- Smart Packaging

- Europe Cement Packaging Market

Europe Cement Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Europe Cement Packaging Market by Material (Paper & Paperboard, Plastic, Others), Packaging Format (Bags & Sacks, Valve Bags & Sacks, Others), Capacity, and Country Analysis for 2026 - 2033

Europe Cement Packaging Market Size and Trends Analysis

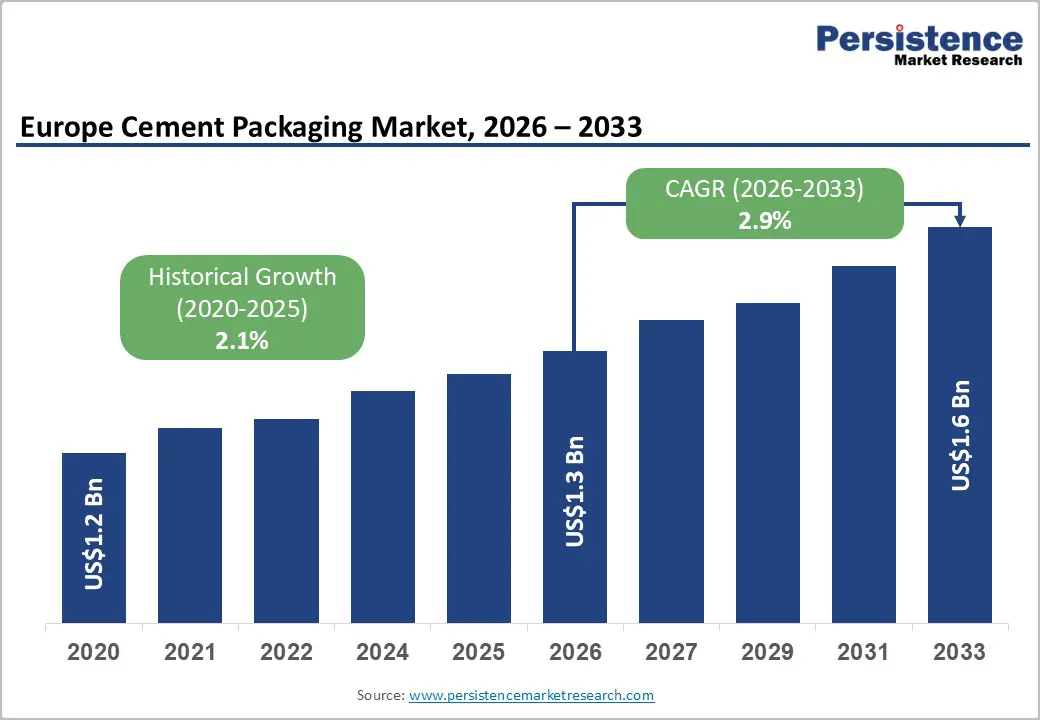

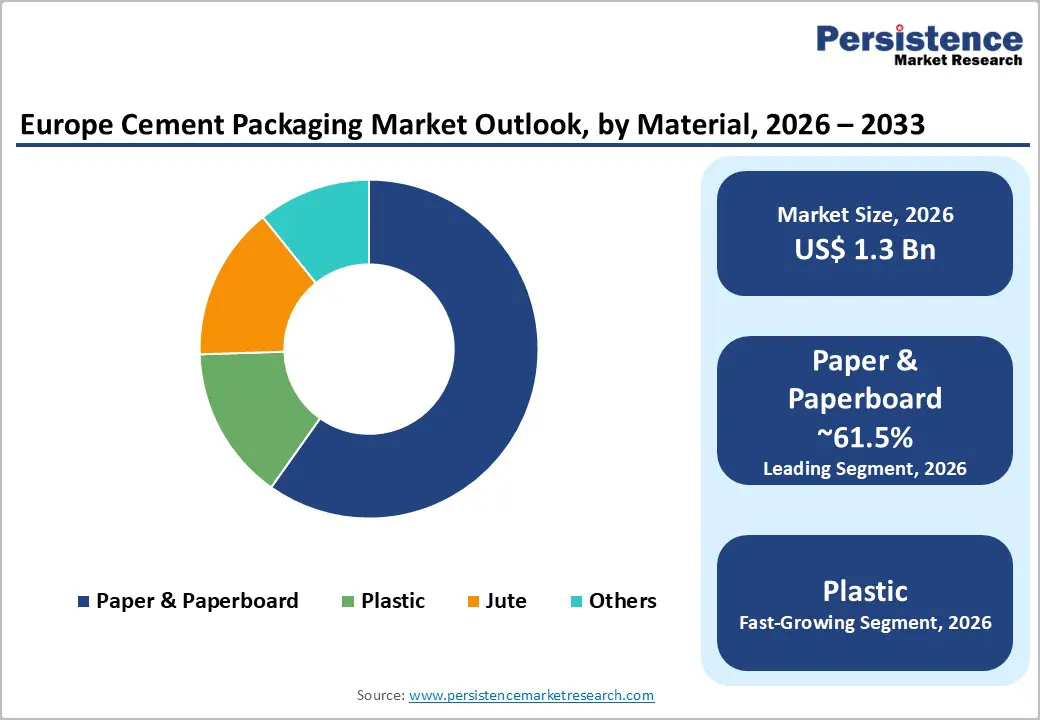

The Europe cement packaging market size is likely to be valued at US$1.3 billion in 2026 and is expected to reach US$1.6 billion by 2033, growing at a CAGR of 2.9% during the forecast period from 2026 to 2033, driven by sustained construction activity and infrastructure modernization across Western and Eastern Europe.

Rising investments in residential, commercial, and infrastructure projects are driving cement consumption, boosting demand for durable, moisture-resistant packaging. The market includes paper