- Bulk Chemicals

- Specialties of Lube Oil Refinery Market

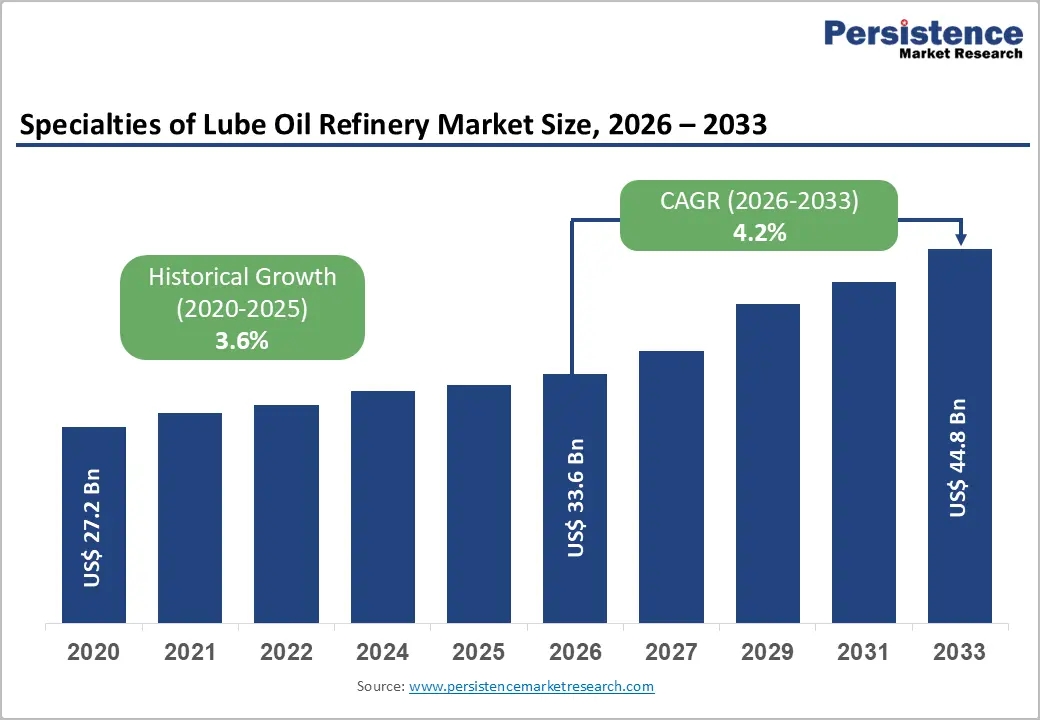

Specialties of Lube Oil Refinery Market Size, Share, and Growth Forecast 2026 - 2033

Specialties of Lube Oil Refinery Market by Product Type (Fully Refined Wax, White Oil, Rubber Process Oil, Slack Wax, Semi Refined Wax, Petrolatum, Microcrystalline Wax, Others), End-user (Automotive, Pharmaceutical, Textile, Cosmetic, Food and Beverages, Others), and Regional Analysis, 2026 - 2033

Specialties of Lube Oil Refinery Market Size and Trend Analysis

The global specialties of lube oil refinery market size is expected to be valued at US$ 33.6 billion in 2026 and projected to reach US$ 44.8 billion by 2033, growing at a CAGR of 4.2% between 2026 and 2033.

Sustained growth in the lube oil refinery specialties market is driven by the diversified industrial demand for high-purity specialty petroleum derivatives across pharmaceutical, cosmetic, food-grade, automotive, and textile applications.

Specialty products such as white oil, fully refined wax, petrolatum, and microcrystalline wax, produced as co-products of the lubricant base oil refining process, are experiencing robust demand expansion driven by growing industrialization in the Asia Pacific, expanding pharmaceutical and personal care manufacturing, and the rising application of rubber process oils in the rapidly growing global tire and rubber goods industry.

Key Industry Highlights

- Leading Region: Asia Pacific holds approximately 43% of the global lube oil refinery specialties market share in 2026, anchored by China's dominance in tire and rubber manufacturing, representing over 60% of global tire output, and India's world-leading pharmaceutical generics production.

