- Sensors & Controls

- Electronic Cylinder Lock Credentials Market

Electronic Cylinder Lock Credentials Market Size, Share, and Growth Forecast 2026 - 2033

Electronic Cylinder Lock Credentials Market by Product Type (Electronic Key, RFID Key Cards, Key Fob & Badge), Technology (Low Frequency RFID, High Frequency RFID/NFC, Others), End-user (Commercial Sector, Residential Sector, Industrial Sector, Government), and Regional Analysis, 2026 - 2033

Electronic Cylinder Lock Credentials Market Size and Trend Analysis

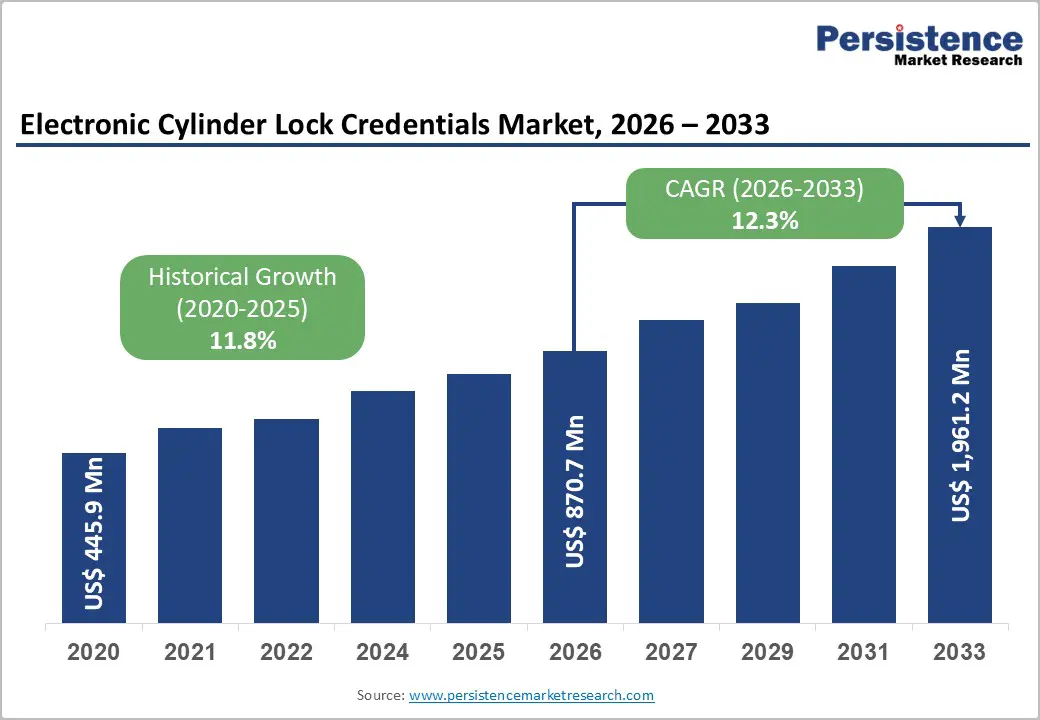

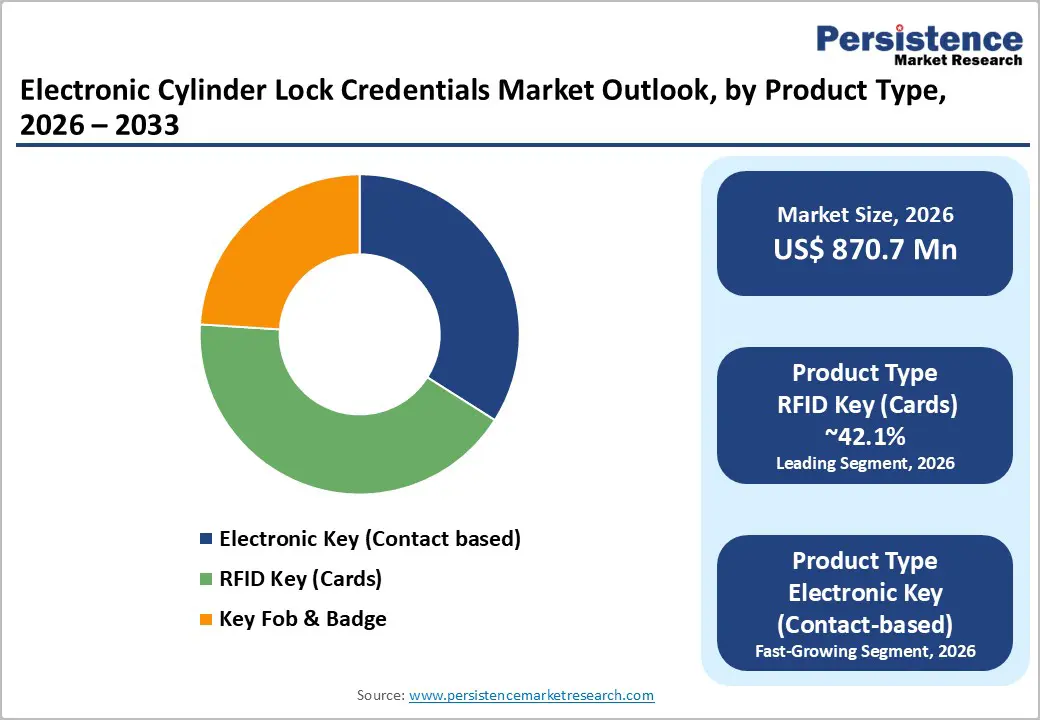

The global electronic cylinder lock credentials market is estimated to be valued at US$ 870.7 million in 2026 and is projected to reach US$ 1,961.2 million by 2033, expanding at a CAGR of 12.3% from 2026 to 2033.

