- Medical Devices

- Fine Medical Wire Market

Fine Medical Wire Market Size, Trends, Share, Growth, and Regional Forecast, 2025 to 2032

Fine Medical Wire Market by Wire Shape (Flat Wire, Round Wire, Others), by Material (Metals, Alloys), by Application (Endoscopic, Orthodontic, Orthopaedic, Surgical Enclosure, Vascular Therapy, Stimulation Therapy, Cochlear Remediation, Neurostimulation, Others), by Regional Analysis, 2025 - 2032

Fine Medical Wire Market Share and Trends Analysis

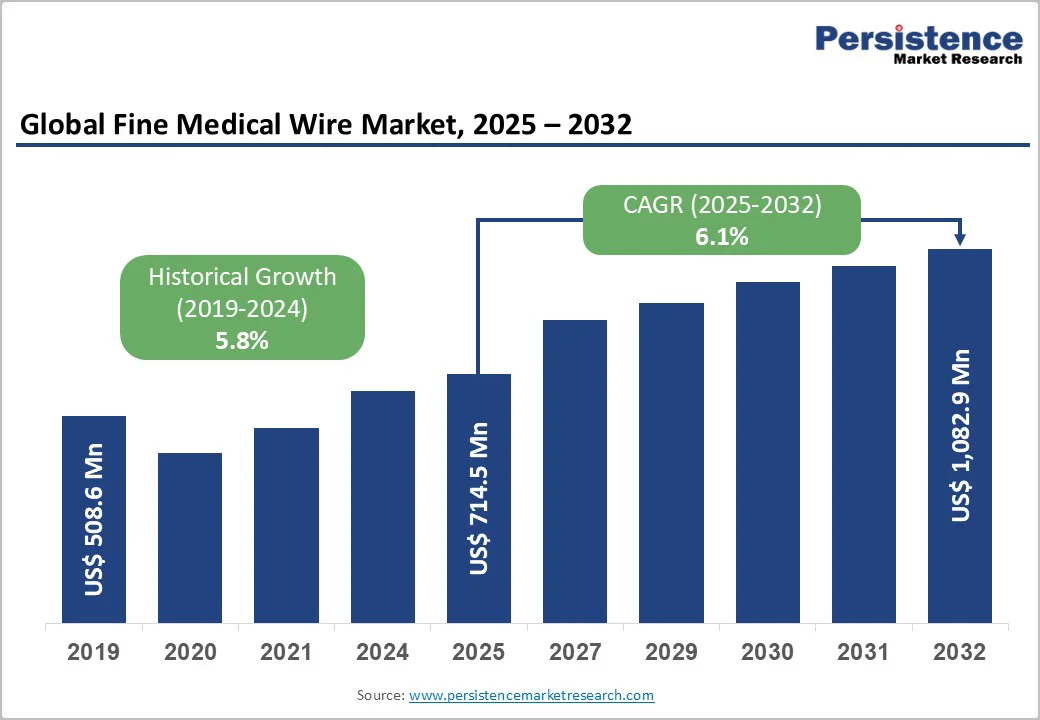

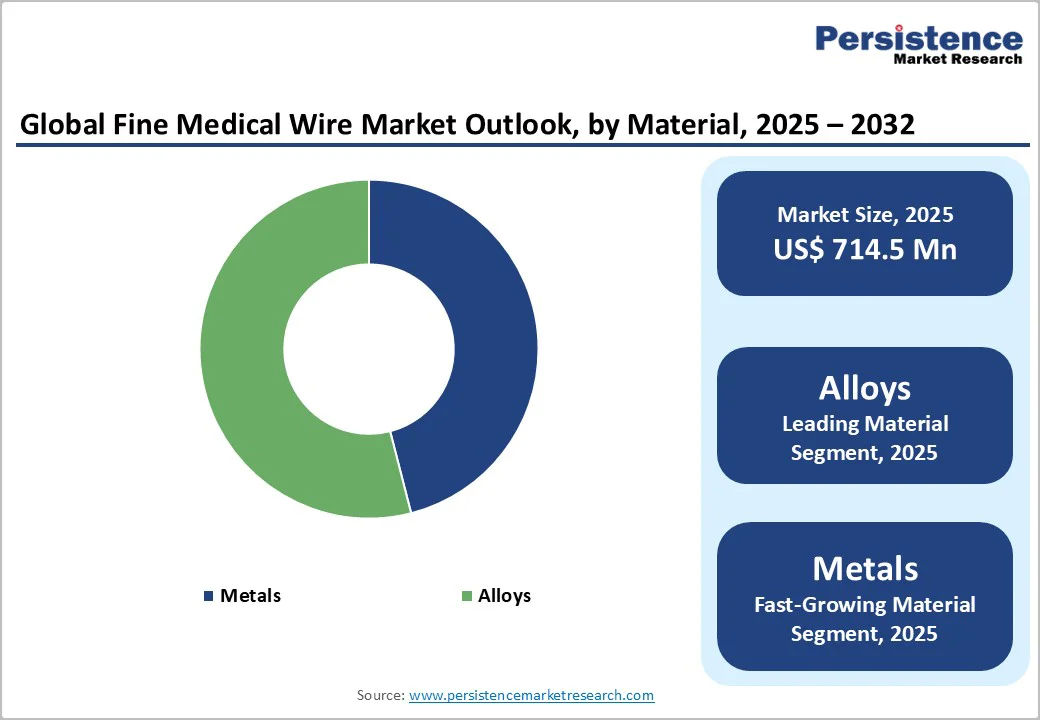

The global fine medical wire market is valued at US$714.5 million in 2025 and is projected to reach US$1,082.9 million, growing at a CAGR of 6.1% from 2025 to 2032.

The minimally invasive method involves a surgical procedure that reduces the size of incisions required and lessens wound healing time