- Food Ingredients & Additives

- Feed Binder Market

Feed Binder Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Feed Binder Market by Ingredient Type (Lignosulfonates, Plant Gums & Starches, Gelatin & Hydrocolloids, Clay, Molasses, Wheat Gluten, Others), by Nature (Natural, Synthetic), by Livestock (Ruminants, Poultry, Equines, Swine, Aquatic Animals, Pets), and by Regional Analysis, 2026 - 2033

Feed Binder Market Share and Trends Analysis

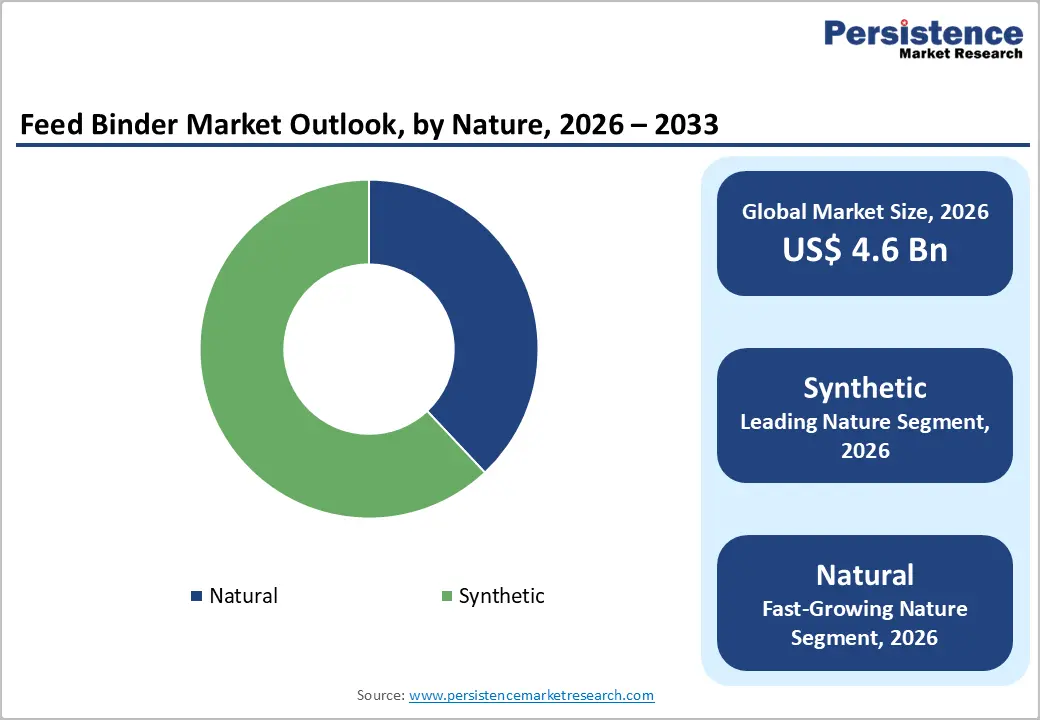

The global feed binder market size is expected to be valued at US$ 4.6 billion in 2026 and projected to reach US$ 6.6 billion by 2033, growing at a CAGR of 5.3% between 2026 and 2033.

The upward trajectory of the market is fundamentally anchored in the surging global consumption of animal-based protein and the consequent industrialization of livestock farming. As commercial producers transition toward precision nutrition, the demand for pelleted feed that ensures high durability and minimal nutrient leaching has become a logistical and nutritional necessity. Furthermore, the expansion of the Aquatic Animals and Pets sectors, which require specialized binders for water stability and palatability, serves as a significant catalyst for technological innovation in binder formulations across both developed and emerging economies.

