- Food Ingredients & Additives

- Food Grade Nylon Market

Food Grade Nylon Market Size, Share, and Growth Forecast, 2026 - 2033

Food Grade Nylon Market by Nylon Type (Nylon 6, Nylon 66, Nylon 12), Distribution Channel (Direct Sales, Distributors, Online Platforms), Application (Food Processing Equipment, Others), and Regional Analysis 2026 - 2033

Food Grade Nylon Market Size and Trends Analysis

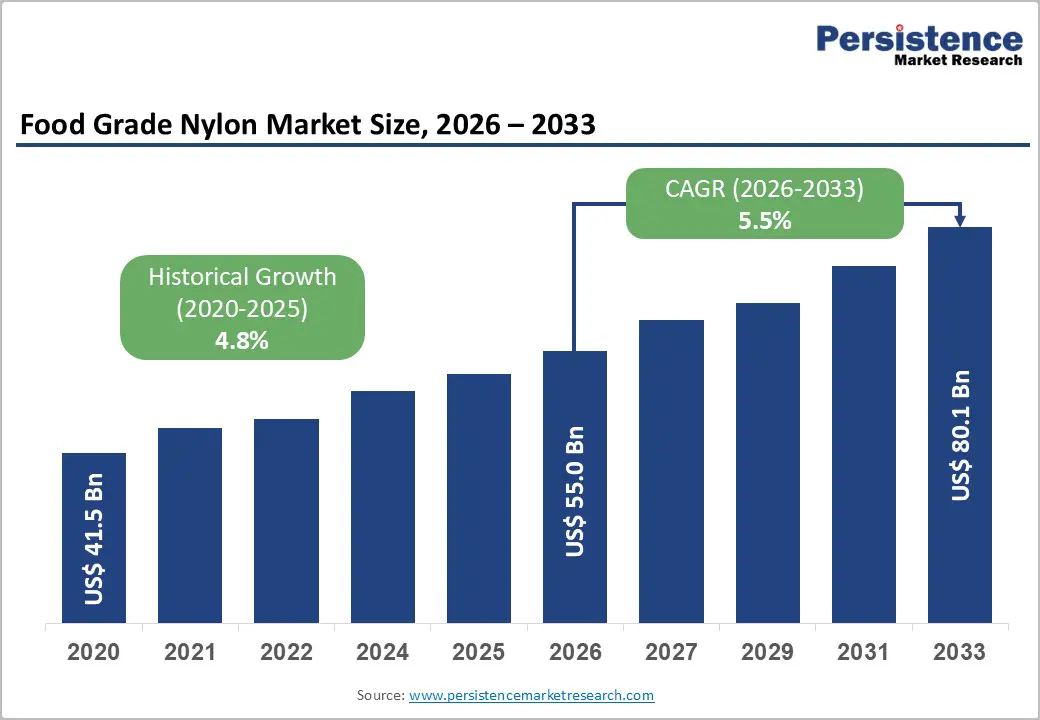

The global food grade nylon market size is likely to be valued at US$55.0 billion in 2026 and is expected to reach US$80.1 billion by 2033, growing at a CAGR of 5.5% during the forecast period from 2026 to 2033, driven by the intensifying global focus on food safety protocols and the rapid expansion of the convenience food sector in emerging economies.

Growth stems from rising demand for safe packaging in food and beverage sectors, driven by stringent regulations such as the FDA 21 CFR 177.1500 and EU Regulation 10/2011. Expanding e-commerce grocery channels and convenience food consumption are boosting the demand for high-performance food packaging materials. The transition from traditional metal components to high-performance polymers in food processing lines, coupled with innovations in multi-layer barrier packaging, serves as the primary engine for value generation.

Key Industry Highlights:

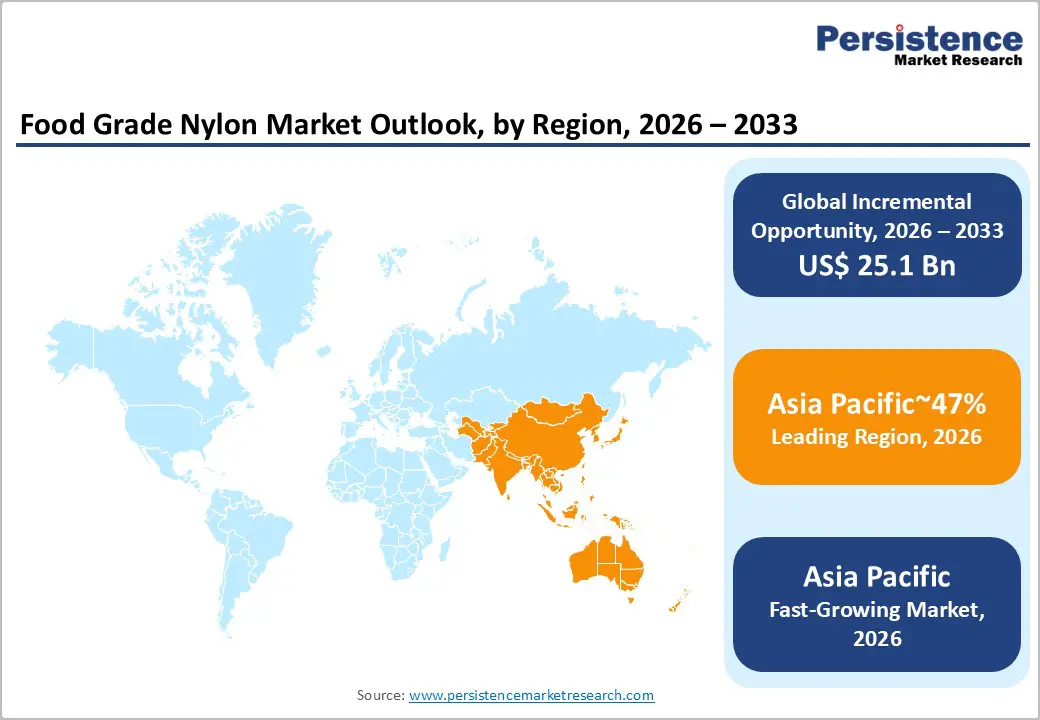

- Leading Region: Asia Pacific is projected to lead due to its integrated polymer manufacturing base, rapid urbanization, and expanding organized food retail ecosystem, accounting for approximately 47% share in 2026, supported by strong technology adoption in BOPA films and deep upstream feedstock integration advantages.

- Fastest-growing Region: Asia Pacific is anticipated to grow fastest due to accelerating industrial food processing capacity, supportive regulatory modernization in key economies, and expanding adoption of high-barrier packaging across e-commerce and convenience food sectors.

- Leading Nylon Type: Nylon 6 is expected to lead, accounting for approximately 60% share through widespread industrial adoption, high processing throughput efficiency in 2026, strong oxygen barrier performance, and broad utilization across flexible packaging and dairy preservation applications.