- Fastest Growing Market: Middle East & Africa is the fastest-growing region through 2033, driven by Saudi Aramco and ADNOC's downstream refinery specialty expansion strategies and Africa's rapidly growing pharmaceutical and personal care manufacturing sectors, creating incremental white oil and petrolatum demand.

- Dominant Product Segment: Fully Refined Wax commands approximately 36% of global product type share in 2026, driven by broad applications across FDA-compliant food packaging, candle manufacturing, cosmetic formulation, and pharmaceutical-grade specialty wax requirements globally.

- Fastest Growing Product Segment: Rubber Process Oil (RPO) is the fastest-growing product type at 5% CAGR, driven by expanding global tire production tracked by the IRSG and REACH-compliant TDAE RPO demand in European tire manufacturing supply chains.

- Key Opportunity: Producers investing in USP and NSF H1 certified food-grade and pharmaceutical-grade white oil production infrastructure in Asia Pacific and Middle East markets stand to capture rapidly growing premium-tier demand from expanding pharmaceutical generics manufacturing and certified food processing sectors.

DRO Analysis

Market Growth Drivers

Expanding Pharmaceutical and Cosmetics Applications for High-Purity White Oil and Petrolatum

The growing global pharmaceutical and personal care manufacturing sectors are generating accelerating demand for white oil (mineral oil) and petrolatum, two of the highest-purity, highest-margin lube oil refinery specialty products, as critical raw material inputs. The United States Pharmacopeia (USP) and European Pharmacopoeia (Ph. Eur.) define stringent quality standards for pharmaceutical-grade mineral oils and petrolatums used in laxatives, skin protectants, ointment bases, and tablet coating applications.

The World Health Organization (WHO) reports global pharmaceutical industry output growing at approximately 5-6% annually, with specialty mineral oil demand tracking this growth closely. In personal care, petrolatum remains the FDA-approved skin protectant of choice, maintaining dominant formulation share in moisturizers, lip care, and wound care products globally.

Robust Tire and Rubber Industry Growth Driving Rubber Process Oil Demand

The Rubber Process Oil (RPO) segment is the fastest-growing product type within the lube oil refinery specialties market, directly driven by expanding global tire manufacturing output and the growing rubber goods industry. The International Rubber Study Group (IRSG) projects global natural and synthetic rubber consumption to exceed 30 million metric tons annually by 2026, with RPO constituting a critical processing aid in tire compound formulation, particularly for tread, sidewall, and inner liner components.

REACH regulation compliance for treated distillate aromatic extract (TDAE) and residual aromatic extract (RAE) oils in the European Union has also driven quality upgrading investments among RPO producers, creating premium product opportunities. Asia's tire manufacturing expansion, particularly in China, India, and Southeast Asia, is a primary demand catalyst.

Market Restraints

Feedstock Dependency on Crude Oil Refining Economics and Base Oil Supply Volatility

Lube oil refinery specialties are co-products of the base oil refining process, meaning their production volumes are structurally tied to crude oil throughput economics and base lube refinery operating rates, a dependency that creates supply volatility independent of end-market demand. OPEC+ production decisions and crude oil price fluctuations directly impact on the economics of lube oil refining and, consequently, the availability and cost of specialty by-products including slack wax, petrolatum, and microcrystalline wax. This supply-side volatility creates procurement risk for downstream specialty chemical and consumer goods manufacturers dependent on consistent feedstock pricing.

Environmental Regulatory Pressure on Aromatic-Content Petroleum Products

Tightening environmental and occupational health regulations, particularly the EU's REACH regulation restrictions on polycyclic aromatic hydrocarbons (PAH) in rubber process oils and the U.S. EPA's scrutiny of certain petroleum-derived specialty oils, are increasing compliance costs and product reformulation requirements for lube oil refinery specialty producers.

These regulatory constraints are suppressing growth of traditional high-aromatic process oils in European and North American markets, diverting demand toward costlier low-PAH compliant grades and creating margin compression for producers that have not invested in upgrading refinery processes to produce TDAE and RAE compliant products.

