- Medical Devices

- Drug Delivery Devices Market

Drug Delivery Devices Market Size, Share, and Growth Forecast, 2025 - 2032

Drug Delivery Devices Market By Device Type (Inhalers, Injection Pens, Others), Indication (Diabetes, Oncology/Cancer, Others), End-user (Hospitals, Home Healthcare, Ambulatory Surgical Centers (ASCs), Diagnostic Centers, Others), and Regional Analysis for 2025 - 2032

Drug Delivery Devices Market Share and Trends Analysis

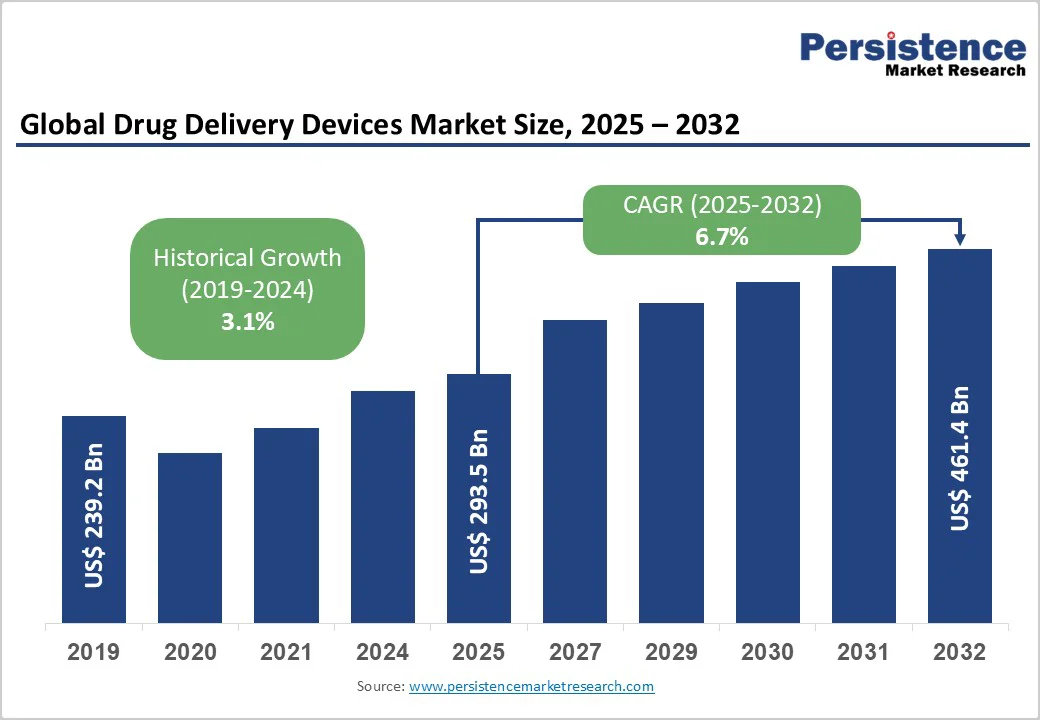

The global drug delivery devices market size is likely to be valued at US$293.5 Billion in 2025, and is estimated to reach US$461.4 Billion by 2032, growing at a CAGR of 6.7% during the forecast period from 2025 to 2032, driven by an accelerating adoption of smart, connected technologies, increased investments in biologics, and the growing prevalence of chronic diseases worldwide.

Market growth is driven by investments in patient-centric drug delivery, supportive regulatory reforms, and ongoing product innovations. Demographic shifts, regulatory alignment, and global supply-chain integration make device innovation and end-user adaptation key to gaining market share and margins.

Key Industry Highlights

- Leading & Fastest-growing Device Types: Inhalers are likely to account for an estimated 24.4% market share in 2025; wearable injectors are projected to achieve the fastest CAGR of about 10.8% from 2025 to 2032.

