- Hardware & Software IT Services

- India Fintech Market

India Fintech Market Size, Share, and Growth Forecast, 2026 - 2033

India Fintech Market by Service (Payment, Lending, Banking, Insurance, RegTech, Wealth Management and Investment, Personal Finance / Financial Planning, Others), Technology (AI & ML, Blockchain, Robotic Process Automation (RPA), API, Others), End-user, and Regional Analysis for 2026 - 2033

India Fintech Market Size and Trends

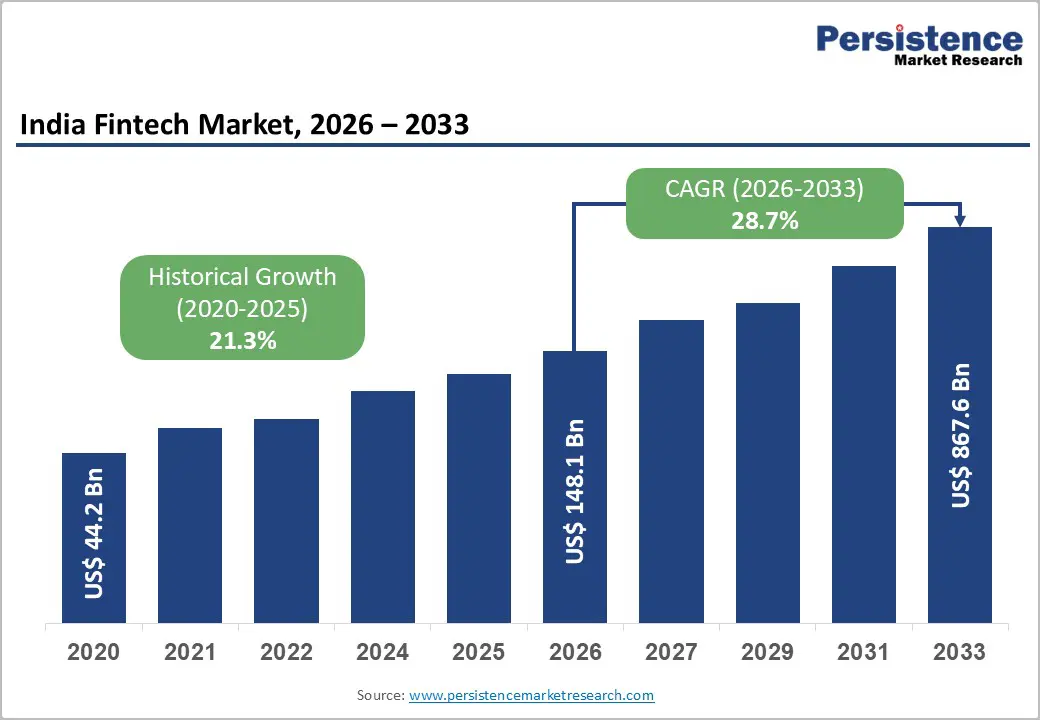

The India fintech market size is projected to rise from US$148.1 billion in 2026 to US$867.6 billion by 2033. It is anticipated to witness a CAGR of 28.7% during the forecast period from 2026 to 2033, driven by the growing need for financial inclusion and access to digital financial services among underbanked populations, micro, small, and medium enterprises (MSMEs), and tech-savvy consumers.

Rising smartphone penetration, increasing internet connectivity, and government initiatives enabling seamless adoption of digital payments, digital lending, and AI-powered financial solutions. The proliferation of UPI, PoS terminal-based lending, and co-lending models is further accelerating access to instant credit and working capital for businesses.

Key Industry Highlights:

- Leading Service: Payment solutions capture more than 39% market share in 2026, valued at over US$ 57.8 Bn, driven by the rise of UPI, mobile banking, and peer-to-peer transfers. Consumers and businesses increasingly rely on seamless, secure, and instant payment platforms, while QR code adoption and app integrations further fuel transaction volumes. Lending demonstrates the highest growth due to increased demand for quick, accessible credit among individuals, MSMEs, and small businesses.

