiency and reduce energy costs in production lines. Sectors such as food processing, packaging, and automotive assembly increasingly rely on motor controllers to automate complex processes, improve productivity, and maintain consistent quality.

Form Insights

The enclosed form segment is expected to dominate the market, capturing around 60% of the total revenue share in 2026, driven by its superior protection against environmental hazards and enhanced safety features. Enclosed panels guard against dust, moisture, and accidental contact with live components, ensuring reliable performance in harsh industrial environments. Standards from organizations such as NEMA and IP ratings support the preference for enclosed designs, particularly in industries with stringent safety and environmental requirements. For instance, Rittal's TS 8 enclosed control panels are commonly used in chemical plants and energy facilities to safeguard sensitive electrical components from corrosion, humidity, and mechanical damage. Enclosed panels are particularly vital in sectors such as oil & gas, water treatment, and heavy manufacturing, where exposure to environmental risks is a constant concern.

The open form segment is projected to be the fastest-growing, driven by its flexibility, lower initial costs, and suitability for controlled environments. Open panels offer easier customization, expansion, and maintenance, making them ideal for applications where environmental hazards are minimal and cost efficiency is a priority. For example, Omron's open-style control panels are often used in electronics assembly and small-scale manufacturing, where quick reconfiguration and integration of additional components are essential. The growth of the open-panel segment is particularly driven by smaller and medium-sized enterprises seeking to reduce initial investment while maintaining operational control and automation efficiency.

Regional Insights

North America Industrial Control Panel Market Trends

North America is anticipated to be the leading region, accounting for a market share of 35% in 2026, driven by the resurgence of manufacturing and industrial automation across the region. The U.S. and Canada are investing heavily in modernizing production facilities, upgrading legacy systems, and integrating Industry 4.0 technologies. Automation adoption, including PLC-controlled machinery, motor controllers, and smart sensors, is increasing operational efficiency, reducing downtime, and improving safety compliance. Regulatory frameworks such as UL 508A and NFPA 79 ensure that control panels meet stringent safety and performance standards, increasing demand for high-quality solutions. The growth is also supported by industries such as automotive, pharmaceuticals, food & beverage, and aerospace, which require reliable and modular control panels to support complex production lines and critical process operations.

Technological innovation is another major trend shaping the North American market. Manufacturers are increasingly adopting IoT-enabled, smart, and modular control panels to enable real-time monitoring, predictive maintenance, and energy optimization. For example, companies such as Rockwell Automation are leveraging these innovations by providing integrated solutions such as Allen-Bradley control panels, which combine advanced PLCs, motor drives, and connectivity features for smart manufacturing. The market is seeing increased focus on cybersecurity, data analytics, and remote monitoring, reflecting the region’s emphasis on operational reliability and industrial safety.

Europe Industrial Control Panel Market Trends

Europe is likely to be a significant market for industrial control panels in 2026, driven by widespread adoption of Industry 4.0 technologies and automation initiatives across manufacturing and process industries. Countries such as Germany, France, and the U.K. are at the forefront of industrial modernization, integrating advanced control systems to enhance operational efficiency, safety, and energy management. The market is fueled by investments in smart factories, renewable energy projects, and automated production lines, which require reliable and modular industrial control panels. Regulatory compliance with standards such as IEC 61439 and EN 60204-1 ensures safety, operational reliability, and protection of personnel and equipment.

Technological advancements are shaping Europe’s market trends, particularly the adoption of IoT-enabled, digitalized, and modular control panels for enhanced monitoring, predictive maintenance, and integration with enterprise systems. For example, Companies such as Siemens AG are leveraging these innovations by providing solutions such as Sirius control panels, which combine PLCs, motor starters, and smart connectivity to support automated and energy-efficient manufacturing. European manufacturers are also emphasizing cybersecurity, energy efficiency, and compact designs, reflecting the regulatory and operational priorities of the region.

Asia Pacific Industrial Control Panel Market Trends

The Asia Pacific region is likely to be the fastest-growing region in 2026, driven by accelerated industrialization, urbanization, and manufacturing expansion in countries such as China, India, Japan, and South Korea. Rising investments in smart manufacturing, renewable energy projects, and infrastructure development are increasing the demand for reliable and efficient control panels. Asia Pacific is the fastest-growing regional market as industries modernize legacy systems and implement automation technologies to improve operational efficiency, reduce downtime, and ensure consistent product quality. Regulatory emphasis on safety, environmental compliance, and energy efficiency encourages the adoption of NEMA- and IEC-compliant panels, particularly in high-growth sectors such as automotive, electronics, food & beverage, and pharmaceuticals.

