- Processed Food

- Food Spread Market

Food Spread Market Size, Share and Growth Forecast, 2026 - 2033

Food Spread Market by Product Type (Honey, Nut & Seed-based Spreads, Fruit-based Spreads, Chocolate-based Spreads, Others), Nature (Conventional, Organic), Packaging Type (Jars, Tubs, Others), and Regional Analysis for 2026 - 2033

Food Spread Market Share and Trends Analysis

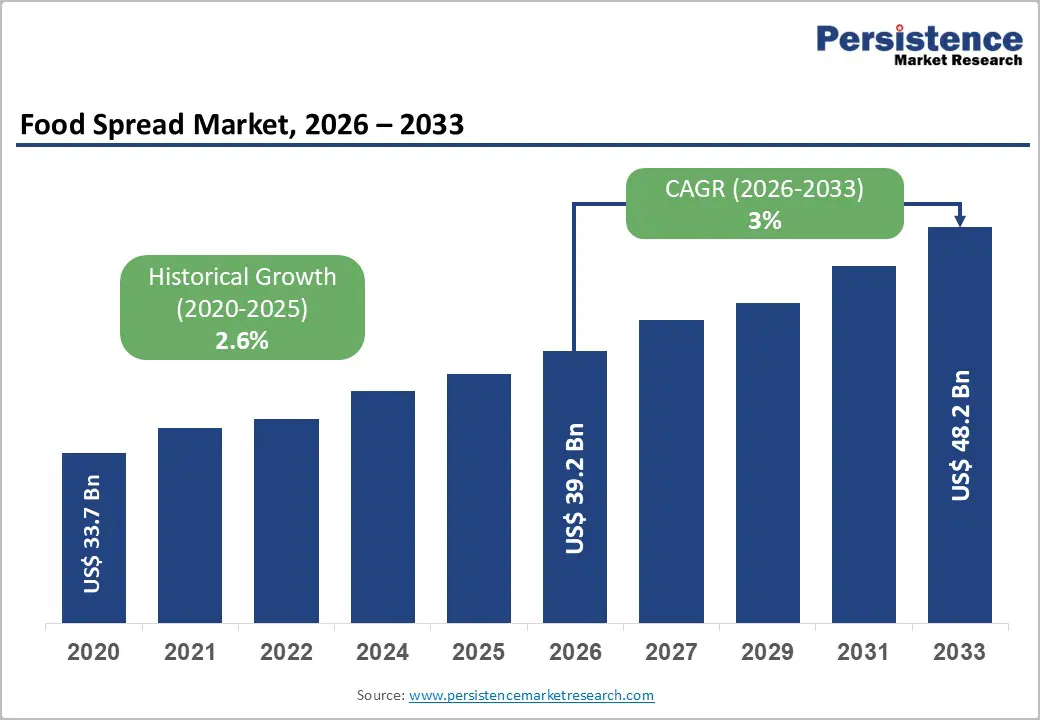

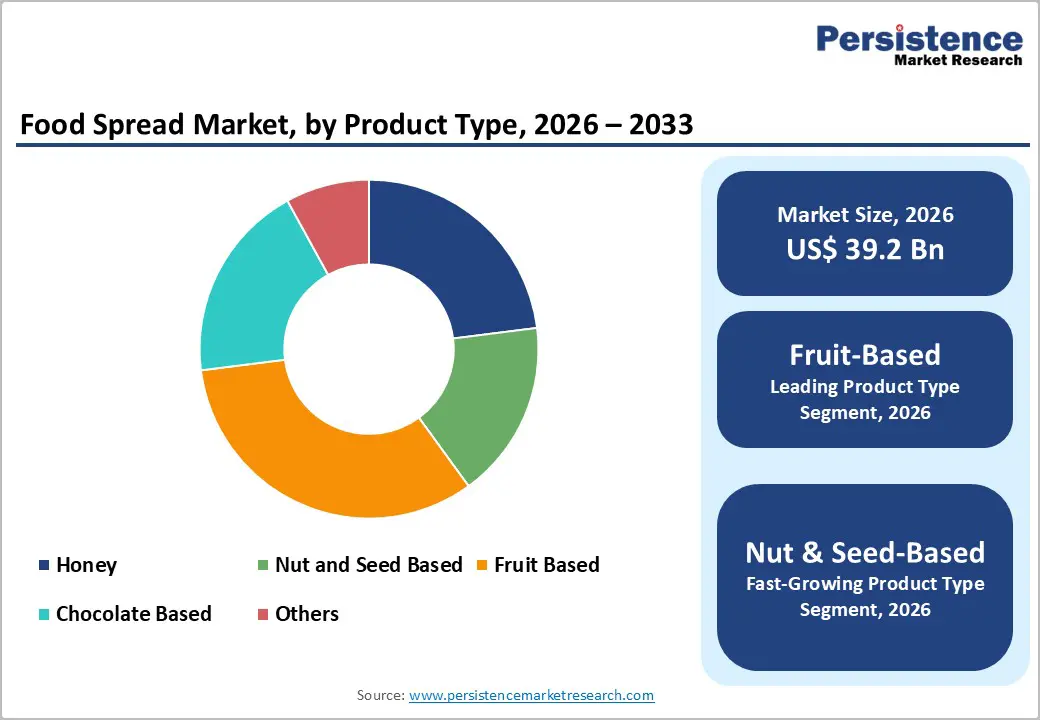

The global food spread market size is likely to be valued at US$ 39.2 billion in 2026, and is projected to reach US$ 48.2 billion by 2033, growing at a CAGR of 3% during the forecast period of 2026–2033. This market is benefiting from rising consumption of ready-to-eat meals and breakfast items, while urban households have been adopting more convenience-oriented eating patterns that favor packaged spreads. Brand owners have been steadily introducing clean-label, organic, and reduced-additive recipes, so product ranges have been aligning more closely with health and transparency expectations.

Underlying demand has remained structurally resilient because spreads have been integrated into daily routines, maintained long ambient or chilled shelf lives, and remained accessible across income brackets. Producers and retailers have been supporting moderate but dependable expansion through gradual premiumization, including higher fruit content jams, nut and seed blends, and protein-enriched options that justify higher price points. At the same time, organized retail chains and e-commerce marketplaces have been widening distribution, allowing consumers to discover more specialized and international offerings without sacrificing convenience.

Key Industry Highlights

- Product Type Leadership: Fruit-based spreads are expected to dominate with 33% market share, supported by high household penetration and consistent demand.

- Nature-based Segmentation: Conventional spreads are expected to retain leadership, with over 75% revenue share, driven by affordability and wide availability, while organic spreads are expected to grow at about 5.5% CAGR, driven by clean-label adoption and regulatory trust.

- Packaging Type Trends: Jars are projected to dominate with around 52% share, benefiting from consumer familiarity, whereas tubs are likely to grow the fastest through 2033, driven by convenience, lightweight design, and sustainability initiatives.