sacks, PP woven bags, and bulk formats that protect product integrity during storage and transport. EU sustainability regulations are accelerating the shift toward recyclable and biodegradable materials. Innovations in valve sacks, high-strength kraft paper, and automated filling systems are improving efficiency, while efforts to reduce material waste and optimize supply chains are reshaping competitive strategies across the region.

Key Industry Highlights:

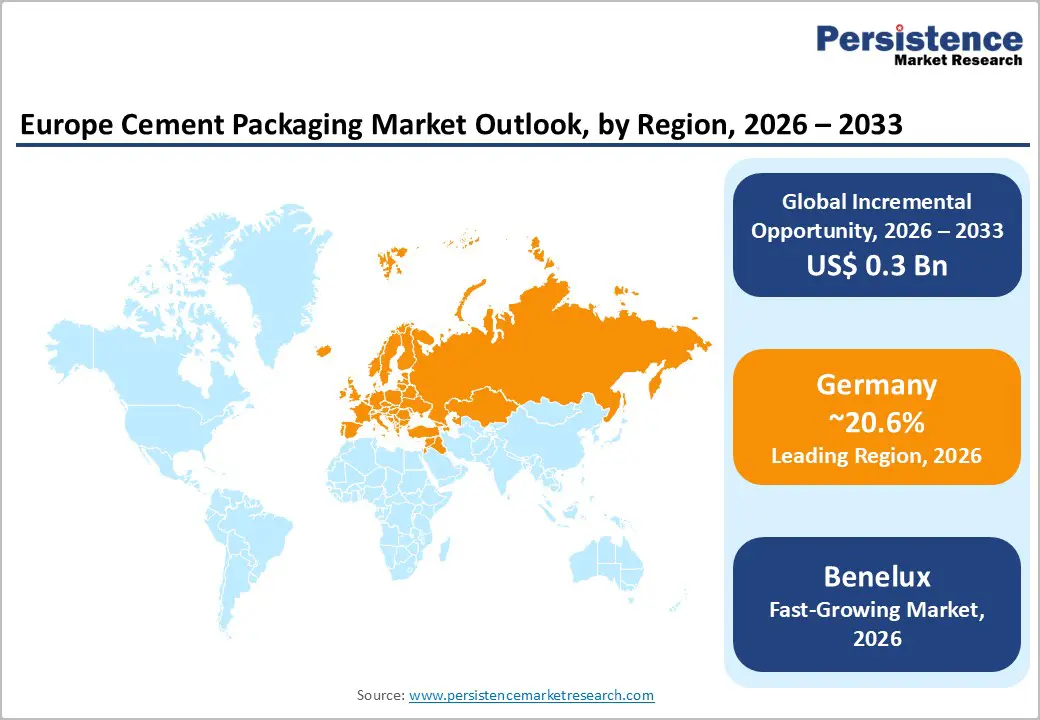

- Leading Region: Germany is projected to lead the market with approximately 20.6% share, supported by its strong cement production base, automated high-speed bagging infrastructure, and sustained infrastructure renovation projects.

- Fastest-growing Region: Benelux (Belgium, Netherlands, and Luxembourg) is the fastest-growing region, driven by port-led cement trade, export redistribution hubs, and increasing adoption of moisture-resistant valve sack systems.

