- Home Care & Utilities

- India Cookware Market

India Cookware Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

India Cookware Market by Product Type (Pots & Pans, Pressure Cookers, Cookware Sets, Kadai & Woks, Tawas & Griddles, Bakeware, Specialty/Traditional Cookware, Others), Material (Stainless Steel, Cast Iron, Carbon Steel, Aluminum, Glass, Stoneware, Others), End-user (Residential Household, Commercial/HoReCa), and Regional Analysis for 2026 - 2033

India Cookware Market Trends & Analysis

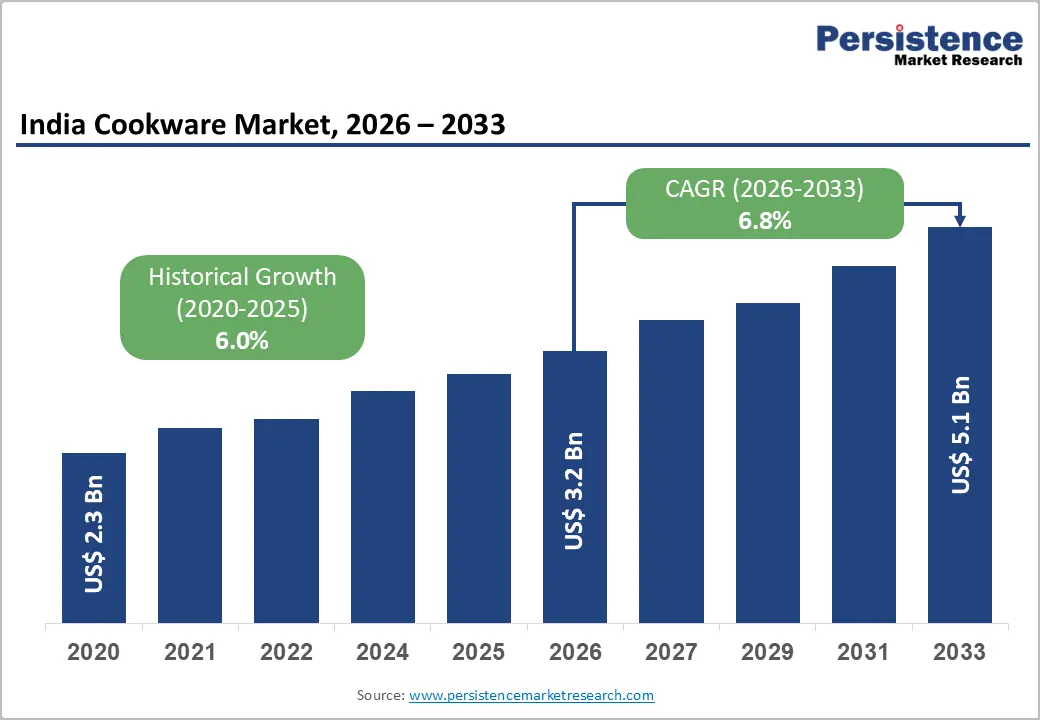

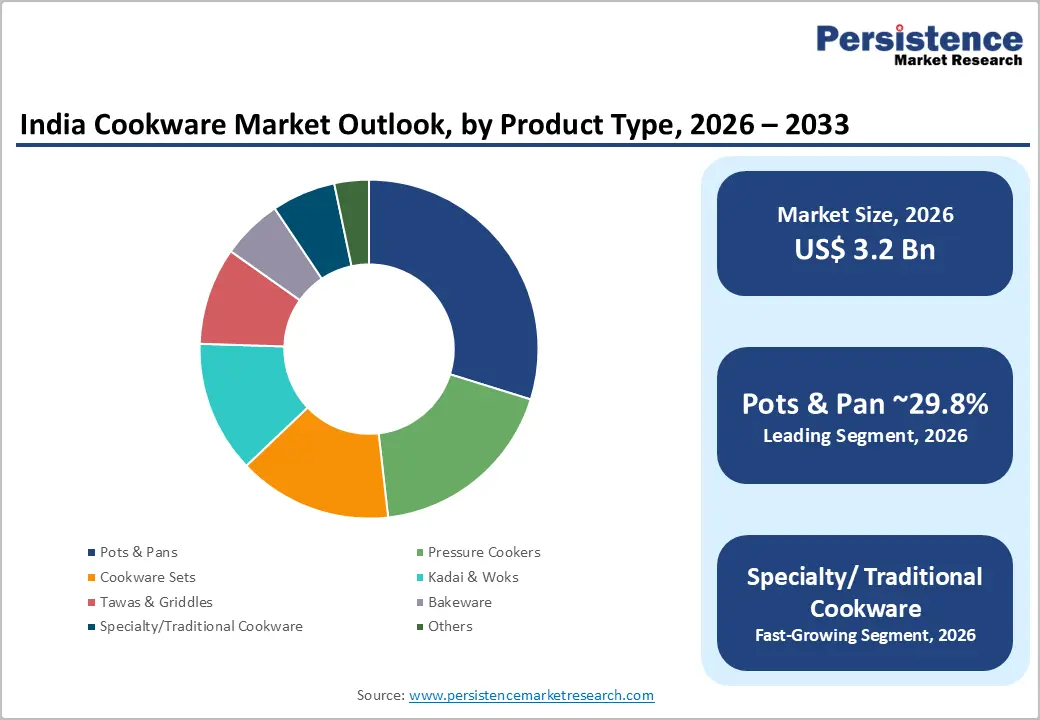

The India cookware market size is projected at US$ 3.2 billion in 2026 and is projected to reach about US$ 5.1 billion by 2033, growing at a CAGR of 6.8% between 2026 and 2033. The rise in disposable incomes, nuclear household formation and rapid adoption of non-stick and specialty cookware. Stainless steel remains the volume leader with