- Telecommunications

- Europe Managed Learning Services Market

Europe Managed Learning Services Market Size, Share, and Growth Forecast, 2026 - 2033

Europe Managed Learning Services Market by Service Type (Managed Training Delivery, Learning Technology Management, Content Development & Customization, Analytics & Reporting, Consulting & Strategy, Support & Helpdesk, Misc.), Organization Size (Small & Medium Enterprises (SMEs), Large Enterprises), Delivery Mode (On Premise, Hybrid, Cloud), End User (IT & Telecom, BFSI (Banking, Financial Services & Insurance), Healthcare & Life Sciences, Manufacturing & Industrial, Retail & eCommerce, Government & Public Sector, Education & Academia, Misc.) and Regional Analysis for 2026 - 2033

Europe Managed Learning Services Market and Trends Analysis

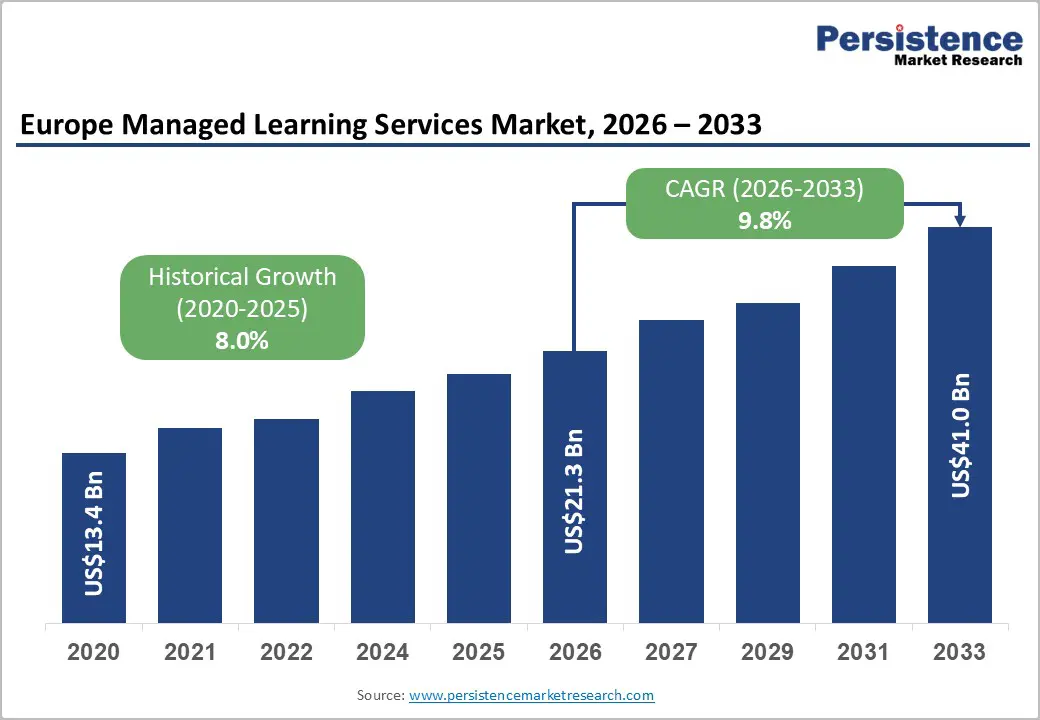

The Europe Managed Learning Services Market size was valued at US$ 21.3 billion in 2026 and is projected to reach US$ 41.0 billion by 2033, growing at a CAGR of 9.8% between 2026 and 2033. The market demonstrated strong historical performance with a CAGR of 8.0% from 2020 through 2026, establishing a foundation for accelerated expansion. This trajectory reflects the strategic imperative for enterprises to optimise learning and development investments through specialised external partnerships.

Organisations across Europe are progressively adopting managed models to address workforce skill transformation, regulatory compliance requirements, and digital capability development while achieving operational efficiency and scalability in their corporate learning infrastructure.