Opportunities

Surging Demand for Food-Grade White Oil and Pharmaceutical Petrolatum in Emerging Markets

The rapid expansion of pharmaceutical manufacturing and packaged food processing in Asia Pacific, Latin America, and Middle East & Africa is creating a significant greenfield opportunity for producers of food-grade white oil and USP-grade petrolatum to expand supply infrastructure in underserved high-growth geographies. Food-grade white oil, used as a release agent, dust suppressant, and equipment lubricant in food processing, must comply with FDA 21 CFR Part 178.3620 and NSF H1 certification standards.

The WHO's Codex Alimentarius Commission's expanding global food safety framework is driving local food manufacturers in emerging markets to source certified-grade food process oils, creating scalable demand for compliant specialty white oil. Producers with established refinery certification infrastructure are best positioned to capture this premium-grade demand growth.

Middle East & Africa: Fastest-Growing Regional Market for Refinery Specialty Investment

The Middle East & Africa region is the fastest-growing market for lube oil refinery specialties, driven by strategic government investment in downstream petroleum processing capacity across Saudi Arabia, UAE, Kuwait, and South Africa. Saudi Aramco's downstream expansion strategy and the Abu Dhabi National Oil Company (ADNOC)'s investment in specialty petrochemical and lube oil refining infrastructure position the region as an emerging export hub for white oil, wax, and petrolatum products.

Africa's rapidly growing personal care and pharmaceutical manufacturing sectors, driven by urbanization and rising middle-class consumer spending, are creating incremental specialty oil demand. Producers investing in Middle East lube oil refining assets will benefit from both favorable crude feedstock access and growing regional end-market demand through 2033.

Category-wise Analysis

Product Type Insights

Fully Refined Wax leads the lube oil refinery specialties market by product type with approximately 36% of global market share in 2026, anchored by its broad industrial utility spanning candle manufacturing, food packaging, cosmetic formulation, polishes, and board sizing applications. Fully refined wax, produced through solvent de-waxing, de-oiling, and hydro finishing of slack wax, meets the stringent purity specifications required by food-contact and pharmaceutical applications under FDA and EU food safety regulations.

Its relatively stable demand profile across packaging, candle, and personal care applications provides producers with diversified revenue resilience. Rubber Process Oil (RPO) is the fastest-growing product type at a 5% CAGR (2026 - 2033), driven by accelerating global tire output and rubber goods manufacturing, particularly across Asia Pacific.

End-user Insights

The Automotive end-user segment leads to demand for lube oil refinery specialties with approximately 32% of global market share in 2026, driven by extensive use of rubber process oils in tire compound formulation, white oil and petrolatum applications in automotive rubber seals, hoses, and underbody coatings, and microcrystalline wax in automotive polishes and protection products.

Global vehicle production, tracked by the International Organization of Motor Vehicle Manufacturers (OICA) at approximately 90 million units annually, creates a vast and stable demand base for RPO, wax, and white oil in tire and automotive rubber component manufacturing. Pharmaceutical is the fastest-growing end-user segment, propelled by global pharmaceutical output growth and expanding generics manufacturing in India and China.

Regional Insights

North America Specialties of Lube Oil Refinery Market Trends and Insights

North America accounted for approximately 22% of global lube oil refinery specialties market share in 2026, underpinned by the region's mature lube oil refining infrastructure and strong demand from pharmaceutical, food processing, and personal care end-user segments. U.S. FDA and NSF H1 certified food- and pharmaceutical-grade white oil and petrolatum production sustains premium product demand. Growing interest in bio-based alternatives is reshaping innovation investment among North American refinery specialty producers.

U.S. Specialties of Lube Oil Refinery Market Size

The United States represents approximately 78-80% of North American lube oil refinery specialties revenue, with major producers including Exxon Mobil Corporation and Chevron Corporation supplying high-specification white oil, wax, and petrolatum. FDA-certified pharmaceutical and food-grade specialty oil demand from the U.S. pharmaceutical and packaged food industries sustains a structurally stable, premium-tier domestic market base through 2033.

