- Hardware & Software IT Services

- Digital Signature Market

Digital Signature Market Size, Share, and Growth Forecast 2026 - 2033

Digital Signature Market by Type of Level (Advanced Electronic Signatures (AES) and Qualified Electronic Signatures (QES)), Component (Solutions and Services), by Industry Vertical (BFSI, Health Care & Life Science, IT & Telecom, Government, Retail and Others), and End- user (Individuals, Businesses and Organizations) and Regional Analysis for 2026 - 2033

Digital Signature Market Size and Share Analysis

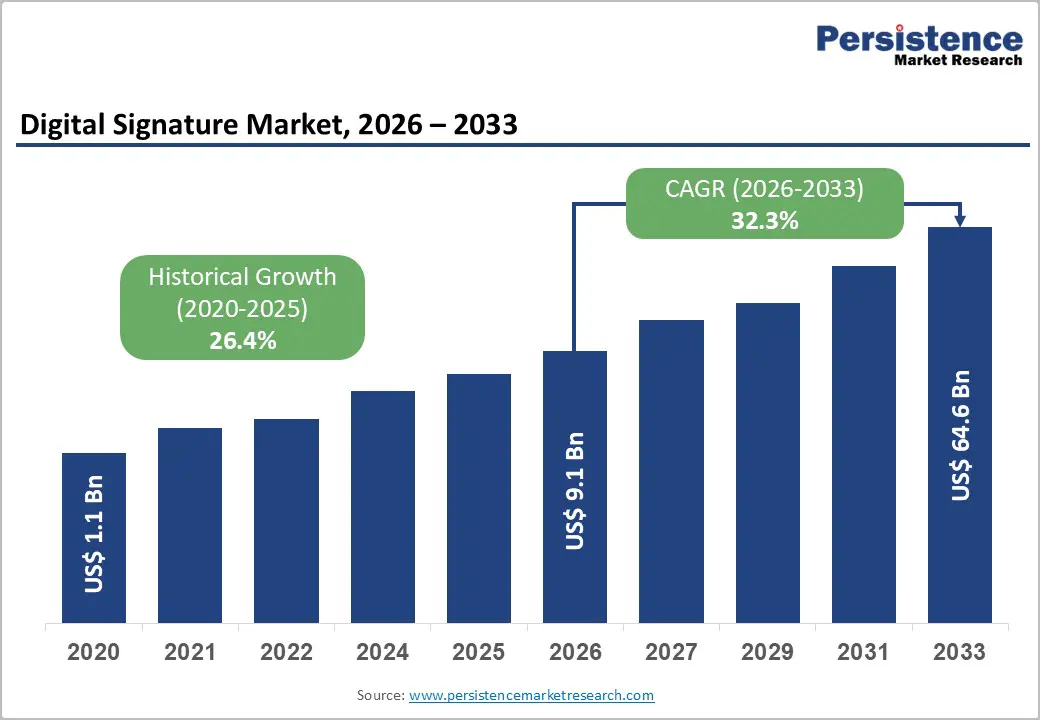

The global Digital Signature Market size was valued at US$ 9.1 Bn in 2026 and is projected to reach US$ 64.9 Bn by 2033, growing at a CAGR of 32.4% between 2026 and 2033.

Market growth is fundamentally driven by the critical imperative for secure and legally binding electronic transactions across all industry verticals and geographies, combined with accelerating government regulatory mandates, including EU eIDAS (Electronic Identification, Authentication and Trust Services), requiring Qualified Electronic Signatures (QES) for high-value and regulated transactions.

Key Market Highlights

- Leading region: North America dominates the digital signature Market with approximately 42–45% global revenue share, driven by the large BFSI sector, advanced technology adoption, stringent regulatory requirements including HIPAA, SEC, and SOX, and concentration of major digital signature vendors and enterprise customers.