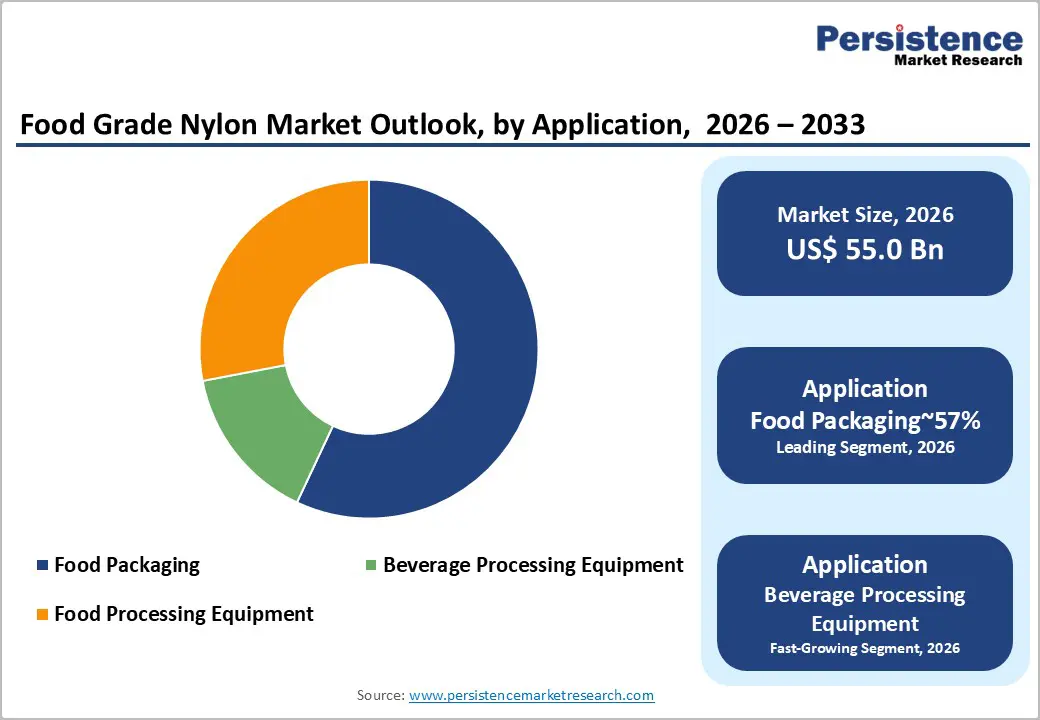

- Leading Application: Food packaging is projected to dominate for its material simplicity in multilayer integration, cost-to-performance balance, large-scale adoption across meat and cheese preservation, and critical functional oxygen barrier use across key retail sectors, holding approximately 57% share in 2026.

| Key Insights | Details |

|---|---|

| Food Grade Nylon Market Size (2026E) | US$55.0 Bn |

| Market Value Forecast (2033F) | US$80.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis – Escalating Food Safety Compliance Mandates Driving Certified Nylon Adoption

Stringent food contact regulations across major economies are intensifying material qualification requirements. Regulatory authorities such as the U.S. Food and Drug Administration enforce migration thresholds under defined polymer standards. Within Europe, the European Food Safety Authority mandates resin compliance testing before market authorization. These frameworks compel processors to adopt certified nylon formulations across equipment and packaging interfaces. Elevated incidence of foodborne illnesses reported by the World Health Organization reinforces preventive measures. Hazard analysis protocols embed polymer traceability and hygiene performance within procurement criteria. Consequently, certified food grade nylon secures structural demand across regulated processing environments.

Compliance escalation materially reshapes cost structures and procurement governance across food manufacturing systems. Non-compliant material substitution exposes processors to recall liabilities and reputational erosion. Testing, documentation, and migration validation increase qualification expenditures for polymer converters. However, regulatory alignment strengthens margin stability for certified nylon suppliers. Equipment manufacturers increasingly specify compliant polymers within design and tender documentation. This institutionalization embeds food grade nylon into long-term capital expenditure cycles. As regulatory scrutiny intensifies, substitution risk diminishes across hygiene-critical applications.

Metal to Plastic Conversion Reshaping Food Processing Equipment Design

The structural transition from metallic components toward engineered polymers is accelerating across food processing systems. Equipment manufacturers increasingly deploy Nylon six and Nylon sixty six in motion assemblies. These grades provide self-lubricating characteristics that reduce dependency on external greasing protocols. Superior wear resistance enhances operational continuity under repetitive mechanical stress conditions. Weight optimization through polymer substitution lowers system inertia and mechanical load factors. Reduced mass contributes to measurable energy efficiency gains across automated processing lines. This material evolution supports hygiene-focused equipment architectures aligned with sanitation compliance requirements.

The transition materially alters lifecycle economics within high-throughput processing environments. Lower equipment weight reduces motor strain and mitigates vibration-related component fatigue. Extended maintenance intervals decrease unplanned downtime across continuous production facilities. Polymer integration also simplifies part machining and modular replacement strategies. In beverage bottling and meat processing lines, durability thresholds remain operationally critical. Nylon-based gears and rollers sustain performance under washdown and thermal cycling conditions. These dynamics reinforce polymer substitution as a structural driver of equipment modernization.

Barrier Analysis – Petrochemical Feedstock Volatility Constraining Margin Stability

Food grade nylon production remains structurally exposed to upstream petrochemical price cycles. Core intermediates such as benzene and adipic acid track crude oil benchmarks. Fluctuations in Brent pricing are transmitted directly into virgin resin procurement costs. Input cost pass-through remains uneven across converter and processor contracts. Sudden feedstock inflation compresses contribution margins within mid-tier manufacturing segments. Working capital requirements expand as raw material inventories rise. This volatility introduces earnings variability across polymer processors supplying regulated food applications.

Cost instability also disrupts procurement planning and capital allocation frameworks. Processors facing margin compression often defer equipment modernization initiatives. Resin price unpredictability complicates long-term supply agreements and budgeting cycles. Buyers may temporarily shift toward recycled or blended material formulations. However, regulatory compliance constraints limit substitution flexibility in food contact environments. Elevated feedstock volatility increases pricing renegotiation frequency across polymer contracts. These dynamics collectively restrain investment confidence in food processing infrastructure expansion.