Key Industry Highlights:

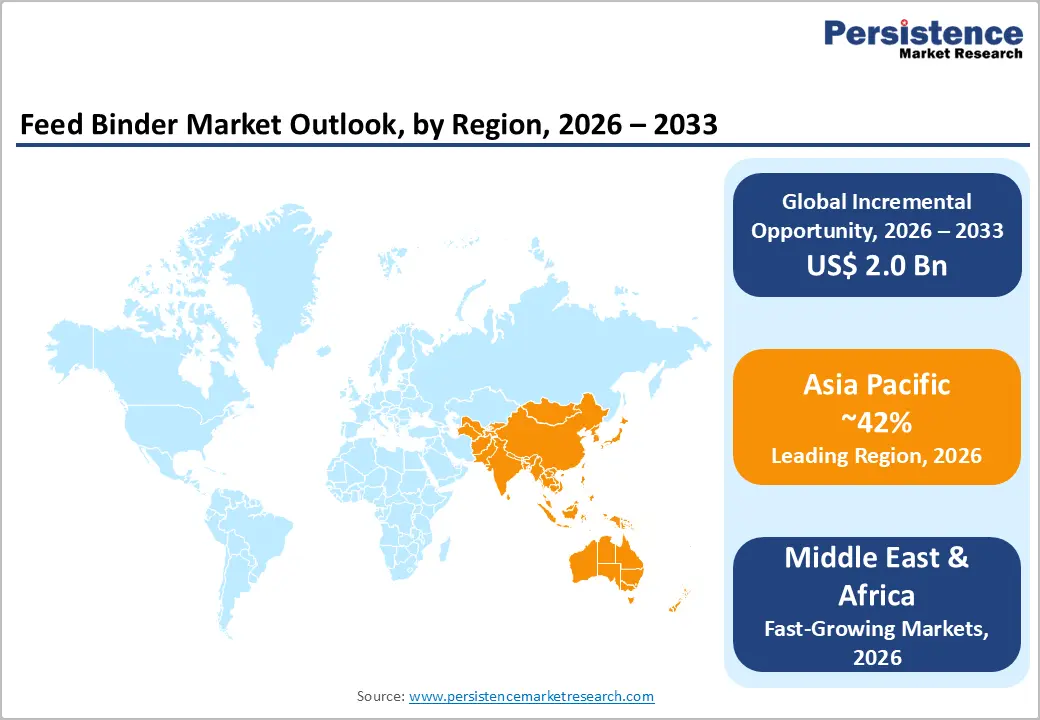

- Leading Region: Asia Pacific, holding 42% market share, supported by large-scale compound feed production, aquaculture dominance, and manufacturing advantages linked to corn and cassava availability across China, India, and ASEAN.

- Fastest-Growing Livestock Segment: Pets, projected to grow at a CAGR of 7.6%, fueled by pet humanization, premiumization of pet food, demand for consistent kibble quality, and rapid scaling of organized pet food manufacturing in emerging markets.

- Market Drivers: Rising shift toward pelleted feed to improve feed conversion efficiency, reduce fines, enhance nutrient uniformity, and support high-throughput industrial feed operations globally.

- Opportunities: Development of specialized binders for premium pet food, aquafeed, and precision nutrition systems, including clean-label, functional, and multi-benefit binder formulations.

- Key Developments: In November 2025, Cargill expanded its Austria micronutrition facility, increasing capacity by 50%. In October 2025, Alltech launched Mycosorb® A+ Evo and Mycosorb® Evo, while DSM-Firmenich partnered with Schothorst Feed Research to advance sustainability in animal nutrition.

| Key Insights | Details |

|---|---|

| Feed Binder Market Size (2026E) | US$ 4.6 Bn |

| Market Value Forecast (2033F) | US$ 6.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.6% |

Market Dynamics

Driver - Rise in Demand for Pelleted Feed and Production Efficiency

The accelerated global shift toward pelleted feed formats to optimize feed conversion ratios (FCR) and minimize environmental waste is a major growth indicator. Pelleting increases the physical density of feed, facilitating easier handling and transportation while preventing the segregation of micro-ingredients. According to the Food and Agriculture Organization (FAO), global compound feed production has surpassed 1.2 billion tonnes annually. Binders are essential to maintain the structural integrity of these pellets, especially under the high-pressure conditions of modern industrial extruders. By reducing the volume of "fines" or dust by up to 15%, binders ensure that livestock receive a consistent nutritional profile in every bite, which directly translates into faster growth cycles and improved operational profitability for large-scale commercial integrators.