- Investment Plans: Packaging manufacturers are investing in lightweight multiwall kraft paper sack technology, recyclable mono-material PP woven bags, and automated valve-bag compatible production lines, aligning with circular economy goals and operational efficiency improvements.

- Dominant Material: The paper & paperboard segment is anticipated to lead with approximately 61.5% market share, owing to its recyclability, high burst strength, and compatibility with Europe’s advanced cement filling systems.

- Leading Packaging Format: Bags & sacks are estimated to dominate with nearly 77.3% share, supported by standardized 25-50 kg formats, seamless integration with rotary filling lines, and strong pallet stability across regional distribution networks.

| Key Insights | Details |

|---|---|

| Europe Cement Packaging Market Size (2026E) | US$1.3 Bn |

| Market Value Forecast (2033F) | US$1.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 2.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 2.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Infrastructure Modernization and Performance-Optimized Sack Demand

Accelerated infrastructure modernization programs and energy-efficient housing construction across Germany, France, Italy, and the Nordics are directly strengthening demand for high-performance cement packaging solutions. Large public works projects require consistent bulk cement movement, increasing the need for moisture-resistant valve sacks for cement, high-strength kraft paper cement bags, and high-capacity FIBC bulk bags for construction materials. Contractors and ready-mix suppliers prioritize packaging that minimizes spillage during pneumatic filling and ensures durability under palletized transport conditions. The growing preference for automated cement bag filling systems and compatible packaging further supports this trend. For example, several European cement plants have upgraded to multi-layer valve sacks designed to reduce product loss during high-speed filling operations, improving both throughput efficiency and cost control.

Regulatory-driven Sustainable and Circular Packaging Transition

Stringent EU circular economy targets and packaging waste regulations are accelerating the shift toward recyclable cement paper sacks, low-carbon footprint packaging for building materials, and plastic-reduced hybrid cement bags. Cement producers are increasingly adopting multi-ply kraft paper solutions with biodegradable barrier coatings to comply with environmental compliance frameworks while maintaining strength and moisture protection. Demand is also rising for fully recyclable construction material packaging formats that align with retailer and distributor sustainability commitments. A notable example includes the introduction of 100% recyclable kraft paper cement sacks by European packaging manufacturers, enabling cement brands to reduce plastic content while maintaining mechanical resistance standards required for heavy building materials.

Barrier Analysis - Performance Limitations in Lightweight and Sustainable Sack Designs

Balancing sustainability objectives with the technical demands of cement distribution presents structural challenges for packaging manufacturers. Cement requires high-burst-strength multiwall paper cement bags, enhanced moisture-barrier valve sacks for bulk cement transport, and tear-resistant palletized construction material packaging to withstand humidity exposure and mechanical stress. Lightweight and plastic-reduced formats, while environmentally attractive, often face performance constraints in high-humidity storage environments or during long-distance cross-border logistics. Failure rates linked to seam rupture, valve leakage, or micro-perforation under pressure can result in product loss and operational disruption. These performance sensitivities slow the large-scale transition toward ultra-light or mono-material packaging formats in heavy-duty construction supply chains.

Operational Disruptions in Cement Distribution and Filling Infrastructure

The efficiency of the Europe cement packaging ecosystem is closely tied to compatibility with high-speed rotary cement bag filling lines, automated pallet stabilization systems for building materials, and pneumatic bulk cement handling infrastructure. Any misalignment between packaging specifications and plant machinery can lead to filling inefficiencies, dust leakage, and reduced line throughput. Packaging formats that require recalibration of filling equipment or adjustments in sealing mechanisms may face slower adoption among cement producers operating legacy infrastructure. Inconsistent bag dimensions, valve positioning tolerances, and material stiffness can also disrupt automated stacking operations, increasing breakage rates during warehousing and transit. Such operational frictions create practical limitations in scaling new packaging innovations across established European cement production networks.

Opportunity Analysis - Integration of Smart and Value-Added Cement Packaging Solutions

Digitalization within the European construction supply chain is opening space for QR-enabled cement bag traceability systems, RFID-integrated bulk cement packaging for inventory control, and anti-counterfeit printed cement sacks for branded distribution networks. As cross-border cement trade increases within the EU, manufacturers are seeking packaging that supports real-time tracking, batch identification, and automated warehouse scanning. Smart labeling integrated into high-strength valve sack packaging for bulk cement can improve stock visibility and reduce pilferage in distributor networks. This creates an opportunity for packaging converters to move beyond basic containment toward value-added service models. For example, select European packaging suppliers have begun offering digitally printed cement sacks with serialized codes, enabling manufacturers to strengthen brand authentication and streamline supply chain verification.