Market growth is driven by the rapid rollout of smart city initiatives, rising cybersecurity concerns related to physical access control, and increasing adoption of IoT-enabled security systems. Growing urbanization across residential, commercial, and government sectors is accelerating demand for contactless and digital credential solutions that enable enhanced security, improved operational efficiency, and real-time access monitoring.

Key Industry Highlights:

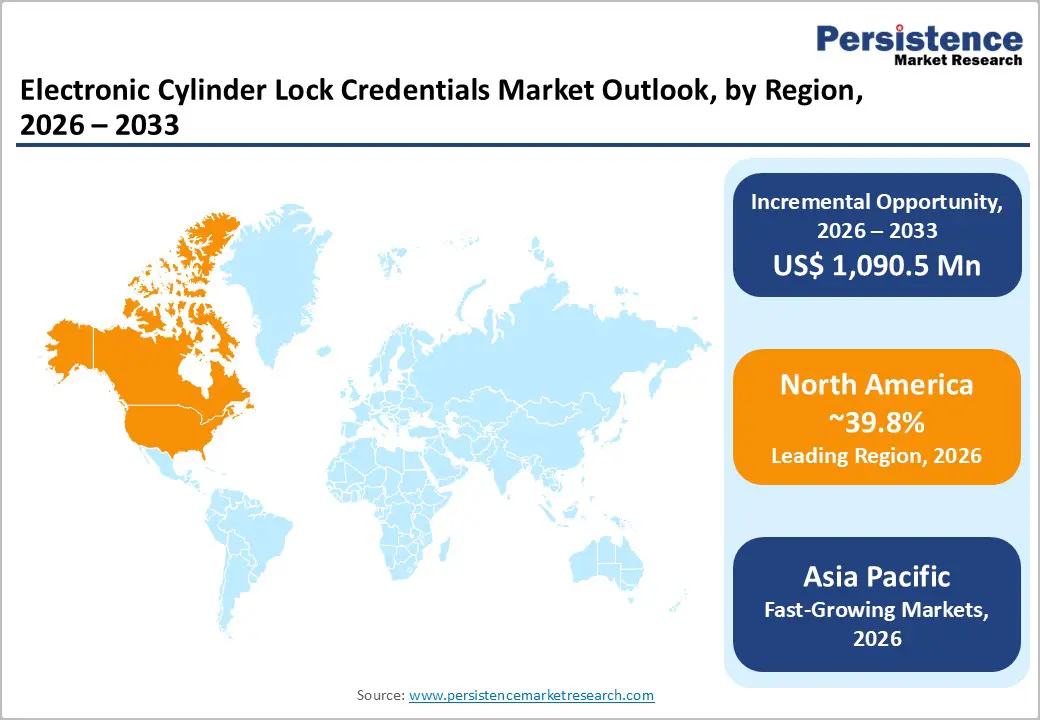

- Leading Region: North America holds ~39.8% of the global market share, driven by smart home adoption, advanced infrastructure, and regulatory security modernization.

- Fastest-Growing Region: Asia Pacific accounts for ~32% of the market, fueled by urbanization, smart city programs, and growing digital credential adoption.

