- Plastics, Polymers & Resins

- Footwear Sole Material Market

Footwear Sole Material Market Size, Share, and Growth Forecast, 2025 - 2032

Footwear Sole Material Market By Material Type (Polyurethane (PU and TPU), Ethylene-Vinyl Acetate (EVA), Others), Product Type (Athletic Footwear, Casual/Lifestyle Footwear, Others), End-user, and Regional Analysis for 2025 - 2032

Footwear Sole Material Market Size and Trends Analysis

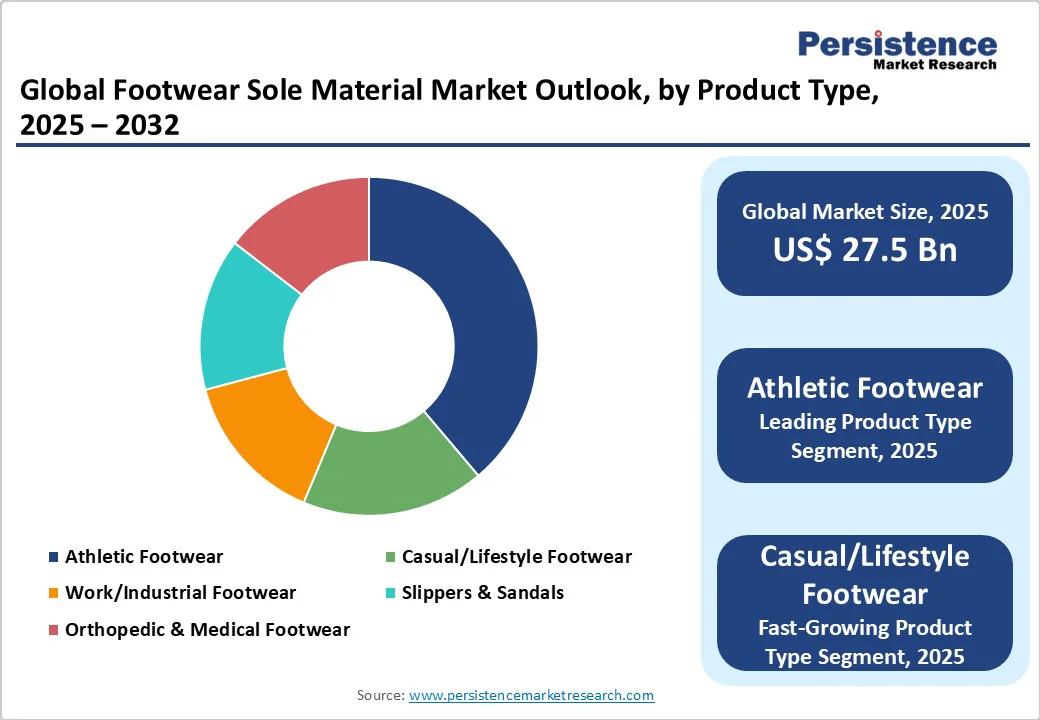

The global footwear sole material market size is likely to be valued at US$27.5?Billion in 2025 and is expected to reach US$39.3 Billion by 2032, growing at a CAGR of approximately 5.1% during the forecast period from 2025 to 2032, driven by the rising demand for lightweight, comfortable, and sustainable footwear solutions. Consumers are increasingly favoring athletic and athleisure footwear that uses advanced midsole and outsole materials offering cushioning, durability, and energy efficiency.

Expansion in online retail channels and heightened awareness of environmentally friendly manufacturing practices also contribute to market expansion. Continuous innovation in polymer technology and bio-based material development further enhances product performance, enabling brands to differentiate through design and sustainability.