Growth of Low-Carbon and Performance-Optimized Industrial Packaging

Europe’s shift toward low-carbon construction materials is generating demand for plastic-reduced multiwall paper cement bags, mono-material recyclable cement packaging solutions, and lightweight high-burst-strength kraft sacks for palletized transport. Cement producers focusing on sustainable product portfolios are aligning packaging choices with their environmental positioning, creating scope for next-generation fiber-based sack technologies. Innovations in micro-creped extensible paper and reinforced seam engineering allow weight reduction without compromising mechanical strength, supporting logistics efficiency. Suppliers that can deliver carbon-footprint-optimized cement packaging formats compatible with automated filling lines are well positioned to secure long-term supply contracts as European construction firms increasingly prioritize lifecycle emissions performance across material categories.

Category-wise Analysis

Material Insights

The paper and paperboard segment is anticipated to account for approximately 61.5% of the market in 2026, making it the dominant material category. Their leadership position stems from a strong balance between mechanical performance, cost efficiency, and environmental compatibility. Multiwall kraft paper sacks offer high burst strength, tear resistance, and stacking stability, which are critical for handling dense cement loads across long-distance road and rail networks. These sacks are also fully compatible with high-speed automated rotary filling lines widely used in European cement plants, ensuring operational continuity without major equipment adjustments.

The established paper recycling infrastructure across Europe further strengthens adoption, as cement producers increasingly align packaging decisions with circular economy targets. Barrier-coated kraft paper solutions provide adequate moisture resistance for most inland distribution environments, reducing reliance on heavier plastic laminates. For example, several European cement manufacturers have adopted reinforced multi-ply kraft paper sacks with optimized seam technology to reduce bag rupture rates during palletized transport, improving supply chain reliability while maintaining sustainability objectives.

Plastic-based cement packaging is likely to emerge as the fastest-growing material segment, driven primarily by lightweight engineering and superior moisture protection capabilities. Polypropylene (PP) woven sacks and polyethylene (PE) laminated bags offer enhanced resistance to humidity, making them particularly suitable for coastal regions, export shipments, and high-moisture storage environments.

Advances in mono-material recyclable PP structures and thin-gauge high-strength films are enabling weight reduction without compromising tensile strength. These innovations directly support logistics optimization by lowering overall packaging weight, improving handling efficiency, and reducing transportation-related emissions per ton of cement shipped. Plastic formats are also gaining traction in specialty cement grades that require extended shelf life and contamination resistance. For instance, high-tenacity PP woven cement sacks with integrated moisture-barrier liners are increasingly specified for cross-border bulk distribution, where climatic variability and extended transit times demand higher protective performance standards. Jute and composite materials remain niche segments within the European market, primarily serving localized or specialty applications where differentiation or specific handling characteristics are required.

Packaging Format Insights

Bags and sacks are estimated to represent nearly 77.3% of the market in 2026, reflecting their central role in standardized cement distribution. Their dominance is closely linked to operational efficiency, compatibility with automated filling infrastructure, and suitability for common weight formats such as 25 kg and 50 kg units. Multiwall sacks integrate seamlessly with palletizing robots and warehouse stacking systems, enabling high throughput across cement plants and distribution hubs. Their structural integrity under compression and vibration ensures product stability during long-haul transportation.

Standardized bag dimensions also facilitate efficient container loading and retail distribution, particularly for small-to-medium construction contractors. A relevant example includes European cement producers adopting reinforced seam multiwall sacks to minimize breakage during mechanical handling, which has led to measurable reductions in product loss and improved customer satisfaction.

Valve bags and sacks are likely to record the fastest growth within packaging formats due to their operational and environmental performance advantages. These bags are designed for high-speed filling through integrated valves that automatically seal after discharge, significantly reducing dust emissions during packaging. This feature supports cleaner plant environments and improves compliance with workplace air-quality standards. Their compatibility with advanced rotary filling systems enhances production efficiency by reducing filling time and minimizing spillage.

Improved valve design and layered barrier integration also enhance moisture resistance and fill accuracy. For example, several European ready-mix suppliers have transitioned to advanced valve sack systems to increase bagging speed while lowering airborne cement dust at filling stations, strengthening both productivity metrics and occupational safety performance. Flexible Intermediate Bulk Containers (FIBCs) and rigid containers serve specialized industrial applications and bulk export requirements but remain secondary to traditional bag formats in overall market share due to their targeted use cases.