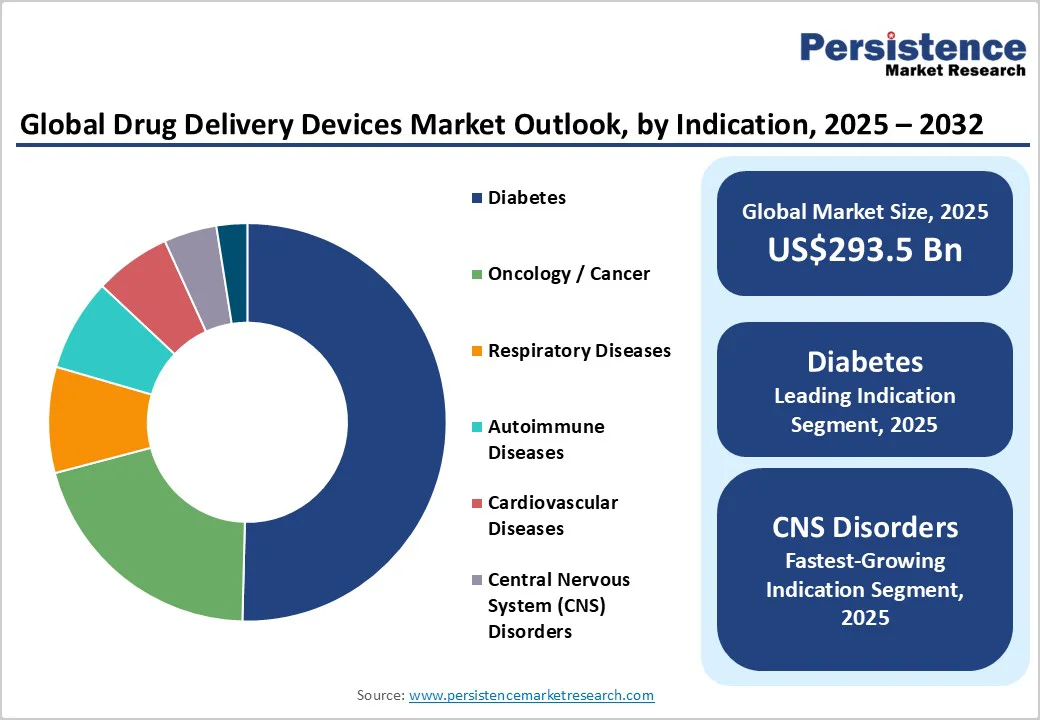

- Dominant Indications: Diabetes is expected to represent 50.4% of market revenues in 2025, while CNS disorders will be the fastest-growing indication through 2032.

- Leading End-users: Hospitals are slated to be the dominant end-users, holding 45.5% market share in 2025, whereas home healthcare is poised to expand at the highest CAGR.

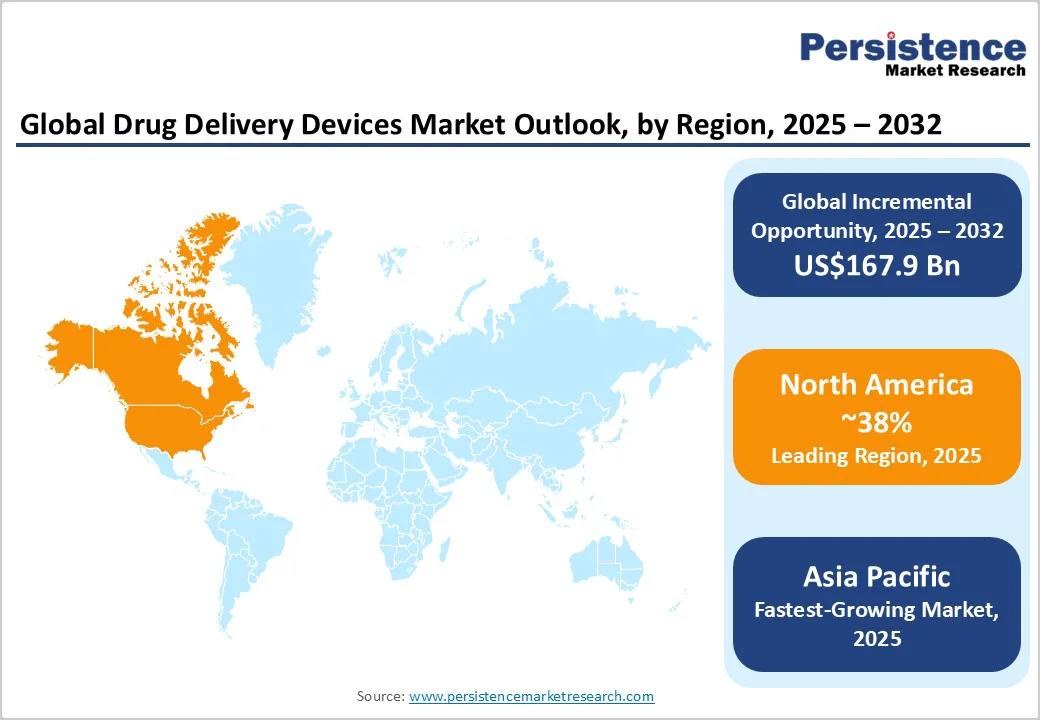

- Regional Leadership: North America is anticipated to maintain market leadership with 38.1% share in 2025, with Asia Pacific being forecast to grow the fastest between 2025 and 2032, due to rising adoption of drug delivery devices in urban home settings.

