- Home Appliances

- Foot Massagers Market

Foot Massagers Market Size, Share, and Growth Forecast, 2026 - 2033

Foot Massagers Market by Product Type (Electric Foot Massagers, Manual Foot Massagers, Smart Electric Foot Massagers), Application (Residential, Commercial, Hospitals), Distribution Channel (Online Retail, Offline Retail), and Regional Analysis for 2026-2033

Foot Massagers Market Share and Trends Analysis

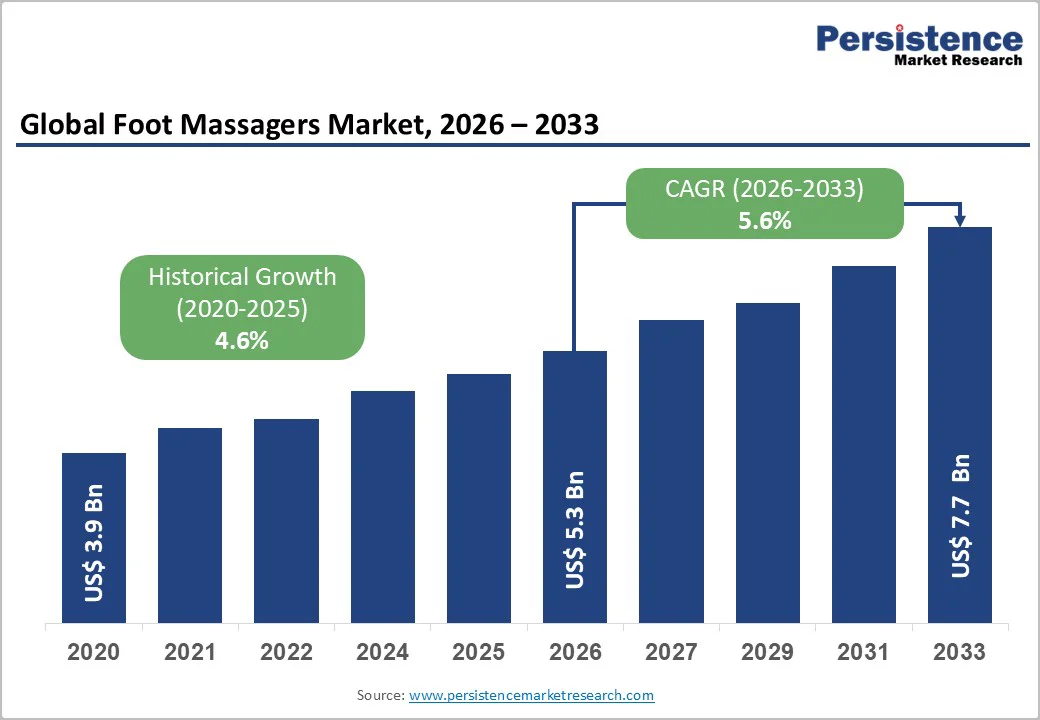

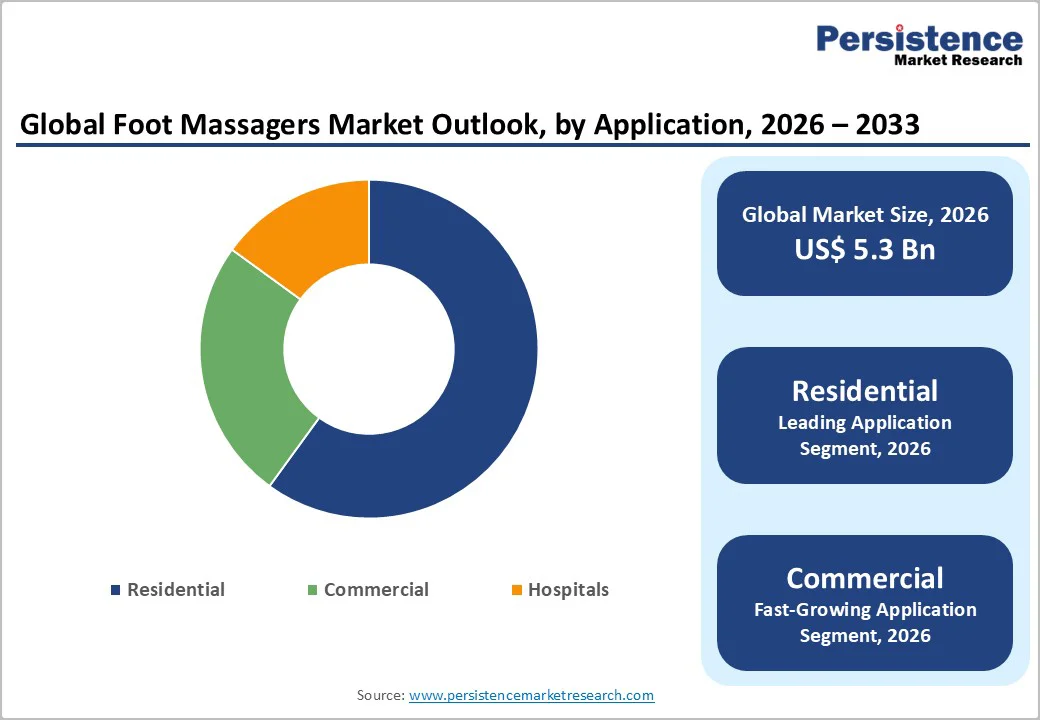

The global foot massagers market size is likely to be valued at US$ 5.3 billion in 2026, and is estimated to reach US$ 7.7 billion by 2033, growing at a CAGR of 5.6% during the forecast period 2026−2033, Rising prevalence of musculoskeletal and lifestyle-related foot pain, growing consumer focus on home wellness, and