Country Analysis

Germany

Germany is projected to lead the Europe cement packaging market with an estimated 20.6% market share during the forecast period, supported by its strong domestic construction output and large-scale cement manufacturing base. The country hosts some of Europe’s most advanced cement production facilities, which rely heavily on automated high-speed bagging lines and performance-optimized valve sack systems. Ongoing investments in residential renovation, transport infrastructure upgrades, and energy-efficient building retrofits continue to sustain cement consumption. Germany’s well-established logistics network and centralized distribution hubs further strengthen demand for durable multiwall paper sacks and moisture-resistant packaging formats capable of supporting both domestic supply and cross-border trade within the EU.

Benelux (Belgium, Netherlands, and Luxembourg)

The Benelux region is projected to be the fastest-growing market. Growth is supported by intensive urban redevelopment programs, port-led trade activity, and strong re-export dynamics through logistics centers in Belgium and the Netherlands. Major port infrastructure in Rotterdam and Antwerp facilitates bulk cement imports and redistribution across Europe, increasing demand for high-performance plastic-lined sacks and bulk packaging solutions. Rising investments in sustainable construction and circular building materials across the region are also encouraging adoption of recyclable and lightweight cement packaging formats tailored for export-oriented supply chains.

Competitive Landscape

The Europe cement packaging market is moderately consolidated, characterized by a mix of large multinational paper and flexible packaging producers alongside specialized regional converters. Market leaders differentiate through scale, broad product portfolios, and deep integration with cement manufacturers’ filling and logistics operations. Key players have invested in high-performance multiwall paper sacks, moisture-resistant valve sacks, and lightweight polypropylene woven formats that meet both operational demands and evolving sustainability criteria. Strategic partnerships with major cement producers and long-term supply contracts help secure stable demand, while investments in automated production lines and digital printing capabilities support responsiveness to bespoke packaging specifications.

Emerging competitors are focusing on niche innovation areas such as recyclable mono-material solutions, smart labeling integration (e.g., QR and RFID for traceability), and customized bulk packaging formats for export and industrial segments. These players often compete on agility, technical service, and the ability to quickly adapt to shifting regional requirements, such as enhanced barrier properties for high-humidity markets or tailored sack dimensions for specialized cement blends. Competitive dynamics are further shaped by sustainability commitments that push firms to develop low-impact, resource-efficient packaging, giving first movers in recyclable and low-plastic variants a potential advantage in securing environmentally driven procurement programs across European cement producers.

Key Industry Developments

- In July 2025, UltraTech Cement received recognition for using cement bags made from 50% recycled polypropylene, achieving a notable reduction in virgin plastic usage at the FIPSA 2025 event, demonstrating cross-industry recognition of more sustainable industrial packaging practices.

- In June, 2025, Klabin showcased its Ekomix dispersible paper cement bags and Ekolayer plastic-free barrier technology at ExpoCimento, highlighting 100% dispersible paper packaging innovations that integrate renewable and recyclable materials into the cement packaging segment.

Companies Covered in Europe Cement Packaging Market

- Mondi Group

- Smurfit Kappa Group

- Billerud AB

- LC Packaging

- NNZ Group

- Coveris

- ProAmpac

- Bischof + Klein

- Koehler Group

- United Bags

- El Dorado Packaging

- Global-Pak

- WestRock

- DS Smith

- Segezha Group

- UFlex Limited

- Alfa Plastics

- Fischer Packaging

Frequently Asked Questions

The Europe cement packaging market size is estimated at US$1.3 billion in 2026.

The Europe cement packaging market is projected to reach US$1.6 billion by 2033.

Key trends include rising adoption of plastic-reduced multiwall paper sacks, increasing demand for high-speed valve bag compatible packaging, integration of dust-minimizing valve sack systems, and growing preference for recyclable mono-material cement packaging formats aligned with circular economy objectives.

By material, paper & paperboard leads the market with approximately 61.5% share, driven by strong mechanical strength, recyclability, and compatibility with automated filling lines.

By packaging format, bags & sacks dominate with nearly 77.3% share, supported by standardized weight formats and widespread adoption across cement distribution networks.

The Europe cement packaging market is expected to grow at a CAGR of 2.9% between 2026 and 2033.

Major companies with strong product portfolios and regional presence include Mondi Group, Smurfit Kappa Group, Billerud AB, LC Packaging, and NNZ Group.