- Investment Trends: Strategic investments in smart, connected drug delivery platforms are driving competitive differentiation and enabling higher-margin growth in oncology and diabetes.

- Competitive Dynamics: Technology partnerships, geographic expansions, and targeted M&A transactions continue to govern competitive decisions, improve innovation outcomes, and facilitate entry into new therapeutic and regional markets.

- September 2025: The U.S. Food and Drug Administration (FDA) cleared Medtronic’s MiniMed™ 780G insulin delivery system for integration with Abbott’s FreeStyle Libre 3 continuous glucose monitor (CGM), enabling more precise and automated glucose management for people with type 2 diabetes.

| Key Insights | Details |

|---|---|

| Drug Delivery Devices Market Size (2025E) | US$293.5 Bn |

| Market Value Forecast (2032F) | US$461.4 Bn |

| Projected Growth (CAGR 2025 to 2032) | 6.7% |

| Historical Market Growth (CAGR 2019 to 2024) | 3.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Introduction of Connected, Patient-Oriented Drug Delivery Technologies

Smart, connected drug delivery devices are redefining therapeutic paradigms in chronic disease management, catalyzing sustained market growth.

Regulatory agencies such as the U.S. FDA and the European Medicines Agency (EMA) have issued landmark guidance promoting digital health technologies and enabling broader authorization pathways for Bluetooth-enabled and mobile-app connected injectors and wearables, positioning the concept of connected care as the new industry standard.

According to healthcare industry associations, the majority of leading hospitals globally have integrated some form of digital drug delivery tracking or compliance monitoring in their chronic disease programs, offering real-time dosing validation and adherence optimization.

Smart injectors and wearable pumps have been proven to reduce hospitalization rates considerably, minimize dosing errors, and improve patient outcomes. This can save billions for both patients and healthcare facilities over the next several years.

Complexity and Cost of Clinical Validation for Advanced Drug Device Combinations

A key constraint confronting the drug delivery device market growth is the escalating cost and complexity associated with regulatory-driven clinical validation, particularly for combination products in biologics and breakthrough therapies.

The average time-to-market for advanced drug-device combinations in the U.S. has increased notably, due to expanded requirements for safety, effectiveness, human factors engineering, and post-market surveillance per the FDA’s Combination Products Rule (21 CFR Part 4).

Industry trade groups highlight that median device development expenditure for biologic-adapted injectors now exceeds US$172 Million, owing to the need for dual regulatory review. The risk-adjusted attrition rate in Phase III human trials for combination therapies also remains high, mainly attributable to device integration failures and adverse event reporting discrepancies.

These dynamics pose substantial risks for investors and strategic planners, as failed clinical validation attempts delay market entry, raise operational costs, and compress short-term profitability.

Integration of Artificial Intelligence and Machine Learning in Drug Delivery Systems

The integration of artificial intelligence (AI) and machine learning (ML) within drug delivery devices is ushering in a new era of personalized medicine, representing a highly lucrative and transformative market opportunity. Healthcare institutions and regulatory agencies globally are increasingly promoting AI-driven therapeutic solutions that optimize dosing, improve patient adherence, and predict adverse events, thereby enhancing treatment efficacy and safety profiles.

AI algorithms embedded in connected wearables, injectors, and infusion pumps analyze real-time patient data, adapting delivery protocols dynamically based on biometrics and drug response patterns, which can reduce hospitalization rates by up to 30% as per clinical trials endorsed by the National Institutes of Health (NIH) and international health bodies.

Industry leaders investing in AI and ML capabilities are achieving revenue uplift through enhanced product differentiation, improved customer retention, and new software-as-a-medical-device (SaMD) revenue streams.

Investors and business strategists prioritizing AI integration as a core innovation pillar are positioned to capture significant market share in rapidly expanding segments such as smart injectors, continuous glucose monitors integrated with insulin pumps, and precision oncology drug delivery platforms.

The potential of AI/ML extends beyond device performance into predictive maintenance, supply chain forecasting, and patient engagement platforms, positioning this intersection of technology and therapeutics as a cornerstone for future growth and competitive advantage.