Technological innovation is a key trend shaping the Asia Pacific market. Industrial control panels are increasingly IoT-enabled, modular, and digitally connected, allowing real-time monitoring, predictive maintenance, and seamless integration with enterprise systems. For example, Companies such as Mitsubishi Electric Corporation provide advanced solutions, such as MelIPC control panels, that integrate PLCs, motor drives, and intelligent sensors to optimize manufacturing processes. The focus on energy efficiency, compact designs, and remote monitoring capabilities drives adoption in both developed and emerging economies in the region.

Competitive Landscape

The global industrial control panel market exhibits a moderately fragmented structure, driven by the presence of several large multinational automation and control systems providers alongside numerous regional specialists. Although no single company dominates outright, the industry’s top-tier vendors collectively account for a significant portion of overall revenue, reflecting a balance between established global players and agile, smaller firms focused on specialized solutions. This competitive landscape is shaped by ongoing technological innovation, strategic partnerships, and expansion into adjacent automation services, as companies strive to meet diverse industrial demands for safety, efficiency, and connectivity.

With key leaders including Siemens AG, ABB Ltd., Schneider Electric SE, Rockwell Automation, and Emerson Electric Co., the competitive field is anchored by firms that deliver broad control panel portfolios integrated with automation, IIoT, and predictive maintenance functionalities. These players compete through continuous product innovation, acquisitions, strategic collaborations, and geographic expansion, enhancing capabilities in smart manufacturing and energy?efficient solutions while addressing cybersecurity and compliance needs.

Key Industry Developments:

- In July 2025, Delta, a global leader in power and smart green solutions, launched the DOP-300S Series Touch Panel HMI, targeting the growing demand for smart manufacturing and Industrial Internet of Things (IIoT) applications. The new HMI series features 7-inch and 10-inch TFT LCDs, a high-performance dual-core ARM-based CPU, and native support for MQTT and OPC UA protocols, enabling seamless connectivity and real-time data exchange. With optional Wi-Fi and built-in 4G connectivity, the DOP-300S Series enhances cloud integration and remote monitoring without requiring additional hardware, making deployment cost-effective for manufacturers. The solution supports DIACloud and DIAWebDesigner, allowing secure data aggregation, customized dashboards, and remote visualization for improved operational efficiency.

- In November 2025, AAEON, a leading provider of industrial PC solutions, launched the NIKY-2155-NX AI Panel PC, expanding its portfolio for smart retail and industrial HMI applications. Powered by the NVIDIA Jetson Orin NX module, the new AI Panel PC enables advanced on-device AI processing for use cases such as smart kiosks, self-checkout systems, and intelligent industrial control interfaces. The system features a 15.6-inch full HD TFT-LCD touchscreen and a robust industrial-grade design suitable for demanding environments. The NIKY-2155-NX offers comprehensive industrial I/O connectivity, including multiple USB ports, dual Gigabit Ethernet, CANBus, RS-232/422/485, and digital I/O support, ensuring compatibility with both modern and legacy equipment.

Companies Covered in Industrial Control Panel Market

- Siemens AG

- Schneider Electric SE

- ABB Ltd.

- Rockwell Automation, Inc.

- General Electric Company

- Honeywell International Inc.

- Mitsubishi Electric Corporation

- Eaton Corporation Plc

- Omron Corporation

- Emerson Electric Co.

- Yokogawa Electric Corporation

- Fuji Electric Co., Ltd.

- Rittal GmbH & Co. KG

- Legrand SA

- Phoenix Contact GmbH & Co. KG

- Panasonic Corporation

- Toshiba Corporation

- WEG SA

Frequently Asked Questions

The global industrial control panel market is projected to reach US$15.5 billion in 2026.

The growing adoption of industrial automation, smart manufacturing, and the modernization of infrastructure across manufacturing and process industries are the key drivers of the market.

The industrial control panel market is expected to grow at a CAGR of 4.9% from 2026 to 2033.

Key opportunities include the rapid industrialization in emerging economies, the modernization of infrastructure, and the increasing adoption of smart, IoT-enabled control panels for Industry 4.0 applications.

Siemens AG, Schneider Electric SE, ABB Ltd., Rockwell Automation, Inc., and General Electric Company are the leading players.