and associated risk of infection and pain. An increasing number of older adults prefer non-invasive or minimally invasive treatments. In addition, the advent of dental materials science in orthodontics presents a significant opportunity for the fine medical wire industry to grow.

Key Industry Highlights

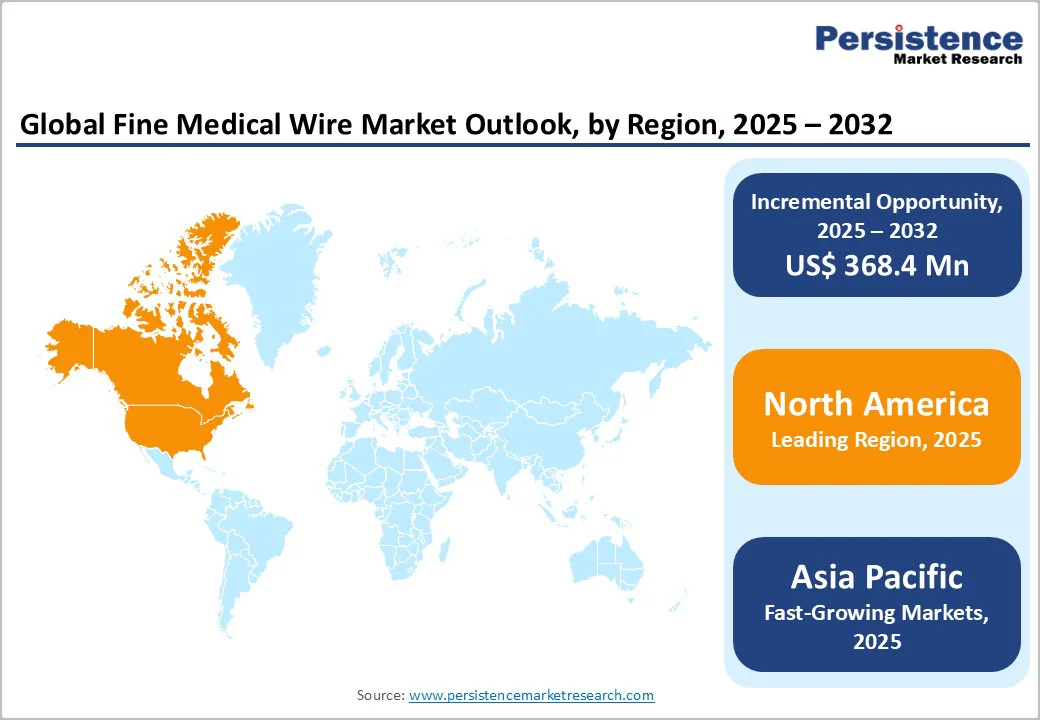

- Leading Region: North America leads global market demand, accounting for more than a third of the total market share, driven by high-tech innovation and robust treatment rates for chronic conditions.

- Fastest Growing Region: Asia Pacific registers the quickest growth, driven by healthcare spending and the boom in modern surgical procedures in emerging markets.

- Dominant Segment: Flat wires account for the top share in the wire shape category, due to better physical properties and efficiency for advanced medical use.