- Leading Category: RFID Key Cards command ~42.1% share due to durability, standardization, and compatibility with enterprise access control systems.

- Fastest-Growing Category: Mobile credentials are rapidly growing with cloud-based management and frictionless smartphone authentication gaining enterprise acceptance.

- Key Market Opportunity: Commercial access control drives ~58% of demand, powered by multi-site operations, enterprise adoption, and ongoing facility modernization.

| Key Insights | Details |

|---|---|

| Electronic Cylinder Lock Credentials Market Size (2026E) | US$ 870.7 Million |

| Market Value Forecast (2033F) | US$ 1,961.2 Million |

| Projected Growth CAGR (2026 - 2033) | 12.3% |

| Historical Market Growth (2020 - 2025) | 11.8% |

Market Dynamics

Drivers - Rising Demand for Contactless, Mobile-Enabled, and Smart Access Control Solutions

The rapid shift toward contactless access has become a structural driver of electronic cylinder lock credentials, accelerated by evolving expectations for health, safety, and convenience. High-frequency RFID (NFC) credentials and mobile-based authentication are increasingly replacing mechanical keys across commercial and residential settings. Organizations favor credential systems that deliver real-time access visibility, detailed audit trails, and instant remote revocation to reduce security risks and administrative burden.

This transition is reinforced by strong momentum in the smart lock ecosystem, where deadbolt smart locks continue to dominate adoption due to perceived reliability and enhanced protection. Integration with mobile wallets and cloud-based credential management platforms further boosts scalability, enabling enterprises to centralize access control while minimizing on-premise infrastructure and strengthening data security compliance.

Government-Led Infrastructure Modernization and Smart City Security Mandates

Public sector modernization programs are a major catalyst for the adoption of electronic cylinder lock credentials, as governments embed digital access control into smart city and critical infrastructure initiatives. Regulatory bodies such as the U.S. National Institute of Standards and Technology (NIST) have established frameworks to ensure secure deployment of connected access technologies, reinforcing confidence in credential-based systems across public buildings and facilities.

Large-scale smart city investments and federal cybersecurity mandates are compelling agencies to upgrade legacy access systems. Requirements from authorities such as CISA for strengthened physical access controls are driving demand for interoperable, standards-compliant electronic credentials across government, healthcare, and educational institutions, creating long-term, regulation-backed market expansion.

Restraints - Cybersecurity Vulnerabilities and Exposure of Physical Access Systems to Digital Threats

Despite technological advancements, electronic cylinder lock credentials remain vulnerable to cybersecurity threats that can undermine physical security. Documented weaknesses in certain smart lock systems include poor encryption practices, insecure firmware architectures, and limited ability to deploy timely security updates. Wireless communication technologies such as Bluetooth and Wi-Fi also introduce exposure to signal interception, replay attacks, and jamming, increasing the attack surface for unauthorized access.

Government cybersecurity agencies and independent security researchers have repeatedly highlighted risks associated with poorly secured connected access devices. These concerns slow adoption among security-sensitive sectors such as government, financial services, and healthcare, where credential compromise can result in severe operational disruption, compliance violations, and heightened liability exposure.

High Initial Investment Requirements and Ongoing Cost of Ownership

The transition from mechanical locks to electronic cylinder lock credential systems requires significant upfront and recurring investments, acting as a restraint on market growth. Organizations must account for costs related to electronic lock hardware, credential issuance infrastructure, cloud-based access management platforms, and workforce training. Beyond installation, ongoing expenses include software subscriptions, system integration, credential lifecycle management, and periodic security audits.

The need for backup power solutions, redundant access mechanisms, and disaster recovery planning further elevates the total cost of ownership. These financial considerations often delay adoption among small enterprises, residential property owners, and cost-sensitive markets, particularly in developing regions where capital expenditure constraints remain a key barrier.

Opportunity - Rapid Integration of Biometric Authentication and AI-Enabled Access Intelligence

Advances in biometric authentication technologies such as fingerprint recognition, facial identification, and iris scanning are creating strong opportunities for electronic cylinder lock credential providers. Improvements in sensor accuracy, processing speed, and system reliability are enabling manufacturers to develop hybrid credential solutions that combine biometrics with mobile or RFID authentication to provide higher-assurance access control. The integration of artificial intelligence and machine learning allows access systems to analyze user behavior, identify anomalies, and dynamically adjust authentication requirements based on risk profiles.

