- Food Ingredients & Additives

- Food Texturizing Agents Market

Food Texturizing Agents Market Size, Share, and Growth Forecast, 2025 - 2032

Food Texturizing Agents Market By Product Type (Emulsifiers, Thickeners) Source (Plant-based, Microbial-derived), Application, and Regional Analysis for 2025 - 2032

Food Texturizing Agents Market Size and Trends Analysis

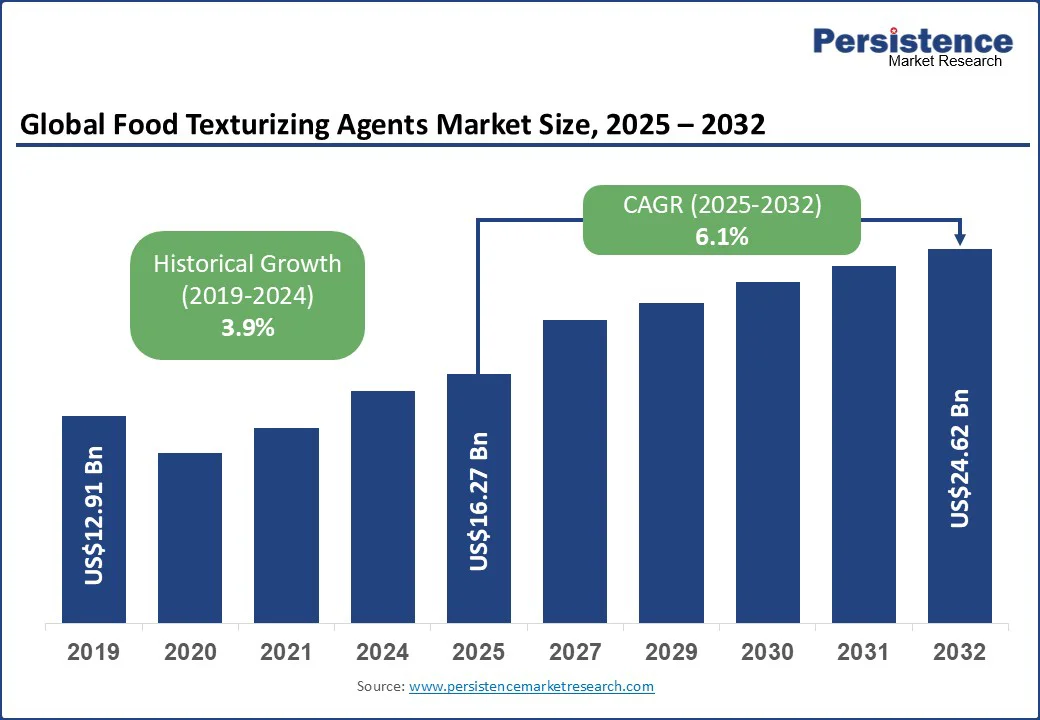

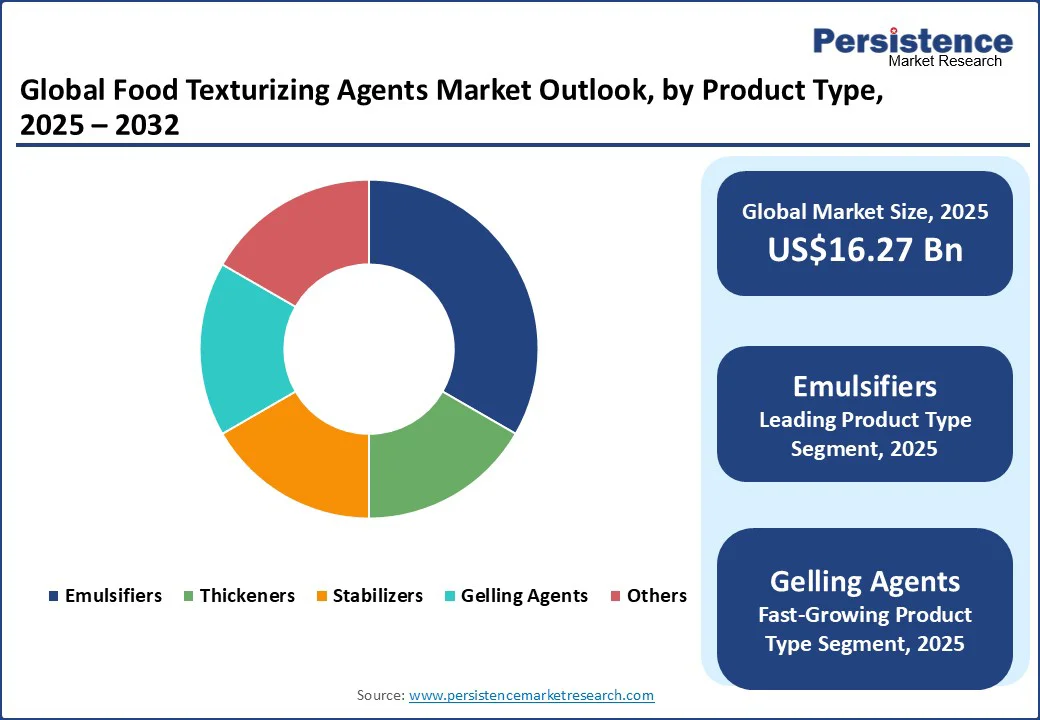

The global food texturizing agents market size is likely to be valued at US$16.27 Bn in 2025 and is expected to reach US$24.62 Bn by 2032, growing at a CAGR of 6.1% during the forecast period from 2025 to 2032.

Key Industry Highlights

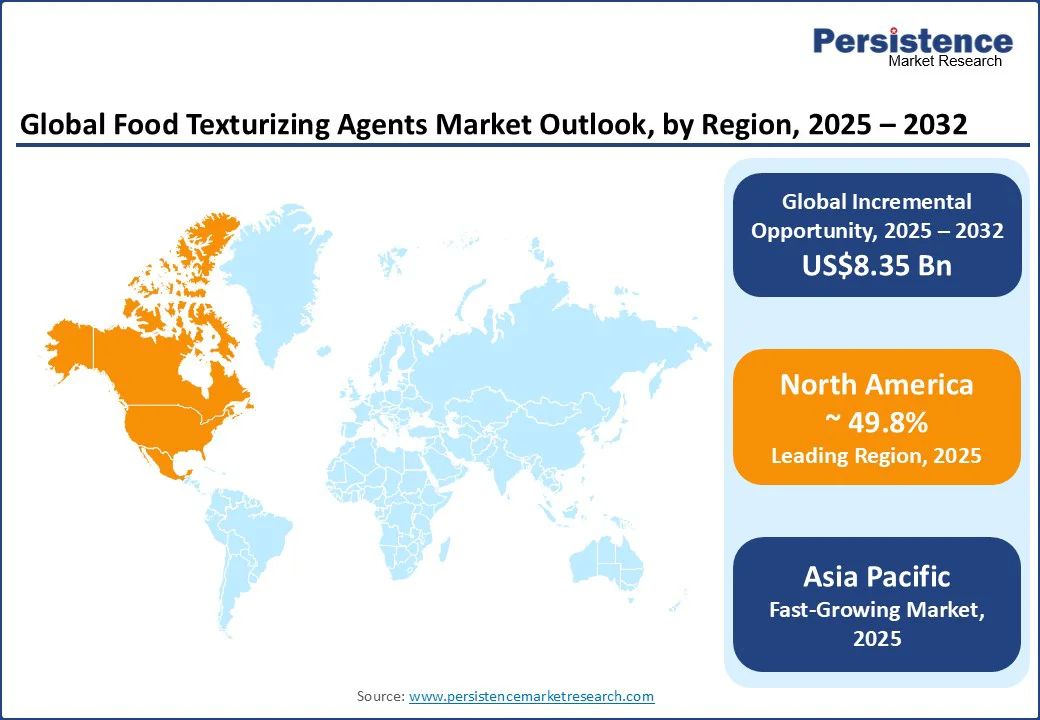

- Leading Region: North America dominates with a market share of 49.8%, supported by high demand for clean-label ingredients and strong adoption of plant-based texturizers in dairy, bakery, and beverage applications.

- Fastest-growing Region: Asia Pacific is the fastest-growing region, driven by the rapid expansion of the processed food sector in China and India, along with rising investments in plant-based and seaweed-derived texturizing solutions.

- Investment Plans: Major players such as Cargill, Tate & Lyle, and Ingredion are expanding production facilities and investing in sustainable, plant-based hydrocolloids to strengthen their presence in emerging markets.

- Dominant Product Type: Emulsifiers are expected to hold approximately 35.1% of the market share in 2025, owing to their wide usage in sauces, dairy, bakery, and convenience foods.