around 35% share in 2025, while cast iron and specialty/traditional formats are projected to outpace the average market growth by around 7.9% CAGR by 2033.

Key Industry Highlights:

- Product & Material Leaders: Core cookware accounts for about 73.6% of market share, with pots & pans leading at 29.8%, while stainless steel holds roughly 33.9% share and remains the dominant material; at the same time.

- Leading Product: Non-stick cookware is forecast to grow at around 6.9% CAGR to 2030. Popularity and positive consumer mindset for non-stick cookware attracts growth.

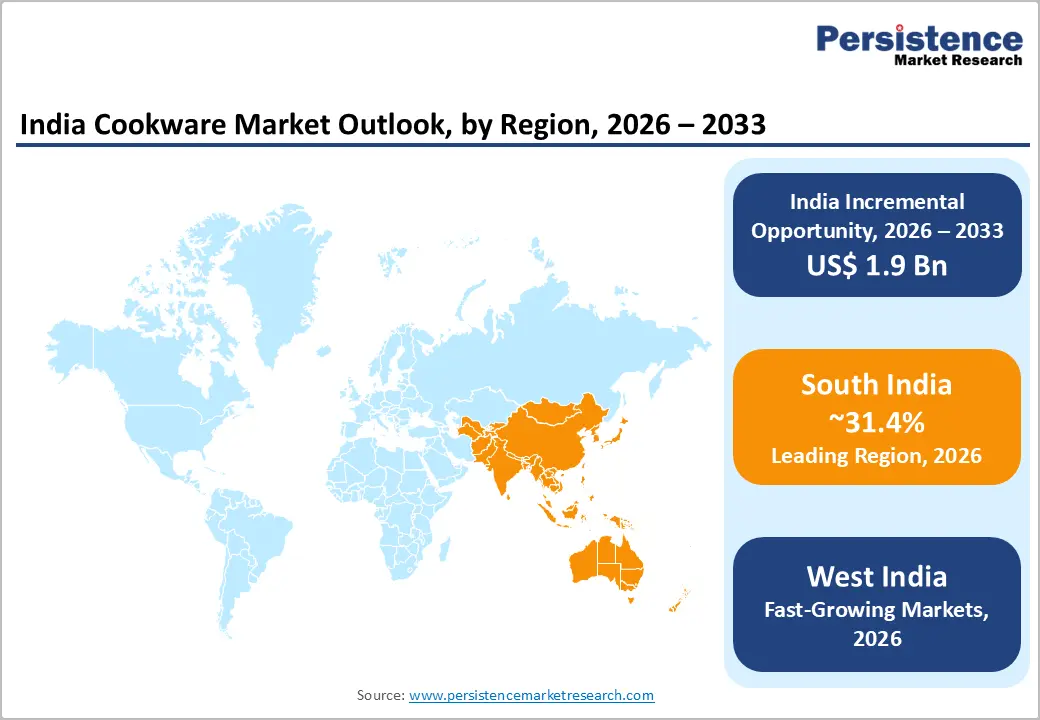

- Regional Performance: South India leads with approximately 31.4% share and the highest CAGR (about 7.6%), backed by manufacturing hubs and higher per-capita spend; North India holds around 28.7% share, and West India has about 23.7% share with roughly 7.0% CAGR, leveraging strong manufacturing and urban demand.

