- Clothing, Footwear, & Accessories

- Skateboard Footwear & Apparel Market

Skateboard Footwear & Apparel Market Size, Share, and Growth Forecast, 2026 – 2033

Skateboard Footwear & Apparel Market by Product Type (T-shirts & Tops, Skate Shoes, Hoodies & Sweatshirts, Bottoms), Consumer Orientation (Men, Women, Unisex, Kids), Distribution Channel (Direct Sales, Specialty Stores, Sports Merchandise, Departmental Stores, Online Retailers), and Regional Analysis for 2026-2033

Skateboard Footwear & Apparel Market Share and Trends Analysis

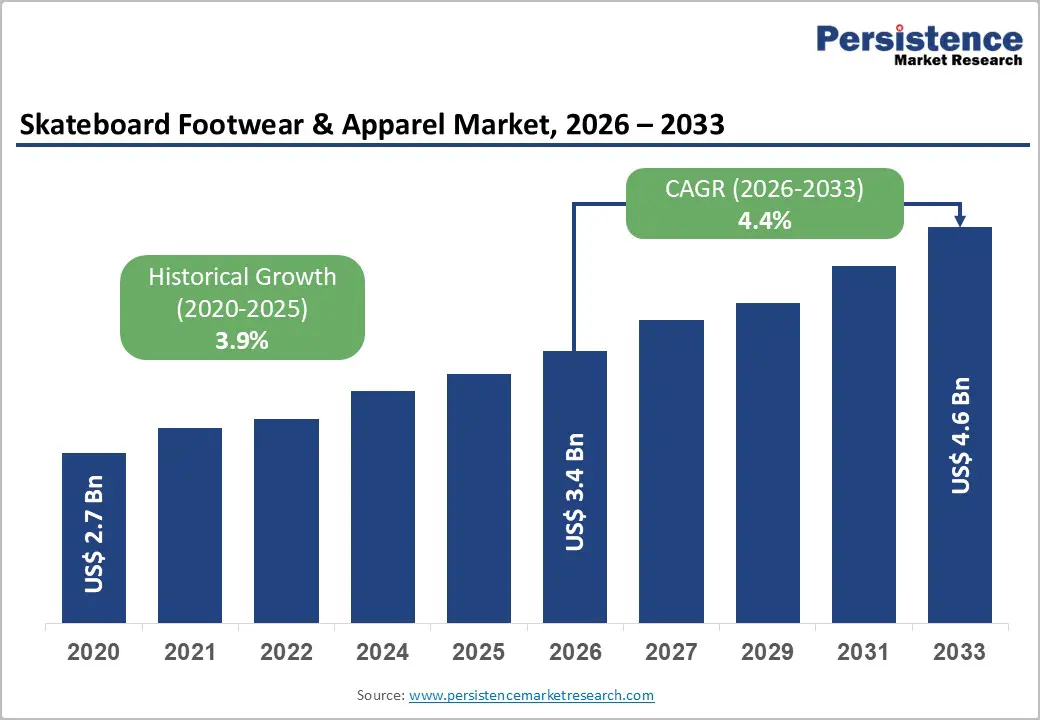

The global skateboard footwear & apparel market size is likely to be valued at US$ 3.4 billion in 2026, and is projected to reach US$ 4.6 billion by 2033, growing at a CAGR of 4.4% during the forecast period 2026−2033. Growth outlook remains stable due to sustained participation in skateboarding as both sport and lifestyle category. Expansion results from demographic concentration among urban youth populations, increased recognition of skateboarding as an organized sport by bodies such as the International Olympic Committee (IOC), rising adoption of specialized footwear designed for board grip and injury prevention, integration of advanced textiles improving durability and comfort, and expansion of retail infrastructure across emerging urban centers.

Participation trends influence apparel demand through identity-driven consumption patterns linked with street culture and athletic fashion. Technical product innovation enhances performance attributes such as impact absorption and abrasion resistance, reinforcing replacement cycles. Infrastructure development including skate parks and urban recreation programs improves accessibility, strengthening equipment and apparel utilization frequency.