Category-wise Analysis

Device Type Insights

Inhalers are expected to firmly dominate with an estimated 24.4% of the drug delivery devices market revenue share in 2025. This leadership position is primarily supported by the massive global burden of chronic respiratory diseases, particularly asthma and chronic obstructive pulmonary disease (COPD), which collectively affect millions of individuals worldwide.

Countries with high prevalence rates, such as the U.S. and parts of Europe, have well-established reimbursement channels that facilitate wide adoption of inhaler technologies. Furthermore, innovation in smart and digital inhalers, incorporating dose counters, connectivity features, and patient adherence tracking, is augmenting the therapeutic effectiveness and user experience.

Wearable injectors are likely to be the fastest-growing device segment through the 2025 - 2032 forecast period, posting the highest CAGR. The segment growth is propelled by an increasing demand for home-administration solutions in chronic disease treatment, advancements in miniaturization and sensor technologies, and regulatory encouragement for connected health devices.

The proliferation of wearable injectors is especially notable in diabetes and oncology, where continuous and accurate drug dosing improves clinical outcomes. The integration of AI and machine learning to personalize drug delivery further distinguishes wearable injectors as a transformative innovation.

Indication Insights

Diabetes is poised to dominate the market landscape with approximately 50.4% of the revenue in 2025, aided by the unprecedented rise in the number of people affected by diabetes globally. According to the International Diabetes Federation (IDF), in 2024, 589 million people worldwide were living with diabetes, and by 2050, this number is projected to rise to 853 million.

The insulin delivery segment, including pens, pumps, and connected devices, has become central to managing the chronic and expanding burden of this disease. Supportive government policies, increasing insurance reimbursements for smart insulin delivery systems, and efforts to enhance patient self-management are reinforcing the segment’s market strength.

Technological innovations such as closed-loop insulin delivery systems and integration with continuous glucose monitors augment therapy precision and convenience, driving higher adoption and satisfaction rates.

CNS disorders are poised to be the fastest-growing indication segment, predicted to display a CAGR of nearly 11% through 2032, fueled by the rising incidence of neurodegenerative diseases such as Alzheimer’s and Parkinson’s among aging populations globally.

Breakthroughs in drug delivery technologies that cross the blood-brain barrier, through implantable pumps, intrathecal delivery systems, and advanced targeted modalities, are expanding therapeutic possibilities for diseases previously considered intractable.

This segment’s growth is supported by increasing investment from biopharmaceutical innovators specializing in precision neurotherapies and favorable regulatory pathways facilitating fast-track approvals for CNS-focused drug-device combinations.

End-user Insights

Hospitals constitute the dominant end-user segment with an estimated 45.5% share in 2025, driven by their role as centralized hubs for acute, chronic, and specialty care requiring high volumes of advanced drug delivery devices.

The hospital environment provides the infrastructure and clinical staffing necessary for managing complex therapies via infusion pumps, implantable devices, and hospital-administered injectors. Strategic investments in hospitals’ acquisition of connected, smart drug delivery platforms are amplified by digital health initiatives that incentivize safety, dosage accuracy, and patient monitoring.

The home healthcare segment is likely to be the fastest-growing over the forecast period 2025 - 2032. This growth trajectory is driven by increasing patient preference for autonomy, the expansion of telehealth services, and technology advances enabling safe, effective drug delivery outside institutional settings.

Self-administered devices, including wearable injectors, smart pens, and connected infusion pumps, are pivotal in chronic disease management, especially diabetes and autoimmune disorders, enabling patients to manage therapies remotely with real-time data sharing to healthcare providers. Insurance coverage enhancements and regulatory reforms promoting at-home care delivery are also expected to accelerate adoption.

Regional Insights

North America Drug Delivery Devices Market Trends

North America is set to hold the leading position with an estimated 38.1% of the drug delivery devices market share in 2025.

The regional market mainly benefits from a progressive regulatory landscape spearheaded by the U.S. FDA’s Digital Health Innovation Action Plan, which incentivizes AI-enabled devices and expedites approval of connected drug delivery platforms. Strong R&D centers, venture capital investment in digital therapeutics, and government-backed chronic disease programs are accelerating the adoption of advanced injectors, smart inhalers, and implantable pumps.

Market growth here is also driven by intensive integration of AI/ML in device design, increasing government support for home-based care technologies, and expanding reimbursement policies for remote patient monitoring. The competitive framework is characterized by a concentrated yet innovation-rich ecosystem, with pivotal players leveraging strategic partnerships with digital health platforms and payer ecosystems to enhance market access and reimbursement viability.

