- Inks, Coatings, Adhesives & Sealants (ICAS)

- Sleeves Market

Sleeves Market Size, Share, Trends, and Growth Forecast 2025 - 2032

Sleeves Market by Product Type (Insulating Sleeves and Exothermic Sleeves), Application (Steel Casting, Aluminum Casting, Cast Iron, SG Iron, Brass & Bronze, and Others), and Regional Analysis 2025 - 2032

Sleeves Market Size and Share Analysis

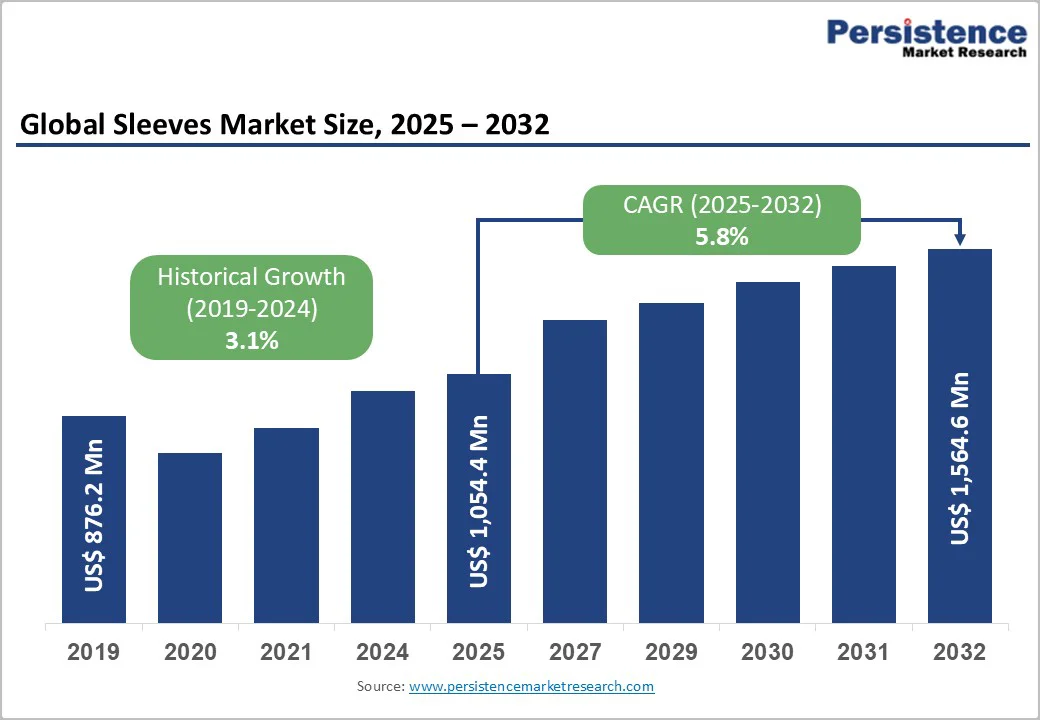

The global sleeves market size was valued at US$ 1,054.4 million in 2025 and is projected to reach US$ 1,564.6 million, growing at a CAGR of 5.8% between 2025 and 2032. Market expansion is driven by accelerating demand for high-quality metal castings across automotive and aerospace industries, rapid industrialization and infrastructure development projects globally supporting heavy machinery and equipment manufacturing. Technological advancements in foundry processes including investment in casting and additive manufacturing, combined with increased emphasis on reducing casting defects and improving yield efficiency also propelling the market growth.

Key Market Highlights:

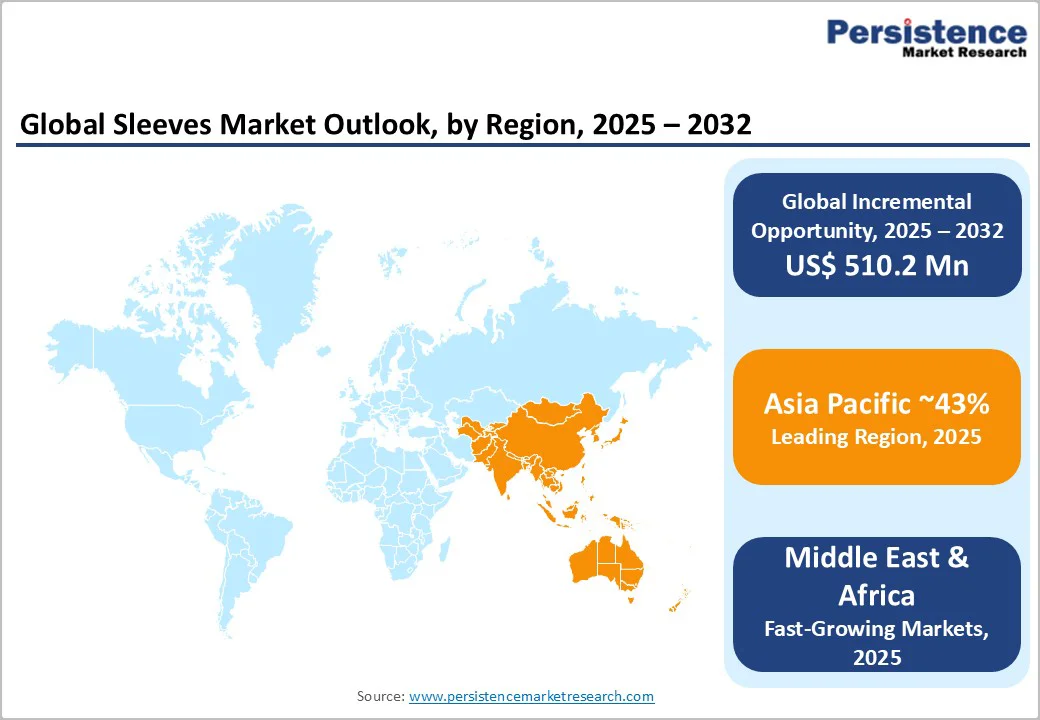

- Leading Region: Asia Pacific maintains dominant market position with 42.8% global market share, driven by China's steel production dominance, rapid industrialization, infrastructure development, and emerging market opportunities supporting sustained regional demand expansion.

- Fastest Growing Country: India and Southeast Asia demonstrate highest growth trajectory at approximately 7.2% and 7.8% CAGR, propelled by infrastructure modernization, automotive industry expansion, manufacturing localization, and government investment programs supporting accelerated market growth.

- Dominant Product Type: Exothermic Sleeves command largest product type segment at 44% market share, driven by superior defect reduction capabilities, automotive and machinery industry preference, and proven effectiveness in yield optimization.

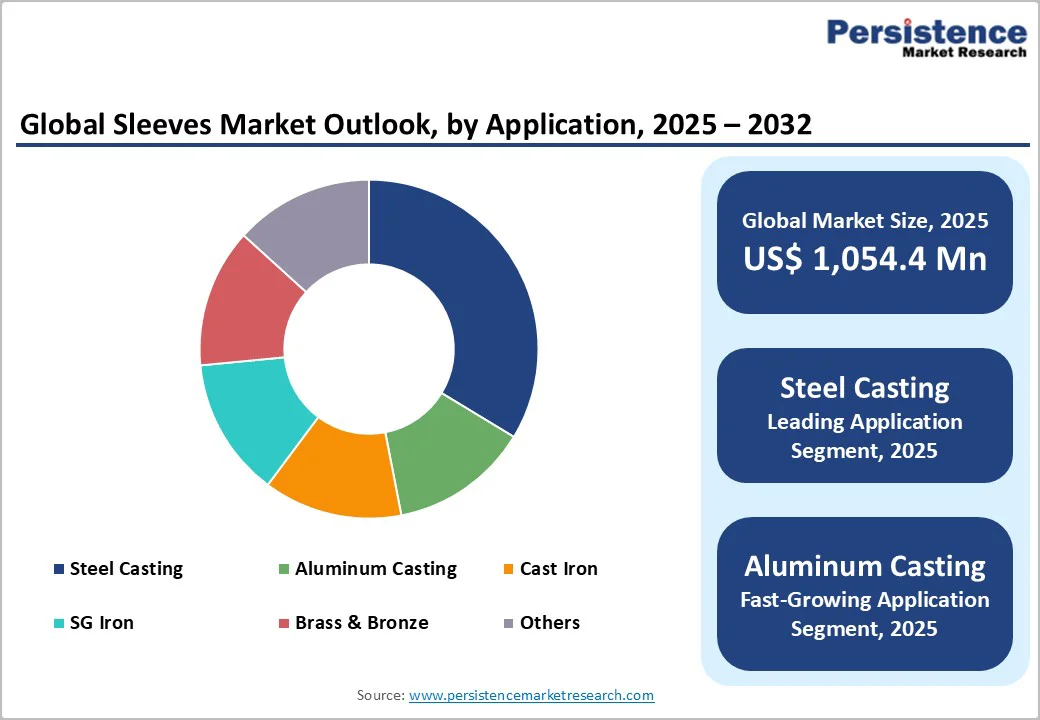

- Dominant Application: Steel Casting Applications represent the dominant end-use segment, accounting for approximately 38% of total market demand through widespread adoption in automotive components and machinery manufacturing.