Leading access solution providers are increasingly investing in AI-driven computer vision and analytics capabilities to enhance security across high-traffic and high-risk environments such as airports, data centers, and critical infrastructure facilities. These developments enable product differentiation through adaptive security, reduced false access events, and improved user experience, positioning biometric-enabled credentials as a premium offering for government and enterprise deployments.

Expansion of IoT Ecosystems and Cloud-Managed Access Control Architectures

The continued expansion of IoT infrastructure and cloud connectivity is creating significant growth opportunities for electronic cylinder lock credential ecosystems. Cloud-managed access control platforms allow organizations to centrally issue, modify, and revoke credentials without on-site servers, improving scalability and operational efficiency across distributed facilities. Integration with edge processing capabilities ensures reliable authentication and rapid response even in environments with intermittent network connectivity.

At the same time, the emergence of globally recognized cybersecurity and interoperability standards, such as ETSI EN 303 645 and ISA/IEC 62443, is reducing integration complexity in multi-vendor environments. This shift toward open, standards-compliant architectures is enabling manufacturers to address smart city, commercial, and institutional projects more effectively. Rapid urban infrastructure development across the Asia Pacific further amplifies demand for flexible, cloud-based credential solutions.

Category-wise Analysis

Product Type Insights

RFID key cards represent the leading product category in the electronic cylinder lock credentials market, accounting for the largest share, which is 42.1% in 2025, due to their durability, standardized security protocols, and seamless compatibility with enterprise access control systems. Approximately 75% of commercial access control installations utilize RFID-based credentials, reflecting strong institutional acceptance. Contact-based electronic keys remain relevant in retrofit and cost-sensitive deployments, while key cards remain dominant in commercial, healthcare, and education environments.

Mobile credentials and NFC-enabled smartphone wallets are emerging as the fastest-growing product category, driven by demand for frictionless access and digital-first credential management. Organizations increasingly view mobile credentials as a long-term replacement for physical media, particularly in multi-site enterprises and smart buildings, despite continued resistance to exclusive reliance on personal devices for critical access control use cases.

Technology Insights

High-Frequency RFID (13.56 MHz NFC) dominates the electronic cylinder lock credentials market with approximately 68% market share in 2025, supported by advanced security features such as AES encryption, mutual authentication, and dynamic credential generation. NFC’s bidirectional communication capabilities and resistance to cloning attacks have positioned it as the preferred technology for enterprise, government, and institutional deployments requiring strong authentication assurance.

Biometric-enabled and AI-integrated credential technologies represent the fastest-growing technology segment, driven by increasing demand for adaptive security and identity-based access control. Fingerprint, facial recognition, and hybrid biometric credentials are gaining traction in high-security environments, as organizations seek systems capable of behavioral analysis, anomaly detection, and real-time risk-based authentication beyond static credential validation.

End-user Insights

The commercial sector is the largest end-use category, accounting for approximately 58% of total market demand in 2025, driven by widespread adoption across office buildings, hospitality, retail, and logistics facilities. Enterprises increasingly deploy electronic cylinder lock credentials to centralize employee access, streamline visitor management, and protect distributed assets. Strong uptake among small and mid-sized businesses further reinforces commercial sector dominance.

The residential sector is the fastest-growing end-use category, supported by smart home adoption, real estate digitization, and developer-led standardization of electronic access systems. Government and institutional demand is also expanding steadily, as public agencies prioritize credential-based access control to meet regulatory compliance, auditability, and high-assurance security requirements across critical infrastructure and sensitive facilities.

Regional Insights

North America Electronic Cylinder Lock Credentials Market Trends

North America represents the largest regional market for electronic cylinder lock credentials, accounting for approximately 39.8% of global market share, led by strong adoption in the United States. High penetration of smart home technologies, mature access control infrastructure, and strong enterprise demand have supported widespread deployment across residential and commercial buildings. Security awareness, combined with a preference for contactless and cloud-managed access solutions, continues to reinforce regional leadership.

Residential applications dominate regional demand, supported by smart home integration and urban security concerns, while commercial adoption is accelerating across hospitality, offices, and multi-tenant properties. Property managers increasingly embed digital credentials into long-term modernization plans to improve access efficiency, reduce operational friction, and enhance user experience through mobile and credential-based entry systems.