- Fastest Growing: Alloy-based wires are the most dynamic segment, driven by material innovation and precision in applications across orthopedics and stimulation therapies.

| Key Insights | Details |

|---|---|

| Fine Medical Wire Market Size (2025E) | US$ 714.5 Mn |

| Market Value Forecast (2032F) | US$ 1,082.9 Mn |

| Projected Growth (CAGR 2025 to 2032) | 6.1% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.8% |

Market Dynamics

Driver - Increasing Prevalence of Chronic Diseases Boosts Market Growth

The increasing prevalence of chronic diseases such as cardiovascular disorders, neurological conditions, orthopedic ailments, and cancer is a key driver of the global fine medical wire market. These wires play a vital role in various medical procedures, including stent placements, neurovascular interventions, orthopedic fixations, and tumor excisions, where precision and flexibility are essential.

According to the World Health Organization (WHO), cardiovascular diseases cause around 17.9 million deaths annually, followed by cancers at 9.3 million, chronic respiratory diseases at 4.1 million, and diabetes at 2 million (including diabetes-related kidney diseases).

The growing burden of these conditions has led to an increased need for advanced medical devices capable of performing minimally invasive and high-precision treatments. Additionally, lifestyle changes, an aging global population, and rising healthcare awareness are driving this demand.

As healthcare systems emphasize improved treatment outcomes and shorter recovery times, fine medical wires designed for enhanced biocompatibility, durability, and control are witnessing steady adoption, thereby fueling consistent growth in the market worldwide.

Restraints - Rising cost of Raw Material Affects the Medical Wire Manufacturing

The medical device industry is growing exponentially, driven by innovative products. Demand for high-quality medical equipment is rising, but the high cost of raw materials is a major hindrance to market growth.

In recent years, there has been an increase in the cost of various raw materials, including steel, aluminium, copper and iron ore, creating an increased burden for the manufacturers of fine medical wires. Furthermore, steel producers have been paying high prices for scrap metal rather than iron ore. This, in turn, is impacting the growth of the market.

One of the major restraints of fine medical wire is the wire breaks and internal defects that occur during the drawing of superfine wires. The fine wire defects can occur due to the difference between tensile stress and compressive stress during the drawing process.

Inclusions in the wire material mostly induce the breakage of wire during the drawing process of fine wires. It was analysed that the fine wire with an inclusion, when a big inclusion passes through a die, the drawing stress rapidly increases, causing wire breakage.

Opportunity - Rising Demand for Customization and Personalized Medicine Creating Growth Opportunities in the Market

The growing focus on customization and personalized medicine presents a significant opportunity for the fine medical wire market. As healthcare shifts toward patient-specific treatment approaches, there is a increasing need for medical components tailored to individual anatomical and procedural requirements.

Fine medical wires are increasingly designed with customizable properties, including multiple diameters, coatings, materials, and flexibility levels, to meet specific surgical and diagnostic applications. These personalized designs enhance procedural accuracy, reduce complications, and improve patient outcomes in cardiovascular, neurovascular, and orthopedic interventions.

Moreover, advancements in materials science and manufacturing technologies, including microfabrication and precision engineering, enable the production of medical wires that support next-generation devices such as customized stents, catheters, and guidewires.

The growing adoption of personalized medical devices, driven by the trend toward precision medicine, presents opportunities for manufacturers to collaborate with healthcare providers and device makers to deliver patient-specific solutions. As a result, customization and personalization are expected to drive innovation and long-term growth in the global fine medical wire market.

Category-wise Analysis

By Wire Shape Insights

The flat wire products segment captured approximately 47.8% of the total fine medical wire market in 2024, emerging as the leading category. Flat medical wires are known for their exceptional dimensional precision, high strength tolerance, and consistent curvature, making them ideal for demanding medical applications.

Their superior flexibility during bending allows easy integration into compact and complex medical devices. Owing to these characteristics, flat wires are extensively utilized in the manufacturing of advanced equipment such as pacemakers, catheters, surgical instruments, and defibrillators.

The increasing demand for minimally invasive procedures and high-performance medical tools has further boosted their adoption across the healthcare industry. Moreover, ongoing advancements in material science, surface finishing, and microfabrication technologies have enhanced the durability, conductivity, and biocompatibility of flat wires.

These innovations enable improved performance, longer device lifespan, and safer patient outcomes. As medical device manufacturers continue to prioritize precision and flexibility, the flat wire segment remains a vital contributor to the overall growth of the fine medical wire market.

By Modality Insights

The alloy segment, by material, accounted for approximately 54.0% of the global fine medical wire market share in 2024, making it the dominant category. Alloys are mixtures of metals or metals combined with other elements to enhance strength, ductility, corrosion resistance, and biocompatibility.