Environmental Regulation and Circular Economy Pressures Limiting Nylon Adoption

Synthetic polymer production carries a comparatively elevated environmental intensity profile. European policy instruments, such as the European Union plastic packaging levy, penalize non-recyclable material streams. Multi-layer nylon films present technical barriers within mechanical recycling infrastructures. Limited recyclability constrains acceptance across jurisdictions pursuing aggressive circular economy mandates. Packaging compliance frameworks increasingly prioritize mono-material and easily recoverable substrates. These regulatory dynamics compel resin producers to fund advanced chemical recycling capabilities. Elevated capital expenditure requirements alter cost competitiveness within food packaging polymer portfolios.

Simultaneously, plastic waste scrutiny accelerates substitution toward bio-based and lower-impact alternatives. Policy targets across Europe emphasize a substantial reduction in conventional plastic packaging volumes. Nylon’s recovery performance trails materials such as polyethylene terephthalate in established recycling systems. Competitive polymers, including polypropylene and polyethylene, exert additional pricing pressure. Substitution risk intensifies where sustainability procurement metrics dominate tender evaluations. Margin compression emerges as converters absorb compliance and technology transition costs. Absent material innovation, incremental market share erosion remains structurally plausible.

Opportunity Analysis – Bio-Based Nylon and Advanced Barrier Technologies Creating Strategic Upside

Regulatory decarbonization agendas under the European Union Green Deal framework are accelerating biobased polymer demand. Renewable feedstock nylons such as polyamide eleven and polyamide fifty six gain traction. These grades derived from castor oil support Scope three emission reduction strategies. Brand owners increasingly integrate certified green nylon into sustainable packaging portfolios. Recyclable grade development expands addressable demand within regulated food contact markets. Beverage packaging applications highlight unmet oxygen barrier performance requirements. Advanced formulation platforms increasingly leverage artificial intelligence to optimize resin properties.

Early certification in food contact compliant green nylon strengthens competitive differentiation. Bio-based segments are projected to secure meaningful valuation expansion through the next decade. Pricing structures indicate measurable premium realization relative to conventional polyamide grades. Premium capture reflects sustainability alignment and documented lifecycle emission benefits. Technology convergence enhances barrier integrity without compromising recyclability targets. Capital flows increasingly support chemical and mechanical recycling compatibility investments. These structural shifts reposition nylon within emerging circular polymer ecosystems.

Expansion of E-Commerce Grocery Logistics Driving High-Performance Packaging Demand

The acceleration of online grocery retail is reshaping packaging performance benchmarks. Digital food distribution models require materials resilient to extended handling cycles. Last-mile logistics impose puncture, compression, and temperature variability stresses. Food-grade nylon demonstrates superior mechanical integrity under distribution shock conditions. Its oxygen barrier capability preserves freshness within vacuum-sealed meal kits. Meat packaging formats increasingly incorporate multilayer nylon structures for transit stability. Growth in e-commerce grocery channels is projected at approximately seven percent annually.

Transit stable packaging is emerging as a structural procurement priority. Retailers internalize spoilage risk within competitive fulfillment service commitments. Durable polymer integration reduces product returns and cold chain failures. Nylon-based laminates extend shelf stability during decentralized delivery operations. Incremental market potential is estimated at several billion dollars through the forecast horizon. Packaging specifications increasingly align with e-commerce-centric distribution architectures. These dynamics embed high-performance nylon within evolving digital food retail ecosystems.

Category-wise Analysis

Nylon Type Insights

Nylon 6 is projected to lead the food grade nylon market, accounting for approximately 60% share in 2026, supported by its cost-to-performance advantage and versatility across flexible packaging formats. Its dominance is reinforced by strong oxygen barrier properties and processing efficiency in BOPA films used for bulk food pouches and dairy packaging. Manufacturers such as BASF SE, UBE Industries, and DuPont anchor this position through established resin platforms, including Ultramid and Zytel portfolios. Capacity expansions across Asia and low-carbon grade launches strengthen supply continuity and brand lock-in. Recycling initiatives such as Cerene from Ascend Performance Materials further enhance circularity credentials. Integrated compliance alignment and mature processing infrastructure sustain utilization intensity across high-volume packaging environments.

