- Display Technologies

- Embedded Displays Market

Embedded Displays Market Size, Share, and Growth Forecast, 2026 – 2033

Embedded Displays Market by Product Type (Touch Displays, Non-Touch Displays), Technology (LCD (Liquid Crystal Display), LED (Light Emitting Diode), OLED (Organic Light Emitting Diode)), and Regional Analysis for 2026 – 2033

Embedded Displays Market Size and Trends Analysis

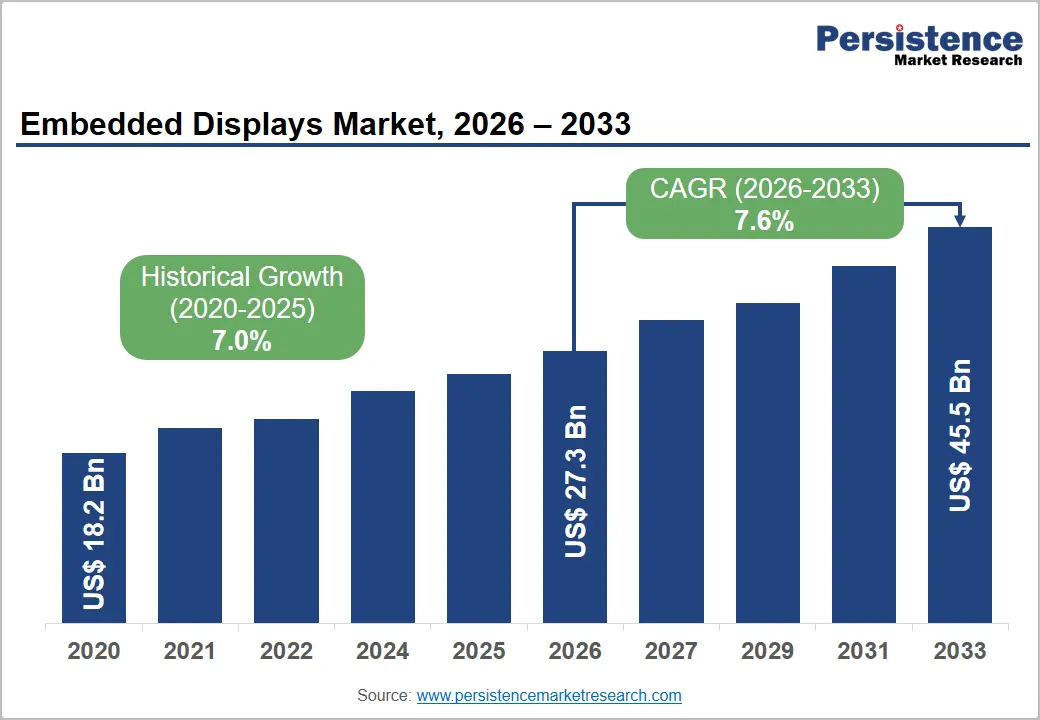

The global embedded displays market size is likely to be valued at US$27.3 billion in 2026 and is expected to reach US$45.5 billion by 2033, growing at a CAGR of 7.6% during the forecast period from 2026 to 2033, driven by increasing deployment of advanced human–machine interface (HMI) systems across automotive, industrial automation, and medical electronics sectors.

According to recent industry assessments from leading display supply-chain analyses (2025–2026), global demand is accelerating due to rapid EV adoption and digital cockpit integration in next-generation vehicles. Samsung Electronics and LG Display Co., Ltd. are scaling OLED and flexible panel production to meet automotive-grade requirements, while industrial adoption of touch-based embedded HMIs is expanding under Industry 4.0 frameworks.

