- LED & Lighting (Optoelectronics)

- Floor Displays Market

Floor Displays Market Size, Share, and Growth Forecast, 2026 - 2033

Floor Displays Market by Material Type (Corrugated, Plastic, Others), Application (Food & Beverage, Cosmetics & Personal Care, Others), Display Type, and Regional Analysis for 2026 - 2033

Floor Displays Market Size and Trends Analysis

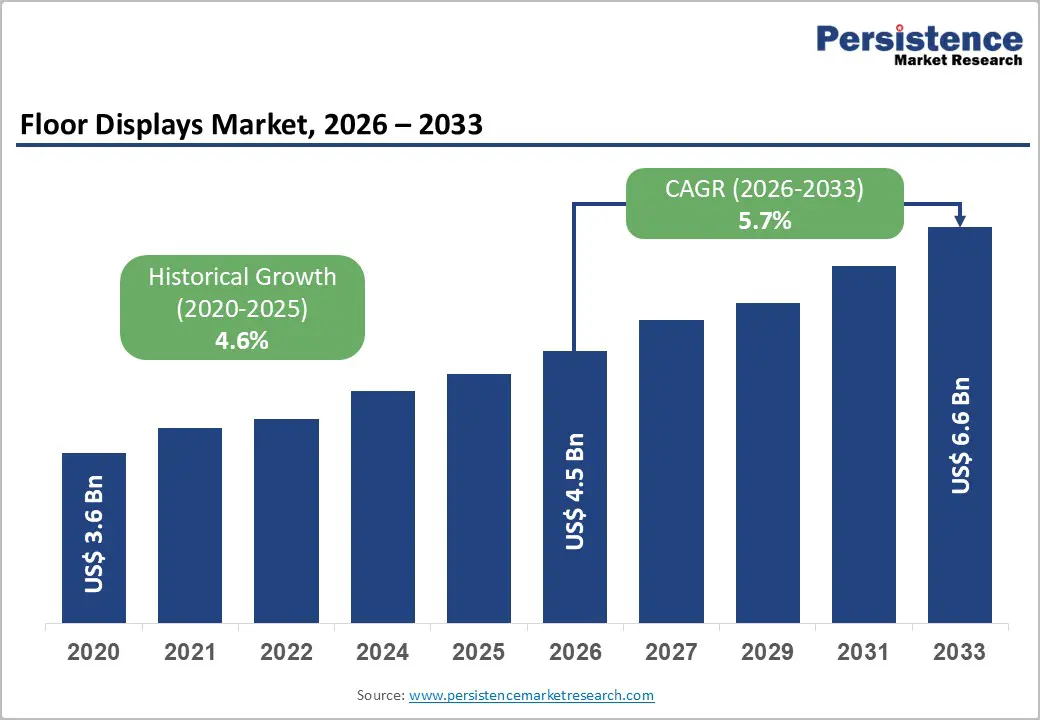

The global floor displays market size is likely to be valued at US$4.5 billion in 2026 and is expected to reach US$6.6 billion by 2033, growing at a CAGR of 5.7% between 2026 and 2033, driven by ongoing retail and FMCG promotional spending, a rising preference for premium and durable materials like plastic, acrylic, and metal, and increased investment in digital and interactive floor displays that incorporate AI and AR technologies for enhanced merchandising.

While corrugated materials dominate the market due to their cost-effectiveness and recyclability, digital and interactive formats are the fastest-growing category. The market reflects a blend of short-term retail promotional demand and long-term structural trends, such as sustainability, personalization, and omnichannel brand engagement.