- Fastest growing region: Asia Pacific is the fastest-growing regional market, expanding at 38–42% CAGR, fueled by rapid government digitalization in India, China, and ASEAN, exploding e-commerce adoption, and emerging qualified electronic signature regulatory mandates driving infrastructure investments.

- Dominant segment: Advanced Electronic Signatures (AES) dominates by type, with approximately 52% market share, reflecting a balance among regulatory recognition, implementation accessibility, and cost-effectiveness, while remaining complementary to the growth of emerging qualified electronic signatures.

- Fastest growing segment: Qualified electronic signatures (QES) is the fastest-growing segment, expanding at 35% CAGR, driven by EU eIDAS compliance mandates, cross-border transaction requirements, and regulated industry adoption particularly in BFSI, government, and healthcare verticals.

- Key market opportunity: Government digitalization initiatives and emerging market expansion in India, China, Latin America, and ASEAN represent the most attractive growth opportunity, with governments mandating digital signatures in administrative, licensing, and regulatory compliance processes, creating massive addressable markets.

| Key Insights | Details |

|---|---|

|

Digital Signature Market Size (2026E) |

US$ 9.1 Bn |

|

Market Value Forecast (2033F) |

US$ 64.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

32.4% |

|

Historical Market Growth (CAGR 2020 to 2024) |

26.5% |

Market Dynamics

Market Growth Drivers

Regulatory Mandates and Demand for Legally Binding Electronic Transactions

Regulatory frameworks globally particularly the EU eIDAS (Electronic Identification, Authentication and Trust Services) Regulation No. 910/2014 and emerging state-level data privacy laws in North America are mandating Qualified Electronic Signatures (QES) for high-value contracts, regulated transactions, and cross-border agreements, creating structural demand for advanced digital signature capabilities.

QES, which carries the same legal weight as handwritten signatures under eIDAS and is automatically recognized across all EU member states, is required for financial instruments, employment contracts with non-compete clauses, loan agreements, and government transactions, establishing digital signatures as regulatory infrastructure rather than discretionary capability. Organizations operating in the BFSI sector report 100% legal requirement for digital signatures in derivatives trading, payment settlement, and regulatory filings, while healthcare organizations increasingly mandate digital signatures for HIPAA-compliant document management and 21 CFR Part 11-regulated pharmaceutical processes.

Acceleration of Remote Work, Mobile Adoption, and Paperless Transformation

The permanent shift toward distributed workforces, hybrid operating models, and mobile-first business processes is driving explosive adoption of digital signature solutions that enable secure document execution from any location, device, or time zone without requiring physical presence. Organizations report that remote work adoption increased from 16% of employees in 2019 to 35% in 2024, with expectations for hybrid arrangements exceeding 60% by 2027, directly creating infrastructure demand for digital signature platforms supporting asynchronous, geographically distributed transaction workflows. Paperless transformation initiatives, motivated by cost reduction, environmental sustainability goals, and operational efficiency, are creating powerful tailwinds for digital signature vendors, with organizations reporting 40–60% cost savings through the elimination of printing, shipping, storage, and retrieval expenses associated with paper-based processes. Mobile device proliferation and the normalization of mobile-first transaction models are enabling seamless digital signature experiences through smartphones and tablets, with mobile-based signing solutions experiencing 45% CAGR and representing a critical growth vector for vendors like DocuSign, Adobe, and SIGNiX.

Market Restraints

Legacy IT Infrastructure Integration Complexity and Interoperability Challenges

Organizations confronting legacy enterprise resource planning systems, fragmented document management ecosystems, and heterogeneous technology stacks face substantial integration complexity when deploying comprehensive digital signature solutions, creating implementation delays and increased total cost of ownership. Interoperability challenges among different digital signature providers, varying regulatory frameworks across jurisdictions, and complexities in certificate management across multiple trust service providers create technical barriers that constrain rapid market adoption. Small and mid-sized organizations particularly struggle with integration complexity, specialized IT expertise requirements, and challenges in implementing qualified electronic signature infrastructure that requires interaction with Qualified Trust Service Providers (QTSPs) and certificate authorities, limiting addressable market penetration in certain customer segments.

