- Beverages

- Functional Soda Market

Functional Soda Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Functional Soda Market by Ingredients (Botanical, Fruits, Herbs, Others), Packaging Type (Cans, Bottles), by Sales Channel (Supermarket/Hypermarket, Departmental Stores, Health Stores, Online Retail, Others), by Regional Analysis, 2026 - 2033

Functional Soda Market Share and Trends Analysis

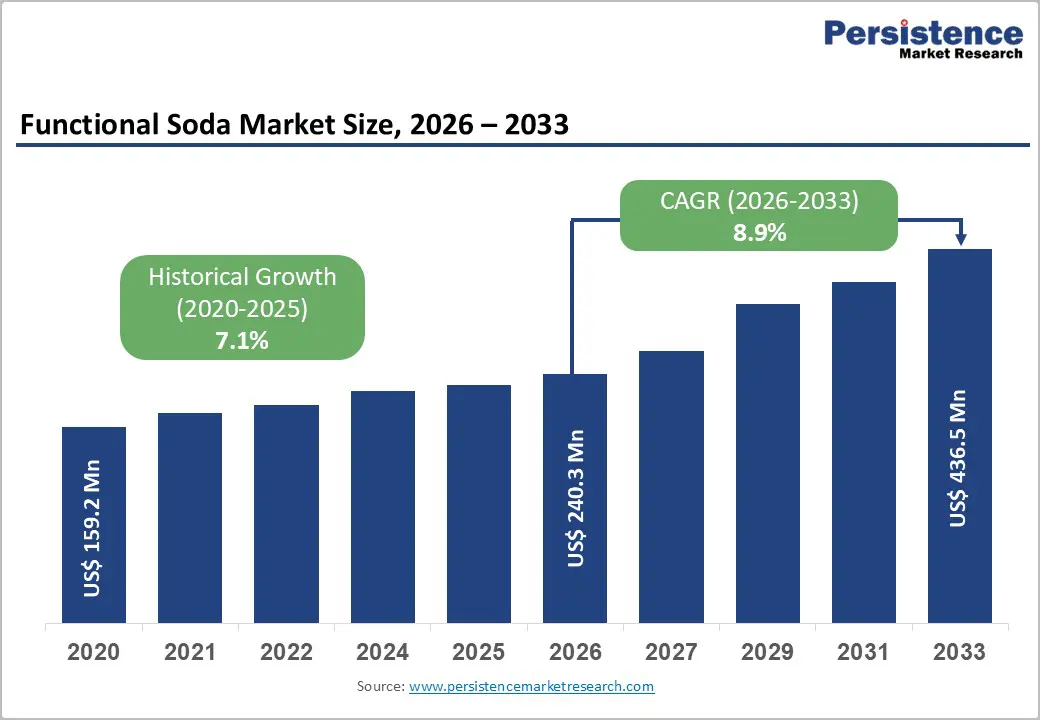

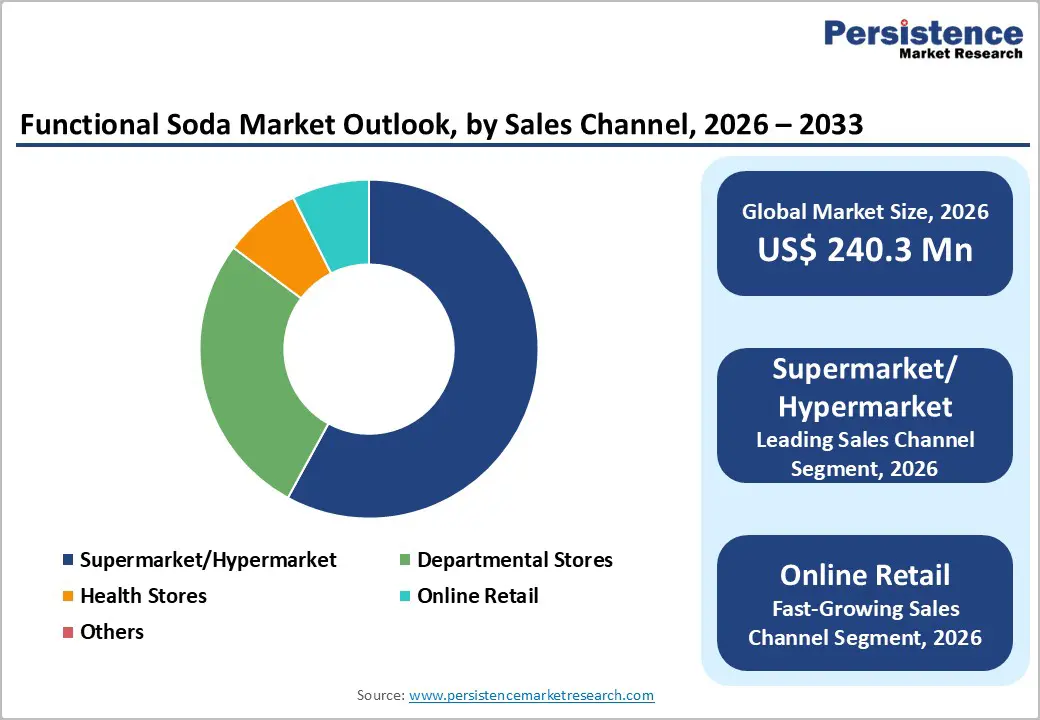

The global functional soda market size is expected to be valued at US$ 240.3 million in 2026 and projected to reach US$ 436.5 million by 2033, growing at a CAGR of 8.9% between 2026 and 2033.