- Leading Technology: AI & ML hold over 36% market share in 2026, valued at US$ 53.3 Bn, supporting real-time fraud detection, automated credit scoring, personalized investment advice, and enhanced customer support via chatbots and virtual assistants. Blockchain is expected to grow at the highest rate with a CAGR of 33.5%, enabling secure, traceable, and efficient transactions, decentralized lending, cross-border payments, and digital identity verification.

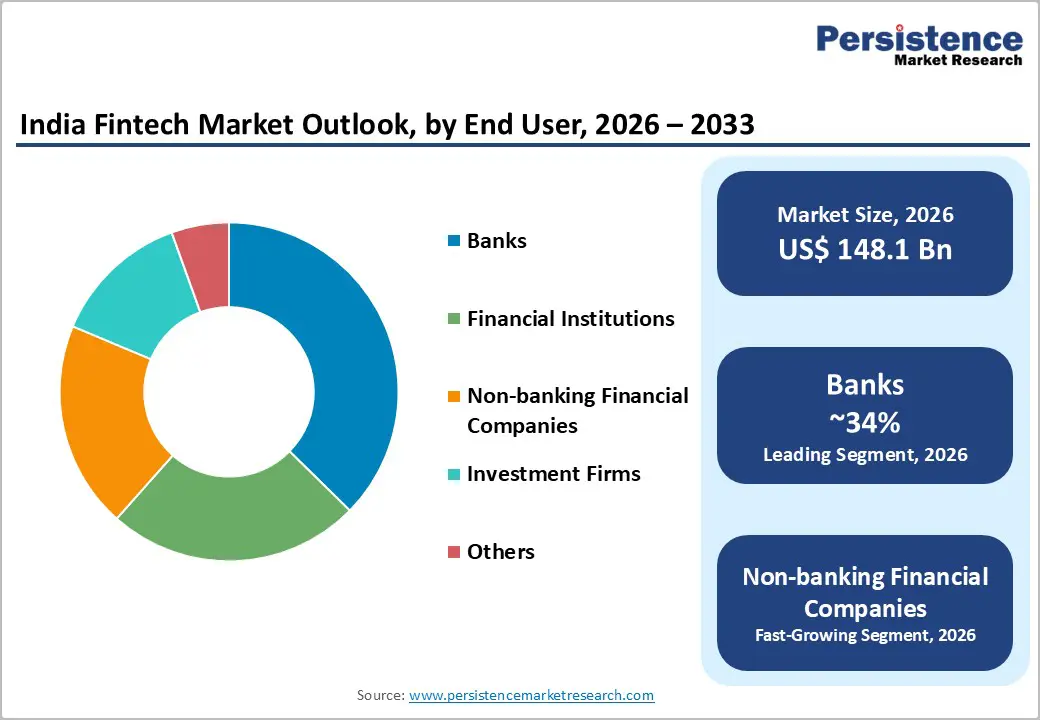

- Leading End-user: Banks command the largest market share at over 34% in 2026, valued at more than US$ 50.4 Bn, leveraging trust, extensive customer bases, and regulatory compliance to provide integrated digital financial services through mobile apps, UPI, and embedded finance. Non-banking financial companies (NBFCs) are expected to grow at the highest rate, addressing urgent financial needs with tech-driven lending solutions, instant loans, buy-now-pay-later options, and inclusive financial services for underserved populations.

| Key Insights | Details |

|---|---|

| India Fintech Market Size (2026E) | US$148.1 Bn |

| Market Value Forecast (2033F) | US$867.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 28.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 21.3% |

Market Dynamics

Driver - Surge Digital Payments Adoption and UPI Growth

UPI’s transaction volume has grown exponentially, facilitating billions of transactions per year and enabling secure, real-time payments across merchant and peer-to-peer use cases. The proliferation of UPI as the dominant payment rail has revolutionized transactions in India, accounting for 85% of digital payment volumes in H1 2025, according to RBI data, up from 9% in 2019. The UPI system now serves 491 million individuals and 65 million merchants. Seamless integration with apps like PhonePe and Google Pay has boosted adoption, while QR code usage grew 91.5% to 658 million, further enhancing merchant acceptance and consumer habituation. This, in turn, drives fintech revenues from payment gateways and value-added services, underpinning sustained ecosystem growth amid urbanization and the e-commerce boom.