Europe Specialties of Lube Oil Refinery Market Trends and Insights

Europe holds approximately 18% of global market share in 2026, shaped by stringent REACH regulation PAH compliance requirements that have compelled producers to invest in TDAE and treated RPO grades. Nynas AB and Repsol SA are key European specialty oil producers, with Germany, Netherlands, and Poland serving as major refining and distribution hubs. Sustainability-driven reformulation in cosmetics and rubber is reshaping specialty oil quality requirements.

Germany Specialties of Lube Oil Refinery Market Size

Germany is Europe's largest lube oil refinery specialties market, contributing approximately 20-22% of regional revenue. Strong demand from Germany's world-class automotive and chemical industries, with over 3 million vehicles produced annually per OICA data, drives substantial RPO and microcrystalline wax consumption. Premium pharmaceutical and cosmetics sectors further reinforce Germany's leadership in high-specification white oil and petrolatum demand.

U.K. Specialties of Lube Oil Refinery Market Size

The United Kingdom accounts for approximately 14-16% of European lube oil refinery specialties market value, with demand supported by established pharmaceutical manufacturing, the Association of the British Pharmaceutical Industry (ABPI) confirms the U.K. as Europe's second-largest pharmaceutical producer, creating stable demand for USP-grade white oil and petrolatum. Nynas AB's Eastham refinery in England is a key regional oil production asset.

France Specialties of Lube Oil Refinery Market Size

France represents approximately 11-13% of the European lube oil refinery specialties market, with demand anchored by strong cosmetics and personal care manufacturing, France is the world's largest cosmetics exporter per Cosmetics Europe data, creating substantial white oil and petrolatum procurement from global brand owners including L'Oréal and LVMH cosmetics supply chains. Total SA's French refinery network supplies regional specialty oil demand.

Asia Pacific Specialties of Lube Oil Refinery Market Trends and Insights

Asia Pacific leads the global lube oil refinery specialties market with approximately 43% of global share in 2026, driven by China's massive tire and rubber manufacturing base, which accounts for over 60% of global tire output, and rapidly expanding pharmaceutical and personal care production across India, South Korea, and Japan. Sinopec Corporation and PetroChina Company Limited dominate regional white oil and wax production, serving a vast domestic industrial consumer base.

India Specialties of Lube Oil Refinery Market Size

India represents approximately 14-16% of Asia Pacific lube oil refinery specialties revenue, with demand driven by India's position as the world's largest generics pharmaceutical manufacturer, requiring significant USP-grade white oil and petrolatum, and a rapidly growing domestic tire industry. Indian Oil Corporation (IOC) and Hindustan Petroleum are key domestic specialty oil producers, with India's specialty wax import dependency creating incremental growth opportunity for global producers.

Japan Specialties of Lube Oil Refinery Market Size

Japan accounts for approximately 10-12% of Asia Pacific lube oil refinery specialties market value, characterized by high-specification demand from Japan's advanced automotive, electronics, and cosmetics industries. Nippon Seiro Co., Ltd. is a leading domestic producer of fully refined and microcrystalline waxes. Japan's automotive OEM sector, producing over 7 million vehicles annually per OICA, sustains substantial RPO and high-purity white oil demand.

Southeast Asia Specialties of Lube Oil Refinery Market Size

Southeast Asia contributes approximately 12-14% of Asia Pacific lube oil refinery specialties revenue and is a fast-growing sub-region, driven by expanding tire manufacturing in Thailand, Indonesia, and Vietnam and growing pharmaceutical and personal care manufacturing investment. Petroliam Nasional Berhad (Petronas) in Malaysia is a key regional specialty petroleum product producer supplying white oil, wax, and petrolatum to Southeast Asian industrial consumers.