Key Industry Highlights:

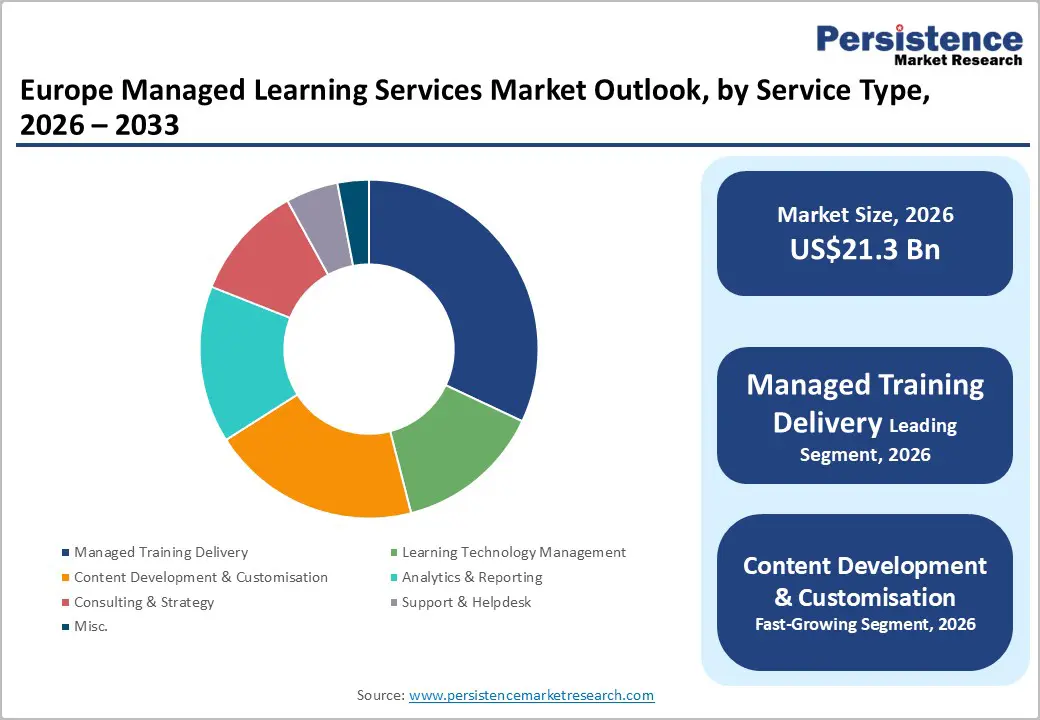

- Leading Service Segment: Managed Training Delivery commands 32.4% share, reflecting strong demand for instructor-led training, virtual classrooms, learner engagement, and scalable corporate learning infrastructure.

- Fastest-Growing Service Segment: Content Development & Customisation expands rapidly, fueled by accelerated skill transformation, evolving technologies, and multilingual, adaptive content needs.

- Dominant Delivery Mode: Cloud-based learning holds 54.4% share, offering accessibility, scalability, and operational efficiency for distributed European workforces with high internet and mobile penetration.

- Fastest-Growing Delivery Mode: Hybrid delivery integrates digital platforms with in-person training to optimise learning effectiveness and meet diverse organisational and learner preferences.

- Market Drivers: Digital transformation, AI-enabled personalisation, analytics integration, and leadership development programs are accelerating managed learning adoption across Europe.

| Key Insights | Details |

|---|---|

| Managed Learning Services Market (2026E) | US$ 21.3 Bn |

| Market Value Forecast (2033F) | US$ 41.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.0% |

Market Dynamics

Growth Drivers

Digital Transformation and Technology Integration in Enterprise Learning Infrastructure

Europe's information and communication services sector represents a substantial economic pillar, with approximately 1.4 million enterprises generating €667 billion in value added and employing 7.2 million people in 2022, according to Eurostat. Computer programming, consultancy, and related activities contributed to sectoral employment, demonstrating the centrality of technology-driven services across the European business economy. This technological advancement directly influences the European Managed Learning Services Market, as organisations require sophisticated learning solutions to maintain a competitive advantage in rapidly evolving digital environments.

The sector's apparent labour productivity reached €92,800 per person employed, significantly exceeding EU business economy averages, which necessitates continuous workforce capability enhancement through managed learning partnerships. Organisations are implementing cloud-based learning platforms, artificial intelligence-enabled personalisation, and data analytics to optimise training effectiveness and measure business impact. The proliferation of digital technologies across industries creates demand for specialised learning content, adaptive delivery mechanisms, and technology management services that managed learning providers are uniquely positioned to deliver at scale.

Structural Workforce Transformation and Skills Gap Mitigation in Manufacturing and Industrial Sectors

Germany, France, Italy, Spain, and Poland collectively accounted for over 75% of financial sector value added and around 67 per cent of employment in the European Union, highlighting the concentration of economic activity in major markets where manufacturing and industrial operations remain significant employers. NIIT Learning Systems Limited's July 2025 acquisition of Germany-based MST Group specifically targeted automotive and industrial sector clients in the DACH region, recognising the critical demand for managed learning solutions in these industries. Manufacturing enterprises face substantial skill transformation requirements as they integrate advanced automation, Industry 4.0 technologies, and sustainable production methodologies into operations.