wider availability of electric and smart massagers across online channels are driving steady growth. Demand is further supported by aging populations, higher disposable incomes in emerging markets, and product innovation such as multifunctional, heated, and app-connected devices that enable at-home therapy and relaxation. Technological advancements also play a crucial role in the market's growth, as manufacturers innovate with new features such as heat therapy, vibrating massage, and customizable intensity settings to enhance user experience.

Key Industry Highlights

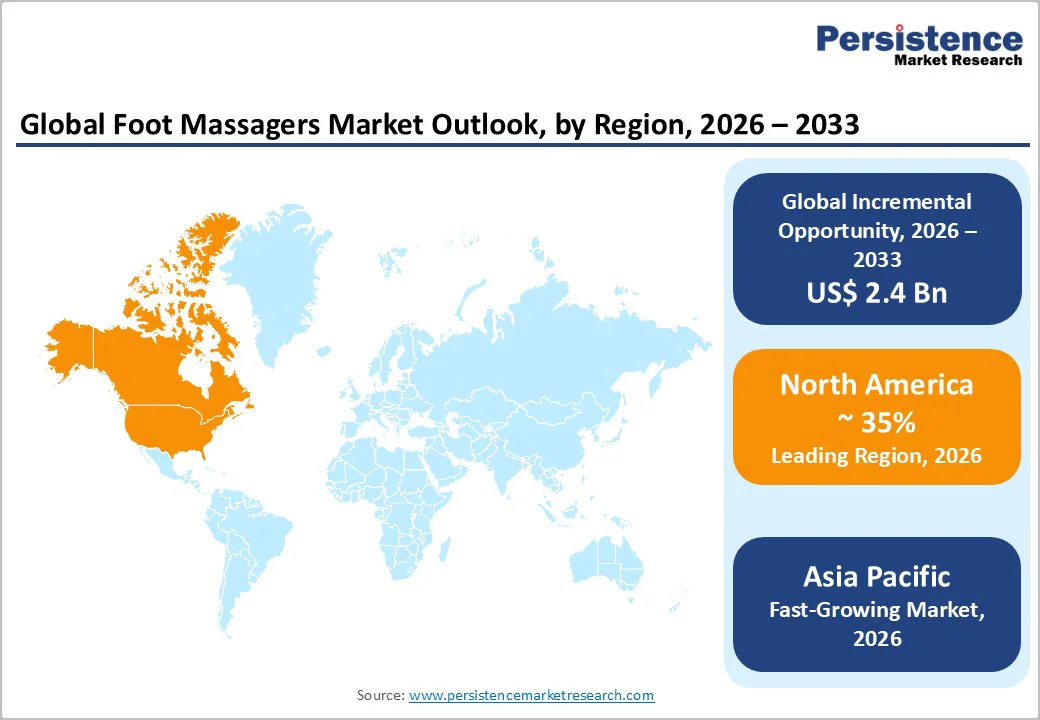

- Dominant Region: North America is expected to command about a 35% market share in 2026, due to consumer awareness of wellness benefits and a cultural emphasis on health and self-care products.