Competitive Landscape

The global specialties of lube oil refinery market is moderately consolidated, with integrated oil majors, Exxon Mobil Corporation, Royal Dutch Shell Plc, Total SA, Sinopec Corporation, and Chevron Corporation, controlling the largest share of premium-grade white oil, wax, and petrolatum production capacity globally. Key competitive differentiators include feedstock integration, refinery certification for pharmaceutical and food-grade products (USP, NSF H1), geographic proximity to end-market demand centers, and REACH-compliant RPO product portfolios. Specialty-focused players like Nynas AB and Nippon Seiro Co., Ltd. compete on product quality and technical service differentiation.

Key Developments

- In February 2025, Sinopec Corporation expanded its lube oil refinery specialties portfolio at its Maoming refinery in China, adding capacity for food-grade white oil and fully refined wax to serve rapidly growing domestic pharmaceutical and food packaging demand.

- In September 2024, Nynas AB launched a new range of REACH-compliant treated distillate aromatic extract (TDAE) rubber process oils for European tire manufacturers, meeting tightening PAH emission standards and reinforcing its technical leadership in specialty naphthenic oils.

- In April, 2024, Exxon Mobil Corporation announced capacity upgrades at its Baytown, Texas refinery complex for Spectrasyn and white mineral oil production, targeting growing North American pharmaceutical and food-grade specialty oil demand segments with expanded high-purity output.

Specialties of Lube Oil Refinery Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 27.2 billion |

| Current Market Value (2026) | US$ 33.6 billion |

| Projected Market Value (2033) | US$ 44.8 billion |

| CAGR (2026 - 2033) | 4.2% |

| Leading Region | Asia Pacific, 43% market share (2026) |

| Dominant Product Type | Fully Refined Wax, 36% market share (2026) |

| Top-Ranking End-user | Automotive, 32% market share (2026) |

| Incremental Opportunity | US$ 11.2 billion (Absolute Dollar Opportunity, 2026 - 2033) |

Companies Covered in Specialties of Lube Oil Refinery Market

- Exxon Mobil Corporation

- Sinopec Corporation

- Royal Dutch Shell Plc

- Eni S.P.A.

- Sasol Ltd.

- Total SA

- Petrochina Company Limited

- Chevron Corporation

- Repsol SA

- LUKOIL

- Petroliam Nasional Berhad (Petronas)

- Grupa Lotos SA

- Nippon Seiro Co., Ltd.

- Hollyfrontier Corporation

- Nynas AB

Frequently Asked Questions

The global Specialties of Lube Oil Refinery market is valued at US$ 33.6 billion in 2026. Growing at a CAGR of 4.2%, the market is projected to reach US$ 44.8 billion by 2033, representing an absolute dollar opportunity of US$ 11.2 billion supported by growing pharmaceutical, automotive rubber, food-grade, and cosmetics applications for high-purity petroleum specialty products globally.

The primary demand drivers are growing global pharmaceutical and cosmetics manufacturing requiring USP-grade white oil and petrolatum, endorsed by FDA and Ph. Eur. pharmacopoeia standards, and rapidly expanding global tire production per IRSG data exceeding 30 million metric tons of rubber consumption annually, driving Rubber Process Oil demand as a critical tire compound processing input.

Asia Pacific leads the global Specialties of Lube Oil Refinery market with approximately 43% of global share in 2026, driven by China's global dominance in tire manufacturing (over 60% of global output), India's world-leading pharmaceutical generics production requiring pharmaceutical-grade white oil, and massive regional industrial demand serviced by Sinopec Corporation and PetroChina Company Limited.

The most significant opportunities are in expanding FDA and NSF H1 certified food-grade white oil production to meet growing food processing and pharmaceutical demand in Asia Pacific and Middle East & Africa, and in the Middle East & Africa region itself, where Saudi Aramco and ADNOC's downstream investment programs are building new specialty oil refining capacity for export to global markets.

The leading companies include Exxon Mobil Corporation, Sinopec Corporation, Royal Dutch Shell Plc, Total SA (TotalEnergies), Chevron Corporation, Nynas AB, Nippon Seiro Co., Ltd., Petroliam Nasional Berhad (Petronas), HollyFrontier Corporation, and LUKOIL, among others profiled in this report.