The Europe Managed Learning Services Market addresses these challenges by providing customised training programs, technical competency development, and change management support that enable industrial organisations to upskill existing workforces while onboarding new talent efficiently. Managed learning partnerships deliver specialised content in multilingual formats, support nearshore delivery capabilities, and provide scalable training infrastructure that adapts to production cycles and operational requirements across diverse European manufacturing landscapes.

Market Restraining Factors

Budget Constraints and Internal Learning Function Prioritisation

European organisations face competing investment priorities as they balance learning and development expenditure against technology infrastructure modernisation, operational efficiency initiatives, and direct business growth activities. The structural transformation in the banking sector, which reduced credit institutions by 2.9 percent to 5,304 entities and decreased branch networks to approximately 129,400 locations, reflects broader efficiency-driven restructuring that constrains discretionary spending across corporate functions.

Learning and development budgets often face pressure during economic uncertainty or margin compression, limiting the scope and scale of managed learning engagements. Organisations may prioritise internal capability development over external partnerships, particularly when they maintain established learning functions or question the return on investment from outsourced models. These budget dynamics create pricing pressure on managed learning providers and necessitate clear value demonstration through measurable business outcomes, operational cost savings, and strategic capability enhancement.

Key Market Opportunities

Strategic Learning Outsourcing and Operational Model Evolution in European Enterprises

Hemsley Fraser's February 2024 research revealed that European organisations are progressively outsourcing learning and development functions, seeking greater flexibility, scalability, and strategic contribution from external providers.

The study highlighted that managed learning services are evolving beyond basic training delivery to influence corporate learning strategies, program design, content access, and learning technology implementation, reflecting a fundamental shift toward integrated, globally aligned solutions. This evolution creates substantial opportunity for the Europe Managed Learning Services Market, as organizations recognize that specialised providers deliver superior capabilities in content development, technology management, analytics sophistication, and delivery innovation compared to internal functions.

The transition from transactional training procurement to strategic learning partnerships enables managed service providers to embed themselves deeply within client organizations, aligning learning initiatives directly with business objectives, performance metrics, and workforce transformation goals. Organizations operating across multiple European markets particularly value providers' ability to deliver consistent learning experiences while adapting content and delivery methods to local language requirements, cultural contexts, and regulatory frameworks.

The establishment of regional delivery capabilities, exemplified by DelphianLogic's August 2022 launch of DelphianLogic AG in Basel, Switzerland, demonstrates provider commitment to proximity, responsiveness, and market-specific expertise that strengthens client relationships and supports geographic expansion.

Leadership Development and Behavioural Change Programs Supporting Organisational Transformation

Franklin Covey's recognition as a Training Industry 2025 Top 20 Leadership Training Company for the 15th consecutive time reflects sustained demand for principle-based frameworks, behavioural change methodologies, and leadership skill development that support organisational effectiveness and strategic execution.

The Europe Managed Learning Services Market benefits from the recognition that leadership capability, team effectiveness, and cultural transformation cannot be achieved through conventional training approaches alone but require sustained development programs, coaching integration, and application support that managed learning providers deliver through comprehensive engagement models. Organisations facing digital transformation, merger integration, geographic expansion, or business model evolution rely on managed learning partners to design and implement leadership development curricula that cascade from senior executives through middle management to frontline supervisors.

These programs incorporate artificial intelligence-enabled personalisation, flexible delivery models, experiential learning methodologies, and performance reinforcement mechanisms that drive lasting behavioural change and business impact. The complexity of leadership development, spanning competency assessment, individualised learning pathways, peer learning facilitation, executive coaching, and impact measurement, aligns naturally with managed service models that provide dedicated program management, specialised content expertise, and delivery scalability.

As organizations prioritize cultural transformation, employee engagement, and leadership pipeline development in response to competitive pressures and workforce expectations, demand for sophisticated leadership development programs delivered through managed learning partnerships will continue to strengthen across European markets.

Category-wise Analysis

Service Type Insights

Managed Training Delivery commands the largest service type segment with 32.4% market share in 2026, reflecting the fundamental role of training execution, facilitation, and learner support in corporate learning programs. This segment encompasses instructor-led training delivery, virtual classroom facilitation, learning pathway administration, and learner engagement management that organizations outsource to specialized providers. The financial and insurance sector's employment of nearly 5 million people across 867,000 enterprises creates substantial demand for scalable training delivery infrastructure that can accommodate diverse learning formats, multiple languages, and geographically dispersed workforces.