- Fastest-growing Regional Market: Asia Pacific is anticipated to emerge as the fastest-growing market from 2026 to 2033, owing to busy urban lifestyles and a cultural familiarity with massage practices.

- Leading & Fastest-growing Product: Electric foot massagers are likely to lead with approximately 70% revenue share in 2026, while smart massagers are poised to be the fastest-growing from 2026 to 2033.

- Dominant & Fastest-growing Application: Residential applications are slated to dominate with an estimated 60% revenue share in 2026, whereas commercial is expected to be the fastest-growing application during the 2026-2033 period.

- Major Driver: Shifting inclination toward at home wellness and self-care is stoking market growth, as consumers are increasingly choosing to these options to reduce reliance on appointments or spa visits.

- Key Opportunity: Smart, connected, and AI driven technologies are enabling foot massagers to evolve from simple mechanical devices into personalized wellness systems.

| Key Insights | Details |

|---|---|

| Foot Massagers Market Size (2026E) | US$ 5.3 Bn |

| Market Value Forecast (2033F) | US$ 7.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.6% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Shift Toward at Home Wellness and Self-Care

Consumers are increasingly choosing to care for their bodies and minds at home rather than relying solely on appointments or spa visits. They build small, intentional wellness routines into their daily lives using simple tools to unwind after work, relax before sleep, or recover from long hours on their feet. As a result, foot and leg care are shifting from occasional indulgences to consistent habits that sit alongside home fitness, meditation applications, and sleep aids as part of a broader, integrated self-care toolkit. For brands, this creates an opportunity to position foot and leg care not as stand-alone gadgets but as essential components of a daily wellbeing ecosystem that supports stress relief, physical recovery, and long-term health.

Foot massagers are a natural fit within this home wellness context because consumers can use them easily, without special training, and experience immediate, noticeable comfort. Users can plug the device in, select a preset mode, and let it work while they watch television, read, or work from home, which aligns with the growing demand for low-effort, routine-friendly solutions. This preference for convenient, set-and-forget experiences is driving interest in compact, portable, and user-friendly designs that fit seamlessly into small apartments or home offices with minimal setup. Companies that focus on intuitive controls, quiet operation, and space-efficient form factors can better meet the expectations of time-pressed consumers who want effortless relief and consistent self-care at home.

Regulatory, Safety, and Quality Compliance Constraints

Manufacturers must navigate multiple layers of compliance, including electrical safety standards, protection against overheating or electric shock, and rules on electromagnetic compatibility (EMC) to ensure devices do not interfere with other equipment in homes or clinical settings. When products are marketed for pain relief, circulation improvement, or rehabilitation, regulatory bodies scrutinize them under medical device frameworks, which introduce additional expectations around testing, labeling, and clinical evidence. This regulatory scrutiny creates a significant barrier to entry, as companies must demonstrate not only that their products work safely but also that they deliver the therapeutic benefits claimed in their marketing materials.

Selling the same product across multiple regions compounds these challenges considerably, since each market operates under distinct certification processes, documentation standards, and testing protocols. Navigating these systems extends development timelines, increases upfront capital requirements, and necessitates sustained investment in quality management systems and post-market surveillance activities. Larger, established brands typically possess the financial resources and regulatory infrastructure to absorb these demands, whereas smaller manufacturers and new entrants often lack the specialized expertise or quality systems needed to manage compliance effectively. For smaller companies, regulatory complexity can become the decisive factor that determines whether they can compete in international markets or remain confined to their domestic region.

Introduction of Smart and Connected Devices

The advent of smart, connected, and AI-driven technologies is enabling foot massagers to evolve from simple mechanical devices into personalized wellness systems. By integrating sensors, wireless connectivity such as Bluetooth or Wi-Fi, and AI algorithms, these devices can learn individual user preferences, adjust pressure and intensity dynamically, and recommend customized programs for relaxation, recovery after prolonged standing, or targeted relief in specific foot areas. This transformation positions foot massagers as intelligent partners in daily wellness rather than passive tools, creating opportunities for brands to deepen user engagement and build loyalty through personalized experiences that improve over time.

These capabilities also connect foot massagers into the broader smart home and digital health ecosystem, enabling seamless integration with mobile applications and health platforms. Users gain the ability to control devices remotely through smartphones, monitor massage session data, and combine foot massage with complementary wellness actions such as guided breathing exercises, curated music playlists, or sleep optimization routines. Linking foot massagers with mobile applications or smart home platforms will allow manufacturers to deliver software updates, introduce new massage programs, provide guided sessions, and share educational content without requiring physical hardware changes. This software-first approach creates recurring value, extends product lifecycles, and establishes direct relationships between brands and consumers.