Cybersecurity Risks, Certificate Fraud, and Trust Infrastructure Vulnerabilities

High-profile incidents involving compromised digital certificates, stolen signing credentials, and sophisticated attacks targeting digital signature infrastructure create organizational hesitation regarding adoption, particularly among risk-averse institutions in BFSI and regulated healthcare environments. The Qualified Electronic Signature infrastructure, while offering superior legal certainty, introduces dependencies on Qualified Trust Service Providers (QTSPs), certificate authorities, and public key infrastructure components, which can create potential systemic vulnerabilities. Organizations report concerns regarding the cybersecurity posture of trust service providers, certificate revocation mechanisms, and long-term archival of digitally signed documents in formats ensuring sustained accessibility and legal validity across technology generations, creating perceived risks that slow adoption in highly regulated verticals.

Market Opportunities

Expansion into Emerging Markets and Government Digitalization Initiatives

Governments in emerging markets, including India, China, Brazil, Mexico, Indonesia, and the Philippines, are implementing large-scale digitalization initiatives mandating digital signatures in public sector procurement, licensing, property registration, and benefit administration, creating massive addressable market opportunities. India's eSign framework and mandates under the Information Technology Act are driving rapid adoption in government services, property transactions, and compliance documentation, making it one of the fastest-growing regional markets with the potential to exceed a 40% CAGR through 2033. China's multi-billion-dollar digital government initiative is similarly driving substantial infrastructure investments in digital signature solutions, with domestic providers like Weisign and international vendors competing aggressively for market share.

AI Integration, Biometric Authentication, and Advanced Signature Technologies

Artificial intelligence-powered document analysis, biometric authentication integration, and advanced cryptographic techniques, including blockchain-based signature verification, represent transformational opportunities creating premium product tiers and differentiated vendor positioning. Leading providers, including DocuSign, Adobe, and emerging vendors, are integrating generative AI to automate document analysis, verify contract compliance, and enable intelligent workflow automation, dramatically enhancing security and the user experience. Biometric authentication, including facial recognition, fingerprint verification, and voice analysis, is being integrated into digital signature platforms to provide multi-factor authentication and enhanced identity assurance, particularly valuable for Qualified Electronic Signature implementations and high-value transactions requiring stringent non-repudiation guarantees.

Category wise Insights

Type of Level Analysis

Advanced electronic signatures (AES) currently dominate the Digital Signature Market, accounting for an estimated 52% of global revenue, driven by a balance between regulatory recognition, implementation accessibility, and cost-effectiveness compared to Qualified Electronic Signatures (QES). AES, verified through signature creation device validation and advanced authentication mechanisms but not requiring Qualified Trust Service Provider certification, offers sufficient legal certainty for most enterprise use cases while maintaining substantially lower infrastructure complexity and operational costs than QES implementations. Qualified Electronic Signatures (QES), commanding the remaining 45–48% of market revenue, are experiencing the fastest growth at 35% CAGR, driven by increasing regulatory mandates in the BFSI and government sectors, cross-border transaction requirements under eIDAS, and risk-averse industries prioritizing maximum legal certainty.

Component Analysis

Solutions, encompassing digital signature software platforms, cloud-based signing systems, and cryptographic infrastructure, command the dominant position, accounting for approximately 57% of market revenue, reflecting strong demand for comprehensive signing platforms offering integration, workflow automation, and audit capabilities. Enterprise-focused solutions from DocuSign, Adobe Acrobat Sign, SIGNiX, and OneSpan dominate this segment, with DocuSign alone serving 1 billion users across 1.7 million customers and commanding approximately 30% market share among solution providers. Services, including implementation consulting, integration services, training, managed services, and support, represent approximately 40% of market value and are expanding at a 35% CAGR, driven by increasing demand for white-glove implementation support, workflow optimization, and managed service models that enable organizations to outsource digital signature infrastructure operations.