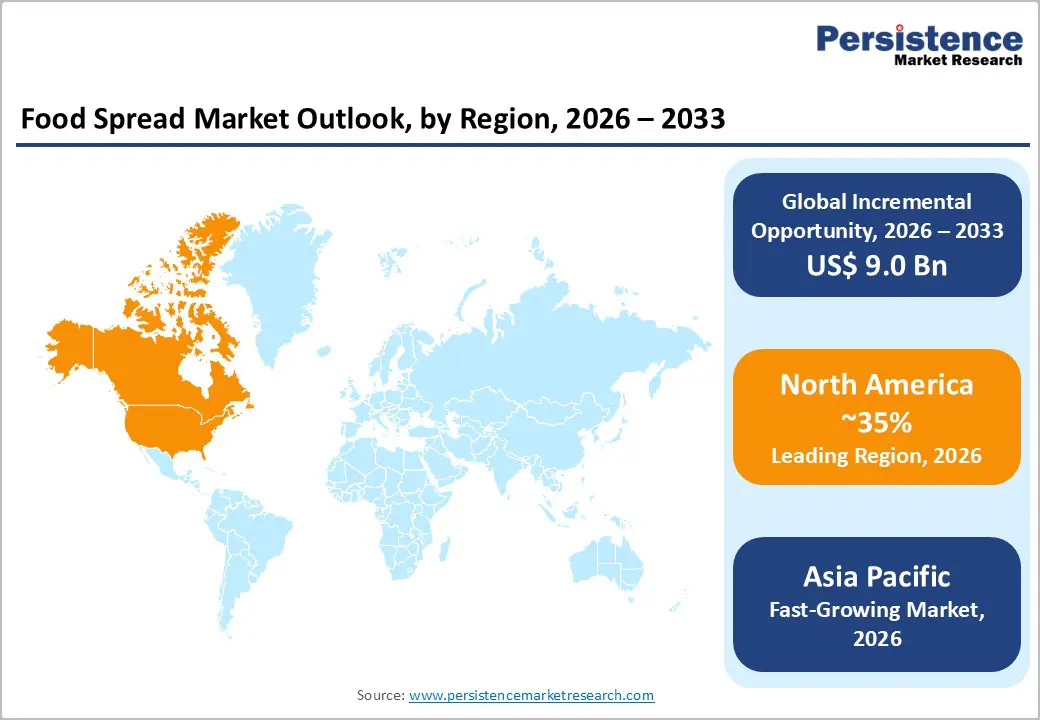

- Regional Dynamics: North America is expected to lead with approximately 35% share, fueled by high per-capita consumption and product innovation.

- Fastest-growing Market: Asia Pacific is projected to be the fastest-growing regional market, registering a 2026-2033 CAGR of around 4.1%, driven by a rapidly expanding organized retail ecosystem.

- Premiumization and Innovation: Organic and clean-label food spreads are emerging as a key driver of value growth, as consumers increasingly prioritize ingredient transparency, health benefits, and sustainable sourcing.

- April 2025: Kraft Heinz introduced TasteMaker, the industry’s first AI-driven platform for product innovation, aiming to cut development cycles, optimize formulations, and ensure faster compliance with North American and European nutrition standards.

| Key Insights | Details |

|---|---|

|

Food Spread Market Size (2026E) |

US$ 39.2 Bn |

|

Market Value Forecast (2033F) |

US$ 48.2 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

3.0% |

|

Historical Market Growth (CAGR 2020 to 2025) |

2.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth in Convenient, Clean-Label Food Consumption Supported by Retail Expansion

The food spread market is increasingly driven by growing demand for convenient breakfast and snack options and a strong consumer preference for clean-label, naturally formulated products. Urban households, particularly dual-income families, favor foods that require minimal preparation, positioning spreads as staples in daily meals. Rising health awareness and concern about ingredient transparency have boosted demand for fruit-, honey-, and nut-based spreads. These products offer both convenience and perceived nutritional value, reinforcing repeat purchases. The shift toward ready-to-eat and functional foods has also encouraged manufacturers to innovate with low-sugar and fortified formulations. Overall, this trend has strengthened consumption consistency, stabilized revenue streams, and enhanced brand loyalty across both developed and emerging markets.

This trend has been reinforced by retail expansion and regulatory alignment across key markets. In North America, manufacturers accelerated clean-label product launches in response to updated federal nutrition labeling and sugar disclosure requirements, prompting widespread reformulation of fruit- and nut-based spreads across mainstream retail chains. Similarly, in India, state-level food processing incentives supported the rapid growth of organized food retail, improving shelf access for branded spreads beyond major metropolitan areas. Investments in e-commerce grocery platforms and cold-chain logistics further enhanced product availability and reach. These initiatives strengthened consumer trust in product quality, enabled broader distribution of both conventional and premium spreads, and facilitated compliance with evolving food safety standards.

Raw Material Volatility and Nutritional Compliance Challenges

Market players faced significant cost pressures from raw material volatility and supply chain disruptions in 2025. Cocoa, a key ingredient for chocolate-based spreads, entered the year at historic highs, peaking in March 2025 at over US$ 12,000 per metric ton, a roughly 150% increase from 2024 levels, driven by crop diseases like Cocoa Swollen Shoot Virus and erratic weather in Côte d’Ivoire and Ghana, which account for 70% of global production. However, by December 2025, prices plunged over 50% to US$ 5,000–US$ 6,000 per ton due to optimistic harvest forecasts and a projected small surplus of 49,000–250,000 metric tons. Simultaneously, fruit pulp markets experienced oversupply, leading to a 15–20% price crash. At the same time, nut production faced logistical and climatic disruptions, including frost in Turkey affecting hazelnuts and geopolitical tensions disrupting pistachio exports.