Key Industry Highlights:

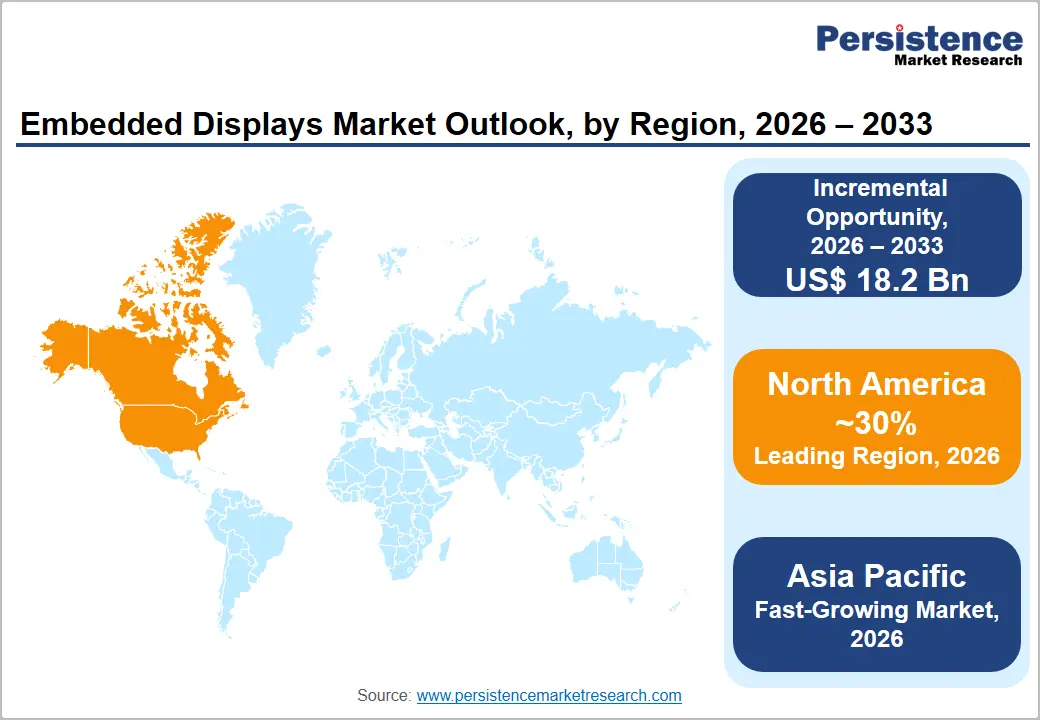

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 30% in 2026, driven by automotive electrification, industrial IoT expansion, and strong adoption of advanced HMI systems.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, supported by China’s manufacturing leadership, Japan’s advanced display innovation, and strong demand growth from India.

- Leading Product Type: Touch displays are projected to represent the leading product type in 2026, accounting for 58% of the revenue share, driven by their widespread adoption in intuitive human-machine interface (HMI) systems across automotive, industrial, and consumer applications.