End-User Analysis

Businesses constitute the dominant end-user segment, commanding approximately 65–68% of the digital signature market demand, encompassing enterprises across all industry verticals leveraging digital signatures for internal document execution, supplier agreements, customer contracts, and regulatory compliance. Organizations, including government agencies, educational institutions, and non-profit entities, account for approximately 20–23% of demand, driven by digitalization initiatives, regulatory compliance requirements, and cost-reduction objectives related to document processing and storage. Individuals represent the emerging segment, accounting for roughly 9% of market adoption, driven by growing mobile-first digital signature applications, remote notarization requirements, and personal document authentication needs, with particularly strong growth in real estate transactions, property sales, and individual legal documentation requiring verified electronic signatures.

Industry Vertical Analysis

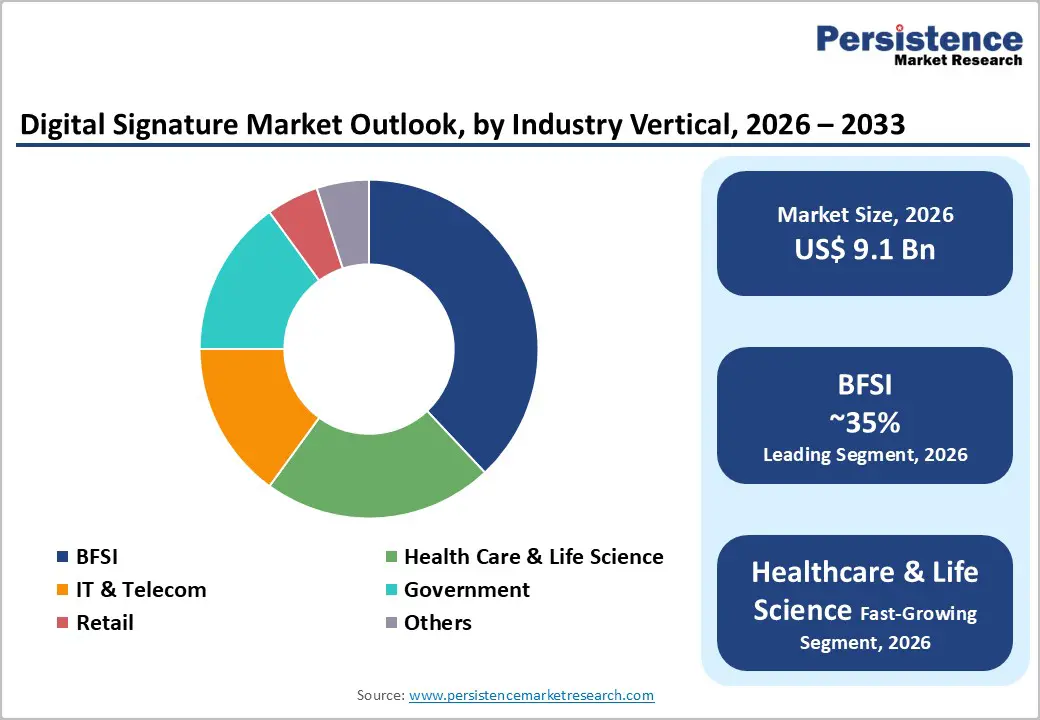

BFSI (Banking, Financial Services, and Insurance) dominates the industry vertical classification, accounting for an estimated 38% of Digital Signature Market revenue, driven by regulatory mandates including KYC (Know Your Customer) requirements, AML (Anti-Money Laundering) regulations, derivatives trading settlement, and digital onboarding processes requiring cryptographically secured, legally binding signatures. Healthcare & Life Science represents the second-largest vertical at approximately 25%, driven by HIPAA compliance requirements, regulatory mandates for Qualified Electronic Signatures in prescription distribution and clinical trial documentation, and 21 CFR Part 11 pharmaceutical compliance necessitating tamper-proof document authentication. IT & Telecom, Government, Retail, and Other verticals collectively account for 34% of demand, each driven by distinct regulatory, operational, and risk-management imperatives toward comprehensive digital signature adoption across internal and customer-facing processes.

