- Advanced Materials

- High Purity Lignin Market

High Purity Lignin Market Size, Share, and Growth Forecast 2025 - 2032

High Purity Lignin Market by Product Type (Kraft Lignin, Organosolv, and Others), Source (Hardwood, Softwood, Sugarcane Bagasse, Straw, and Others), Application (Binders & Adhesives, Phenol, Vanillin, Carbon Fibre, Activated Carbon, and Others), and Regional Analysis for 2025 - 2032

High Purity Lignin Market Size and Share Analysis

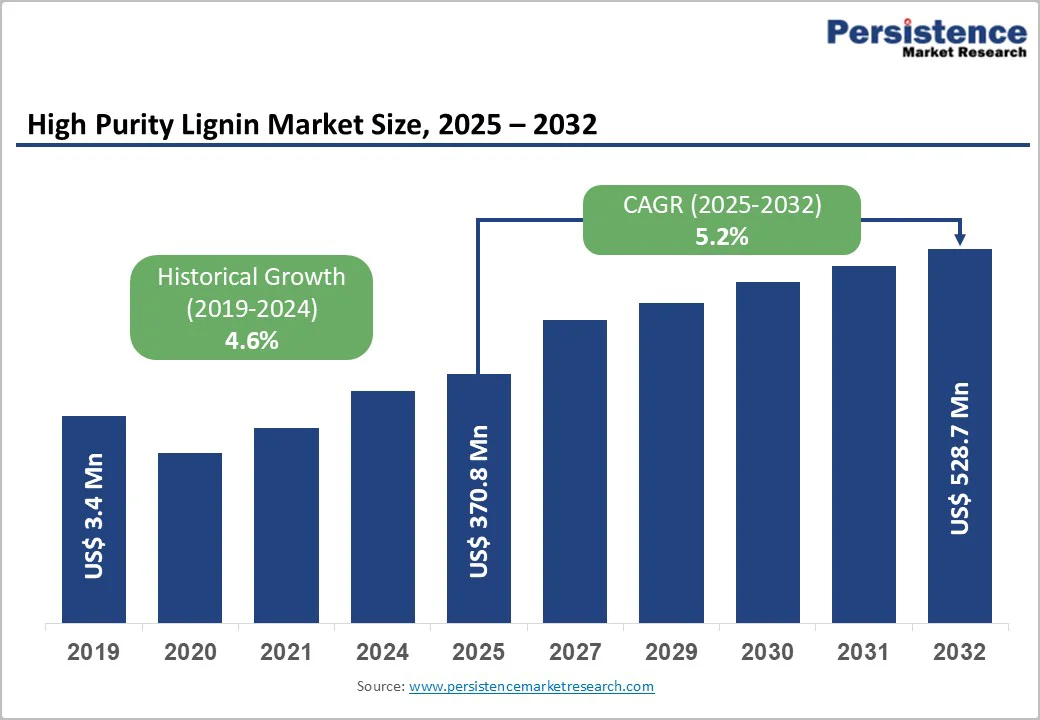

The global high purity lignin market size is valued at US$ 370.8 million in 2025 and is projected to reach US$ 528.7 million by 2032, growing at a CAGR of 5.2% between 2025 and 2032.

Market expansion is driven by accelerating demand for sustainable bio-based alternatives to petroleum-derived chemicals, rising environmental consciousness supporting circular economy principles and renewable resource utilization, and technological advancements improving lignin extraction and purification capabilities.

Expanding applications across diverse industries, including binders and adhesives, phenol derivatives, vanillin production, and carbon fiber manufacturing, combined with government policies promoting green chemistry and formaldehyde-free formulations, sustain market growth through enhanced product accessibility and end-use diversification.