Organizations value managed training delivery for its operational efficiency, delivery consistency, facilitator quality, and administrative burden reduction compared to internally managed training operations. The segment's leadership position is reinforced by the ongoing need for instructor-led development in technical skills, regulatory compliance, leadership capabilities, and product knowledge areas, where facilitated learning demonstrates superior effectiveness over self-paced digital alternatives.

Content Development & Customization emerges as the fastest-growing service type segment, driven by the accelerated pace of business change, technology evolution, and skill transformation requirements that render existing learning content obsolete or insufficient.

Delivery Mode Insights

Cloud-Based delivery mode holds a dominant market position with 54.4 percent share in 2026, reflecting the fundamental shift toward software-as-a-service learning platforms, cloud-hosted content repositories, and internet-delivered training experiences. Eurostat data showing 94 percent of EU individuals used the internet within the last three months in 2025, with mobile devices used by nearly nine out of ten individuals, demonstrates the technological foundation supporting cloud-based learning adoption.

Organisations value cloud delivery for its accessibility, scalability, cost efficiency, and rapid deployment capabilities compared to on-premise learning management systems requiring substantial capital investment and internal technical expertise. Cloud platforms enable anytime, anywhere access to learning content, supporting distributed workforces, remote employees, and flexible work arrangements that have become standard across European organisations.

The banking sector's digital transformation, evidenced by branch network reductions to approximately 129,400 locations while maintaining 2 million employees, illustrates the shift toward digital service delivery models that extend naturally to learning and development infrastructure. Cloud-based solutions provide managed learning providers with centralised content management, unified learner data, real-time analytics, and streamlined administration across multi-country client organisations, delivering operational efficiency and service consistency advantages.

Hybrid delivery mode represents the fastest-growing segment, combining cloud-based learning platforms with on-premise systems, blending virtual and in-person training experiences, and integrating digital content with classroom facilitation to optimise learning effectiveness while accommodating organisational constraints and learner preferences.

Competitive Landscape

The Europe Managed Learning Services market is moderately consolidated, led by major players such as BTS Group AB, FranklinCovey, Hemsley Fraser, GP Strategies, and DDI. These companies dominate through expertise in leadership development, strategy execution, and digital learning solutions, serving large enterprises across the region. Alongside them, smaller regional providers offer specialised or localised services, adding a fragmented dimension in certain countries.

The market is highly competitive, with innovation in AI-driven platforms, virtual classrooms, and performance analytics becoming key differentiators. Strategic partnerships, acquisitions, and alliances are common as firms seek to expand reach and enhance offerings.

Key Industry Developments

- May 27, 2025 – FranklinCovey, a global leader in leadership development, was named among the Top 20 Leadership Training Companies for the 15th time, reflecting its continued impact on corporate learning and development. The company’s principle-based frameworks, AI-enabled learning solutions, and flexible delivery models support lasting behavioural change, leadership skill development, and team effectiveness, enhancing strategic L&D capabilities for organisations across Europe and worldwide.

- February 29, 2024 – Hemsley Fraser’s study on managed learning revealed that European organizations are increasingly outsourcing L&D functions, seeking greater flexibility, scalability, and strategic contribution from providers. The research highlighted that managed learning services are evolving beyond basic training delivery to influence corporate learning strategies, programme design, content access, and L&D technology implementation, reflecting a shift toward more integrated and globally aligned learning solutions.

Companies Covered in Europe Managed Learning Services Market

- TÜV Rheinland

- BTS Europe

- DDI UK

- Hemsley Fraser

- FranklinCovey U.K.

- 2logical

- KnowledgePool

- The Cegos Group

- Wilson Learning

- Center for Creative Leadership

- EY Lane4

- GP Strategies Corporation

- The Ken Blanchard Companies

- Linkage, Inc.

Frequently Asked Questions

The Europe Managed Learning Services Market is projected to be valued at US$ 21.3 Bn in 2026.

The Managed Training Delivery segment is expected to account for approximately 32.4% of the Europe Managed Learning Services Market by Service Type in 2026.

The Europe market is expected to witness a CAGR of 9.8% from 2026 to 2033.

The Europe Managed Learning Services Market growth is driven by digital transformation, AI-enabled learning, cloud adoption, skills gap mitigation, and workforce upskilling in Europe.

The key market opportunities in the Europe Managed Learning Services Market are strategic learning outsourcing, evolving operational models, regional delivery expansions, and demand for leadership development and behavioural change programs that drive workforce transformation, digital adoption, and organizational effectiveness.

Key players in the Europe Managed Learning Services include BTS Group AB, FranklinCovey, Hemsley Fraser, GP Strategies, and DDI.