Key Industry Highlights

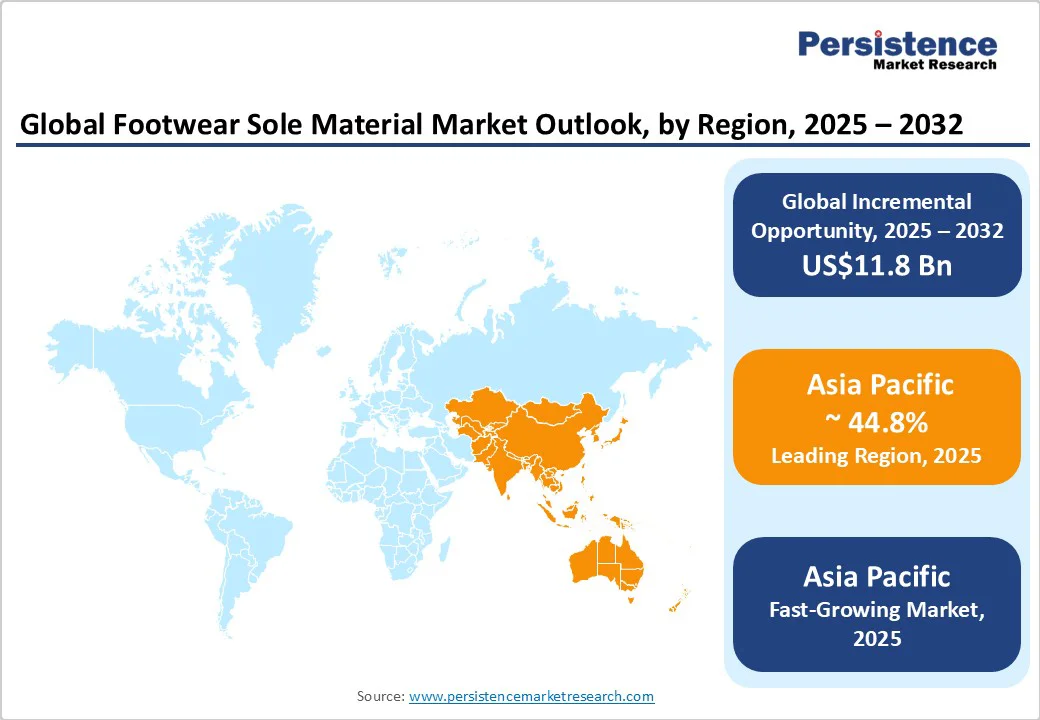

- Leading Region: Asia Pacific, accounting for over 44.8% of the market share in 2025, driven by large-scale manufacturing hubs in China, Vietnam, and India.

- Fastest-growing Region: Asia Pacific supported by rapid industrialization, export growth, and expanding domestic footwear brands.

- Investment Plans: Major players such as BASF SE and Covestro AG are investing in bio-based polyurethane and recycled rubber technologies, with over US$500 Million allocated globally toward sustainable material R&D and automation facilities by 2027.

- Dominant Product Type: Athletic Footwear contributed around 40.3% of total demand in 2025, reflecting high material usage per unit and continuous innovation in cushioning, traction, and stability.

- Leading Material Type: Polyurethane (PU) and Rubber Compounds captured nearly 51% of the market share in 2025 due to durability, flexibility, and widespread adoption across athletic and casual footwear.

| Key Insights | Details |

|---|---|

|

Footwear Sole Material Market Size (2025E) |

US$27.5 Bn |

|

Market Value Forecast (2032F) |

US$39.3 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.1% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Demand for Performance and Athleisure Footwear

The ongoing popularity of athletic and athleisure footwear has significantly influenced the footwear sole material market. Increasing participation in fitness activities, coupled with lifestyle shifts toward casual and sporty attire, is driving manufacturers to use high-performance materials such as thermoplastic polyurethane (TPU), ethylene-vinyl acetate (EVA), and advanced rubber compounds. Athletic footwear currently represents the largest application segment by value. The growing emphasis on energy return, shock absorption, and lightweight design has accelerated R&D investments by brands such as Nike, Adidas, and Puma, boosting the usage of multi-density soles and hybrid compounds.