Category-wise Analysis

Product Insights

Electric foot massagers are anticipated to be the leading segment with approximately 70% of the market revenue share in 2026. These devices combine convenience with a broad set of functional benefits that manual products cannot match. Rather than relying on simple rolling or pressing, electric massagers typically integrate features such as heat therapy for relaxation, multiple massage modes and intensities, and automatic programs or timers that enable users to enjoy a complete session with minimal effort. The appeal of electric models is further reinforced by the growing preference for tech-enabled, at-home wellness solutions, where consumers expect their devices to be easy to operate, comfortable, and capable of delivering consistent performance over time.

Smart electric foot massagers are likely to be the fastest-growing segment from 2026 to 2033, as they incorporate several benefits into a single device rather than offering only basic vibration or simple rolling. These products typically integrate heat, kneading, vibration, and air compression, and are controlled through digital panels or touch interfaces that let users choose from multiple pre set programs or fine tune intensity and duration. As a result, smart foot massagers are finding widening acceptance among consumers, especially those preferring at-home care models.

Application Insights

The residential segment is slated to dominate with an estimated 60% of the foot massagers market revenue share in 2026. In the residential segment, foot massagers are now woven into everyday self-care routines, as people look for simple ways to ease stress and support circulation without leaving home. Many users treat a short foot massage session as part of their winding-down ritual after work or exercise, alongside activities like stretching, meditation. Residential demand for foot massagers continues to grow, supported by rising awareness of foot health and a strong preference for convenient, in-home relaxation.

The commercial segment is expected to be the fastest-growing application between 2026 and 2033. Spas, wellness centers, gyms, and hospitality venues that use these devices to upgrade their service experience and generate additional revenue per customer. These businesses install automatic or high end foot massagers in waiting areas, relaxation zones, or dedicated massage corners, offering quick, hygienic sessions that can be used between treatments, after workouts, or while guests are in transit.

Distribution Channel Insights

Supermarkets and hypermarkets are poised to lead with an approximate 55% of the foot massagers market share in 2026. These entities remain the popular choice for purchasing foot massagers, owing to their extensive reach and the consumer's ability to physically examine products before purchase. These retail giants offer an assortment of brands and models, often accompanied by promotional deals that attract a broad spectrum of consumers. The in-store shopping experience allows consumers to make informed decisions based on product demonstrations and expert advice available at these outlets.

Online retail is anticipated to be fastest-growing segment during the 2026-2033 forecast period. Online channels now play a central role in how consumers buy foot massagers, largely because they make the entire purchase journey simpler and more transparent. Shoppers can browse a wide range of brands and models, compare features, read user feedback, and check prices from multiple sellers in one place, without needing to visit a physical store.

Regional Insights

North America Foot Massagers Market Trends

North America is predicted to capture around 35% of the foot massagers market share in 2026, driven by widespread consumer awareness of wellness benefits and a strong cultural emphasis on health and self-care products. The region expects steady growth, supported by the adoption of advanced technologies and the presence of established industry leaders who drive innovation and improve product accessibility. The United States serves as the primary growth engine, where consumers increasingly demand sophisticated, multifunctional foot massagers that combine user convenience with high performance capabilities. This preference for feature-rich products reflects the region's affluent consumer base and openness to investing in premium wellness solutions that integrate into broader home health systems.

The regional market operates under robust regulatory oversight for electrical safety and consumer products, with specialized devices claiming therapeutic benefits potentially subject to medical device requirements. This stringent regulatory environment creates competitive advantages for established brands that can invest in compliance infrastructure, quality management systems, and comprehensive liability coverage. Consequently, North America exhibits a moderately consolidated competitive landscape where larger manufacturers with proven regulatory expertise and distribution networks can compete more effectively than smaller or newer entrants. For companies seeking to establish or expand their presence in this market, the combination of high consumer demand and significant regulatory barriers creates both substantial opportunities and considerable operational challenges that demand careful strategic planning and adequate capital resources.

Europe Foot Massagers Market Trends

The Europe foot massager market is distinguished by its diverse consumer demographics and a pronounced commitment to holistic wellness and product quality. Key markets such as Germany, the United Kingdom, and France drive demand, with consumers prioritizing self-care and effective stress management as integral components of their daily routines. European buyers demonstrate a strong preference for premium, high-quality foot massagers, directing spending toward devices that deliver superior durability, advanced functionality, and exceptional performance. This orientation toward premium offerings reflects broader European consumer values around craftsmanship, longevity, and sustainable consumption, positioning quality and reliability as primary purchase drivers.