Key Industry Highlights:

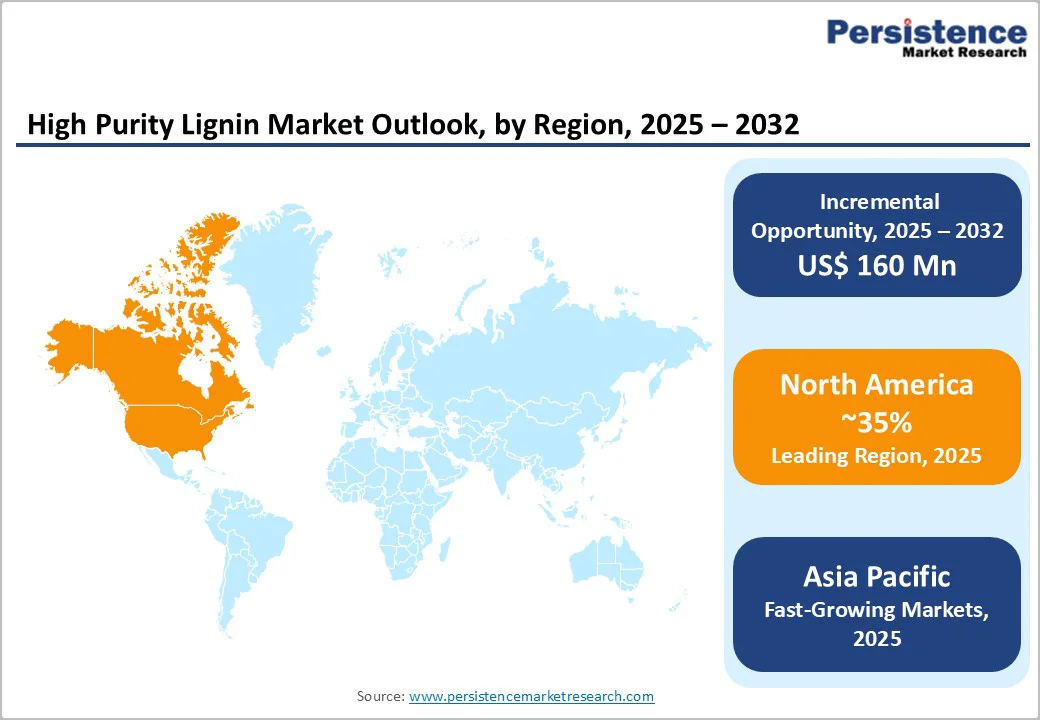

- Leading Region: North America maintains combined market dominance with 35% global market share, driven by established pulp and paper industry, advanced manufacturing capabilities, environmental regulations, and government support for green chemistry.

- Fastest Growing Region: Asia Pacific demonstrates highest growth trajectory at 7.2% CAGR, propelled by manufacturing expansion, pharmaceutical and biopolymer sector growth, emerging market opportunities, and government sustainability initiatives.

- Dominant Product Type: Kraft Lignin commands largest product type at 57% market share, driven by established pulp mill availability, proven industrial compatibility, cost advantage, and widespread application adoption.

- Fastest Growing Application: Carbon Fiber Applications represent fastest-growing end-use at 7.5% CAGR, driven by pilot production achievements, automotive lightweighting requirements, and commercialization targeted for 2026.

- Key Market Opportunity: High-value chemical applications including vanillin production and phenolic compound manufacturing, representing the highest-value opportunity through 30% cost advantage and expanding specialty chemical demand supporting premium pricing.

| Key Insights | Details |

|---|---|

| High Purity Lignin Market Size (2025E) | US$ 370.8 Mn |

| Market Value Forecast (2032F) | US$ 528.7 Mn |

| Projected Growth CAGR (2025 - 2032) | 5.2% |

| Historical Market Growth (2019 - 2024) | 4.6% |

Market Dynamics

Market Growth Drivers

Growing Demand for Bio-Based and Sustainable Materials Driving Market Growth

The accelerating global shift toward sustainable, renewable, and environmentally compliant materials is a primary driver for the high-purity lignin market. Governments and industries are actively reducing reliance on fossil-fuel-derived chemicals, creating strong demand for bio-based alternatives that support carbon reduction commitments.