- Leading Source Segment: Plant-based texturizing agents are anticipated to lead the market with over 40.2% of the market share, supported by consumer demand for natural, non-GMO, and sustainable food ingredients.

| Global Market Attribute | Key Insights |

|---|---|

| Market Size (2025E) | US$16.27 Bn |

| Market Value Forecast (2032F) | US$24.62 Bn |

| Projected Growth (CAGR 2025 to 2032) | 6.1% |

| Historical Market Growth (CAGR 2019 to 2024) | 3.9% |

Growing demand for convenience foods, the rapid expansion of plant-based and clean-label products, and continuous innovation in natural and multifunctional texturizers are shaping the market’s growth global growth trajectory.

Market Dynamics

Driver- Clean-Label and Multi-Functional Ingredients Fuel the Shift Toward Natural Texturizing Solutions

Food texturizing agents play a crucial role in enhancing the sensory attributes, stability, and shelf life of a wide range of food and beverage products. These agents, which include emulsifiers, stabilizers, thickeners, and gelling agents, are increasingly used across bakery, dairy, confectionery, and ready-to-eat segments to meet the rising consumer expectations for quality and consistency. Hence, the rising adoption of plant-extracted hydrocolloids as replacements for modified starches pumps market growth.

Ingredients such as citrus fiber and acacia gum are increasingly preferred in sauces, dressings, and plant-based meat products because they offer clean-label transparency and strong functional performance. Microbial-fermentation-derived exopolysaccharides are emerging as novel clean-label alternatives to synthetic stabilizers, such as carboxymethyl cellulose. These innovations not only meet regulatory and labeling requirements but also allow manufacturers to maintain desired texture, stability, and mouthfeel without relying on artificial additives.

Formulation Challenges Arise from Instability and Inconsistency in Natural Texturizers

One key restraint in the food texturizing agents market is the limited heat and acid stability of plant-based hydrocolloid blends. Certain starch-derived texturizers tend to lose viscosity or break down under high-temperature processing or in acidic environments, which restricts their use in products such as sterilized sauces, dressings, and acidic beverages. This instability often forces manufacturers to use multi-component systems to achieve the desired texture, which can complicate formulation efforts, particularly in clean-label products where simplicity is highly valued.

Another challenge is the seasonal variability of raw materials impacting the consistency of natural gums, including algae-based agents such as agar-agar and seaweed-derived carrageenan. Variations in harvest yield and quality can lead to inconsistent gelling strength and batch-to-batch differences, making it difficult for manufacturers to maintain uniform texture in end products. This unpredictability poses significant challenges for small and medium-sized producers, affecting consumer perception of product quality, particularly in premium and plant-based segments.

Opportunity - Advanced Texturizing Technologies Open New Frontiers in Plant-Based and Sustainable Foods

The rapid expansion of the plant-based and vegan food sector is creating significant opportunities for specialty hydrocolloid blends designed to optimize plant protein mouthfeel. These advanced blends help bridge the texture gap in products such as plant-based meats, dairy-free yogurts, and vegan cheeses by replicating creaminess, cohesiveness, or fibrous bite, attributes typically provided by animal proteins. As consumer demand for realistic and satisfying alternatives grows, the development of such targeted texturizing solutions is becoming a crucial innovation area for manufacturers.

Another promising opportunity lies in the application of texturizing agents for edible films and biodegradable packaging. Plant-derived hydrocolloids can serve as both food stabilizers and sustainable film-forming materials, allowing brands to combine product protection with eco-friendly packaging innovation.

The use of microencapsulation-enabled texture layering, where hydrocolloids encapsulate flavors, probiotics, or nutrients, offers new ways to deliver enhanced sensory experiences and extend shelf life. This creates new growth prospects in functional snacks, convenience foods, and fortified beverages where consumer demand for both health and indulgence is on the rise.

Category-wise Analysis

Product Type Insights

Within product types, emulsifiers dominate, accounting for 35.1% of the total share. Their prevalence stems from the unique ability to blend immiscible ingredients such as oil and water, while also improving the stability, texture, and longevity of food products. Emulsifiers are indispensable across a wide array of food categories, including bakery, dairy, sauces, and beverages.

For example, mono- and diglycerides are essential in baked goods and ice creams, where they strengthen dough, enhance mouthfeel, and maintain fat stability. In sauces and dressings, emulsifiers prevent separation and maintain a uniform texture. The push for low-fat and reduced-calorie products has also spurred innovation in emulsifier formulations, especially clean-label alternatives such as sunflower lecithin and enzyme-based ingredients.