Restraints - Stringent Regulatory Frameworks and Quality Compliance Standards

The market is subject to rigorous scrutiny by regulatory bodies such as the U.S. Food and Drug Administration (FDA) and the European Food Safety Authority (EFSA) regarding the safety and purity of feed additives. Any binder used in animal nutrition must comply with strict non-toxicity standards and be free from heavy metals or chemical residues that could potentially enter the human food chain. These compliance requirements necessitate continuous investment in Quality Assurance (QA) and sophisticated testing protocols, which can increase operational overheads. Smaller market participants often struggle to keep pace with the evolving regulatory landscape, creating a high entry barrier and slowing down the commercialization of novel, high-efficiency synthetic binders in highly regulated regions.

Opportunity - Technological Advancements in Specialized Pet Food and Companion Animal Nutrition

The rapid humanization of pets represents a significant high-margin opportunity for the feed binder market. Modern pet owners prioritize the aesthetic and textural qualities of pet food, driving demand for specialized binders that enable unique kibble shapes and "gravy" textures in wet food. The Pets segment is currently the fastest-growing livestock category, driven by rising disposable incomes and urbanization in the Asia-Pacific and Latin America regions. Innovations in hydrocolloid technology allow for the creation of semi-moist treats and functional pet snacks that require precise binding properties. According to the American Pet Products Association (APPA), pet food spending continues to break historical records, offering a stable and recession-resilient revenue stream for binder suppliers who can provide customized formulations for this highly specialized and quality-driven market.

Category-wise Analysis

By Ingredient Type Insights

The Synthetic segment, primarily encompassing binders like urea-formaldehyde and specialized polymers, held the leading position in the Feed Binder Market in 2025, accounting for a dominant 62% market share. This dominance is primarily attributed to the superior binding efficiency and consistency of synthetic agents, which confer greater pellet durability at lower inclusion rates than traditional natural alternatives. This justification is further supported by the cost-effectiveness and heat stability of synthetic binders, which make them the preferred choice for high-volume Poultry and Swine feed production. However, the Natural segment, which includes Plant Gums & Starches and Lignosulfonates, is recognized as the fastest-growing category. This growth is driven by the escalating global demand for antibiotic-free and organic animal products, particularly in the European and North American markets, where regulatory support for sustainable feed additives is most pronounced.

By Livestock Insights

The pet segment is projected to achieve a 7.6% CAGR over the forecast period as companion animals shift from backyard care to nutrition-led wellness. Premium pet foods increasingly demand consistent pellet integrity, uniform nutrient delivery, and improved palatability, elevating the role of advanced feed binders. Rising urbanization, smaller households, and delayed parenthood are reinforcing pet humanization, thereby pushing manufacturers to replicate food-grade standards for texture, stability, and appearance. Functional binders that support digestive comfort, moisture control, and clean-label positioning are gaining preference across dry kibble, treats, and specialty diets.

Growth is further supported by the expansion of veterinary nutrition, the aging pet population, and heightened sensitivity to feed safety incidents. Binders that enable mycotoxin risk management, reduce fines, and provide precise nutrient dispersion help brands protect quality and compliance. Emerging markets in Asia, Latin America, and the Middle East are accelerating adoption as organized pet food manufacturing scales rapidly globally.

Region-wise Insights

North America Feed Binder Market Trends and Insights

North America remains a significant hub for innovation and consumption, driven by the United States' mature livestock sector and a highly sophisticated regulatory environment. The region is a pioneer in the adoption of precision feeding technologies, where feed binders are integrated into specialized formulations for high-performance dairy cattle and poultry. According to the American Feed Industry Association (AFIA), the region has witnessed a significant shift toward the utilization of "high-efficiency" binders to reduce the carbon footprint of meat production by minimizing feed waste.

The innovation ecosystem in the U.S. and Canada is characterized by a strong emphasis on sustainability. Companies in this region are increasingly investing in the development of upcycled binders derived from food-processing side streams. Furthermore, the massive pet food industry in North America acts as a critical engine for the Pets binder segment, where the focus is on grain-free and high-protein formulations that require advanced binding agents to maintain structural stability. The regional market also benefits from a robust retail infrastructure and a high penetration of modern e-commerce channels for specialized feed distribution.