- Regulatory & Quality: BIS standards IS 1660:2009 for aluminium utensils and IS 14756:2022 for stainless steel cookware, along with associated QCOs, reinforce quality and safety, favouring organized players that invest in compliance and testing over unorganized or sub-standard products.

- Strategic Investments: Borosil’s plan to invest INR 250 crore and target INR 7,000 crore revenue, and TTK Prestige’s multi-plant, 620+-store network, highlight ongoing capacity, product and retail expansion, while non-stick and cast-iron growth rates signal sustained innovation in coatings and materials.

- Premiumization & Rural Penetration: Rise in non-stick penetration (over 70% for frying pans) and the spread of exclusive brand stores and e-commerce into Tier-2/3 and rural markets underpin premiumization, creating sizeable opportunities for branded cookware to capture share from unorganized vendors.

Market Dynamics Analysis

Drivers - Health, Safety and Regulatory Standards

Consumer awareness of material safety and longevity is rising, aided by the Bureau of Indian Standards (BIS) and Quality Control Orders (QCOs) covering stainless steel and aluminium cookware. BIS mandates certification for wrought aluminium utensils under IS 1660:2009, specifying requirements for thickness, corrosion resistance, and non-stick coating quality, with tests for visual defects, adhesion and salt-water corrosion resistance. For stainless steel cookware, the introduction of IS 14756:2022 reinforces confidence in steel grades free from harmful admixtures and ensures performance in everyday cooking.

Such standards help differentiate organized, compliant brands from unorganized or counterfeit products, particularly in mass-market stainless steel and aluminium segments. Research confirms that stainless steel and are likely to hold about 35.9% share of India's cookware value in 2026, owing to their durability, safety, and compatibility with Indian cooking styles. As QCO enforcement becomes stricter, branded players that invest in testing, certification and traceability gain an edge in both urban and rural markets, reinforcing stainless steel’s leadership (33.7% share) while enabling premiumization into tri-ply and encapsulated-base formats.

Restraints - Large Unorganized Sector and Counterfeit / Sub-standard Products

A significant portion of cookware sales, particularly basic aluminium and low-grade stainless steel utensils, still flows through the unorganized sector, where products may not conform to BIS standards. The presence of sub-standard non-stick coatings and thin-gauge metals can erode consumer confidence and depress pricing in lower-tier markets, challenging organized brands trying to maintain quality and margins. While BIS certification is mandatory for certain categories, enforcement gaps and limited consumer awareness in rural regions limit the immediate impact, constraining premiumization in some segments.

Competition from low-cost imports and adjacent categories

Cookware faces competition from low-cost imported products, particularly in glassware, steel and non-stick categories, as well as from adjacent kitchen appliances such as air-fryers and multi-cookers. Borosil’s management, for instance, notes intense competition from low-priced Chinese solar glass, and similar pricing pressure is seen in kitchen categories where imported products can undercut domestic players. These competitive dynamics can limit price increases, slow category upgrades and force brands to invest heavily in marketing and innovation to differentiate, thereby compressing short-term profitability.

Opportunities - HoReCa expansion and institutional kitchens

The commercial/HoReCa (hotels, restaurants, cafés, institutional kitchens) segment is projected as the fast-growing end-user at a positive CAGR, supported by India’s expanding food-service industry and rising organized dining. National restaurant and QSR chains, cloud kitchens, corporate cafeterias and institutional caterers require standardized, durable, often induction-compatible cookware and bakeware, with replacement cycles driven by heavy usage. This segment tends to favour stainless steel, heavy-gauge aluminium, cast iron and speciality bakeware, offering higher average order values and opportunities for B2B relationships.

As India’s HoReCa sector expands in major metros and Tier-2 cities, the commercial cookware market could reasonably approach 25% of total cookware value. Manufacturers with dedicated HoReCa lines, technical support and financing/leasing solutions for large kitchens can build sticky, higher-margin business, complementing mass-market household sales, particularly in North and West Indian urban clusters with dense hospitality and corporate presence.