The market is primarily driven by the radical shift in consumer beverage preferences toward low-sugar, health-optimizing alternatives that offer more than basic hydration. Modern consumers are increasingly replacing traditional carbonated soft drinks with functional versions that contain prebiotics, probiotics, and minerals to support gut health and immunity. This growth is further supported by the massive expansion of the clean-label movement and the rising prevalence of lifestyle-related health conditions, prompting a surge in demand for beverages with verified wellness benefits.

Key Industry Highlights:

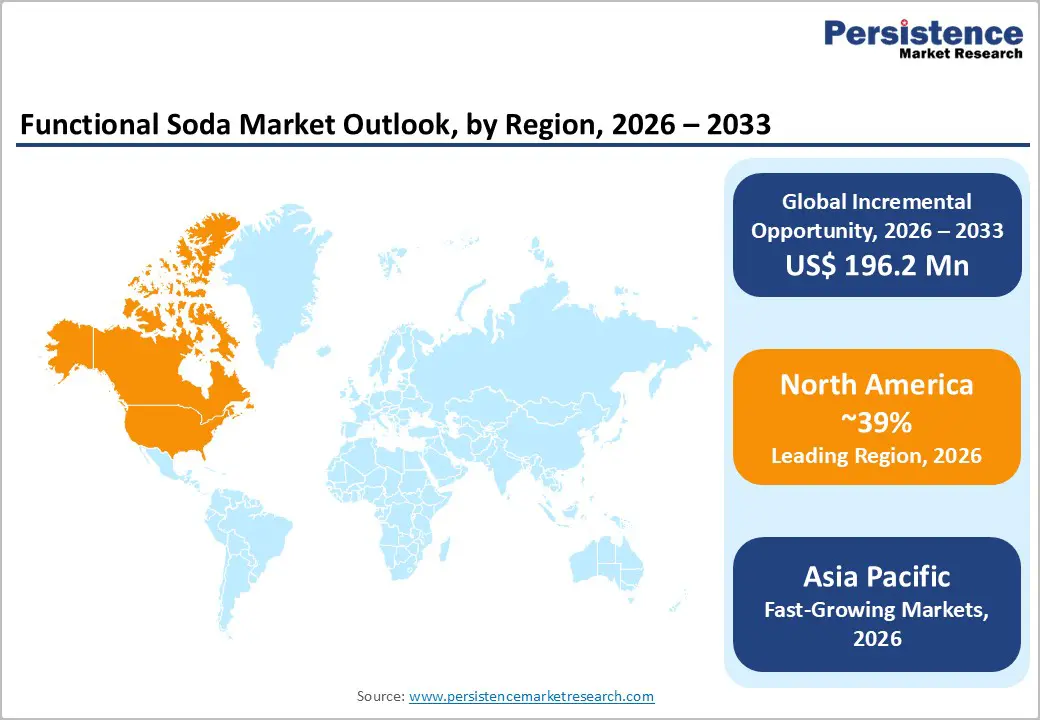

- Leading Region: North America dominates the landscape with a 39% share, fueled by a high concentration of wellness-conscious consumers and a robust venture-backed startup ecosystem in the U.S.