Expansion of PoS Terminal-Based Lending and Co-Lending Models

The rise of PoS terminal-based lending and co-lending partnerships is significantly accelerating fintech growth. PoS-based lending enables merchants to access instant credit directly at the point of sale, with over 11 million active PoS devices, facilitating frictionless working capital loans for SMEs and micro-entrepreneurs. Co-lending models, guided by RBI regulations, allow banks to share loan capital with fintech firms that handle origination, underwriting, and customer engagement. This collaboration reduces risk, accelerates credit disbursement, and expands financial services to underbanked populations. Platforms such as Pine Labs Pvt. Ltd., BharatPe, and Lendingkart Finance Ltd. are leveraging these models to improve credit accessibility, increase transaction volumes, and strengthen financial inclusion across Tier-2 and Tier-3 cities.

Restraint - Regulatory and Compliance Complexity

Government policies have largely been supportive, but the fintech sector also faces challenges related to regulatory compliance. Proposals such as market share caps on UPI transactions have generated uncertainty among operators and influenced competitive dynamics. For example, delays in enforcing transaction caps were implemented to balance concerns about market concentration and ensure competitive fairness. Such regulatory uncertainty deters investments and long-term planning. Navigating India’s layered regulatory frameworks, which require adherence to RBI guidelines, the Digital Personal Data Protection Act, and cybersecurity standards, slows down product launches or expansions, especially for smaller or emerging players.

Cybersecurity and Data Privacy Risks

With the proliferation of digital payments, associated cybersecurity risks have expanded significantly. Digital transactions generate vast volumes of sensitive financial and personal data, increasing the potential for fraud, data breaches, and identity theft. While authorities such as the RBI and NPCI mandate robust data protection and fraud-detection protocols, the evolving threat landscape demands continuous investment in cybersecurity infrastructure. Concerns over data privacy and surveillance have also emerged, impacting user trust and necessitating greater transparency and secure data-handling practices.

Opportunity - Growth in Embedded Finance and Financial Inclusion

Embedded finance models, which integrate financial services directly into non-financial platforms and ecosystems, offer significant opportunities for fintech companies. These models allow businesses to provide credit, payments, insurance, or investment services alongside digital experiences, improving customer engagement and reducing friction in financial decisions. With a large and growing digital user base, the adoption of embedded finance in India is poised to accelerate, particularly across sectors such as e-commerce, logistics, and travel. There is increased focus on extending services to Tier-2 and Tier-3 cities, where digital penetration is rising but formal financial access remains limited. By enabling seamless financial interactions across third-party ecosystems, fintech operators capture new user segments and generate diversified revenue streams.

Expansion of Digital Lending and AI-Enabled Financial Services

Digital lending platforms are rapidly gaining traction due to unmet credit demand among individuals, micro, small, and medium enterprises (MSMEs), and underbanked sectors. Fintech firms are deploying advanced analytics and AI-powered solutions in financial services to streamline credit scoring, reduce loan turnaround times, and customize loan products based on user behavior and risk profiles. According to a study, fintech NBFCs have sanctioned record volumes of personal loans, deepening access to formal credit channels traditionally bypassed by conventional lenders. By automating credit risk assessment and leveraging alternative data sources, AI-enabled lending solutions enhance financial inclusion while managing credit risk more effectively.

Category-wise Analysis

Service Insights

Payment capturing more than 39% market share in 2026 with a value exceeding US$ 57.8 Bn, as they address the core need for fast, convenient, and secure transactions in daily life. With the rise of digital commerce, mobile banking, and peer-to-peer transfers, individuals and businesses increasingly rely on seamless payment platforms. The need to manage bills, subscriptions, and online shopping efficiently drives widespread adoption. Contactless and real-time payment options fulfill the growing demand for instant financial accessibility and financial inclusion across urban and rural areas.

Lending demonstrates the highest growth due to individuals and small businesses increasingly need quick, accessible credit for consumption, working capital, and expansion. Traditional banks often have lengthy approval processes, while fintech platforms offer instant loans with minimal documentation. Rising digital adoption, smartphone penetration, and UPI-based transactions make it easier for borrowers to access personalized credit. Consumers also prefer flexible repayment options and credit tailored to their income cycles, fueling demand for digital lending solutions.