This consumer preference for high-end products gains further momentum from the expansion of wellness tourism, established spa culture, and an aging population increasingly seeking therapeutic benefits within home and commercial environments. Both residential consumers and hospitality venues such as spas, wellness centers, and hotels are generating robust demand for feature-rich foot massagers that support their wellness missions. The dual demand from individual households and professional settings has opened multiple revenue channels for manufacturers and reinforced the market opportunity for products that combine therapeutic effectiveness with premium design. Europe's aging demographic trends further brighten long-term market outlook, as older consumers often prioritize mobility, pain management, and preventive health measures that foot massage devices effectively address.

Asia Pacific Foot Massagers Market Trends

Asia Pacific is anticipated to emerge as the fastest-growing foot massagers market through 2033, driven by rapid adoption across key markets including China, India, and ASEAN countries. Consumers in these markets actively seek convenient solutions to manage stress, fatigue, and lifestyle-related physical discomfort within homes and wellness centers. This growth momentum reflects rising health consciousness, accelerating urbanization with increasingly demanding work schedules, and deep cultural acceptance of massage as a therapeutic practice.

The region possesses substantial manufacturing infrastructure that creates competitive advantages for brands operating in Asia Pacific. China and other Asian economies host extensive original equipment manufacturer (OEM) and original design manufacturer (ODM) facilities that serve both multinational brands and local private-label producers, resulting in a diverse product portfolio spanning entry-level devices to premium smart systems. Simultaneously, regulators in major markets are progressively strengthening requirements around electrical safety, product labeling, and online marketplace compliance standards. This regulatory tightening creates a market shift that increasingly favors reputable, quality-focused brands over unverified low-cost imports, suggesting that manufacturers prioritizing compliance and product integrity can capture meaningful share growth.

Competitive Landscape

The global foot massagers market displays a moderately concentrated structure, dominated by key players such as Panasonic Corporation, OSIM International, HoMedics, and Beurer GmbH. These leaders collectively command an estimated 55% market share in 2026 through their strong presence across multiple regions and robust distribution networks. They maintain competitive advantages by allocating substantial resources to research and development, which fuels product innovation and line expansions tailored to shifting consumer preferences. This strategic focus on continuous improvement enables established firms to sustain leadership positions amid growing demand for advanced wellness solutions.

Several leading companies are utilizing contract manufacturing partnerships in Asia to control production costs while testing innovative features and direct-to-consumer sales channels. At the lower market tier, hundreds of generic and online-only brands offer budget-priced devices, which heighten price competition but often fall short on regulatory compliance and lasting brand trust. This bifurcated landscape underscores the value of differentiation through quality, innovation, and reliability for manufacturers aiming to ascend from commodity providers to premium category dominators.

Key Industry Developments

- In November 2025, Fit King launched its 2025 Black Friday mega sale, featuring steep discounts on advanced home recovery devices such as foot and leg massagers. The promotion highlights next-generation technology designed for consumer wellness and recovery.

- In June 2025, Renpho upgraded its Heated Foot Massager Machine to deliver Shiatsu kneading, adjustable heat up to 131°F, and air compression for arch/heel relief, ideal for plantar fasciitis and daily unwind. It was at its lowest price of US$ 85 on Amazon, while being FSA/HSA eligible, compact, quiet, with washable covers, and fitting men's size 12 or smaller.

- In May 2025, Nooro Foot Massager received positive reviews for its deep Shiatsu kneading, heat therapy, and portability, targeting foot pain, plantar fasciitis, and circulation issues with customizable intensity levels. Priced affordably with strong user feedback on comfort and effectiveness, it stands out as a home wellness solution amid growing demand for convenient recovery devices.

Frequently Asked Questions

The global foot massagers market is projected to reach US$ 5.3 billion in 2026.

Rising foot discomfort, at‑home wellness adoption, aging populations, and tech‑enhanced, multifunctional electric devices are driving the market.

The market is poised to witness a CAGR of 5.6% from 2026 to 2033.

Smart connected devices, emerging markets, institutional adoption, and personalized, data‑driven wellness ecosystems are opening new market opportunities.

Panasonic Corporation, OSIM International, HoMedics, Beurer GmbH are some of the key players in the market.