- Key Market Opportunity: Digital integration and smart foundry technologies including real-time monitoring and AI-based process optimization supporting next-generation casting efficiency and quality improvements attracting technology-focused foundry operators.

| Key Insights | Details |

|---|---|

| Sleeves Market Size (2025E) | US$ 1,054.4 Mn |

| Market Value Forecast (2032F) | US$ 1,564.6 Mn |

| Projected Growth CAGR(2025-2032) | 5.8% |

| Historical Market Growth (2019-2024) | 3.1% |

Market Dynamics

Drivers - Rising Demand for High-Quality Metal Castings in Automotive and Aerospace Industries

Global automotive and aerospace sectors create exceptional market opportunity for advanced foundry sleeves supporting precision component manufacturing. Automotive industry producing approximately 93 million vehicles annually with complex metal casting components requiring advanced insulation and exothermic sleeve technologies. Aerospace sector manufacturing high-precision components demanding minimal defect rates and superior material properties driving demand for specialized sleeve solutions. Lightweight material requirements for fuel efficiency and emissions reduction necessitating advanced casting technologies and sleeve innovations.

Non-ferrous metal casting expansion including aluminum and magnesium components requiring precision casting processes supported by specialized sleeves. Defense and military equipment modernization programs supporting demand for high-performance casting solutions. Investment casting applications expanding for intricate and precision components across diverse industries requiring controlled solidification and feeding processes. Market growth reflects industry commitment to reducing casting defects and improving yield efficiency through advanced sleeve technologies.

Infrastructure Development and Heavy Machinery Manufacturing Growth

Global infrastructure expansion and heavy machinery manufacturing create substantial foundry sleeve demand through increased metal casting requirements. Infrastructure development projects worldwide including roads, bridges, and building construction requiring steel and metal components manufactured through casting processes. Rapid urbanization particularly in Asia-Pacific region driving construction and infrastructure investment requiring metal castings. Heavy machinery manufacturing for mining, agriculture, and industrial equipment consuming significant volumes of metal castings dependent on quality sleeve technologies.

Industrial modernization and automation initiatives supporting investment in advanced manufacturing equipment and foundry capabilities. Energy sector expansion including renewable energy equipment manufacturing requiring specialized metal castings with precise dimensional control. Government infrastructure investment programs and public works initiatives supporting sustained demand for metal casting applications. Consistent infrastructure development supports multi-year revenue visibility for foundry sleeve manufacturers.

Restraints - High Production Costs and Raw Material Price Volatility

Elevated foundry operating costs driven by energy expenses and raw material sourcing constraining market profitability. Department of Energy reporting 35% increase in foundry operation energy costs since 2022 reducing operational margins and pricing competitiveness. Raw material price fluctuations affecting sleeve composition costs including ceramic and refractory materials. Specialized manufacturing equipment and technical expertise requirements limiting production capacity and supplier diversity. Quality assurance and testing expenses adding significant operational burden to manufacturers.

Environmental Regulations and Worker Safety Requirements

Occupational Safety and Health Administration enhanced workplace safety requirements for foundry operations mandating investments in safer sleeve handling systems. Environmental compliance regarding emissions and hazardous material management increasing operational expenses and facility requirements. Waste management and recycling obligations creating additional compliance costs. Regulatory restrictions on conventional sleeve materials requiring transition to alternative compositions and processes.

Opportunity - Advanced Materials and Eco-Friendly Sleeve Development Presents Growth Opportunities

Development and commercialization of advanced materials and environmentally-friendly sleeve solutions represent exceptional market opportunity addressing sustainability and performance requirements. Ceramic-based riser sleeve materials emerging with superior high-temperature performance supporting advanced casting applications. Recyclable and eco-friendly sleeve materials reducing environmental impact aligning with industry sustainability priorities. Innovative sleeve designs incorporating enhanced thermal properties and dimensional stability improving casting quality and yield optimization.