Regional Insights

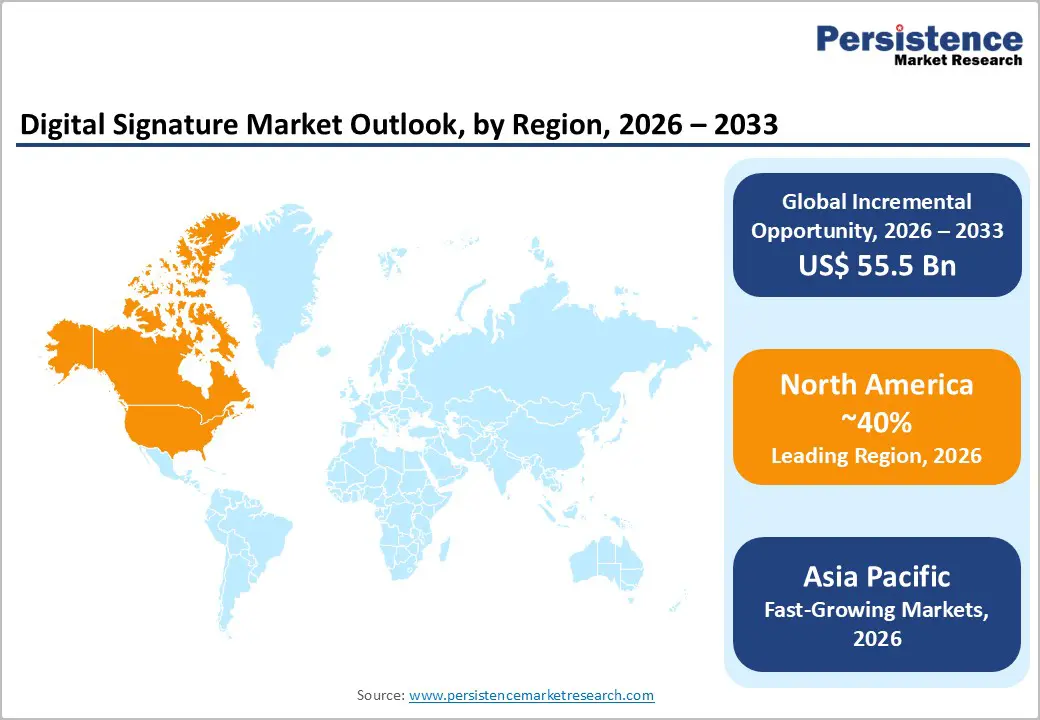

North America Digital Signature Market Trends

North America, led by the United States, commands the largest regional market share of the Digital Signature Market, accounting for approximately 40% of global revenue, anchored by concentration of major BFSI institutions, advanced technology sector participants, stringent regulatory frameworks including HIPAA, SOX, SEC regulations, and early adoption of digital transformation technologies. The U.S. digital signature market, estimated at approximately US$ 3.8 billion in 2026, is projected to expand at a CAGR of 30%, driven by permanent remote work adoption, accelerating digitalization in financial services, healthcare compliance mandates, and substantial investments by leading technology companies including DocuSign, Adobe, and emerging vendors.

The region features a mature, competitive digital signature ecosystem with established vendor relationships, robust implementation expertise, and strong regulatory tailwinds supporting sustained market expansion. U.S. government agencies, driven by digital government transformation initiatives, federal remote work mandates, and modernization of legacy systems, are increasingly adopting enterprise digital signature solutions for inter-agency collaboration, regulatory filings, and public-facing services.