High-purity lignin, a natural, biodegradable polymer extracted from biomass, serves as a valuable substitute for conventional petrochemicals across sectors such as adhesives, plastics, coatings, carbon fibers, and dispersants. According to industry estimates, the bio-based chemicals market is projected to grow at 10-12% annually, directly supporting uptake of high-purity lignin as a key functional ingredient.

Corporations are investing in circular economy strategies, pushing adoption of renewable raw materials with low environmental footprints. Lignin’s potential to reduce greenhouse gas emissions by up to 40-60% compared to petroleum-derived counterparts further enhances its appeal.

With increasing regulatory pressure in Europe and North America promoting sustainable sourcing and low-carbon manufacturing, demand for high-purity lignin continues to strengthen across industrial applications.

Rising Use of High-Purity Lignin in High-Performance Material Applications

The rapid development of advanced materials, especially in automotive, aerospace, construction, and energy sectors, is significantly boosting demand for high-purity lignin due to its exceptional structural, antioxidative, and reinforcement properties.

High-purity lignin is increasingly being used in carbon fiber production, where it can reduce precursor costs by 30-50% compared to traditional polyacrylonitrile (PAN), making lightweight composite materials far more cost-effective. Its antioxidant and UV-resistant characteristics also make it ideal for high-performance polymers, resins, and coatings requiring enhanced durability and thermal stability.

In the automotive industry, lightweight materials supporting fuel efficiency and emission reduction are growing at approximately 9% CAGR, directly influencing lignin adoption.

Furthermore, ongoing R&D in lignin-based batteries and energy storage materials is opening new high-value applications, attracting investments from material science companies and research institutions. As high-purity lignin enables both performance enhancement and cost savings, its integration into next-generation materials continues to rise globally.

Market Restraints

High Production Costs and Limited Industrial Scale Operations

A limited number of commercial-scale lignin production facilities constraining supply and maintaining elevated pricing. Organosolv lignin production processes require specialized equipment and technical expertise, restricting market accessibility.

Lack of standardized industrial processes is hindering cost reduction and market scaling. Batch-to-batch variability in lignin quality creates consistency challenges for downstream users. Infrastructure investment requirements for expanded production capacity limit new market entrants.

Insufficient Market Awareness and Limited Commercial Applications Development

Limited awareness regarding lignin applications among end-users is constraining demand growth. Insufficient research and development funding for application development, particularly in developing markets. Established a petroleum-based product ecosystem and infrastructure, creating switching barriers for manufacturers. Regulatory uncertainty regarding lignin-based product approvals is extending commercialization timelines.

Market Opportunities

High-Value Chemical Applications and Vanillin Production Expansion

Expansion into high-value chemical applications represents fastest-growing market opportunity driven by increasing specialty chemical demand. Global vanillin demand is reaching over 16,000 metric tons in 2023 with lignin-derived vanillin capable of meeting 20% of demand at 30% cost advantage. Lignin as a platform chemical for producing phenolic compounds supporting diverse industrial applications.

Phenolic resins manufacturing utilizing lignin feedstock, creating formaldehyde-free alternatives. Carbon fiber precursor development showing 25% production cost reduction potential in Swedish and Japanese trials. Bio-based chemicals and biofuel expansion are driven by government investments.

Industrial trials demonstrating 12% improvement in oil extraction using lignin-based chemicals in enhanced oil recovery applications. High-value applications represent fastest-growing opportunity attracting technology-focused manufacturers.

Carbon Fiber and Advanced Composites Market Development

The carbon fiber and advanced composites segment represents an emerging high-growth opportunity driven by the need for automotive and aerospace lightweight components. Pilot facilities in Sweden producing 1,800 kg of lignin-carbon fibers in 2023 with commercialization targeted for 2026. Automotive and aerospace sectors anticipating lightweight composite demand exceeding 10,000 metric tons annually by 2027.

Lignin-based precursors offering cost-efficient alternatives to polyacrylonitrile, supporting wider industry adoption. The automotive industry actively testing lignin-based composites for interior parts, reducing production costs by 25%. Weight reduction supporting fuel efficiency improvements and emission reduction targets, driving adoption.