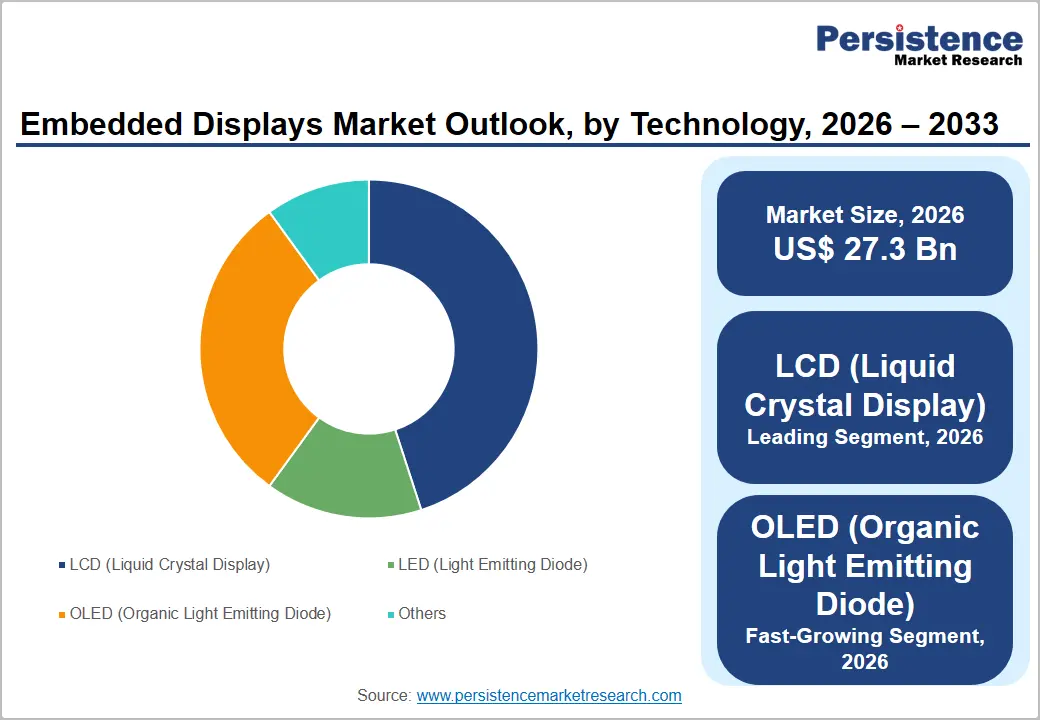

- Leading Technology Type: LCD (Liquid Crystal Display) is anticipated to be the leading technology type, accounting for over 45% of the revenue share in 2026, supported by its cost efficiency and widespread use in automotive and industrial systems.

- Key Opportunity: The key market opportunity in the embedded displays market lies in the rapid integration of advanced OLED/microLED and AR-enabled smart display systems across electric vehicles, industrial automation, healthcare devices, and connected IoT ecosystems, enabling immersive, real-time human–machine interaction.

DRO Analysis

Driver - Wearable Medical Device Proliferation & Remote Patient Monitoring

The embedded displays market is experiencing strong growth due to the rapid expansion of wearable medical devices and remote patient monitoring systems across healthcare ecosystems. Increasing demand for real-time health tracking through smartwatches, biosensors, and portable diagnostic equipment is driving the adoption of high-resolution, low-power embedded screens.

Hospitals and homecare providers are integrating connected monitoring solutions to improve patient outcomes and reduce costs. Advancements in miniaturized display technology enable continuous data visualization in compact devices. Rising chronic disease prevalence and aging populations accelerate demand.

Continuous advancements in embedded display technologies are significantly improving performance, durability, and energy efficiency across wearable and healthcare monitoring devices. Manufacturers are focusing on flexible OLED and micro-LCD panels that enable lightweight, compact designs suitable for continuous patient use. Integration with artificial intelligence and cloud-based analytics enhances real-time diagnostics and predictive healthcare insights.

Restraint - Data Security, Regulatory Compliance & Privacy Concerns

Embedded displays integrated into healthcare, automotive, and industrial systems face increasing concerns related to data security, regulatory compliance, and user privacy. As these systems become more connected through IoT and cloud platforms, the risk of cyberattacks and unauthorized data access increases significantly.

Regulatory complexity and evolving data protection standards further challenge the embedded displays market. Companies must navigate varying compliance requirements across regions, increasing operational costs, and slowing product deployment cycles. Frequent updates to cybersecurity frameworks require continuous system upgrades and validation processes, adding additional burden on manufacturers.

Opportunity - Augmented Reality & Next-Gen Display Convergence

Integration of AR interfaces into automotive heads-up displays, industrial maintenance systems, and healthcare visualization tools is creating new high-value applications. Advancements in microLED, flexible OLED, and waveguide optics are enabling more immersive and interactive user experiences. Companies are investing in lightweight, high-resolution embedded display systems that support real-time spatial computing.

This convergence is also driving innovation in smart glasses and wearable AR devices. Increasing demand for immersive visualization across defense, manufacturing, and medical training sectors is further accelerating market expansion. Another major opportunity arises from the increasing adoption of connected ecosystems and Industry 4.0 technologies, which require advanced embedded display systems for real-time monitoring and control.