Europe Drug Delivery Devices Market Trends

Europe is likely to secure a substantial 28.3% market share in 2025. Germany, the U.K., France, and Spain are expected to play leading roles through well-established public healthcare systems, harmonized regulatory environments shaped by the Medical Device Regulation (MDR) of the European Union (EU), and pan-European clinical trial networks enabling efficient multi-country product launches.

The growth trajectory of the market in Europe reflects accelerated adoption of minimally invasive and AI-driven delivery devices, bolstered by integrated European health technology assessment agencies and wide-ranging reimbursement schemes. The EU’s regulatory environment also strongly supports interoperability standards and data security protocols, mandating compliance-driven design innovations.

Asia Pacific Drug Delivery Devices Market Trends

Asia Pacific is slated to emerge as the fastest-growing regional market and capture roughly 31% of the market share in 2025. China dominates regional sales with significant government initiatives fostering regulatory modernization, digital health integration, and reimbursement expansions specific to chronic disease device adoption.

India and ASEAN nations offer high-potential emerging markets supported by expanding middle-class healthcare accessibility and domestic manufacturing capabilities. The regional market is also fueled by healthcare policy reforms, expanding health insurance coverage, and a growing chronic disease burden induced by an exponential expansion of urban areas.

Competitive dynamics are characterized by a mix of global players establishing localized production and agile domestic manufacturers innovating cost-effective, user-friendly devices tailored to regional needs. Strategic imperatives include robust regulatory engagement, scalable supply chain configurations, and culturally adaptive marketing and distribution models well-aligned with the region's digitizing healthcare ecosystems.

Competitive Landscape

The global drug delivery devices market structure exhibits moderate consolidation. Medical device industry giants such as Johnson & Johnson, Becton Dickinson, and Medtronic command extensive device portfolios covering injectable, infusion, and wearable sectors, augmented by significant R&D investment.

Market fragmentation persists within high-growth connected devices and region-specific segments, where medium-sized innovators and startups compete through niche product focus and agile deployment.

The ongoing shift toward software-driven drug delivery platforms fosters emerging partnerships and platform cooperatives, indicating a gradual trend toward a convergent market structure underpinned by regulatory standardization and interoperability requirements. Competitive positioning is increasingly predicated on digital health integration capabilities, patient adherence technologies, and strategic geographic expansion.

Key Industry Developments

- In October 2025, Stevanato Group expanded its Bad Oeynhausen facility with a new ISO 8 cleanroom, boosting injection molding and automated assembly for Aidaptus® autoinjectors and Alina® pen injectors. The upgrade enhances operational flexibility, accelerates time-to-market, and strengthens the Group’s role in patient-centric, personalized self-injection therapies.

- In September 2025, Biogen acquired Alcyone Therapeutics, gaining its proprietary convection-enhanced delivery (CED) technology for targeted CNS therapy delivery. This acquisition strengthens Biogen’s neurodegenerative disease portfolio, enhances next-generation CNS treatment development, and reinforces its commitment to innovative drug delivery solutions addressing unmet medical needs.

- In May 2025, researchers from Andhra Pradesh, with Saudi Arabia and UAE scientists, developed a colon-targeted drug delivery system using cross-linked mastic gum nanoparticles. Encapsulating 5-fluorouracil with 83.5% efficiency, it delivers 95.2% of the drug to the colon, maximizing efficacy and minimizing systemic toxicity and side effects.

Companies Covered in Drug Delivery Devices Market

- Becton, Dickinson and Company

- Johnson & Johnson

- Medtronic PLC

- Roche Holding AG

- Boston Scientific Corporation

- Smiths Medical (ICU Medical, Inc.)

- Bayer AG

- Novartis AG (Alcon)

- 3M Health Care

- Terumo Corporation

- Baxter International Inc.

- Merck & Co., Inc.

- Abbott Laboratories

- Pfizer Inc.

- Siemens Healthineers AG

Frequently Asked Questions

The drug delivery devices market is projected to reach US$293.5 Billion in 2025.

The drug delivery devices market is driven by rising adoption of smart, connected medical devices, increased biologics investments, and the growing global prevalence of chronic diseases, particularly diabetes and cancer.

The drug delivery devices market is poised to witness a CAGR of 6.7% from 2025 to 2032.

Increasing preference for patient-centric drug delivery solutions, proactive regulatory reforms supporting device innovation, and integration of medical supply chains are the key market opportunities.

Becton, Dickinson and Company, Johnson & Johnson, and Medtronic PLC are a few of the key market players.