Research and development investments creating specialized sleeves for complex casting geometries and exotic materials. National Science Foundation advanced manufacturing research grants totaling US$ 2.1 billion supporting development of smart riser sleeve systems with embedded sensors. Collaboration between manufacturers and foundries developing next-generation solutions addressing emerging casting challenges. Technology advancement supporting premium pricing and competitive differentiation.

Digital Integration and Smart Foundry Technologies

Digital transformation and Industry 4.0 integration create market opportunity for intelligent sleeve solutions optimizing casting operations. Simulation software integration enabling optimization of sleeve placement and design minimizing waste and ensuring optimal cooling. Real-time process monitoring systems tracking casting parameters improving quality control and defect reduction.

Additive manufacturing enabling custom-designed sleeves for specialized casting requirements and rapid prototyping. Digital twin technology allowing virtual testing and optimization before physical production. Foundry automation driving demand for standardized sleeve solutions supporting integrated manufacturing systems. Data analytics enabling predictive maintenance and process optimization extending sleeve lifespan and improving efficiency. Smart technologies attracting technology-focused foundry operators supporting market expansion.

Category-wise Analysis

Product Type Insights

Exothermic Sleeves dominate the foundry sleeves market, commanding approximately 44% market share driven by superior defect reduction capabilities and widespread adoption across steel and iron casting operations. Exothermic sleeves incorporating chemical reactions generating additional heat maintaining molten metal temperature and extending solidification time. Superior performance in feeding large and complex castings reducing shrinkage defects and improving casting yield. Automotive and heavy machinery industries preferring exothermic sleeves for demanding applications requiring extended feeding periods. Continuous technological improvements in exothermic material formulations providing better temperature control and longer reaction times.

Insulating sleeves capturing approximately 32% market share through efficient thermal management and widespread use in non-ferrous and precision casting applications. Slurry sleeves and high-density sleeves commanding remaining market share addressing specialized applications. Market leadership reflects effectiveness in reducing casting defects and improving yield optimization.

Application Insights

Steel casting applications constitute the largest application in the global sleeves market, accounting for around 38% of total demand. The dominance of this segment is driven by the extensive use of sleeves across automotive, heavy machinery, industrial equipment, and engineered component manufacturing, where precision and durability are critical.

In steel foundries, the production of complex castings such as engine blocks, transmission housings, pump bodies, valve components, and structural machine parts requires sleeves that deliver exceptional thermal resistance, dimensional stability, and anti-reactive properties. Premium insulating and exothermic sleeves help manufacturers minimize casting defects such as shrinkage, porosity, and cold shuts by ensuring directional solidification and stable heat control.

Regional Insights

North America Sleeves Market Trends

North America maintains a significant market position through established manufacturing base and automotive industry leadership. U.S. Geological Survey data indicating domestic steel production reaching 78.7 million metric tons in 2024, supporting consistent sleeve demand. Automotive manufacturing in the United States and Mexico is driving regional sleeve consumption for precision casting applications. Advanced manufacturing initiatives and CHIPS Act investments supporting foundry modernization and capacity expansion.

The aerospace industry concentration in North America supports premium sleeve adoption for high-precision applications. The Government Defense Department modernization programs are creating opportunities for specialized casting solutions. Environmental regulations in developed markets support the adoption of eco-friendly sleeve technologies.

Europe Sleeves Market Trends

Europe maintains a stable market position supported by its strong engineering base, mature automotive manufacturing ecosystem, and advanced industrial machinery sector. The region’s foundry landscape continues to emphasize high-precision ferrous and non-ferrous castings, with Germany, Italy, France, and Spain remaining the largest producers. European steelmakers reported gradual recovery in output through 2024, helping sustain consistent demand for insulating and exothermic sleeves across automotive components, rail systems, and heavy equipment casting operations.

Strong regulatory emphasis on energy efficiency and emissions reduction is also accelerating modernization within foundries, encouraging the adoption of high-performance, low-emission sleeve technologies. Additionally, Europe’s transition toward lightweight materials in automotive and aerospace manufacturing is boosting the need for premium sleeves that ensure tight tolerances and defect-free production. Continued investments in automation, Industry 4.0 adoption, and sustainable casting practices collectively reinforce Europe’s relevance in the global sleeves market.