Key Industry Highlights

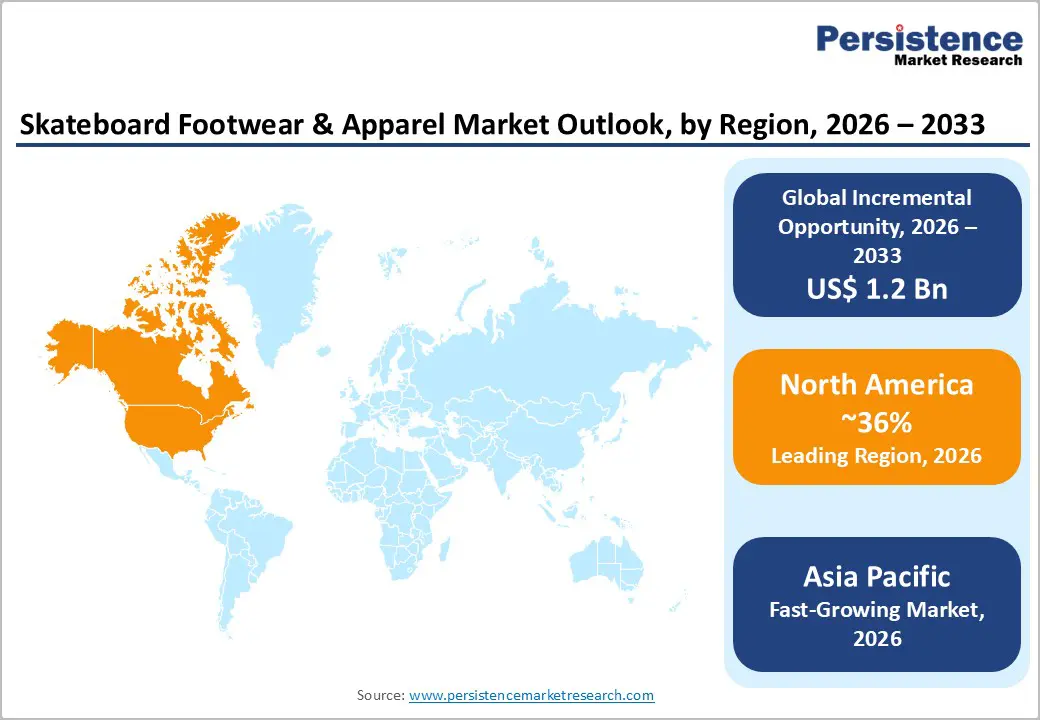

- Dominant Region: North America is projected to hold around 36% of the skateboard footwear and apparel market share in 2026, driven by sport, fashion, and tech integration.

- Fastest-growing Regional Market: Asia Pacific is forecasted to be the fastest-growing market between 2026 and 2033, fueled by urban sports, youth participation, and regional manufacturing.