Key Industry Highlights

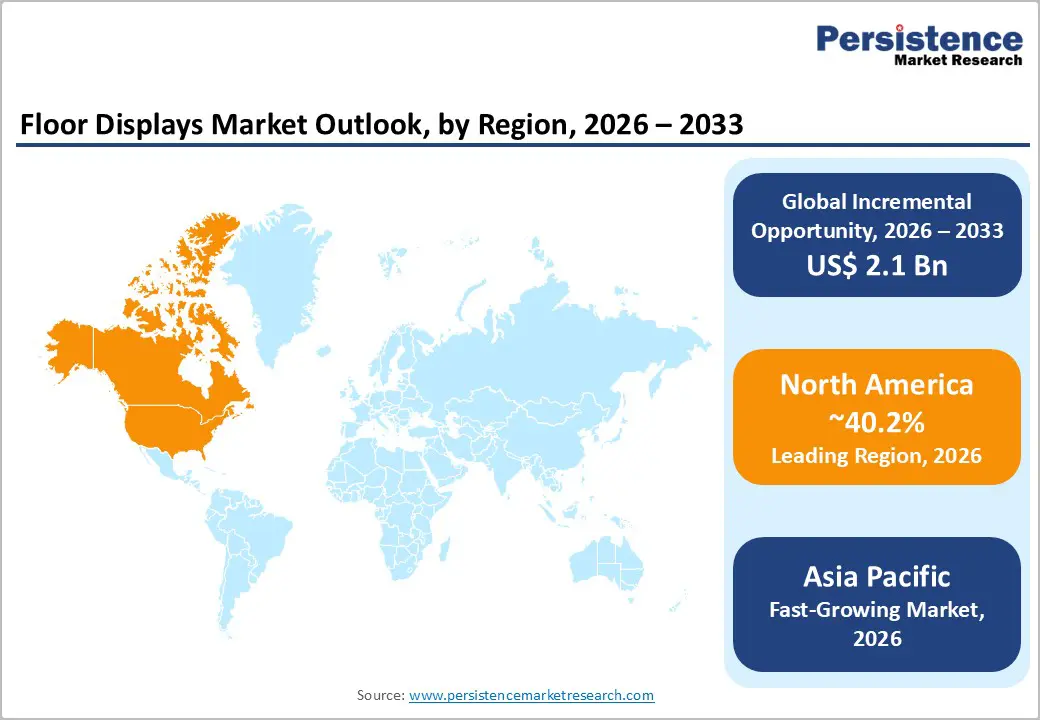

- Leading Region: North America is projected to hold approximately 40.2% of the market share in 2026, supported by a strong retail structure, frequent FMCG promotional cycles, and robust private-label expansion across major retail chains, particularly in the U.S.

- Fastest-growing Region: Asia Pacific remains the fastest-growing regional market, driven by retail modernization in China and India, rising consumer spending, and expanding organized retail penetration across tier-1 and tier-2 cities.

- Investment Plans: Companies are expanding regional production hubs, recycled fiber capacity, and digital printing infrastructure, while integrating vertically aligned service models to shorten lead times and improve campaign scalability.