Aerospace industry seeking advanced materials for structural components supporting premium applications. Government infrastructure investment programs supporting advanced materials development. Advanced composites represent fastest-growing segment, supporting premium pricing and margin expansion.

Category-wise Insights

Product Type Analysis

Kraft Lignin holds a dominant position in the global high-purity lignin market, accounting for approximately 57% of the total market share. This leadership is primarily attributed to its abundant availability as a byproduct of large-scale kraft pulping operations, which ensures a consistent raw material supply and cost-effective extraction.

Kraft lignin’s well-established industrial presence enables manufacturers to integrate advanced purification techniques, such as membrane filtration, solvent extraction, and precipitation processes, to achieve higher purity levels suitable for high-value applications. Its chemical structure, rich in phenolic and aromatic compounds, makes it particularly compatible with downstream processing routes for bio-based chemicals, carbon fibers, adhesives, dispersants, and polymer additives.

Moreover, ongoing investments by major pulp producers in lignin valorization technologies further strengthen kraft lignin’s market position, enabling scalable production, improved quality control, and broader application development. As industries increasingly prioritize renewable and low-carbon materials, kraft lignin continues to serve as the preferred product category supporting both commercial viability and technological innovation in the high-purity lignin landscape.

Source Analysis

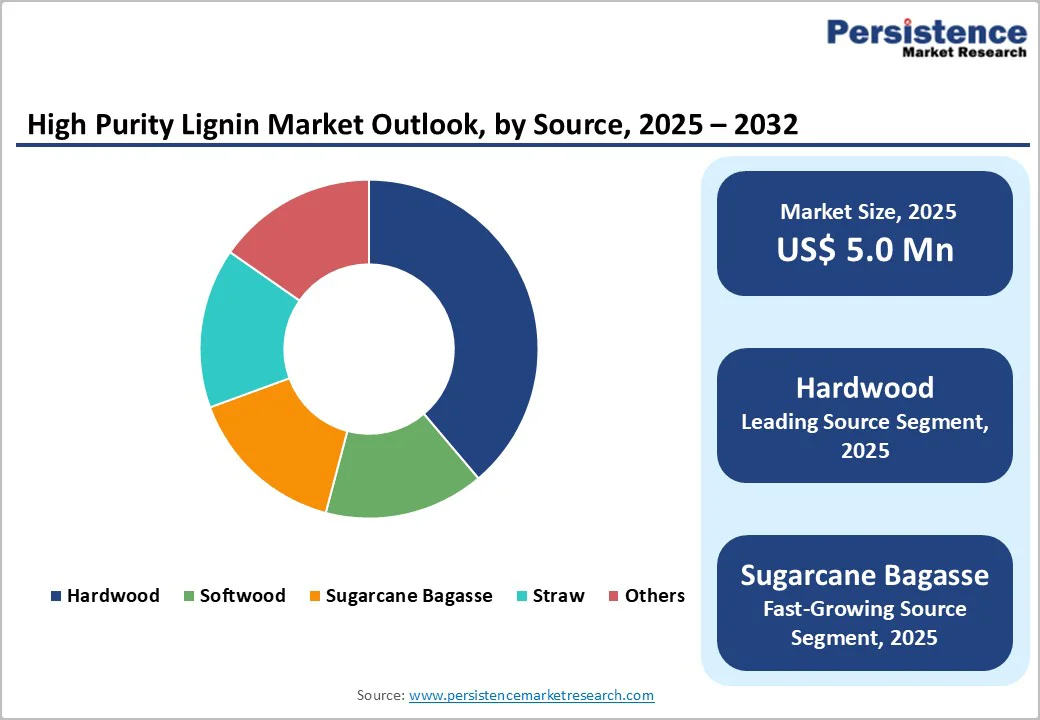

Hardwood sources hold a dominant position in the high-purity lignin market, accounting for approximately 48% of the total market share. This dominance is driven by the inherent structural characteristics of hardwood biomass, which enables the production of high-quality lignin with superior purity, uniformity, and processability.