Supply chain and logistical constraints further compounded cost pressures. Port congestion, new tariffs, and retaliatory trade measures, particularly between North America and Canada, increased operational complexity and transportation costs for spread manufacturers. Concurrently, regulatory scrutiny on sugar and saturated fat content forced companies to reformulate chocolate- and fruit-based spreads to comply with updated federal nutrition labeling in North America and enhanced sugar labeling in India. While some leading companies in the fast-moving consumer goods (FMCG) sector have invested in reduced-sugar and fortified products, these efforts have, in turn, increased production and R&D costs. Such raw material fluctuations, logistical hurdles, and nutritional compliance created structural barriers that limited profit stability and constrained aggressive market expansion.

Progress in Organic, Functional, and Innovative Food Spreads

Global consumer trends are shifting toward organic, clean-label, and health-focused food spreads, creating significant opportunities for manufacturers. Companies like Marico and Dabur in India expanded certified organic spreads under India Organic standards. At the same time, North American FMCG brands introduced fruit- and nut-based organic spreads aligned with the U.S. Department of Agriculture (USDA) Organic labeling. Beyond organic positioning, manufacturers invested in new product formulations, including low-sugar fruit spreads and allergen-free nut spreads, catering to health-conscious consumers and expanding reach in both urban and semi-urban markets. These initiatives enhanced brand credibility, enabled premium pricing, and strengthened long-term revenue potential in the organic segment.

Innovation and functional product development further drive opportunities across regions. Several companies launched fortified spreads enriched with protein, fiber, probiotics, or micronutrients to address unmet nutritional needs among millennials and aging populations in North America, Europe, and Asia. In addition, new flavor profiles, plant-based chocolate spreads, and hybrid fruit-nut combinations are being regularly introduced, reflecting product discovery and R&D investment. Governments in emerging markets, including India and Nigeria, supported local packaged food production through incentives, improving distribution reach. Combined, these advances in product innovation, fortification, and regional market expansion create a high-potential growth segment for strategic investment and long-term market development.

Category-wise Analysis

Product Type Insights

Fruit-based spreads are expected to account for around 33% of the food spread market's revenue share in 2026, driven by high household consumption and a strong presence in foodservice channels. Their affordability, long shelf life, and versatility across age groups make them a staple in daily diets. Jam and preserves are especially popular in North America and Europe, consumed with bread, cereals, and bakery products. In 2025, for instance, Smucker’s maintained leadership through consistent innovation and broad retail distribution. This segment also benefits from high repeat consumption and stable demand patterns. Its wide appeal across both urban and semi-urban populations reinforces its market dominance.

Nut & seed-based spreads are projected to grow at the highest CAGR in the product-type category through 2033, fueled by rising protein consumption, plant-based diets, and clean-label trends. Peanut, almond, and mixed-seed spreads are increasingly popular among health-conscious urban consumers. Brands such as Justin’s and MaraNatha expanded e-commerce and retail presence for almond and mixed-nut spreads. Premium pricing and innovative flavors further accelerate adoption. The segment’s growth is reinforced by consumer interest in nutrient-rich, convenient snack options.

Nature Insights

Conventional spreads are anticipated to dominate the market with over 75% share in 2026, primarily due to affordability, mass-market availability, and extensive retail penetration. Large FMCG companies leverage economies of scale, strong production capabilities, and established distribution networks to maintain leadership across both developed and emerging markets. Nestlé and Hershey expanded their conventional spread portfolios in supermarkets and convenience stores, ensuring accessibility for a broad consumer base. High-volume production and long-standing logistics systems allow these brands to maintain consistent supply and competitive pricing. Additionally, brand recognition and consumer trust reinforce repeat purchases, supporting market stability. The segment continues to benefit from steady demand in urban and semi-urban areas.

Organic spreads are poised to grow rapidly, with a CAGR of roughly 5.5% from 2026 to 2033, driven by rising consumer preference for chemical-free, clean-label products and increasing disposable incomes. Regulatory certifications such as USDA Organic, EU Organic, and India Organic provide credibility, enabling premium positioning and export potential. Premium pricing supports higher margins, while innovative flavors and formulations enhance product differentiation. Growing awareness of health and wellness trends, coupled with trust in regulatory compliance, is accelerating adoption globally. This combination of consumer demand, regulatory support, and brand innovation makes organic spreads one of the fastest-growing market segments.