Rural and Tier-2/3 penetration via e-commerce and exclusive stores

E-commerce growth and the expansion of exclusive brand outlets (EBOs) present a structural opportunity in under-penetrated rural and Tier-2/3 markets. TTK Prestige, for example, operates more than 620 Prestige Xclusive stores in over 363 cities across 28 states, alongside multi-brand retail and online channels. Stovekraft (Pigeon, Gilma) and Wonderchef similarly emphasize presence in smaller towns through modern trade, general trade and digital marketplaces. As logistics networks deepen and online platforms improve last-mile delivery, branded cookware can penetrate beyond metros at scale.

Category-wise Analysis

Product Type Insights

Pots & Pans accounts for the leading product type, accounting for about 29.8% share of India’s cookware market, as they are core to everyday Indian cooking across boiling, sautéing, and frying. Market data indicates that “core cookware” (including pots, pans, pressure cookers, tawas, kadai/woks, and basic sets) collectively accounts for around 73.7% share in 2026, reinforcing the primacy of these categories. Compared with bakeware or niche specialty items, pots & pans enjoy wide household penetration and steady replacement demand, so their leadership is likely to persist even as specialty products gain share.

Specialty/traditional cookware is the fast-growing product segment projected to reach about 7.8% CAGR, supported by rising interest in regional cooking styles, health-centric marketing, and the revival of cast-iron, clay, and stoneware formats. This category includes kadai variants, grill pans, appam pans, idli/dhokla steamers, and ethnic cookware, which appeal to premium consumers and urban households seeking authenticity and versatility.

Material Insights

By material, stainless steel is the leading segment, with approximately 35% share of India’s cookware market value in 2025, reflecting its durability, corrosion resistance, and entrenched role in Indian cooking traditions. Market research notes that stainless steel held about 35.1% market share in 2026, supported by consumer trust and compliance with IS 14756:2022 standards that ensure safe steel grades free of harmful admixtures. Compared with aluminium, glass, or coated surfaces, stainless steel combines affordability with perceived safety, keeping it dominant in both household and HoReCa kitchens.

Cast Iron is the fast-growing material segment, with a forecast CAGR of about 7.9% (close to the 7.86% projected through 2033), driven by consumer interest in “chemical-free” cooking, heat retention and potential iron fortification benefits. premium brands increasingly market enameled and seasoned cast-iron tawas, grills, and Dutch-oven-style pots, targeting health-conscious and experimental home cooks, especially in South and West India.

End-user Insights

On an end-user basis, residential households are the leading segment, contributing around 70.4% share of India’s cookware market value, as household purchases dominate volumes and drive core category penetration. Rise in nuclear families, urban working couples, and increased home cooking post-pandemic continue to support higher-value purchases across pots & pans, sets, and specialty items.

Commercial/HoReCa is the fast-growing end-user segment with a projected CAGR of about 7.3%, underpinned by expansion in organized food-service, quick-service restaurants, cloud kitchens, and institutional catering. Hotels and restaurants demand heavier-gauge, high-durability cookware and specialized bakeware, while institutional kitchens increasingly standardize stainless steel and induction-compatible equipment, creating recurring bulk procurement opportunities.

Zonal Insights

North India Cookware Market Trends

North India holds a prominent 28.7% share, driven by large consumption bases in Delhi-NCR, Uttar Pradesh, Punjab, Haryana, and Rajasthan, where rising incomes and urbanization accelerate replacement and premiumization of cookware categories. Within North India, the Delhi-NCR cluster (Delhi, Gurugram, Noida) contributes a major share of cookware revenues estimated in the hundreds of millions of dollars annually by 2026, driven by nuclear families, modern retail, and strong e-commerce penetration across stainless steel, non-stick, and premium brands such as TTK Prestige, Meyer, and Wonderchef.

Beyond Delhi-NCR, Uttar Pradesh, Punjab, Haryana, and Rajasthan provide robust demand from Tier-1 and Tier-2 cities such as Lucknow, Kanpur, Chandigarh, Ludhiana, and Jaipur, where organized cookware brands are rapidly expanding distribution and capturing share from unorganized players, particularly in core cookware and pressure cooker categories.

South India Cookware Market

South India is the fast-growing market with an estimated 31.4% share and about 7.6% CAGR in the forecast period, driven by the presence of cookware manufacturing clusters and high per-capita cookware spending in states such as Karnataka, Tamil Nadu, Telangana, and Kerala. States such as Karnataka and Tamil Nadu host major manufacturers, including TTK Prestige (headquartered in Bengaluru with plants at Hosur and Coimbatore) and Stovekraft (Pigeon, Gilma) with ISO-certified facilities, collectively anchoring a regional market worth hundreds of millions of dollars by 2026 in both domestic and export-oriented cookware.