Hardwood-derived lignin typically contains lower molecular weight fractions and a more balanced syringyl-to-guaiacyl (S/G) ratio, making it easier to refine and more suitable for advanced applications such as carbon fibers, specialty chemicals, dispersants, and performance polymers.

Hardwood pulping operations, especially kraft and organosolv processes, are widely established across North America, Europe, and parts of Asia, ensuring stable raw material availability and cost-efficient extraction. The rising demand for premium-grade lignin in electronics, automotive composites, and bio-based chemical formulations further strengthens the preference for hardwood sources.

As manufacturers continue to invest in purification technologies and value-added lignin derivatives, hardwood-based lignin is expected to maintain its competitive edge in meeting the performance and consistency requirements of emerging high-value applications.

Application Analysis

Binders and Adhesives applications dominate end-use consumption in the high-purity lignin market, accounting for approximately 42% of total market demand. This strong market position is supported by lignin’s excellent binding capability, phenolic structure, and high compatibility with industrial adhesive formulations.

High-purity lignin serves as a renewable and cost-effective alternative to petroleum-based phenols used in phenolic resins, plywood adhesives, particleboard binders, and engineered wood products. In the construction sector, increasing emphasis on sustainable building materials and low-VOC formulations is driving greater adoption of lignin-enhanced adhesives.

Likewise, the manufacturing sector utilizes lignin-based binders in coatings, molded composites, insulation materials, and industrial sealants, where performance reliability, thermal stability, and reduced environmental impact are key requirements.

Technological advancements in lignin purification and chemical modification have further improved adhesion strength, curing behavior, and compatibility with various substrates, enabling broader commercialization. As global industries continue transitioning toward bio-based and eco-friendly adhesive solutions, the demand for high-purity lignin in binder and adhesive applications is expected to expand steadily over the forecast period.

Regional Insights

North America High Purity Lignin Market Trends

North America maintains a strong and influential position in the global high-purity lignin market, accounting for an estimated 35% market share in 2025. This regional strength is underpinned by a well-established pulp and paper industry that ensures consistent availability of high-quality lignin feedstock, enabling large-scale extraction and purification.

The U.S. and Canada host several major kraft pulp facilities, which continue to invest in lignin separation, purification, and valorization technologies to support premium-grade product development.

The region also benefits from a rapidly expanding bio-based chemicals sector, driven by sustainability mandates, decarbonization goals, and growing demand for renewable raw materials across adhesives, composites, carbon fibers, and specialty chemicals.

North America’s innovation ecosystem, supported by leading research universities, government-backed clean technology programs, and strong industry-academia partnerships, accelerates advancements in lignin-based materials, including engineered polymers, dispersants, and energy storage components.

Europe High Purity Lignin Market Trends

Europe demonstrates strong technology leadership and regulatory momentum in the global high-purity lignin market, making it one of the most progressive regions in lignin innovation and commercialization. The region benefits from a mature pulp and paper industry, particularly in countries such as Finland, Sweden, France, and Germany, where high-purity kraft and organosolv lignin production is well-integrated with advanced biorefinery operations.

European manufacturers are at the forefront of developing cutting-edge purification technologies, including organosolv extraction, enzymatic fractionation, and controlled depolymerization, which enable production of premium lignin suitable for specialty chemicals, carbon fibers, adhesives, and high-performance composites.

Growing demand for low-carbon construction materials, electric vehicle components, and eco-friendly industrial chemicals positions Europe as a major driver of lignin-based technology advancement. With its combination of policy support, technological capacity, and sustainability priorities, Europe continues to expand its influence within the high-purity lignin market.

Asia Pacific High Purity Lignin Trends

Asia Pacific emerges as the fastest-growing region in the global high-purity lignin market, supported by rapid industrial expansion, strong manufacturing capabilities, and increasing demand for sustainable materials. The region is projected to have a CAGR of 7.2% during 2025 - 2032, driven by the rising adoption of bio-based chemicals, composites, and high-performance materials across China, Japan, India, and Southeast Asia.