These properties make them highly suitable for various diagnostic and therapeutic applications where precision and reliability are crucial. Owing to their superior mechanical performance and biological compatibility, alloy-based medical wires are extensively utilized across multiple healthcare segments.

Materials such as stainless steel, Nitinol, and MP35N are widely used in the manufacture of guidewires, orthodontic appliances, catheters, and implantable medical devices. Their ability to maintain flexibility, durability, and corrosion resistance under physiological conditions ensures consistent performance and patient safety.

Additionally, continuous advancements in alloy processing and surface treatment technologies have improved wire precision and longevity, contributing to better clinical outcomes. The combination of versatility, high performance, and compatibility positions alloy materials as a critical component driving revenue and innovation in the global fine medical wire market.

Region-wise Analysis

North America Fine Medical Wire Market Insights

The U.S. accounted for nearly 87% of the North American fine medical wire market in 2025, and this dominance is expected to continue in the coming years. The growing prevalence of cardiovascular diseases is a major factor driving demand for fine medical wires in the country. According to the Centers for Disease Control and Prevention (CDC), in 2022, one person in the United States died from cardiovascular disease every 34 seconds.

Conditions such as aortic dissection and aneurysm pose significant challenges across surgical, radiologic, and critical care disciplines, underscoring the need for precision medical devices. Fine medical wires are essential components in catheter reinforcements, pacing leads, and guidewires used to manage such disorders. North America’s strong healthcare infrastructure, advanced research ecosystem, and high healthcare expenditure further support the market’s growth.

Asia and Pacific Fine Medical Wire Market Trends & Insights

Asia Pacific represents the fastest-growing region in the global fine medical wire market, driven by rapid industrialization, expanding healthcare infrastructure, and increasing healthcare spending.

The region’s aging population and growing burden of chronic diseases such as cardiovascular disorders and diabetes are fueling the need for advanced medical devices utilizing fine medical wires. Countries like China, Japan, and India are emerging as key contributors to market growth, supported by technological innovation and the establishment of local manufacturing units.

China is expanding its production capacity for medical components, reducing dependence on imports and enhancing export potential. Japan remains at the forefront in precision engineering and high-quality medical wire applications, while India is experiencing rapid adoption driven by government-led healthcare programs and private investments.

Additionally, rising medical tourism and the presence of cost-effective manufacturing capabilities are boosting regional competitiveness. With strong public-private partnerships and continuous innovation, the Asia-Pacific region is expected to experience sustained growth and gradually become a global hub for fine medical wire production and application.

Competitive Landscape

The fine medical wire market is moderately fragmented, with global leaders leveraging R&D to stay competitive. Established players focus on expanding their specialty product portfolios and form strategic collaborations to address regional as well as global demand. New entrants and niche manufacturers are active in alloy innovations and coating technologies to differentiate their product offerings.

Key Industry Developments:

- In November 2024, Ulbrich Stainless Steels & Special Metals completed the acquisition of ATI Inc.'s precision-rolled strip operations located in New Bedford, Massachusetts, and Remscheid, Germany.

- In October 2024, Ulbrich introduced the Braid Wire Accelerator® Program to support faster medical device development. This initiative enables quicker turnaround times and greater precision in meeting specific design and performance requirements.

- In Oct 2021, Sandvik acquired the medical wire forming company Accuratech Group.

Companies Covered in Fine Medical Wire Market

- Elmet Technologies

- Ulbrich Stainless Steels and Special Metals

- American Elements

- Sandvik

- Central Wire

- Haynes International

- Elektrisola Group

- Prince Izant Medical

- Metal Cutting Corporation

- Sumiden wire (Sumitomo)

- California Fine Wire

- Luma Metall

- Tokusen Kogyo Co., Ltd.

- KOS LTD

- Others

Frequently Asked Questions

The global fine medical wire market is projected to be valued at US$ 714.5 Mn in 2025.

Growing demand for minimally invasive procedures, advanced medical devices, and precision surgical instruments drives the global fine medical wire market.

The global market is expected to witness a CAGR of 6.1% between 2025 and 2032.

Rising adoption of tungsten wire, increased awareness regarding fine medical wire for specific application, and outbreak of COVID-19 creating vast opportunity for healthcare industries to expand are some of the key trends in this market.

Major companies include Elmet Technologies, Ulbrich Stainless Steels and Special Metals, American Elements, Sandvik, Central Wire, and several others.