Gelling agents are the fastest-growing segment. The rising popularity of plant-based and vegan diets has significantly increased the demand for natural, plant-derived gelling substances. Agents such as agar-agar, pectin, and gelatin are widely used to create desirable textures in confectionery, dairy alternatives, and plant-based foods.

These ingredients impart firmness and elasticity, which consumers associate with indulgent and premium-quality products. In particular, agar-agar has gained popularity in vegan confectionery and dairy-free desserts due to its excellent gelling properties and plant-based origin. As more consumers prioritize clean-label and allergen-free products, there is a marked shift away from animal-derived gelatin in favor of plant-based alternatives.

Source Insights

Among sources, plant-based texturizing agents represent both the largest and the fastest-growing category. They hold approximately a 40.2% share of the global market, supported by strong demand for natural, clean-label, and vegan-friendly ingredients. This segment is expanding at a CAGR of nearly 9.5%.

Plant-derived starches, gums, and pectin are versatile and can be used across bakery, dairy alternatives, beverages, and sauces, making them the most commercially viable option. A common example is citrus pectin, which is widely applied in jams, plant-based yogurts, and sauces because it delivers gelling and thickening properties while fitting clean-label requirements.

The preference for plant-based agents also stems from their alignment with sustainability and health trends, as well as their ability to substitute synthetic or animal-based texturizers without compromising product performance. Ingredients such as guar gum, sourced from guar beans, have seen rising adoption in dairy alternatives and vegan desserts to provide viscosity and stability. This has positioned the plant-based category as the most dynamic growth driver in the overall food texturizing agents market.

Regional Insights

North America Food Texturizing Agents Market Trends - Innovation in Clean-Label and Functional Texturizing Agents

North America continues to dominate the food texturizing agents market, accounting for over 49.8% of the market share. The region’s leadership stems from a mature and innovation-driven food manufacturing ecosystem, paired with increasing consumer demand for processed foods that meet clean-label and functional expectations. Companies in North America are increasingly investing in R&D to develop next-generation texturizing agents that balance performance with transparency and sustainability.

U.S. food manufacturers are at the forefront of transitioning to clean-label formulations, focusing on natural, minimally processed ingredients without compromising on functionality. A prime example of this trend occurred in 2024, when Ingredion launched NOVATION Indulge 2940, a groundbreaking non-GMO native corn starch designed specifically for gelling and co-texturizing applications in dairy, plant-based dairy, and dessert products.

This innovation highlights the industry's strategic shift toward texturizers that offer both high performance and label-friendly appeal, supporting a broader clean-label movement gaining traction across the U.S.

In Canada, the food texturizing landscape is closely tied to the growth of plant-based products. According to the NECTAR “Taste of the Industry 2024” report, which analyzed over 54 plant-based meat products, key texture parameters such as bite, chew, and juiciness are increasingly optimized through innovative texturizing agents.

Canadian food innovators are leveraging ingredients such as pea protein, lentils, and even seaweed-derived compounds to meet evolving consumer expectations for texture in alternative proteins. These efforts are often supported by government-backed initiatives aimed at advancing sustainable and functional food technologies.

Asia Pacific Food Texturizing Agents Market Trends - Rapid Growth Fueled by Innovation and Urbanization

The Asia Pacific region represents the fastest-growing market for food texturizing agents, with a high CAGR through 2032. Urbanization, increasing disposable incomes, and rising demand for processed and convenience foods are fueling this surge. China is taking a leading role in pioneering next-gen food textures.

One notable innovation is Xinqitian’s 3D peel-off gummies, which deliver a layered, interactive snacking experience. This format taps into consumer desires for novelty and fun, particularly among younger demographics. Many Chinese manufacturers are exploring texturizing solutions to combat food waste by reformulating products for longer shelf life, texture retention, and ingredient flexibility.

Companies such as Yihai Kerry and Angel Yeast are also making strides in food ingredient development. For instance, Angel Yeast is working on yeast-derived texture enhancers that are functional in plant-based meat analogs, soups, and ready-to-eat meals, meeting the dual demand for clean-label and performance.

India is emerging as a crucial growth market for food texturizers. The country’s processed food sector is growing at over 10% annually, and its vast culinary diversity is driving innovation in multi-texture applications, from crispy snacks to chewy sweets and smooth dairy analogs.

Local startups such as GoodDot and Blue Tribe Foods are working to perfect textural authenticity in plant-based meats, using texturizing agents such as pea protein isolates, gum blends, and enzymatically modified starches to replicate traditional Indian textures such as kebabs or creamy paneer.