Europe Electronic Cylinder Lock Credentials Market Trends

Europe is experiencing stable and regulation-driven growth in the electronic cylinder lock credentials market, supported by strong data protection, cybersecurity, and interoperability requirements. The regional market is projected to expand at a CAGR of around 14.6% during the forecast period, driven by adoption across commercial, healthcare, and financial institutions seeking high-assurance access control solutions.

Regulatory frameworks such as GDPR, the EU Data Act, and digital interoperability mandates are influencing purchasing decisions, favoring secure, standards-compliant credential platforms. Enterprises across Germany, the UK, and France are prioritizing cloud-managed credentials that support multi-site operations, auditability, and integration with broader building management and security ecosystems.

Asia Pacific Electronic Cylinder Lock Credentials Market Trends

Asia Pacific is emerging as a high-growth region and accounts for approximately 32% of the global electronic cylinder lock credentials market, driven by rapid urbanization and smart infrastructure development. China, Japan, India, and South Korea are leading adoption through residential high-rise construction, commercial real estate expansion, and government-backed smart city programs.

The region is witnessing the rapid adoption of mobile credentials, RFID systems, and integrated smart building solutions across residential and commercial environments. Growing middle-income groups, increasing digital literacy, and integration with IoT platforms are accelerating deployment. Local manufacturing capabilities and cost-competitive solutions further support large-scale adoption of credential systems across diverse Asia-Pacific economies.

Competitive Landscape

The electronic cylinder lock credentials market is moderately consolidated, with global leaders strengthening their positions through continuous portfolio expansion, geographic diversification, and technology-focused acquisitions. Market participants are increasingly emphasizing digital credential ecosystems, software-driven revenue models, and integration of advanced technologies such as biometrics, edge computing, and AI-based access intelligence. Strategic investments are aimed at enhancing interoperability, scalability, and recurring service revenues while addressing growing enterprise and government security requirements.

Competition is increasingly shaped by adherence to open standards, secure encryption architectures, and cloud-managed credential platforms. Vendors are differentiating through credential-as-a-service models, mobile-first access solutions, and unified platforms supporting both physical and logical access control. Innovation around secure data handling, auditability, and ecosystem compatibility remains a key determinant of long-term competitive advantage.

Key Market Developments:

- In September 2024, ABLOY, the global leader in access solutions, acquired Level Lock, a California-based smart lock company with approximately 70 employees and US$ 16 million in annual sales. The acquisition strengthens ASSA ABLOY's digital access portfolio and innovative credential technologies for the North American residential market.

- In January 2025, Allegion launched Schlage Sense Pro and Arrive Smart WiFi deadbolts with Matter-over-Thread compatibility, enabling seamless integration with smart home ecosystems. The products support mobile credentials, including MIFARE and Bluetooth technologies, to enhance user convenience and enterprise-grade security.

- In November 2025, dormakaba announced a strategic investment in RealSense Inc., a pioneer in AI-powered computer vision, to accelerate the development of intelligent access solutions for data centers, airports, and critical infrastructure. The partnership combines RealSense's computer vision leadership with dormakaba's global access solutions expertise to deliver next-generation biometric authentication systems.

Companies Covered in Electronic Cylinder Lock Credentials Market

- ASSA ABLOY Group

- Dormakaba Group

- Allegion plc

- SALTO Systems

- SimonsVoss Technologies

- HID Global

- Identiv Inc.

- NXP Semiconductors

- Thales Group

- IDEMIA

- Suprema Inc.

- ZKTeco Co. Ltd.

- Paxton Access Ltd.

- Gallagher Group

- Giesecke+Devrient

Frequently Asked Questions

The market is projected to reach US$ 870.7 Million in 2026, growing at a CAGR of 12.3% through 2033, driven by smart city initiatives, IoT integration, and regulatory compliance.

Demand is fueled by smart city development, IoT-enabled security investments, CISA/NIST compliance, contactless credential adoption, and cloud-based credential management, reducing operational costs.

High-Frequency RFID (NFC) leads with approximately 68% market share, offering AES encryption, mutual authentication, dynamic code generation, and multi-application support for high-assurance use.

North America holds ~39.8% share, supported by smart home adoption, advanced infrastructure, and government-driven smart city and security mandates.

Opportunities include biometric integration, IoT infrastructure expansion, cloud-managed access control, and government smart city initiatives, especially in the Asia Pacific (~32% share).

Key players include ASSA ABLOY Group, Dormakaba Group, Allegion plc, SALTO Systems, and SimonsVoss Technologies.