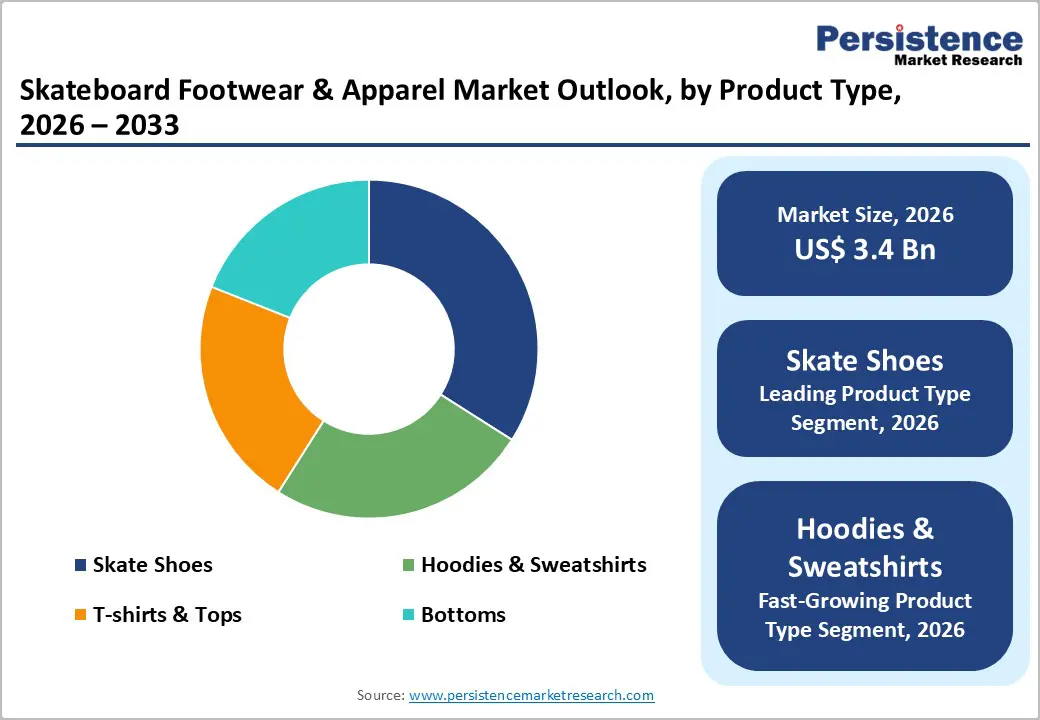

- Leading Product Type: Skate shoes are set to lead with 34% of the market in 2026, supported by sport necessity, high replacement, injury prevention, and broad retail accessibility.

- Fastest-growing Product Type: Hoodies and sweatshirts are set to grow fastest between 2026 and 2033, driven by lifestyle adoption, streetwear influence, brand collaborations, and digital retail expansion.

- February 2026: Adidas AG and Metalwood Studio launched their first golf capsule combining Y2K street style with performance apparel and footwear.

| Key Insights | Details |

|---|---|

| Skateboard Footwear & Apparel Market Size (2026E) | US$ 3.4 Bn |

| Market Value Forecast (2033F) | US$ 4.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Urban Youth Participation Expansion

Participation growth among city-based young populations functions as a structural demand catalyst for skate-style fashion segments. Urban districts concentrate skate parks, street-sport zones, and youth recreation programs, producing dense participation clusters that translate into frequent apparel rotation, style experimentation, and peer-driven trend diffusion. Government-supported activity expansion reinforces this ecosystem. Official records from the Jammu and Kashmir Sports Council indicate about 2.7 million youths engaged in structured sports during 2024–25, reflecting institutional success in embedding sports into everyday youth culture. Concentrated participation elevates visibility of sport-inspired aesthetics in schools, transit hubs, and digital content, positioning performance-inspired clothing as identity markers rather than functional gear.

City environments accelerate diffusion cycles through social media micro-communities, campus groups, and public event circuits, producing rapid adoption curves for footwear silhouettes, oversized fits, and graphic layers associated with skating culture. Informal sport formats attract teenagers seeking low-cost, flexible recreation, which raises frequency of casual practice sessions and therefore increases wear-and-tear replacement demand for shoes and apparel. Urban infrastructure density shortens distance between retail, sport venues, and peer networks, enabling faster product discovery and impulse acquisition. Retailers respond through localized drops, pop-up collaborations, and influencer tie-ins targeted at metropolitan youth clusters.

Material Innovation and Performance Engineering

Advanced textile systems, impact-resistant foams, abrasion-tolerant fabrics, and moisture-control constructions shape product differentiation within this sector. Technical design priorities align with biomechanical demands such as shock absorption during landings, board-feel precision, grip traction, and thermal comfort. Engineering teams integrate layered midsoles, vulcanized rubber compounds, and reinforced stitching zones to reduce failure rates under repetitive stress. Performance validation protocols using lab abrasion rigs and flex-cycle testing create measurable durability benchmarks that guide procurement decisions among retailers and sports institutions. Government health policy frameworks reinforce this innovation focus, noting that structured athletic participation supports physical fitness, cognition, and skill development, which strengthens demand for specialized gear built for safety and efficiency.