Government initiatives under the Pradhan Mantri Kisan SAMPADA Yojana are also funding R&D in plant-based processing, especially involving millets, legumes, and pulses, which require specific texturizing agents to appeal to mass markets.

Europe Food Texturizing Agents Market Trends - Regulatory Frameworks and Natural Preferences Drive Steady Growth

Europe maintains a steady, sustainable growth pattern in the food texturizing agents market, supported by strict regulatory frameworks, high-quality standards, and a strong consumer preference for natural and clean-label ingredients. The U.K. stands out for its technical innovation, especially in the alternative protein space.

Companies such as THIS, Meatless Farm, and Quorn are leveraging advanced technologies such as extrusion, fermentation-derived fibers, and algae-based texturizers to improve bite, juiciness, and structural integrity in meat analogs.

U.K.-based ingredient companies such as Kerry Group (U.K. arm) and Tate & Lyle are also pioneering in clean-label starches, plant gums, and dietary fibers that provide stability and mouthfeel in sugar-reduced and fat-reduced formulations. The U.K. Food Standards Agency’s increasing focus on ingredient traceability and consumer labeling is further incentivizing producers to favor transparent, minimally processed texturizers.

Germany, known for its engineering-led food science, remains a key influencer in texture innovation. Leading ingredient suppliers such as Jungbunzlauer and Hydrosol are producing plant-based hydrocolloids, pectins, and enzymatically modified starches designed to cater to vegan, gluten-free, and organic-certified markets.

German firms are also aligning with EU sustainability mandates, using upcycled ingredients from sources such as apple pomace or chicory root fibers as texture agents in bakery and dairy-alternative categories.

Competitive Landscape

The global food texturizing agents market is moderately consolidated, with a mix of global leaders and regional specialists competing through product innovation and strategic partnerships. Major players such as Ingredion Incorporated, Cargill, Kerry Group, Tate & Lyle, and CP Kelco are heavily investing in clean-label, plant-based, and multifunctional solutions to align with evolving consumer preferences.

Smaller regional players are also gaining traction by focusing on niche applications such as seaweed-derived gelling agents or microbial-based stabilizers. Companies in the Asia Pacific are driving innovations in cost-effective texturizers tailored to local food products, while European manufacturers are strengthening their portfolios with sustainable and non-GMO offerings. This blend of global innovation and regional specialization is shaping a highly dynamic and competitive market environment.

Key Industry Developments

- In February 2024, Ingredion launched NOVATION Indulge 2940, a non-GMO corn starch designed to deliver improved gelling and indulgent textures in dairy and dessert applications.

- In January 2024, CP Kelco expanded its range of pectin-based stabilizers in response to growing demand for clean-label texturizers in beverages and fruit preparations.

Companies Covered in Food Texturizing Agents Market

- Ingredion Incorporated

- Cargill, Incorporated

- Kerry Group plc

- Tate & Lyle PLC

- CP Kelco U.S., Inc.

- Archer Daniels Midland Company (ADM)

- DuPont de Nemours, Inc.

- Ashland Global Holdings Inc.

- Royal DSM N.V.

- Givaudan S.A.

- Darling Ingredients Inc.

- Fuerst Day Lawson Ltd.

- Avebe U.A.

- Ajinomoto Co., Inc.

- Jungbunzlauer Suisse AG

- Palsgaard A/S

- Riken Vitamin Co., Ltd.

- Fiberstar, Inc.

- BASF SE

- Lonza Group AG

Frequently Asked Questions

The food texturizing agents market size is estimated to reach US$16.27 Bn in 2025.

By 2032, the market is projected to attain a value of US$24.62 Bn.

Key trends include the rising demand for plant-based texturizers, growing adoption of clean-label and non-GMO formulations, innovations in microbial-derived stabilizers, and the use of texturizing agents in plant-based meat and dairy-alternative products.

By product type, emulsifiers dominate the market with a significant share due to their wide usage in dairy, bakery, and convenience foods. By source, plant-based texturizers hold the largest share, supported by consumer preference for natural and sustainable ingredients.

The market is anticipated to grow at a CAGR of 6.1% between 2025 and 2032, driven by the increasing use of natural and multifunctional texturizers in processed and functional foods.

Key players include Ingredion Incorporated, Cargill Incorporated, Tate & Lyle PLC, Kerry Group plc, and CP Kelco U.S., Inc.