Nylon 66 is projected to be the fastest-growing segment in the food grade nylon market, driven by demand for higher thermal resistance and mechanical strength in retort packaging and cook-in-pouch applications. Its elevated melting point enables performance stability in high-temperature food processing components and beverage filling systems. Companies including Invista, Ascend Performance Materials, Asahi Kasei, and DOMO Chemicals are expanding specialty PA66 platforms to capture premium demand. Metal to plastic substitution trends and automation upgrades accelerate integration into precision equipment assemblies. Recycled and bio-based PA66 grades enhance sustainability positioning without compromising structural integrity. Growing validation in beverage and processed meat applications positions this segment to outpace overall market expansion.

Application Insights

Food packaging is projected to lead the food grade nylon market, accounting for approximately 57% share, supported by its critical role as a functional oxygen and aroma barrier in meat and cheese preservation. Dominance is reinforced by rising consumption of flexible multilayer films and vacuum skin packaging across urban retail networks. Resin platforms from BASF SE, UBE Industries, AdvanSix, and Unitika Ltd. underpin large-scale BOPA film production. Down gauging innovations and antimicrobial film integration enhance performance while controlling material intensity. Migration-compliant high-purity grades create barriers to entry for new suppliers. Recycling aligned nylon polyethylene blends further entrench deployment within structured global packaging ecosystems.

Beverage processing is projected to be the fastest-growing segment, driven by the modernization of bottling lines and demand for carbonation-resistant components. Equipment suppliers such as Krones AG and Sidel integrate high-performance nylon into filling valves and handling assemblies. Filtration leaders, including Pall Corporation, expand nylon membrane adoption in craft beer and wine clarification. Chemical-resistant grades withstand aggressive clean-in-place cycles across dairy and functional beverage plants. Metal detectable compounds and on-site additive manufacturing reduce downtime and recall exposure. Growing ready-to-drink beverage volumes reinforce durable polymer substitution across automated processing infrastructures.

Regional Insights

Asia Pacific Food Grade Nylon Market Trends

Asia Pacific is expected to lead the global market with a 47% revenue share and is projected to remain the fastest-growing region in 2026. The region is positioned to anchor the global supply of Nylon 6 and Nylon 6,6 resins, while simultaneously driving end-use consumption through rapid urbanization and dietary shifts toward packaged protein products. Demand is anticipated to scale in parallel with organized retail expansion, e-commerce logistics penetration, and rising middle-class purchasing power across dense metropolitan clusters. Integrated upstream feedstock availability, cost-competitive manufacturing, and strong foreign direct investment inflows are projected to preserve Asia Pacific’s structural advantage in both resin production and downstream flexible packaging innovation.

China is expected to function as the primary regional anchor, shaping supply discipline, regulatory enforcement, and capital allocation across the Asia Pacific nylon ecosystem. Implementation of updated food-contact migration standards is anticipated to elevate compliance thresholds, driving consolidation toward vertically integrated producers and technologically advanced converters. Simultaneously, multinational suppliers, including BASF SE, are expected to deepen localization strategies to align with regulatory traceability and performance certification requirements. Investment momentum is likely to concentrate around recyclable mono-material structures, bio-based polyamides, and high-puncture BOPA films tailored for e-commerce distribution. China is positioned to sustain Asia Pacific’s leadership trajectory while shaping pricing, technology standards, and vendor strategy evolution across the forecast horizon.

North America Food Grade Nylon Market Trends

North America is expected to remain the second-largest and structurally mature regional market, supported by a deeply institutionalized regulatory framework and high-value application intensity. The region is positioned as a premium-grade market where demand is anticipated to concentrate in specialized food packaging formats, including sous-vide systems and medical-grade supplement applications requiring documented migration stability and traceability. A stringent approval ecosystem led by the U.S. Food and Drug Administration is expected to preserve elevated entry barriers, favoring vertically integrated producers with validated toxicological data and long-cycle compliance capabilities. Supply-side stability is projected to remain anchored in a robust petrochemical base with competitive access to adipic acid and hexamethylenediamine, reinforcing cost efficiency relative to other mature markets.

The U.S. is expected to anchor regional momentum by defining compliance thresholds, technology standards, and circular-economy investment flows. State-level PFAS restrictions and extended producer responsibility frameworks are projected to intensify reformulation cycles, prompting resin suppliers such as Ascend Performance Materials and AdvanSix to prioritize specialty-grade innovation and recycled-content integration. Automation-led reshoring strategies are anticipated to strengthen domestic conversion capacity while mitigating geopolitical supply exposure. Closed-loop nylon recycling platforms are expected to scale in response to retailer-driven sustainability metrics and institutional procurement mandates.