Competitive branding strategies emphasize engineered functionality as a value signal rather than aesthetic novelty. Material science adoption allows manufacturers to communicate technical credibility through data-supported claims such as tensile strength, friction coefficient, or energy return metrics. Supply chains integrate advanced polymers, recycled composites, and knit structures that meet regulatory expectations for product safety while improving wear longevity. Retail channels prioritize items with certified performance attributes, as institutional buyers and training programs seek equipment aligned with injury-reduction objectives. Investment flows toward research laboratories, athlete testing panels, and digital prototyping platforms that shorten development cycles and raise specification accuracy.

Counterfeit Distribution and Brand Dilution

Illicit imitation networks weaken pricing authority, reduce trademark differentiation, and disrupt channel discipline across branded action-sports merchandise segments. Official enforcement data reported in 2025 by the European Commission (EC) indicates about 112 million counterfeit goods valued near €3.8 billion were detained during 2024 inspections, demonstrating industrial-scale replication activity rather than isolated infringement. Such volume signals structured supply systems capable of rapid design copying and large-batch distribution. Parallel informal sellers introduce replicas at artificially low price points, shifting reference pricing in consumer perception and compressing margins for legitimate producers. Visual similarity between authentic and fake products diminishes logo recognition value and erodes exclusivity perception, a core factor influencing purchase decisions in style-driven footwear and apparel categories.

Organized counterfeit operations rely on distributed production clusters, independent labeling units, and fragmented logistics routes that mask origin trails and complicate enforcement monitoring. Digital marketplaces accelerate circulation speed, allowing imitation listings to appear within hours of authentic product launches, which weakens promotional return on investment and reduces lifecycle profitability. Retail partners face elevated reputational exposure when imitation goods enter inventory streams through unauthorized wholesalers. Material inferiority in fake merchandise increases probability of performance failure, yet negative consumer experience often transfers to legitimate brand reputation due to misidentification of source.

Safety Concerns and Injury Risks

Elevated perception of physical risk restricts participation across recreational users, retailers, and training institutions. Reports of fractures, concussions, and ligament trauma create caution among guardians, insurers, and municipal authorities, shaping purchasing patterns and event approvals. Footwear grip reliability, abrasion resistance, and impact absorption remain under scrutiny, raising product testing intensity and certification costs. Design teams face pressure to balance board control, comfort, and protection, which extends development cycles and limits rapid product turnover. Media coverage of accident incidents strengthens public sensitivity toward liability exposure, prompting stricter venue rules and supervision standards.

Skill variability and urban terrain complexity intensify incident probability, reinforcing caution across stakeholder groups. Uneven pavement, traffic proximity, and trick-focused culture raise fall exposure, directing attention toward protective apparel standards and liability frameworks. Manufacturers encounter rising compliance documentation, labeling obligations, and material verification protocols, which increase administrative load and extend time to market. Brand positioning strategies shift toward safety messaging, limiting emphasis on style innovation and lifestyle branding. Event organizers, schools, and sports clubs apply strict participation criteria, reducing entry of new participants and narrowing addressable demand. Insurance providers adjust premium structures for venues and training programs, influencing operating budgets and partnership feasibility.

Proliferation of Digital Commerce and Customization Platforms

Digital retail infrastructure and product personalization frameworks represent a structural opportunity due to rapid expansion of digital payment ecosystems and mobile commerce access across emerging consumer segments. High transaction frequency across online payment networks signals strong platform familiarity, reduced checkout friction, and elevated trust in online financial flows, enabling brands to deploy direct-to-consumer channels with lower acquisition cost and faster conversion cycles. Data-rich purchase trails generated through these platforms strengthen demand forecasting, targeted promotions, and inventory optimization, raising margin efficiency while lowering stock-out risk in seasonal or trend-driven product categories.