- Fastest Growing Region: Asia Pacific is the fastest-growing market due to the rapid urbanization of China and India and the long-standing cultural acceptance of functional, plant-based medicinal ingredients.

- Dominant Segment: Botanical ingredients lead the market as consumers increasingly trust plant-derived extracts like ginger and turmeric for their perceived natural efficacy and clean-label appeal.

- Fastest Growing Segment: The Herbs ingredient category is expanding at an 11% CAGR, driven by the rising consumer interest in adaptogens and herbal stress-relief solutions.

- Key Opportunity: The expansion of Online Retail and subscription models provides a vital path for niche functional soda brands to scale and collect direct consumer feedback.

| Key Insights | Details |

|---|---|

| Functional Soda Market Size (2026E) | US$ 240.3 Mn |

| Market Value Forecast (2033F) | US$ 436.5 Mn |

| Projected Growth (CAGR 2026 to 2033) | 8.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.1% |

Market Dynamics

Driver - Rise in Prevalence of Sugar-Related Health Concerns and the Soda Tax Influence

The global crackdown on high-sugar beverages by health organizations and governments has catalyzed the growth of the functional soda sector. With the World Health Organization (WHO) advocating for reduced free-sugar intake to combat obesity and type 2 diabetes, over 50 jurisdictions worldwide have implemented some form of sugar-sweetened beverage tax. This regulatory environment has forced a pivot toward functional formulations that use natural sweeteners such as stevia, monk fruit, or erythritol. Data suggests that as traditional soda consumption in the U.S. and Europe continues to stagnate or decline, the functional soda category benefits from a migration of consumers who desire the carbonated experience without the metabolic consequences, effectively filling the void in the market.

Restraints - Premium Pricing Barriers and Inflationary Pressures

A significant restraint on the functional soda market is its high price point relative to conventional carbonated beverages. While a standard soda may retail for under US$ 1.50, functional variants often range from US$ 2.49 to US$ 3.99 per unit due to the cost of premium functional ingredients like ashwagandha, apple cider vinegar, and specialized fiber. Statistics from various retail price index reports indicate that during periods of high inflation, price-sensitive consumers may view functional sodas as a non-essential luxury. This economic barrier limits the mass-market adoption of these products, particularly in emerging economies where the price-per-ounce remains a decisive factor in purchasing behavior.

Opportunity - Expansion of E-Commerce and Subscription-Based Business Models

The rapid growth of the Online Retail sales channel presents a massive opportunity for functional soda brands to bypass traditional retail gatekeepers. Subscription models allow companies to build direct-to-consumer relationships, ensuring recurring revenue and enabling the collection of granular consumer data. During the 2023-2025 period, many digital-native beverage brands reported that online sales accounted for over 30% of their total revenue. By leveraging social media marketing and influencer partnerships, brands can target specific health-conscious demographics more effectively than through traditional television advertising. This digital ecosystem enables rapid testing of new flavors and functional additives, such as l-theanine for stress relief or collagen for skin health, before scaling to physical retail.

Category-wise Analysis

Ingredients Insights

The botanical segment represents the leading ingredient category, holding a 38% market share in 2025. The dominance of botanicals is attributed to their long-standing reputation in traditional medicine and their perceived naturalness by the modern consumer. Ingredients such as ginger, turmeric, and various flower extracts provide both unique flavor profiles and functional benefits like anti-inflammatory properties. Data from the American Botanical Council indicates a steady increase in the retail sale of herbal supplements, a trend that has directly bled into the beverage industry. Furthermore, botanicals often serve as a bridge for consumers who are wary of synthetic additives, providing a clean-label solution that resonates with the transparency demands of the Gen Z and Millennial demographics.