Smart factories, autonomous vehicles, and digital healthcare platforms rely heavily on intuitive visualization interfaces for operational efficiency. The shift toward edge computing is enabling faster data processing directly on embedded display devices, reducing latency and improving performance. Demand for customizable, energy-efficient, and high-durability display solutions is increasing across multiple industries.

Category-wise Analysis

Product Type Insights

Touch displays are expected to lead, accounting for 58% of revenue in 2026, due to strong demand for intuitive and interactive human–machine interfaces across automotive, industrial, and consumer electronics applications. For example, modern EV platforms developed by companies like Tesla, Inc. rely heavily on large central touchscreen interfaces to control multiple vehicle functions, reflecting the strong market leadership of this segment.

Touch displays are also likely to represent the fastest-growing segment, supported by rising demand for advanced user interfaces, smart connectivity, and seamless digital interaction across industries. Growth is particularly strong in automotive electrification, wearable devices, and industrial automation systems, where real-time data visualization is critical. For instance, smart wearable healthcare devices such as advanced patient monitoring systems by Apple Inc. use embedded touch displays to provide real-time health insights and user interaction.

Technology Type Insights

LCD (Liquid Crystal Display) is projected to lead the market, capturing around 45% of the revenue share in 2026, supported by its cost-effectiveness, mature manufacturing ecosystem, and widespread use across automotive dashboards, industrial HMIs, and consumer electronics. A notable example includes industrial control systems used by Siemens AG, which commonly integrate LCD-based embedded displays for monitoring and process control applications.

OLED is likely to be the fastest-growing technology type due to its superior contrast ratio, flexibility, faster response time, and energy efficiency. These advantages make OLED highly suitable for premium automotive interiors, wearables, and next-generation consumer devices requiring high-quality visual output. For instance, automotive manufacturers such as BMW Group are increasingly integrating OLED-based curved dashboards in premium vehicles to enhance user experience and design aesthetics.

Regional Insights

North America Embedded Displays Market Trends

North America is anticipated to be the leading region, accounting for a market share of 30% in 2026, supported by the rapid adoption of advanced human–machine interfaces across automotive, healthcare, and industrial automation sectors. A notable example includes Tesla, Inc., which utilizes large embedded touchscreen interfaces in its electric vehicles, showcasing advanced integration of embedded display technology in next-generation mobility solutions across the region.

U.S. Embedded Displays Market Trends

The U.S. is expected to dominate the regional market, accounting for approximately 80% of the market share in 2026, driven by strong EV penetration, advanced healthcare digitalization, and Industry 4.0 deployment. The U.S. is investing heavily in smart factories and connected healthcare systems, boosting demand for embedded HMIs in monitoring and diagnostic devices. Wearable health technologies and remote patient monitoring platforms are increasingly integrated with high-performance display systems.

Canada Embedded Displays Market Trends

Canada is likely to be a significant market for embedded displays, holding approximately 20% of the market share in 2026, supported by the increasing adoption of smart industrial automation and digital healthcare infrastructure. Canadian manufacturers are focusing on energy-efficient display integration in medical imaging and transportation systems. Rising investments in AI-based healthcare analytics and smart city projects are further accelerating embedded display adoption across the country.

Europe Embedded Displays Market Trends

Europe is likely to be a significant market for embedded displays in 2026, due to strong automotive innovation, industrial automation, and increasing demand for energy-efficient display technologies. For example, BMW Group is integrating advanced curved OLED dashboards in its premium vehicles, highlighting Europe’s focus on high-end embedded display innovation and user-centric mobility design.

U.K. Embedded Displays Market Trends

The U.K. is expected to be a significant market for embedded displays, accounting for approximately 15% of the Europe market share in 2026, driven by increasing adoption across healthcare, aerospace, and smart infrastructure applications. Investments in digital hospitals and remote patient monitoring systems are accelerating demand for advanced medical display interfaces, while the aerospace and defense sectors continue to integrate rugged embedded displays for mission-critical operations.