Customization platforms strengthen commercial advantage through algorithm-driven sizing tools, design configurators, and preference tracking engines that translate consumer interaction into differentiated product output. Personalized design modules enhance perceived value while limiting price sensitivity, supporting premium positioning strategies. Integrated analytics from digital storefronts enable micro-segmentation based on activity, style preference, and purchase timing, allowing precise campaign deployment and dynamic pricing structures. Operational integration between manufacturing systems and configuration interfaces shortens production cycles for individualized orders, improving fulfillment speed and working-capital rotation.

Technological Convergence with Electric Skateboarding

Integration of smart mobility technology with electric skateboards creates a strategic growth avenue for skateboard footwear and apparel manufacturers. Sensor-enabled boards, mobile application connectivity, and battery performance upgrades reshape rider expectations toward performance-oriented gear. Footwear design now aligns with vibration control, shock absorption, and grip optimization suited for powered riding speeds. Apparel producers respond through aerodynamic fabrics, abrasion-resistant textiles, and climate-adaptive materials tailored for longer commute sessions. Product development teams gain scope for premium pricing through functional differentiation tied to electric riding dynamics. Retail positioning shifts from lifestyle orientation toward performance mobility segment, expanding consumer base across urban commuters, tech enthusiasts, and micro-mobility adopters.

Rising adoption of electric skateboards within metropolitan transport networks stimulates cross-industry collaboration between wearable technology firms, component suppliers, and sportswear brands. Integrated lighting, reflective panels, impact monitoring chips, and app-synced safety indicators elevate value perception of footwear and apparel lines. Such convergence supports data-driven customization, enabling manufacturers to tailor cushioning density, sole geometry, and fabric ventilation according to ride analytics. Distribution channels benefit from technology partnerships that strengthen product credibility and attract investors seeking mobility-aligned consumer goods segments. Competitive differentiation emerges through patentable materials, embedded electronics, and modular gear systems compatible with evolving board specifications.

Category-wise Analysis

Product Type Insights

Skate shoes are poised to lead with a forecasted 34% of the skateboard footwear & apparel market revenue share in 2026, owing to functional necessity within the sport and high replacement frequency due to wear from grip tape friction. Clinical acceptance parallels protective equipment logic, since proper footwear reduces foot fatigue and impact stress. Treatment effectiveness analogy applies through injury prevention attributes such as reinforced toe caps and padded collars. Provider preference aligns with recommendations from sports trainers who emphasize specialized footwear for performance safety. Accessibility remains strong because footwear appears in multiple price tiers across retail channels. Adherence levels remain high since participants require shoes for each session.

Hoodies & sweatshirts are anticipated to be the fastest-growing segment between 2026 and 2033, fueled by expanding adoption as lifestyle apparel beyond active participation. Cultural acceptance extends into mainstream fashion influenced by streetwear aesthetics. Consumer trust strengthens through brand collaborations with professional skateboarders. Retail penetration increases as apparel lines appear in department stores and digital marketplaces. Preventive healthcare analogy applies through thermal regulation and injury protection during practice sessions. Digital commerce expansion supports global reach for limited-edition designs. Innovation includes sustainable fabrics and ergonomic tailoring enhancing mobility.

Consumer Orientation Insights

Men are likely to be the leading segment with a projected 41% market share in 2026, due to historically higher participation rates in skateboarding communities and strong cultural association between male youth identity and action sports. Brand sponsorship investments concentrate on male athlete ambassadors, reinforcing visibility across competitions, video content, and social media campaigns. Product development strategies prioritize durability standards, wider size ranges, and performance testing aligned with intensive riding patterns. Event organizers frequently design contests and leagues targeting male participation clusters, strengthening segment dominance. Pricing structures reflect strong demand elasticity within this demographic, supporting premium collections and limited releases. Distribution agreements with urban retailers, sporting chains, and online marketplaces sustain availability across regions.