Sales Channel Insights

The Supermarket/Hypermarket segment remains the leading sales channel for functional sodas, accounting for over 45% of global sales. This dominance is driven by the expansion of natural and wellness aisles in major global chains like Walmart, Tesco, and Carrefour. These retailers provide the high-traffic environment necessary for impulse purchases and brand discovery. According to the Food Marketing Institute (FMI), consumers are increasingly using grocery stores as a primary source for health-related products. However, the online retail segment is the fastest-growing channel, as it allows niche brands to reach consumers in regions where local grocery stores may not stock premium functional sodas, proving that digital accessibility is a key growth lever for the industry.

Regional Insights

North America Functional Soda Market Trends and Insights

North America is the leading region in the functional soda market, holding a 39% share in 2025. The United States market leadership is driven by a highly developed innovation ecosystem where venture capital funding for wellness-focused startups is abundant. Brands like Olipop, Inc and Bloom Nu LLC have successfully disrupted the market by targeting the American consumer's desire for nostalgic soda flavors but with a significantly improved nutritional profile.

The regulatory framework in the U.S., overseen by the Food and Drug Administration (FDA), allows for structure-function claims on labels, which helps companies market the benefits of prebiotics and minerals. Moreover, the high density of health-conscious urban populations and the prevalence of specialized retailers like Whole Foods Market provide an ideal testing ground for new functional soda concepts. The region's infrastructure also supports a rapid shift toward e-commerce, which has become a vital channel for growth.

Asia Pacific Functional Soda Market Trends and Insights

The Asia Pacific region is the fastest-growing market for functional sodas, driven by the massive manufacturing advantages and the rapidly evolving consumer landscape in China, Japan, and India. Governments in the region are increasingly focusing on preventive healthcare, with Japan's FOSHU (Food for Specified Health Uses) system serving as a global pioneer in functional food regulation. This has created a high level of consumer trust in beverages that claim specific health benefits, such as weight management or blood sugar control.

In China and India, the growth of the middle class and the rise of the ASEAN economic block are creating millions of new potential consumers. The regional market benefits from a rich heritage of traditional medicine, making consumers naturally inclined toward Botanical and Herbal sodas. Furthermore, the rapid adoption of digital payment systems and food delivery apps has made the Online Retail channel an even more powerful force in Asia Pacific than in the West, allowing for the rapid scaling of domestic functional soda brands.

Competitive Landscape

The functional soda market is currently a fragmented landscape, characterized by a mix of high-growth startups and established global beverage giants. While The Coca-Cola Company and Nestlé have entered the space through strategic acquisitions or internal R&D, much of the innovation is led by agile companies like Olipop, Inc and Bloom Nu LLC. Key strategies for expansion include aggressive retail expansion and the use of social media to build lifestyle brands. Market leaders are increasingly employing a differentiation strategy by obtaining third-party certifications (e.g., Non-GMO Project Verified, Certified B Corp) to build consumer trust. Emerging business trends suggest a shift toward multi-functional sodas that combine gut health with other benefitss like energy or mental clarity.

Key Developments:

- In February 2026, Nestlé expanded its Sanpellegrino portfolio into functional soda with a new vitamin-fortified offering, signaling growing competition in better-for-you carbonated beverages.

- In March 2025, Bloom Nutrition launched Bloom Pop, a prebiotic functional soda, in collaboration with Nutrabolt to strengthen its presence in the gut-health beverage space.

- In February 2025, Olipop raised $50 million in Series C funding to accelerate product innovation, distribution expansion, and brand building in the fast-growing functional soda segment.

Companies Covered in Functional Soda Market

- The Coca‑Cola Company

- Olipop, Inc

- Bloom Nu LLC

- Reed's Inc.

- GuTSY, INC.

- Nestlé

- Don Chico's

- Cove Soda

- Others

Frequently Asked Questions

The global Functional Soda market is projected to be valued at US$ 240.3 Mn in 2026.

Rising Prevalence of Sugar-Related Health Concerns and the Soda Tax Influence is driving demand for Functional Soda market.

The Global Functional Soda market is poised to witness a CAGR of 8.9% between 2026 and 2033.

Expansion of E-Commerce and Subscription-Based Business Models is creating opportunities for key players in the Functional Soda market.

Key industry leaders include The Coca‑Cola Company, Olipop, Inc, Bloom Nu LLC, Reed's Inc., GuTSY, INC., Nestlé, and Others