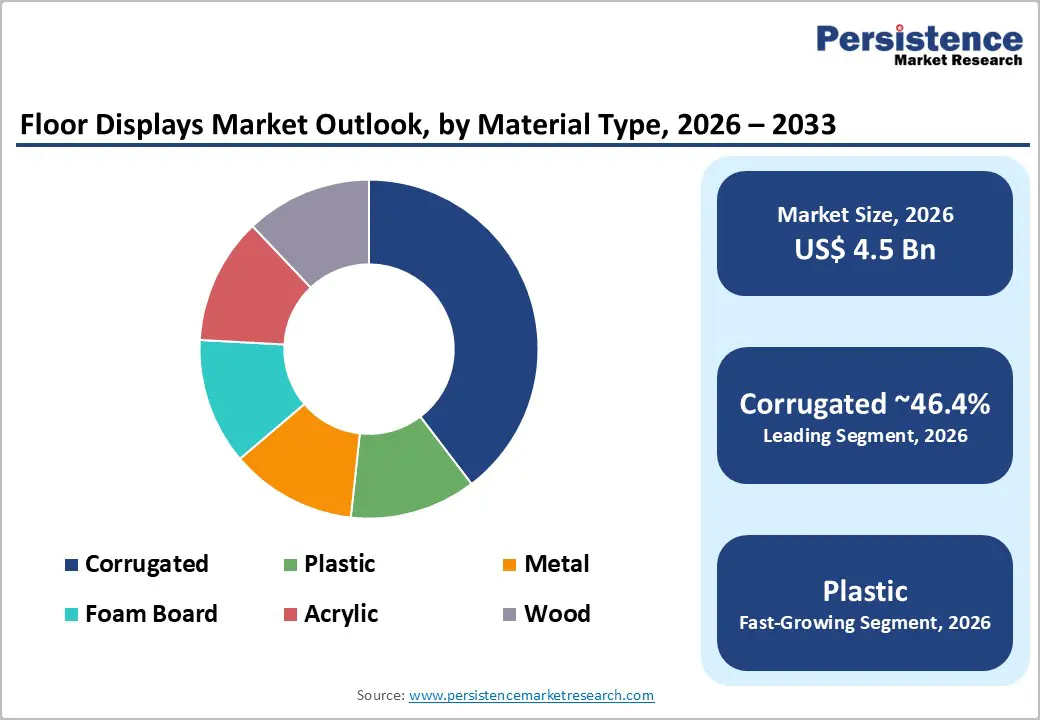

- Dominant Material Type: Corrugated material is expected to lead with an anticipated 46.4% share, benefiting from cost-efficiency, recyclability, lightweight construction, and suitability for large-scale FMCG promotional deployments.

- Leading Application: The food & beverage segment is expected to account for a 32.3% market share, supported by seasonal promotions, high inventory turnover, and impulse-driven merchandising strategies.

| Key Insights | Details |

|---|---|

| Floor Displays Market Size (2026E) | US$4.5 Bn |

| Market Value Forecast (2033F) | US$6.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Retail Promotional Investment & FMCG Shelf Strategies

Retailers and consumer packaged goods (CPG) brands continue allocating a meaningful portion of their marketing budgets to in-store promotional execution. Physical merchandising remains a proven driver of impulse purchasing, product trial, and seasonal campaign visibility. In large grocery and mass retail environments, a measurable share of trade promotion budgets, often in the single-digit to low-teen percentage range, is directed toward fixtures, floor displays, and point-of-purchase programs. This ongoing allocation supports the projected 5.7% CAGR between 2026 and 2033. For manufacturers, this driver creates predictable reorder cycles aligned with promotional calendars. Corrugated floor units, dump bins, and standees benefit from recurring campaigns in food and beverage, beverages, snacks, and household goods. National rollouts across chain retailers require scalable production and logistics capabilities, reinforcing stable volume demand across North America and Europe.

Materials Innovation and Digital Integration

Technological enhancements are increasing the revenue intensity of floor displays. Retailers are investing in reusable and modular units that incorporate rigid plastics, acrylic panels, and integrated digital components such as LCD screens, QR codes, or AR-enabled interfaces. These formats command higher average selling prices (ASPs) compared with traditional corrugated units and often deliver longer service lives. Digital and interactive floor displays are transforming traditional in-store merchandising by enabling dynamic content updates, real-time data collection, and measurable performance tracking. Through the integration of technologies such as digital screens, sensors, and analytics platforms, these solutions move beyond static promotional fixtures and function as accountable, insight-driven marketing assets. While overall unit growth in the floor display market remains relatively moderate, the increasing adoption of higher-value, technology-enabled installations is contributing to stronger revenue expansion. Premium pricing, enhanced functionality, and improved return-on-investment for retailers and brands are driving this value shift.

Sustainability and Regulatory Pressure toward Recycled Materials

Environmental, social, and governance (ESG) commitments among major retailers are reshaping procurement standards. Retail chains increasingly require suppliers to provide displays made from recyclable materials, certified fiber content, and low-emission production processes. Corrugated materials benefit from well-established recycling streams and lower carbon footprints relative to certain plastics and metals. Although sustainability compliance may increase production costs through certification, traceability, and documentation requirements, it strengthens preferred supplier relationships and expands order volumes. Innovation in recycled plastics and coated boards further supports eco-conscious merchandising strategies. These regulatory and buyer-driven requirements function as structural demand amplifiers for manufacturers capable of meeting certified sustainability benchmarks.