Women are expected to grow the fastest between 2026 and 2033, driven by rising inclusion initiatives and visibility of female athletes in international competitions. Investment flows toward women focused skate programs, training clinics, and sponsorship pipelines designed to expand participation depth. Apparel designers respond with tailored fits, lightweight protection materials, and color palettes aligned with consumer research insights. Footwear brands introduce cushioning geometries calibrated for lower average body mass metrics, improving comfort and control. Community events, workshops, and digital forums strengthen engagement and brand loyalty. Retail analytics show rising conversion rates among female buyers across e commerce channels.

Regional Insights

North America Skateboard Footwear & Apparel Market Trends

North America is expected to dominate with an estimated 36% of the skateboard footwear & apparel market share in 2026, reflecting a structurally integrated ecosystem spanning United States, Canada, and Mexico that links sport participation, fashion commercialization, and technology adoption. Market leadership stems from dense concentration of performance footwear innovators, advanced textile laboratories, and action sports marketing agencies that collectively accelerate product differentiation cycles. Established competition circuits and professional leagues generate continuous demand signals that guide inventory planning and design investment. Retail consolidation across specialty skate outlets and omnichannel platforms strengthens price control and brand positioning. High discretionary expenditure among youth demographics supports premium product tiers, enabling manufacturers to maintain margins while funding research in sole traction engineering, shock dispersion layers, and abrasion resistant fabrics aligned with high intensity riding environments.

Sustained dominance is primarily driven by synchronized collaboration across manufacturers, event organizers, digital media producers, and athlete networks that amplify product visibility and shorten adoption timelines across these economies. Distribution efficiency benefits from sophisticated warehousing systems, predictive demand analytics, and rapid fulfillment infrastructure that reduce stock imbalances. Licensing agreements with entertainment brands and street culture labels create limited release collections that stimulate urgency driven purchasing behavior. Institutional support through school programs, urban recreation facilities, and training academies sustains participation inflow, ensuring recurring demand for footwear replacements and apparel upgrades.

Europe Skateboard Footwear & Apparel Market Trends

Europe demonstrates strong positioning in skateboard footwear and apparel through a market structure shaped by regulatory standards, design innovation, and cultural integration of skateboarding within urban creative economies. Strict product compliance frameworks across Germany and France encourage manufacturers to adopt high-grade materials, certified safety components, and environmentally responsible production methods, elevating perceived product quality. Fashion capitals influence global streetwear direction, enabling skate brands to align collections with runway trends and seasonal style cycles. Public infrastructure planning incorporates multipurpose plazas and skate friendly architecture, sustaining participation visibility. Specialty boutiques and concept stores emphasize curated merchandising, which supports premium pricing strategies and strengthens brand differentiation within competitive retail landscapes.

Market expansion momentum emerges from cross-industry collaboration linking sportswear firms, sustainability innovators, and digital customization platforms across United Kingdom and Netherlands. Demand patterns reflect preference for ethically sourced fabrics, recyclable soles, and low-emission manufacturing, prompting companies to invest in traceable supply chains and circular product lines. Independent skate labels gain traction through limited production runs and localized branding narratives that resonate with urban youth culture. E-commerce penetration supports direct engagement models where brands analyze rider data to refine fit, cushioning density, and durability specifications.

Asia Pacific Skateboard Footwear & Apparel Market Trends

Asia Pacific is forecasted to be the fastest-growing market for skateboard footwear & apparel between 2026 and 2033, stimulated by rapid transformation of youth recreation economies and expansion of urban lifestyle sports infrastructure across Asia Pacific. Metropolitan development programs increasingly allocate space for skate parks, mixed-use sports zones, and public activity corridors, creating consistent participation pipelines that translate into recurring product demand. Rising disposable income among urban middle-income populations supports transition from entry-level gear toward performance-grade footwear and technical apparel. Regional manufacturing ecosystems supply advanced textiles, molded soles, and reinforced stitching components at competitive cost structures, enabling brands to scale production volumes while preserving margin stability. Climate-diverse geography encourages development of specialized materials engineered for humidity control, heat resistance, and surface grip optimization, strengthening product relevance across varied environments.