China’s large-scale pulp and paper industry provides a strong foundation for lignin extraction, while Japan and South Korea are investing heavily in carbon fiber innovation, creating significant opportunities for lignin-based precursors in advanced composites and EV components.

Government-led sustainability initiatives and decarbonization goals across the region are accelerating interest in renewable materials, particularly in construction, automotive manufacturing, and polymer production.

Growing investments in biorefineries, green chemical production, and lignin-derived specialty materials further strengthen market momentum. the expansion of adhesives, coatings, and engineered wood product manufacturing in emerging economies such as Vietnam, Indonesia, and India boosts the demand for lignin-based binders and additives.

Competitive Landscape

The global high-purity lignin market is moderately consolidated, with major players such as Suzano SA, Domtar Corporation, West Fraser, Stora Enso Oyj, and Ingevity Corporation collectively accounting for 50-55% of the total market share.

Their dominance is driven by integrated pulp mill operations, strong production capacities, and well-established global distribution networks. Tier-two manufacturers, including Liquid Lignin Company and Green Value S.A., hold notable regional shares by specializing in niche extraction and purification technologies. A growing base of emerging organosolv lignin producers is leveraging advanced purification methods to target premium, high-value application segments.

Research-driven organizations and academic spinoffs are also contributing to market evolution, particularly through innovations in high-performance lignin derivatives and application-specific material development.

Across the competitive landscape, companies are prioritizing technological advancements, innovative purification processes, collaborative application development, sustainable raw material sourcing, and supply chain integration to strengthen market presence and unlock new growth opportunities.

Key Market Developments

- In April 2024, Stora Enso Oyj expanded its lignin-based product portfolio by introducing new high-purity lignin grades designed for advanced material applications, including adhesives, dispersants, bioplastics, and energy storage components. The initiative strengthens the company’s strategy to deliver scalable, low-carbon alternatives to petrochemical-based materials.

- In February 2024, Leading automotive manufacturers initiated five OEM-level pilot programs to evaluate lignin-based composite materials for interior automotive components such as door trims, dashboards, and structural reinforcement parts.

- In September 2023, Pilot programs in Sweden and Japan successfully demonstrated large-scale lignin-based carbon fiber production, marking a significant technological breakthrough for the industry. The trials yielded approximately 1,800 kg of commercial-grade carbon fiber, validating lignin’s potential as a cost-efficient precursor.

Companies Covered in High Purity Lignin Market

- Suzano SA

- Domtar Corporation

- West Fraser

- Stora Enso Oyj

- Liquid Lignin Company

- Metsa Group

- Sigma Aldrich

- Alberta Pacific

- Green Value S.A.

- Ingevity Corporation

- Borregaard

- Fortum

Frequently Asked Questions

The global high purity lignin market was valued at US$ 370.8 million in 2025 and is projected to reach US$ 528.7 million by 2032, representing a CAGR of 5.2% during the forecast period.

Growing shift toward bio-based, sustainable materials as industries move away from petroleum-derived chemicals, supported by rising adoption in advanced applications such as carbon fibers, specialty chemicals, adhesives, and high-performance composites is accelerating its market growth.

Kraft Lignin //commands approximately 57% market share, driven by established pulp mill availability, proven industrial compatibility, cost advantage through byproduct status from paper production, and widespread application adoption across multiple industries.

North America maintain combined market dominance with 35% global market share, driven by established pulp and paper industry, advanced manufacturing capabilities, stringent environmental regulations, and government support for green chemistry initiatives.

Carbon fiber and advanced composites applications represent highest-value opportunity growing at 12-15% CAGR, with pilot production achieving 1,800 kg in 2023 and commercialization targeted for 2026, supported by automotive lightweighting demand exceeding 10,000 metric tons by 2027.

Market leaders include Suzano SA (Brazil) leveraging pulp production integration, Stora Enso Oyj (Finland) with innovative product development, and Domtar Corporation (Canada) utilizing North American pulp infrastructure, collectively representing approximately 50-55% market concentration.