Growing Focus on Sustainable and Recyclable Materials

Sustainability has become a central focus in the footwear industry, prompting widespread adoption of recyclable and bio-based materials. Manufacturers are experimenting with natural rubber, algae-based foams, and biodegradable thermoplastics to reduce environmental impact. Several leading footwear brands have committed to net-zero carbon targets by 2030, driving the need for eco-friendly sole materials. These sustainable alternatives not only lower carbon emissions but also support premium pricing strategies in Western markets.

Technological Innovation in Manufacturing Processes

Automation, additive manufacturing, and 3D printing are reshaping footwear sole production. Robotic spraying, advanced molding, and laser sintering allow for precision-engineered soles that optimize material usage and reduce waste. These innovations enable brands to customize footwear, reduce lead times, and improve design flexibility. Manufacturing technology investments are particularly notable in North America and Asia Pacific, where major players are adopting hybrid production models combining automation and sustainable raw materials. The integration of smart factory systems supports scalable, efficient, and localized manufacturing, reducing dependency on low-cost offshore production.

Barrier Analysis - Raw Material Price Volatility and Supply Chain Dependence

Sole materials rely heavily on petrochemical feedstocks, exposing manufacturers to significant cost fluctuations linked to crude oil prices. Variations in resin and chemical pricing can directly affect profit margins for footwear brands and OEMs. Supply chain disruptions, including delays in polymer shipments or shortages of specialty additives, have compounded these challenges. Given that raw materials account for 40–50% of total production costs, prolonged volatility can reduce investment capacity and hinder innovation in smaller manufacturing units.

Limited Recycling Infrastructure and End-of-Life Challenges

The complex construction of footwear soles, often involving adhesives, foams, and multiple polymers, makes recycling a difficult and costly process. The lack of specialized infrastructure for separating and processing these materials has resulted in less than 10% of footwear waste being recycled globally. This structural barrier limits the scalability of circular business models and deters large-scale adoption of recyclable materials. Until more efficient take-back systems and chemical recycling technologies are deployed, end-of-life management will remain a significant restraint for market growth.

Opportunity Analysis - Emergence of Bio-Based and Chemically Recyclable Polymers

The development of bio-based polymers and recyclable TPU alternatives represents a major commercial opportunity. Material innovators are creating foams derived from castor oil, sugarcane, and other renewable sources that maintain elasticity and durability comparable to synthetic materials. These solutions are gaining traction among high-performance footwear producers seeking low-carbon supply chains. By 2030, bio-based sole materials are expected to represent a multi-billion-dollar market opportunity as leading chemical producers commercialize scalable production.

Expansion of Nearshoring and On-Demand Manufacturing

The shift toward localized, on-demand production is redefining the footwear supply chain. Automated and modular sole manufacturing enables brands to respond rapidly to design trends while minimizing inventory waste. North American and European brands are increasingly establishing regional production facilities, reducing lead times and transportation emissions. The integration of digital fabrication tools such as 3D knitting and additive manufacturing in soles provides both customization and sustainability advantages. This transition could unlock a US$1–2 Billion market for specialized sole compounds within premium footwear categories by 2032.

Adoption of Circular Design and Repair Models

As brands embrace circular design principles, re-soling and modular footwear models are gaining traction. These approaches extend product lifespans and create recurring aftermarket demand for sole components. Emerging business models that emphasize replaceable sole units are expected to contribute to both sustainability goals and incremental revenue streams. Growth in this area will also stimulate demand for flexible adhesives, modular designs, and recyclable compounds, providing new avenues for compounders and component suppliers.