Technology Insights

AI & ML hold over 36% market share in 2026, with a value exceeding US$ 53.3 Bn, due to the need for faster, smarter, and more personalized financial services. Consumers and businesses demand real-time fraud detection, automated credit scoring, and tailored investment advice. AI-driven chatbots and virtual assistants improve customer support, while ML models enhance risk management and predictive analytics. The push for efficiency, accuracy, and convenience in transactions and financial decision-making makes these technologies indispensable.

Blockchain is expected to grow at the highest rate, with a CAGR of 33.5%. With digital payments, lending, and remittances rising, blockchain addresses fraud, reduce settlement times, and ensure traceability. Its decentralized nature also supports trust in peer-to-peer lending, cross-border payments, and digital identity verification. As fintech adoption expands, the need for efficiency, security, and regulatory compliance drives blockchain’s rapid integration across services.

End-user Insights

Banks command the largest market share at over 34% in 2026, with a value exceeding US$ 50.4 Bn. They are the primary providers of financial services; their extensive customer base, trust, and regulatory compliance make them the go-to source for digital financial solutions. Consumers and businesses increasingly demand seamless, secure, and integrated digital experiences, which banks are uniquely positioned to offer through mobile apps, UPI, and embedded finance. Banks’ ability to leverage data for personalized offerings meets the growing need for convenience, speed, and tailored financial services.

Non-banking financial companies are expected to grow at the highest rate as they fulfill urgent financial needs that traditional banks often cannot. They offer quick, flexible credit and digital lending solutions for individuals and small businesses, addressing gaps in access to capital. With rising consumer demand for instant loans, buy-now-pay-later options, and convenient online financial services, NBFCs meet the need for speed, accessibility, and tailored credit products. Their tech-driven platforms also make financial services more inclusive for underserved segments across urban and rural areas.

Competitive Landscape

India fintech market exhibits a moderately consolidated structure, with a mix of large platforms and a vibrant landscape of emerging startups. Key players like PhonePe Pvt. Ltd., Google Pay, and PayPal capture considerable transaction volumes in payments, while lending specialists and digital broking platforms compete on service depth and customer engagement. Market leaders differentiate through customer-centric app experiences, regulatory compliance, and strategic alliances with banks and NBFCs.

Key Industry Developments

- In September 2025, PhonePe received final approval from the Reserve Bank of India (RBI) to operate as an online payment aggregator. This authorization allows the company to expand its services, particularly targeting small and medium businesses across India, offering secure and reliable payment solutions.

- In February 2025, Razorpay unveiled four industry-first innovations at its FTX event, including RazorpayX Corporate Cards for startup founders, India’s first Buyer Protection program, the AI-powered RAY Agentic toolkit, and Engage Gift Cards. These solutions aim to simplify payments, enhance financial intelligence, and strengthen customer trust, empowering businesses to scale efficiently and innovate seamlessly.

Companies Covered in India Fintech Market

- PhonePe Pvt. Ltd.

- Pine Labs Pvt. Ltd.

- Zerodha Broking Ltd.

- Razorpay Payments Private Limited

- MobiKwik

- CRED

- One97 Communications Ltd.

- PB Fintech Limited

- BharatPe

- Lendingkart Finance Ltd.

- Google Pay

- PayPal

- Others

Frequently Asked Questions

India Fintech market is projected to be valued at US$148.1 Bn in 2026.

The need for financial inclusion, faster digital payments, and accessible credit is key driver of the market.

India Fintech market is expected to witness a CAGR of 28.7% from 2026 to 2033.

The expanding digital lending, AI-powered financial services, embedded finance, and underserved segments like micro, small, and medium enterprises (MSMEs) are creating strong growth opportunities.

PhonePe Pvt. Ltd, Pine Labs Pvt. Ltd., Zerodha Broking Ltd., Razorpay Payments Private Limited, MobiKwik, CRED, One97 Communications Ltd. are among the leading key players.