Andhra Pradesh, Telangana and Kerala add substantial consumption and export potential, with urban centres such as Hyderabad, Kochi and Visakhapatnam adopting premium non-stick, cast iron, and specialty cookware faster than the national average, supported by modern retail, e-commerce and strong HoReCa sectors.

West India Cookware Market

West India holds approximately 23.7% share and is likely to reach 7% CAGR, supported by manufacturing hubs and high urbanization in Maharashtra and Gujarat, and rising cookware consumption across Mumbai, Pune, Ahmedabad, Surat, and Vadodara. Maharashtra, with Mumbai and Pune as key markets, anchors a large share of cookware demand and supply; major brands such as Hawkins (based in Mumbai), Vinod Cookware, and Wonderchef have corporate offices or manufacturing in the region.

Gujarat contributes through growing urban centres (Ahmedabad, Vadodara, Surat) and emerging middle-class consumption, while companies like Borosil invest in expanding glass and kitchen product capacity and pursue acquisitions in the kitchen sector, reinforcing West India’s role as a key production and innovation base.

Competitive Landscape

India cookware market is moderately concentrated among leading branded players in pressure cookers, non-stick and stainless steel, yet fragmented across regional and unorganized manufacturers, particularly in aluminium and low-end steel. Key differentiators include coating durability, material safety (BIS compliance), induction-compatibility, design, distribution reach, and omni-channel presence spanning exclusive brand outlets and digital marketplaces.

Dominant strategic themes are innovation in non-stick and cast-iron offerings, cost leadership via scale manufacturing in South and West India, and market expansion into Tier-2/3 cities through brand-owned stores and e-commerce, supported by regulatory alignment and marketing around health, safety and heritage cooking formats.

Key Developments:

- In October 2024, Borosil announced plans to double group revenues to about INR 7,000 crore in four years, backed by INR 250 crore of investments in new plants and product expansions, including kitchen and household categories, highlighting aggressive growth and inorganic-expansion ambitions in the wider kitchenware space.

- In July 2024, TTK Prestige highlighted its nationwide footprint of over 620 exclusive stores and five manufacturing plants, underscoring continued investments in distribution, R&D, and capacity to strengthen its leadership in pressure cookers and cookware across urban and rural India.

India Cookware Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 2.3 Bn |

| Current Market Value (2026) | US$ 3.2 Bn |

| Projected Market Value (2033) | US$ 5.1 Bn |

| CAGR (2026 - 2033) | 6.8% |

| Leading Region | South India - 31.4% |

| Dominant Material Type | Stainless Steel - 33.7% |

| Top-ranking Product Type | Pots & Pans - 29.8% |

| Incremental Opportunity | US$ 1.9 Bn |

Companies Covered in India Cookware Market

- TTK Prestige

- Hawkins Cookers Ltd.

- Stovekraft (Pigeon)

- Wonderchef Home Appliances

- Butterfly Gandhimathi Appliances

- Vinod Cookware

- Cello World

- Borosil Limited

- Hamilton Housewares (Milton)

- Meyer India

- Bajaj Electricals

- Usha International

- Bergner India

- Nirlep Appliances

- Stahl Kitchens

Frequently Asked Questions

The India Cookware Market is expected to reach about US$ 3.2 Bn in 2026 and approximately US$ 5.1 Bn by 2033, reflecting steady expansion across core and specialty cookware categories.

The market is driven by rising incomes and urbanization, increasing penetration of non-stick and premium cookware, and strengthened BIS quality and safety standards for stainless steel and aluminium utensils, which support organized brands and consumer upgrades.

From 2026 to 2033, the India Cookware Market is projected to grow at around 6.8% CAGR.

Key opportunities lie in fast-growing non-stick, cast-iron and specialty/traditional segments, expanding Commercial/HoReCa demand, and deeper penetration of branded cookware into rural and Tier-2/3 markets via e-commerce and exclusive stores.

Key players include TTK Prestige, Hawkins Cookers, Stovekraft (Pigeon), Wonderchef, Vinod Cookware, Meyer Housewares India and Borosil, along with several regional and specialized brands active in stainless steel, aluminium, non-stick and cast-iron cookware.