Europe Food Grade Nylon Market Trends

Europe is expected to remain a structurally mature and regulation-led market, supported by harmonized sustainability mandates and advanced compliance architecture. The region is positioned as the global benchmark for environmental governance in food-contact polymers, where demand is anticipated to pivot from virgin resins toward bio-based and chemically recycled polyamides. Implementation of the European Green Deal and Packaging and Packaging Waste Regulation is expected to accelerate the transition toward recyclable nylon-rich nanomaterials and mass-balanced feedstock integration. While structurally higher energy costs and feedstock volatility are likely to compress commodity margins, the regional market is expected to defend value through specialization, digitalized manufacturing optimization, and premium high-temperature food-processing applications.

Germany is expected to function as the regional anchor, shaping industrial standards, recycling infrastructure scale-up, and specialty-grade innovation across the European nylon ecosystem. Chemical depolymerization investments coming online are anticipated to strengthen closed-loop monomer recovery, reinforcing circularity targets embedded within EU policy frameworks. Producers such as DOMO Chemicals and BASF SE are projected to expand mass-balanced and recyclable nylon portfolios to align with digital product passport requirements and PFAS phase-out mandates. As import pressure from Asia persists, Germany is positioned to sustain Europe’s competitive posture through high-value specialty polyamides, compliance-driven differentiation, and energy-efficiency-led operational recalibration.

Competitive Landscape

The global food grade nylon market is moderately consolidated, with leadership concentrated among multinational resin producers that collectively command a majority share of global supply. Competitive intensity is structured around high capital barriers in polymerization, compounding, and purification infrastructure, alongside stringent food-contact certification requirements under frameworks administered by the U.S. Food and Drug Administration and the European Food Safety Authority. Leading suppliers are expected to shape procurement standards through vertically integrated value chains, proprietary additive technologies, and embedded compliance documentation that supports multinational food processors. While global leaders consolidate influence through scale and certification depth, regional manufacturers such as Cast Nylon India are anticipated to compete on localized relationships and application-specific customization.

Key Industry Developments:

- In January 2026, ePAC Flexible Packaging unveiled Easy Open Barrier Films utilizing advanced nylon layers. Improves consumer accessibility for high-barrier food packaging such as coffee bags.

- In March 2025, BASF launched loopamid®, a circular textile-to-textile recycling process for Nylon 6. Enables high-quality nylon recovery with 70% lower CO2 emissions for sustainable packaging applications.

Companies Covered in Food Grade Nylon Market

- BASF SE

- DuPont de Nemours, Inc.

- Invista

- Ascend Performance Materials

- DOMO Chemicals

- Lanxess AG

- Toray Industries, Inc.

- AdvanSix Inc.

- DSM‑Firmenich

- Ube Industries, Ltd.

- Arkema S.A.

- Celanese Corporation

- RadiciGroup

- Huntsman Corporation

- Highsun Holding Group

- Asahi Kasei Corporation

Frequently Asked Questions

The global food grade nylon market is projected to be valued at US$55.0 billion in 2026 and is expected to reach US$80.1 billion by 2033, driven by rising food safety compliance mandates, expanding flexible packaging demand, and material substitution in high-performance food processing equipment.

Stringent food-contact compliance frameworks enforced by the U.S. Food and Drug Administration and the European Food Safety Authority are compelling processors to adopt certified nylon formulations with validated migration limits and traceability documentation, embedding compliant polyamides into long-term equipment and packaging procurement cycles.

The food grade nylon market is forecast to grow at a CAGR of 5.5% from 2026 to 2033, reflecting sustained demand from regulated packaging applications, metal-to-polymer conversion in processing systems, and the expansion of e-commerce grocery logistics.

Asia Pacific is the leading regional market, accounting for approximately 47% share, supported by large-scale Nylon 6 and Nylon 66 production capacity, expanding food processing infrastructure, and strong demand from organized retail and export-oriented packaging industries.

The market is moderately consolidated, with key players including BASF SE, DuPont de Nemours, Inc., Ascend Performance Materials, DOMO Chemicals, and Lanxess AG. These companies compete through upstream integration, regulatory certification depth, specialty-grade innovation, and circular polyamide platform development aligned with evolving sustainability mandates.