Germany Embedded Displays Market Trends

Germany is anticipated to dominate the regional market, accounting for around 37% of the Europe market share in 2026, due to its strong automotive and industrial manufacturing base. The country is a leader in automotive digitalization, with widespread use of embedded HMIs in EV dashboards, factory automation systems, and robotics. German Industry 4.0 initiatives are accelerating the adoption of real-time monitoring and smart control interfaces.

Asia Pacific Embedded Displays Market Trends

The Asia Pacific region is likely to be the fastest-growing region for embedded displays in 2026. It has strong manufacturing ecosystems, rising consumer electronics demand, and rapid automotive electrification. For instance, Samsung Display is expanding OLED and flexible display production to meet rising demand in automotive and consumer electronics applications.

China Embedded Displays Market Trends

China is projected to dominate the regional market, holding around 30% market share in 2026, due to massive electronics manufacturing, EV expansion, and strong government support for high-tech industries. China dominates display production with extensive LCD and OLED fabrication capacity. The country is rapidly adopting digital cockpits in electric vehicles and smart industrial systems.

India Embedded Displays Market Trends

India is expected to emerge as a significant market, accounting for approximately 22% share in 2026, due to increasing EV adoption, expanding healthcare digitization, and smart manufacturing initiatives under government programs. Rising smartphone penetration and affordable electronics production are increasing demand for LCD-based embedded systems. India’s automotive sector is gradually integrating digital dashboards and infotainment systems in both passenger and commercial vehicles.

Competitive Landscape

The global embedded displays market exhibits a moderately fragmented structure, driven by rising demand for advanced human–machine interfaces across automotive, healthcare, and industrial applications. Increasing integration of OLED, LCD, and emerging microLED technologies is intensifying competition among display manufacturers.

With key leaders including Samsung Display, LG Display Co., Ltd., BOE Technology Group Co., Ltd., AU Optronics Corp., and Sharp Corporation dominating the landscape, competition remains technology-driven and highly innovation-centric. These players compete through continuous R&D investment, expansion of OLED and flexible display production capacity, and development of next-generation automotive-grade and industrial-grade embedded display solutions.

Key Industry Developments:

- In June 2026, Avalue introduced the EPC-TWL fanless embedded system powered by Intel Twin Lake processors, designed for edge AI and industrial automation applications. The system supports dual 4K displays, low power consumption, and industrial-grade reliability, making it suitable for smart manufacturing, healthcare, surveillance, and retail environments, strengthening demand for advanced embedded display-based computing solutions.

- In April 2026, Samsung Electronics Co., Ltd. launched its new IBF Series indoor LED displays designed for storefront and retail environments. The series features ultra-high brightness up to 3,500 nits, enabling clear visibility even in direct sunlight and enhancing customer engagement in digital signage applications.

Companies Covered in Embedded Displays Market

- Kyocera Corporation

- LG Display Co., Ltd.

- Samsung Electronics Co., Ltd.

- AU Optronics Corp.

- BOE Technology Group Co., Ltd.

- Sharp Corporation

- Panasonic Corporation

- Planar Systems, Inc.

- NEC Display Solutions, Ltd.

- CPT Technology Group, Ltd.

Frequently Asked Questions

The global embedded displays market is projected to reach US$27.3 billion in 2026.

Rising adoption of smart HMIs across automotive, healthcare wearables, and industrial IoT systems is driving the embedded displays market.

The embedded displays market is expected to grow at a CAGR of 7.6% from 2026 to 2033.

Integration of OLED, microLED, and AR-enabled next-generation display technologies in EVs, smart devices, and Industry 4.0 systems creates major growth opportunities.

Kyocera Corporation, LG Display Co., Ltd., Samsung Electronics Co., Ltd., and AU Optronics Corp. are the leading players.