Asia Pacific Feed Binder Market Trends and Insights

Asia-Pacific is the leading regional segment, accounting for 42% of the market in 2025. This leadership is propelled by the massive and rapidly industrializing livestock sectors in China, India, and ASEAN countries. Rapid urbanization and rising disposable incomes have led to a substantial increase in demand for animal protein, necessitating the expansion of high-throughput feed manufacturing facilities. China is currently the world's largest producer of compound feed, and the adoption of pelleted feed is becoming standard practice among small- to medium-scale farmers to improve efficiency.

The region's growth dynamics are further bolstered by its status as a global powerhouse in aquaculture. Vietnam, Thailand, and Indonesia are major exporters of shrimp and fish, creating a huge requirement for water-stable aquafeed binders. According to reports from the Asian Development Bank (ADB), the intensification of farming practices in the region is increasing demand for cost-effective synthetic binders that deliver high performance in tropical climates. Manufacturing advantages, including lower labor costs and proximity to raw material sources such as cassava and Corn, provide the region with a competitive edge, ensuring it remains the primary engine of volume growth for the global Feed Binder Market.

Middle East & Africa Feed Binder Market Trends

Middle East & Africa feed binder market Market is expected to grow at a CAGR of 7.8% as feed manufacturers prioritize pellet durability, nutrient retention, and cost efficiency amid volatile raw material supplies. In Egypt, rising poultry and dairy production is driving demand for molasses- and lignosulfonate-based binders that support local feed formulations. GCC countries are accelerating the adoption of high-performance synthetic binders to improve feed stability under hot climates and long storage cycles.

Across African countries, the expansion of commercial aquaculture and organized livestock farming is reshaping patterns of binder use. Clay-based binders are gaining traction for toxin management, while plant-derived binders align with clean-feed and sustainability narratives. Investments in modern feed mills across Nigeria, Kenya, and South Africa are further encouraging consistent inclusion of binders to reduce fines, improve feed conversion efficiency, and support export-oriented animal protein value chains.

Market Competitive Landscape

The global feed binder market is characterized by a moderate degree of consolidation, with a handful of global agricultural and chemical conglomerates, such as Cargill, Incorporated, ADM, and BASF SE, commanding significant market power through their extensive distribution networks and vertically integrated supply chains. These market leaders maintain their dominance by employing aggressive strategies for expansion, including strategic acquisitions of niche technology firms and significant investments in R&D for "next-generation" bio-binders.

Key differentiators employed by these leaders include the ability to provide comprehensive technical support for custom feed formulations and to maintain global sustainability certifications. Emerging business model trends indicate a shift toward "Precision Additive" systems, in which binders are paired with enzymes or probiotics to create synergistic health effects. The market remains fragmented at the regional level, where numerous local players compete on price and localized sourcing advantages, particularly in the Clay and Molasses segments.

Key Developments:

- In November 2025, Cargill Animal Nutrition & Health completed a major expansion at its Engerwitzdorf, Austria facility, boosting micronutrition production capacity by 50% to address rising customer demand.

- In October 2025, Alltech launched Mycosorb® A+ Evo and Mycosorb® Evo, introducing the next generation of its Mycosorb® mycotoxin management solutions to enhance feed safety and animal performance.

- In October 2025, DSM-Firmenich Animal Nutrition & Health and Schothorst Feed Research announced a strategic partnership focused on advancing sustainability across animal nutrition and feed production systems.

Companies Covered in Feed Binder Market

- Cargill, Incorporated

- ADM

- Borregaard AS

- GELITA AG

- Darling Ingredients Inc.

- Roquette Frères

- BASF SE

- DSM-Firmenich

- Tate & Lyle

- Kemin Industries, Inc.

- Alltech Inc.

- Others

Frequently Asked Questions

The global feed binder market is expected to be valued at approximately US$ 4.6 billion in 2026, growing steadily from its 2020 base of US$ 3.5 billion.

The primary driver is the global shift toward pelleted feed formats to improve feed conversion ratios and reduce environmental waste in industrial livestock and aquaculture farming.

Asia Pacific is the leading region, holding a 42% market share in 2025, primarily due to the large-scale livestock sectors in China and India.

A significant opportunity lies in the Natural binder segment and the Pets livestock category, where owners are increasingly seeking clean-label and premium quality nutritional products.

The market is led by global giants including Cargill, Incorporated, ADM, Borregaard AS, GELITA AG, BASF SE, and DSM-Firmenich.