Category-wise Analysis

Product Type Insights

Athletic footwear remains the largest consumer of sole materials, accounting for approximately 40.3% of the market share in 2025. This dominance is driven by high material consumption per unit and continuous innovation in design and performance. Performance shoes require soles that offer cushioning, flexibility, traction, and stability, achieved through multi-layered constructions using PU, EVA, TPU, and rubber compounds. Models such as the Nike React Infinity Run and Under Armour HOVR incorporate advanced composites such as energy-return foams, TPU plates, and gel pods to enhance comfort and reduce injury risk. Collaborations between material innovators and athletic brands, such as Vibram with Salomon and Merrell, focus on improving durability and grip, particularly for trail and outdoor footwear. The sustained popularity of running, basketball, and athleisure sneakers reinforces athletic footwear’s leadership in sole material demand.

The casual and lifestyle segment is projected to grow fastest, driven by consumer demand for comfort, versatility, and sustainable fashion. Footwear such as Allbirds Tree Dashers, Skechers Everyday Comfort, and Nike SB sneakers combine EVA foam, TPU midsoles, and rubber outsoles for lightweight support and style. Digital-native brands enhance growth through online customization and eco-materials. With fewer technical constraints, this segment allows faster experimentation with sole innovations, positioning it as a key growth area over the next decade.

End-user Insights

OEMs (Original Equipment Manufacturers) dominate the footwear sole material market with a 51% share, supplying international brands and private-label products through centralized, high-volume procurement. Key manufacturing hubs in China, Vietnam, and Indonesia produce soles for brands such as Nike, Adidas, and Puma, selecting materials based on specific performance, durability, and sustainability standards. OEMs play a vital role in shaping market direction, often collaborating with material suppliers to co-develop proprietary polymers and injection-molding techniques. These partnerships help align product performance with brand expectations while optimizing costs and production timelines. Their influence spans both budget and premium segments, granting OEMs strategic control over material choices and quality standards.

The custom and aftermarket segment is rapidly expanding, driven by demand for personalized footwear solutions. Technologies such as 3D scanning, digital foot-mapping, and additive manufacturing are enabling custom-fit soles tailored to individual biomechanics and preferences. Innovators such as Feetz, Wiivv, and Form Athletics are leveraging 3D printing to deliver enhanced comfort, performance, and modularity. This segment promotes circular economy principles through replaceable components and material reuse, opening new revenue streams for material suppliers and 3D fabrication firms. As consumers increasingly prioritize fit, sustainability, and customization, this segment is expected to grow faster than traditional channels, offering strategic value to forward-looking industry players.

Regional Insights

Asia Pacific Footwear Sole Material Market Trends - Manufacturing Powerhouse with Rapid Adoption of Green Technologies

Asia Pacific holds the largest share of 44.8%, with major manufacturing hubs in China, Vietnam, India, and Indonesia. The region is also the fastest-growing and benefits from abundant raw materials, cost-effective labor, and large domestic markets, making it a dominant force in global footwear manufacturing. Rising disposable incomes, urbanization, and lifestyle changes are boosting demand for branded athletic, casual, and performance footwear. Both OEMs and local brands are expanding production to meet growing domestic and export requirements.

The region is experiencing rapid industrialization, and government initiatives promoting sustainable production and green manufacturing practices are enhancing competitiveness. For example, China’s footwear industry has adopted eco-friendly polymer production standards, while Vietnamese factories are implementing energy-efficient injection molding and recyclable sole materials. The expansion of local brand ecosystems, combined with export-oriented growth, is expected to drive the highest CAGR in the market between 2025 and 2032.

North America Footwear Sole Material Market Trends - Innovation Hub for Sustainable and High-Performance Sole Materials

North America represents one of the most mature markets for footwear sole materials. The United States dominates the region due to its strong base of global sportswear brands such as Nike, Under Armour, and New Balance, which drive demand for high-performance and lifestyle footwear. Premium pricing strategies, coupled with a growing focus on sustainability, have prompted brands to adopt bio-based and recyclable sole materials.

The region also benefits from advanced manufacturing technologies, including automated molding, 3D printing, and robotic assembly, which improve production efficiency and product consistency. Government policies promoting recycling, eco-friendly manufacturing, and waste reduction are encouraging collaborations between chemical suppliers and footwear producers.