Packaging Type Insights

Jars are set to continue to dominate the food spread market share, accounting for over 52% of the total volume, due to their durability, ease of storage, and high product visibility on retail shelves. Glass jars, in particular, are preferred for premium and organic spreads, as they enhance perceived quality and support brand positioning. Companies such as Smucker’s and Bonne Maman emphasized glass jar packaging for fruit and nut spreads in 2025, reinforcing both premium appeal and shelf differentiation. Jars also simplify handling for consumers and retailers, while maintaining product freshness and extending shelf life. Their long-standing acceptance across households and foodservice channels ensures steady demand. Considering these factors, jars are likely to remain the benchmark packaging format, balancing functionality, aesthetics, and market familiarity.

Tubs and other flexible packaging formats are slated to be the fastest-growing segment between 2026 and 2033, supported by tier cost-effective production, lighter weight, and suitability for bulk or institutional use. Their adoption is expected to accelerate further, driven by innovations in sustainable and recyclable packaging that appeal to environmentally conscious consumers. Brands such as Skippy and Nutella have introduced spreads in tubs and pouches for retail and foodservice channels, improving convenience and streamlining logistics. These formats also provide portability and easy portioning, catering to modern lifestyles and high-volume consumption. The synergy of operational efficiency, eco-friendly design, and evolving consumer preferences reinforces the growth potential of tubs and flexible packaging globally.

Regional Insights

North America Food Spread Market Trends

North America is positioned to command approximately 35% of the food spread market share in 2026, with the United States serving as the dominant revenue engine. This sustained leadership stems from established dietary habits, where high per-capita intake of bread, breakfast items, and packaged snacks has created a reliable baseline for volume demand. Regulatory clarity has further bolstered consumer trust, as the U.S. Food and Drug Administration (FDA) has enforced rigorous oversight on nutrition labeling and sugar disclosure, prompting shoppers to favor transparent brands. Manufacturers have responded by accelerating the development of reduced-sugar, protein-enriched, and organic formulations that align with modern wellness priorities. Strategic investments have strengthened domestic supply chains and improved speed-to-market for these evolving product lines.

Innovation across retail channels has been revitalizing this mature sector, with e-commerce grocery platforms and wholesale club stores broadening access to premium and functional spread varieties. Brands have been enhancing shelf appeal and environmental credentials by adopting sustainable packaging solutions, including recyclable glass jars and lightweight tubs. The region’s advanced cold-chain and logistics infrastructure has ensured efficient nationwide distribution, reinforcing the availability of both mainstream and niche products. High brand loyalty and deep consumer awareness have continued to drive repeat purchases, anchoring global revenues in North America while setting standards for formulation quality and packaging design that other markets often follow.

Europe Food Spread Market Trends

Europe is a significant market for food spreads, led by Germany, the U.K., France, and Spain in production and consumption. Harmonized regulatory standards under the European Food Safety Authority (EFSA) have facilitated cross-border trade, streamlined compliance, and enabled faster product launches across regional markets. Consumer preferences increasingly favor artisanal, organic, low-sugar, and origin-labeled spreads, directly shaping product portfolios and innovation strategies. Private-label products occupy substantial shelf space in supermarkets, intensifying price competition within conventional categories. In 2025, Ferrero’s acquisition of a Germany-based organic nut spread producer strengthened its clean-label capabilities and broadened access to premium European retail channels. Sustainability credentials have become a central pillar of brand positioning across the region.

Growth momentum is reinforced by rising health awareness and demand for transparent ingredient sourcing across European consumers. Manufacturers are increasingly investing in recyclable, lightweight, and reusable packaging formats to meet sustainability targets and retailer mandates. Origin labeling and traceability claims are being strengthened to build consumer trust and comply with regional food transparency norms. Premium and specialty spreads continue to benefit from strong penetration in organic stores, gourmet retailers, and specialty bakeries. E-commerce platforms are supporting wider visibility for niche, regional, and artisanal brands. Regulatory consistency enables efficient multi-country rollouts. Europe remains a mature yet innovation-focused market driven by quality differentiation and sustainability leadership.