Asia Pacific Sleeves Market Trends

Asia Pacific dominates the global sleeves market with a commanding 42.8% share, driven by rapid industrialization and unprecedented expansion in casting production across China, India, Japan, and Southeast Asia. The region accounts for the largest global output of ferrous and non-ferrous castings, supported by extensive automotive manufacturing, machinery production, and infrastructure development.

China remains the core demand center with its massive steel casting capacity and continuous foundry modernization, while India’s fast-growing industrial base further accelerates sleeve consumption for high-precision automotive and engineering components. Strong government-led manufacturing initiatives, increasing investments in heavy industries, and rising adoption of advanced insulating and exothermic sleeves to improve casting quality continue to reinforce Asia Pacific’s dominant position in the global market.

Competitive Landscape

The global sleeves market is moderately consolidated, with leading manufacturers such as Vesuvius plc, ASK Chemicals, INEXO Cast Metal Solutions, and Shengquan Group collectively accounting for an estimated 45–50% of total market share. These companies maintain strong competitive positions through extensive product portfolios, advanced sleeve technologies, and long-standing relationships with major foundries. Their global supply networks, technical expertise, and continuous investment in high-performance insulating and exothermic sleeve solutions further reinforce their market leadership.

Strategic capacity expansion, material science innovation, and collaborative development programs with automotive and industrial foundries remain key drivers of differentiation across the industry. Emerging manufacturers, particularly from East and South Asia, are rapidly scaling their presence by utilizing cost-efficient production, expanding export capabilities, and integrating automated manufacturing processes.

Key Market Developments:

- In June 2024, Vesuvius plc announces development of new advanced ceramic-based riser sleeves achieving superior thermal properties for aerospace and automotive precision casting applications.

- In September 2024, ASK Chemicals launches eco-friendly sleeve formulation reducing environmental emissions by 40% while maintaining performance standards.

- In April 2025, Shengquan Group completes expansion of sleeve production capacity in China supporting regional demand from automotive and infrastructure sectors.

Sleeves Market Research Segmentation

By Product Type:

- Insulating Sleeves

- Exothermic Sleeves

- Slurry Sleeves

- High-density Sleeves

By Application:

- Steel Casting

- Aluminum Casting

- Cast Iron

- SG Iron

- Brass & Bronze

- Others

By Region:

- North America

- Latin America

- Europe

- East Asia

- South Asia and Pacific

- Middle East and Africa

Companies Covered in Sleeves Market

- INEXO Cast Metal Solutions Pvt. Ltd.

- Cangzhou Sefu Ceramic New Materials Co., Ltd.

- Suzhou Xingye Materials Technology Co., Ltd

- ASK Chemicals

- Vesuvius plc

- INTOCAST AG

- Shengquan Group

- Freeman (Japan) Co., Ltd.

- TOCHU Corporation

- Essem Metachem Industries (P) Limited

- Kore Mart Limited

- KITANI Corporation

- Pine Pacific

- Smelko Foundry Products

- Opta Minerals

- Foseco International Limited

Frequently Asked Questions

The global sleeves market was valued at US$ 1,054.4 million in 2025 and is projected to reach US$ 1,564.6 million by 2032, representing a CAGR of 5.8% during the forecast period.

Primary demand drivers include rising automotive production, aerospace sector emphasizing high-quality components with minimal defects, infrastructure development projects worldwide, heavy machinery manufacturing expansion, and emphasis on reducing casting defects and improving yield efficiency through advanced sleeve technologies.

Exothermic Sleeves command the dominant segment at approximately 44% market share, driven by superior defect reduction capabilities, widespread adoption in automotive and machinery manufacturing, and proven effectiveness in maintaining molten metal temperature during solidification.

Asia Pacific dominates with 42.8% global market share, driven by China's position as world's largest steel and metal producer, rapid industrialization, infrastructure development projects, and emerging market opportunities supporting sustained regional growth.

Digital integration and smart foundry technologies including real-time monitoring systems, AI-based process optimization, and embedded sensor systems represent the highest-growth opportunity supporting next-generation casting efficiency and quality improvements attracting technology-focused foundry operators.

Market leaders include Vesuvius plc wwith comprehensive FEEDEX exothermic sleeve portfolio and global manufacturing network, ASK Chemicals (Germany) specializing in EXACTCAST sleeve innovations, and INEXO Cast Metal Solutions Pvt. Ltd. (India) leveraging regional manufacturing capabilities, collectively representing approximately 45-50% market concentration.