Growth acceleration is driven primarily by digitally integrated retail architecture that allows emerging labels to access consumers directly through mobile commerce platforms and livestream sales channels. Algorithm-driven merchandising enables precise targeting based on activity level, style preference, and price sensitivity, improving conversion efficiency. Regional entertainment industries and street culture networks amplify visibility of skate aesthetics through music videos, gaming collaborations, and influencer partnerships that shape purchasing intent. Investment flows toward sportswear startups foster experimentation with recyclable composites, lightweight cushioning foams, and sensor-compatible garments aligned with evolving mobility trends.

Competitive Landscape

The global skateboard footwear and apparel market structure remains moderately fragmented due to the coexistence of multinational athletic corporations and culturally rooted skate labels operating with distinct strategic models. Major revenue concentration sits with Nike, Inc., Adidas AG, and VF Corporation, which leverage diversified product portfolios, advanced material research, and global distribution systems to secure strong shelf visibility and brand recall. Scale advantages allow these firms to invest heavily in athlete sponsorships, digital campaigns, and rapid product iteration cycles. Specialist skate companies such as HUF Worldwide, Globe International, and Sole Technology operate with focused branding strategies that emphasize subculture credibility, technical riding performance, and limited release collections designed to maintain exclusivity perception among core participants.

Competitive intensity remains shaped by differentiation variables rather than price competition alone. Distribution reach through retailers such as CCS and Tactics determines product accessibility across urban consumer clusters, influencing purchasing frequency and brand switching probability. Authenticity signaling through rider collaborations and grassroots event sponsorships strengthens market positioning for labels including Element that rely on community alignment rather than mass advertising scale. Innovation capability in cushioning systems, abrasion resistant fabrics, and board feel sole engineering functions as a core competitive lever, since performance credibility directly affects adoption among experienced riders.

Key Industry Developments

- In February 2026, Louis Vuitton introduced the LV Tilted sneaker “Skateboard P”, a skate-inspired luxury model blending heritage house codes with playful proportions and streetwear influences to create a new footwear category within the brand.

- In February 2026, Vans reintroduced its iconic Skate Era silhouette to mark 50 years of Vans Skateboarding, launching the new Skate Era WaffleCup™ with advanced outsole technology that combines cupsole support with vulcanized board feel for modern skate performance.

- In September 2025, New Balance Numeric redesigned and launched the classic 1990s-era 770 tennis trainer into a skateboarding shoe, incorporating stability features such as a reinforced footframe system, molded performance insoles, and lace-protection elements while maintaining a lifestyle-focused hybrid design.

Companies Covered in Skateboard Footwear & Apparel Market

- HUF Worldwide

- Adidas AG

- CCS

- Globe International

- VF Corporation

- Tactics

- Nike, Inc.

- Sole Technology Inc.

- Element

- New Balance

- High Speed Productions Inc.

- DC Shoes

- NHS Inc.

- Volcom, LLC

- Lakai Limited

Frequently Asked Questions

The global skateboard footwear & apparel market is projected to reach US$ 3.4 billion in 2026.

Demand growth in the market is driven by rising participation in skate culture, expansion of urban sports infrastructure, strong influence of streetwear fashion, and continuous innovation in performance materials and design.

The market is poised to witness a CAGR of 4.4% from 2026 to 2033.

Key market opportunities lie in electric skateboard integration, digital commerce expansion, gender-inclusive product lines, and sustainable, performance-driven footwear and apparel innovations.

Some of the key market players include HUF Worldwide, Adidas AG, CCS, Globe International, VF Corporation, Tactics, Nike, Inc., Sole Technology Inc., and Element.