Barrier Analysis - Cost Pressures and Raw Material Volatility

Floor display manufacturing is exposed to commodity price fluctuations across paperboard, plastics, and metal inputs. Corrugated pulp prices and resin costs can shift in response to global supply-demand imbalances, trade dynamics, and energy prices. A sustained 10-15% increase in pulp pricing, for example, can compress supplier gross margins by several percentage points if cost pass-through is delayed. Freight cost volatility also affects profitability, particularly for bulky assembled units. Smaller display specialists without long-term procurement contracts or hedging mechanisms face greater exposure, potentially limiting their competitiveness against larger integrated suppliers.

Supply Chain Lead Times and Production Complexity

Customized floor displays often require short production cycles aligned with promotional launch windows. Complex designs involving multiple components, specialty finishes, or integrated digital hardware increase assembly time and quality-control requirements. Delays can materially impact campaign effectiveness, particularly for seasonal promotions. Missed promotional windows can reduce marketing return on investment by double-digit percentages in high-turn categories. Retailers are therefore demanding faster fulfillment and localized production capacity. Suppliers must either invest in regional facilities or maintain inventory buffers, both capital-intensive strategies that may limit margin expansion.

Opportunity Analysis - Premium Reusable Retail Fixtures

Reusable plastic, acrylic, and metal floor fixtures represent a substantial value-creation opportunity. These installations generate higher margins due to durability, design sophistication, and extended service contracts. Manufacturers can differentiate through modular engineering, refurbishment programs, and installation services. Transitioning from one-time promotional sales to lifecycle-based service models enhances recurring revenue streams and strengthens long-term retailer partnerships.

Digital and Interactive Conversion with Data Services

Digital and interactive displays offer monetization beyond hardware sales. AI-enabled recommendations, AR-based product visualization, and QR-driven engagement create opportunities for subscription-based content management and analytics services. Bundling hardware with software licenses and performance dashboards allows suppliers to capture recurring income while delivering measurable marketing value to brands.

Emerging Markets and Retail Modernization

Rapid urbanization and retail infrastructure expansion across Asia Pacific are increasing demand for modern merchandising formats. Growing middle-class consumption in urban centers supports premium in-store branding investments. Capturing even an additional 1-2% of global market share by 2033 through expansion in high-growth economies could translate into tens of millions of dollars in incremental revenue. Strategic partnerships with local manufacturers reduce freight exposure and enhance compliance with regional sustainability standards.

Category-wise Analysis

Material Type Insights

Corrugated board is anticipated to account for approximately 46.4% of market share in 2026, maintaining its position as the dominant material segment. Its structural strength-to-weight ratio, low production cost, and ease of die-cutting make it highly suitable for mass promotional rollouts across supermarkets and hypermarkets. Brands in beverages and snacks frequently deploy corrugated floor stands, pallet-ready displays, and dump bins for limited-time offers, for example, carbonated drink multipacks or festive confectionery bundles. The material’s compatibility with high-quality flexographic and digital printing enables vibrant branding at scale. Growing retailer sustainability mandates and recycling targets further strengthen demand for fiber-based, biodegradable display solutions.

Plastic materials are gaining share due to their durability, structural rigidity, and premium aesthetic appeal. Rigid polymers such as PET and polypropylene enable modular construction, reusable fixtures, and integration with lighting or digital screens. Cosmetics brands often use molded plastic floor units with illuminated shelving to enhance in-store visibility for skincare launches. Consumer electronics retailers deploy reinforced plastic display stands to securely hold high-value products such as headphones or smart devices. Advances in recycled resin content and improved injection-molding technologies are improving environmental performance while retaining design flexibility. These attributes position plastic as the preferred choice for long-term, high-traffic retail environments.