Recent developments include Nike’s Move to Zero initiative, which emphasizes zero-carbon and zero-waste products, and Under Armour’s HOVR sustainable midsole program. Companies are increasingly investing in automated and nearshore manufacturing facilities to reduce logistics costs, shorten supply chains, and respond faster to market trends.

Europe Footwear Sole Material Market Trends - Regulation-Driven Sustainability and Premium Material Innovation

Europe’s footwear sole material market is characterized by stringent environmental regulations and a strong emphasis on sustainable production. Leading production centers include Germany, Italy, and Spain, while major consumption markets are the U.K. and France. European manufacturers are increasingly adopting recycled and bio-based polymers to meet regulatory requirements, including directives under the European Green Deal and national waste management policies. These regulations encourage companies to implement circular design principles and develop soles that can be recycled or repurposed at the end of life.

Local manufacturers are leveraging a combination of traditional craftsmanship and advanced material science to create premium footwear with high durability and comfort. Recent developments include Vibram’s eco-friendly rubber soles, which incorporate recycled rubber and sustainable production techniques, and Adidas’ Futurecraft Loop, a fully recyclable sneaker featuring modular sole systems. Continued innovation in recycled rubber, bio-based foams, and TPU materials positions Europe as a global benchmark for sustainability in the footwear materials industry.

Competitive Landscape

The global footwear sole material market is moderately concentrated, with major chemical firms such as BASF, Dow, and Covestro leading in polyurethane and elastomer supply. Specialized players such as Vibram and Trelleborg focus on high-performance, branded soles. Competition revolves around innovation, sustainability, and long-term contracts with global footwear brands.

Key trends include investment in bio-based materials, regionalized manufacturing, and circular design. Companies are leveraging proprietary technologies, lightweight formulations, and transparent supply chains to meet rising demand for sustainable, high-performance footwear solutions.

Key Industry Developments

- In July 2025, On Holding AG introduced LightSpray, a robotic manufacturing process for lightweight soles and uppers, enabling local production with reduced material waste. The innovation marked a breakthrough in sustainable manufacturing, positioning the brand as a pioneer in automation-led design.

- In February 2025, multiple industry consortia launched bio-based polymer development programs, focusing on castor oil and algae-based materials for footwear soles. These collaborations aim to achieve commercial-scale deployment by 2030, signaling an industry-wide transition toward renewable polymers.

- In April 2025, Under Armour partnered with regenerative footwear company UNLESS to launch a zero-plastic, plant-based shoe line, demonstrating the feasibility of regenerative sole materials. This collaboration underscores the growing alignment between innovation and environmental stewardship.

Companies Covered in Footwear Sole Material Market

- BASF SE

- Dow Inc.

- Covestro AG

- Huntsman Corporation

- Vibram S.p.A.

- Solvay S.A.

- Evonik Industries AG

- SABIC

- Arkema S.A.

- Wanhua Chemical Group Co., Ltd.

- Trinseo PLC

- Mitsui Chemicals, Inc.

- INOAC Corporation

- Asahi Kasei Corporation

- Tosoh Corporation

- Lubrizol Corporation

- Bridgestone Corporation

- Hexpol AB

- BASF Elastollan

- Lanxess AG

Frequently Asked Questions

The footwear sole material market size was US$27.5 Billion in 2025.

The footwear sole material market is projected to reach US$39.3 Billion by 2032.

Key trends include the rising adoption of sustainable and bio-based materials, growth in athleisure and casual footwear, technological innovations in lightweight and high-performance soles, and customized/3D-printed soles for personalization and circular economy initiatives.

By material type, polyurethane (PU) and rubber compounds remain the leading segment, accounting for nearly half of the total market value due to their flexibility, durability, and widespread use across athletic and casual footwear.

The market is expected to grow at a CAGR of 5.1% from 2025 to 2032.