Asia Pacific Food Spread Market Trends

Asia Pacific is projected to be the fastest-growing regional market for food spreads, with a 2026-2033 CAGR of 4.1%, driven by strong momentum across the economies of China, India, Japan, and ASEAN. Rapid urbanization and rising disposable incomes are reshaping breakfast, snacking, and at-home consumption patterns. The expansion of modern retail chains and digital grocery platforms has significantly improved access to branded food spreads. Local manufacturing and regional sourcing provide cost efficiencies and operational flexibility for producers. Britannia Industries commissioned a new spreads manufacturing facility in India, focused on premium, fortified, and export-oriented products. Strengthening food safety frameworks across the region continues to formalize the market.

Regional market growth is further supported by the rising demand for functional, fortified, and plant-based spreads, particularly among urban and younger consumers. Affordable pack sizes and localized flavor profiles are expanding adoption beyond metropolitan areas. Government incentives for food processing and agri-value addition are encouraging capacity expansion and private investment. E-commerce and quick-commerce platforms enable deeper penetration into tier-2 and tier-3 cities. Export competitiveness is improving as regulatory standards align with international norms. Asia Pacific remains the primary long-term growth engine for the global food spread market.

Competitive Landscape

The global food spread market is moderately consolidated, dominated by influential participants such as Nestlé, Ferrero, The J.M. Smucker Company, Kraft Heinz, and Unilever. These organizations have leveraged extensive brand equity and expansive retail networks to maintain a leading presence across international shelves. Market leaders have prioritized clean-label reformulations, eco-friendly packaging initiatives, and strategic portfolio diversification to defend their market share amid shifting consumer tastes. Operations have achieved significant scale efficiencies and established enduring alliances with retailers that promote pricing stability and shelf-space priority. Innovation in the premium and low-sugar segments has remained a critical instrument for entities seeking to outpace competitors and capture health-conscious demographics.

Regional manufacturers and private-label alternatives have been intensifying competitive pressures through localized flavor profiles and aggressive cost positioning, particularly within Europe and Asia Pacific. Formidable entry obstacles such as rigorous food safety certifications, consistent feedstock sourcing, and the necessity for deep consumer trust have shielded established brands from erratic shifts. However, the rise of e-commerce grocery platforms has empowered artisanal and niche brands to achieve visibility without the need for traditional retail footprints. Larger corporations will have pursued strategic acquisitions of organic and specialty producers to integrate high-growth assets into their broader structures. Collaborative ventures in sustainable ingredient sourcing and packaging design have continued to reshape industry dynamics as stakeholders seek to balance profitability with environmental responsibility.

Key Industry Developments

- In July 2025, Schuman Cheese launched Delve, a new line of cheese-based dips and spreads featuring Basil Pesto Parm, Garlic Herb Asiago, and Whipped Feta, all using Cello Mascarpone for smooth texture. Award-winning at 2024 World Dairy Expo, 16-oz tubs are available at Costco in select U.S. regions.

- In June 2025, Tyson Foods brought out Hillshire Snacking Dips and Spreads, featuring single-serve packs that pair pepperoni with cream cheese-based spreads and toasted rounds in three flavors. Each 6g-protein pack targets convenient on-the-go snacking, expanding the brand's high-quality offerings amid rising consumer demand.

- In May 2025, Ferrero announced the launch of the Nutella Peanut spread in spring 2026, blending its iconic cocoa-hazelnut formula with roasted peanuts to target U.S. consumers amid soaring peanut demand. The five-year development is backed by a US$75 million investment in an Illinois facility.

Companies Covered in Food Spread Market

- Unilever plc

- Kraft Heinz Company

- Ferrero Group

- Hormel Foods Corporation

- Andros Group

- Bonne Maman

- Hershey Company

- Conagra Brands

- The J.M. Smucker Company

- Wilmar International

- Marico Ltd.

- Dabur India Ltd.

- St. Dalfour

Frequently Asked Questions

The global food spread market is projected to reach US$ 39.2 billion in 2026.

Rising consumption of convenient breakfast and snack foods, increasing demand for clean-label and natural products, and expanding organized retail and e-commerce channels across developed and emerging markets are key growth drivers.

The market is poised to witness a CAGR of 3% from 2026 to 2033.

Expansion of organic and functional spreads, premiumization through clean-label innovation, and growing penetration in emerging markets supported by modern retail and food processing investments present major opportunities.

Nestlé S.A., Ferrero Group, The J.M. Smucker Company, Kraft Heinz Company, and Unilever PLC are among the leading players operating in the market.