Application Insights

The food and beverage segment is anticipated to hold approximately 32.3% of market share in 2026, making it the leading application category. Frequent product launches, seasonal promotions, and impulse-driven purchasing patterns drive sustained investment in aisle-end and freestanding displays. For instance, snack manufacturers commonly introduce themed corrugated stands during major sporting events, while beverage companies deploy pallet displays during summer promotional cycles. High inventory turnover supports repeat display orders, ensuring consistent procurement volumes. Retail chains favor scalable, lightweight display formats that can be assembled quickly across multiple store locations, reinforcing this segment’s structural dominance.

The cosmetics and personal care segment represents the fastest-growing application segment. Premiumization strategies and experiential retail formats encourage brands to invest in visually sophisticated and interactive floor displays. Skincare and beauty brands frequently incorporate LED backlighting, mirrors, and QR-code-enabled engagement features to enhance shopper interaction. The shift toward influencer-driven product launches and limited-edition collections increases the need for eye-catching in-store visibility. Durable materials such as reinforced plastic or hybrid wood-metal combinations support multi-season usage, enabling brands to justify higher capital expenditure per installation while strengthening brand positioning within specialty and department stores.

Regional Insights

North America Floor Displays Market Trends - Organized Retail Scale & Promotional Standardization

North America is projected to account for an estimated 40.2% of the market, positioning it as the largest regional contributor. The U.S. drives the majority of regional demand due to its highly organized retail ecosystem, dense network of big-box stores, and structured promotional calendars tied to holidays, sporting events, and seasonal resets. Large retailers such as Walmart and Target continue to rely heavily on standardized yet customizable floor displays to support nationwide FMCG rollouts and private-label expansions, reinforcing consistent procurement volumes.

Procurement models range from centralized national contracts managed by brand owners to direct brand-retailer collaborations for exclusive campaigns. Growth is fueled by high-frequency FMCG promotions, increasing private-label penetration, and rising investment in experiential merchandising, particularly within beauty, electronics, and seasonal categories. For example, global brands such as Procter & Gamble regularly deploy short-cycle corrugated displays for household and personal care launches, while premium electronics brands use durable modular fixtures for extended in-store visibility.

Regulatory pressure at state and retailer levels, especially around recyclability and packaging waste reduction, continues to influence material selection, accelerating the shift toward fiber-based and recycled-content displays. Investment trends increasingly favor regional production hubs, expanded digital printing capacity, and vertically integrated service models that shorten lead times and support rapid campaign execution across the U.S.

Europe Floor Displays Market Trends - Sustainability-Driven Compliance & Premium Merchandising

Europe represents a mature yet structurally stable market, shaped by stringent sustainability regulations, extended producer responsibility (EPR) frameworks, and harmonized packaging directives. Germany leads the region in manufacturing innovation and sustainable fiber processing, supported by its strong industrial base and emphasis on circular economy practices. German suppliers frequently collaborate with multinational brands to develop high-recyclability corrugated and hybrid displays, aligning with retailer sustainability scorecards.

The U.K. and France place greater emphasis on premium merchandising and digitally enabled retail formats, particularly within cosmetics, luxury food, and specialty retail. Brands such as L'Oréal invest in high-finish, semi-permanent floor displays incorporating lighting and modular components to enhance in-store storytelling, especially in department stores and drugstore chains. Spain, meanwhile, supports steady seasonal promotional demand, driven by tourism-linked retail activity and high promotional intensity in food, beverages, and confectionery.

Across the region, regulatory compliance related to recyclability, material traceability, and lifecycle transparency directly influences procurement decisions. Investment is increasingly directed toward recycled fiber capacity, short-run digital printing, and closed-loop material recovery systems. European suppliers compete less on price and more on sustainability credentials, documentation, and verified environmental performance, reinforcing Europe’s role as a benchmark market for compliant and environmentally responsible floor display solutions.

Asia Pacific Floor Displays Market Trends - Rapid Retail Expansion & Manufacturing Scale-Up

Asia Pacific stands out as the fastest-growing regional market, driven by rapid urbanization, rising consumer spending, and continued expansion of organized retail formats. China leads the region in scale and manufacturing capacity, serving both its vast domestic consumption base and export-oriented display production. Large-format retailers and e-commerce-linked offline formats increasingly deploy high-volume corrugated and hybrid displays to support aggressive promotional cycles. Chinese manufacturers supply global brands while simultaneously upgrading domestic capabilities in digital printing and automated finishing.

Japan emphasizes premium retail fixtures and advanced display integration, reflecting its focus on design precision and brand experience. Retailers frequently adopt semi-permanent and reusable floor displays for cosmetics, electronics, and specialty foods, favoring durability and refined aesthetics. India is demonstrating rapid momentum as organized retail expands across tier-1 and tier-2 cities. Chains such as Reliance Retail are scaling standardized floor display programs to support private-label growth and national brand partnerships, directly boosting demand for cost-effective yet visually impactful display solutions.

Regional growth is supported by improving retail infrastructure, rising brand investment in in-store visibility, and increasing localization of display production. Regulatory developments related to plastic waste management and recycling targets are shaping material innovation, particularly in India and parts of Southeast Asia. In response, multinational suppliers are expanding regional production footprints and forming local partnerships to reduce lead times, manage costs, and capture long-term growth opportunities across Asia Pacific.

Competitive Landscape

The global floor displays market is moderately concentrated, where large integrated packaging corporations and specialized display manufacturers operate alongside one another. Leading integrated firms collectively account for an estimated 35-40% of global volume, leveraging scale, national retail contracts, and vertically integrated production capabilities. In contrast, numerous regional and niche specialists serve localized, short-run, and premium segments, particularly in cosmetics, electronics, and experiential retail categories.

Large players dominate multi-location rollouts and long-term procurement agreements, while agile specialists excel in customized, digitally enhanced, and design-intensive installations. Core competitive strategies include vertical integration across design-to-production workflows, development of premium reusable and modular fixtures, and bundling of digital engagement services. Differentiation increasingly centers on sustainability certifications, rapid fulfillment capabilities, lifecycle transparency, and the ability to demonstrate measurable in-store engagement performance.

Key Industry Developments:

- In 2025, DS Smith Plc and Carlsberg Group collaborated to develop a new recyclable corrugated cardboard floor display for a premium beer brand, focusing on enhanced in-store appeal and end-of-life recyclability as part of sustainability initiatives. This showcased how floor displays can combine strong branding with eco-friendly materials.

- In March 2025, Standee Company announced a strategic partnership with Visual Merchandising to co-develop a modular POP display system designed for accelerated deployment in fast-turn retail environments. This collaboration aims to offer brands flexible and customizable floor and point-of-purchase solutions.

Companies Covered in Floor Displays Market

- DS Smith PLC

- WestRock Company

- Smurfit Kappa Group PLC

- International Paper Company

- Sonoco Products Company

- Menasha Packaging Company LLC

- Georgia-Pacific LLC

- Pratt Industries Inc.

- FFR Merchandising Inc.

- Marketing Alliance Group

- Creative Displays Now

- Great Northern Corporation

- Graphic Packaging International

- Stora Enso Oyj

Frequently Asked Questions

The global floor displays market is valued at approximately US$4.5 billion in 2026.

The floor displays market is projected to reach approximately US$6.6 billion by 2033.

Key trends include growing adoption of recyclable corrugated materials, rising demand for modular and reusable plastic fixtures, expansion of digital printing for short-run campaigns, and increasing integration of interactive features such as LED lighting and QR-enabled engagement in cosmetics and electronics displays.

Corrugated material leads the market with an anticipated 46.4% share, driven by cost efficiency, lightweight structure, high print customization capability, and alignment with retailer sustainability mandates.

The floor displays market is projected to grow at a CAGR of approximately 5.7% through 2033.

Major players include Smurfit Kappa, DS Smith, International Paper, WestRock, and Sonoco Products Company.