Europe Digital Signature Market Trends

Europe is experiencing explosive growth in digital signature adoption, driven by the EU eIDAS (Electronic Identification, Authentication and Trust Services) Regulation No. 910/2014, which establishes unified standards for Qualified Electronic Signatures (QES) and ensures legal recognition across all 27 member states of the European Union. Key economies including Germany, the U.K., France, Spain, and Netherlands are driving market expansion through mandatory adoption of QES in government services, regulated industry transactions, and cross-border business processes.

European organizations demonstrate sophistication regarding digital signature compliance, with stringent requirements for eIDAS-certified solutions, integration with national eID infrastructure, and adherence to GDPR data protection and privacy standards. The region's regulatory harmonization creates substantial demand for vendors offering multi-jurisdictional QES support, integration with diverse national eID systems, and compliance with evolving EU directives around digital identity, trust services, and electronic transaction standards, positioning vendors with strong European regulatory expertise and partnerships with Qualified Trust Service Providers for sustained competitive advantage.

Asia Pacific Digital Signature Market Trends

Asia Pacific is the fastest-growing regional market for digital signatures, projected to expand at CAGR exceeding 30% through 2033, driven by rapid government digitalization initiatives, exploding e-commerce adoption, and escalating demand for secure electronic transaction infrastructure across China, India, Japan, and emerging ASEAN economies. India's digitalization agenda, supported by government mandates for digital signatures under the Information Technology (Reasonable Security Practices and Procedures and Sensitive Personal Data or Information) Rules, Aadhar digital identity infrastructure integration, and property transaction digitalization, is creating substantial market opportunities for vendors developing Aadhar-compatible digital signature solutions.

Japan, with mature regulatory frameworks and high technology adoption, is increasingly mandating Qualified Electronic Signatures for government services, financial transactions, and notary functions, supporting steady market expansion. Emerging ASEAN economies, including Indonesia, Vietnam, the Philippines, and Thailand, are implementing government digitalization initiatives that represent substantial emerging market opportunities as regulations mandate digital signatures in administrative processes, licensing, and business registration.

Competitive Landscape

The digital signature market is moderately consolidated, with DocuSign commanding approximately 30% global market share, followed by Adobe (through Acrobat Sign), OneSpan, SIGNiX, and regional leaders including GlobalSign, PrimeKey AB, Visma, and emerging vendors. Market leaders differentiate through comprehensive solution portfolios spanning solutions and managed services; breadth of integrations with enterprise systems, cloud platforms, and CRM solutions; advanced security capabilities, including biometric authentication and fraud detection; and proven compliance with eIDAS QES, HIPAA, 21 CFR Part 11, and industry-specific regulatory frameworks. Strategic consolidation has accelerated, with Adobe's acquisition of EchoSign, OneSpan's platform expansions, and emerging vendors building specialized solutions for healthcare, government, and emerging markets.

Key Market Developments

- In March 2025, DocuSign, Inc., engaged in a strategic partnership with Algebrik AI. Through this collaboration, DocuSign would integrate its e-signature and agreement automation capabilities into Algebrik AI’s platform to enable seamless loan origination workflows and enhance customer experience.

- In July 2024, Protean eGov Technologies Ltd launched eSignPro, an electronic signature tool. It is enabled with an enterprise-grade full-stack smart documentation and automation suite that helps organizations with the ease of doing business.

Companies Covered in Digital Signature Market

- Docusign, Inc.

- SIGNiX, Inc.

- Adobe Inc.

- OneSpan Inc.

- GlobalSign

- IdenTrust, Inc.

- PrimeKey AB

- Visma

- Ascertia

- Topaz Systems, Inc.

- Entrust Corporation

- Other Key Players

Frequently Asked Questions

The global Digital Signature Market is projected to reach approximately US$ 64.9 billion by 2033, expanding from US$ 9.1 billion in 2026, at a compound annual growth rate (CAGR) of 32.4% between 2026 and 2033.

Key demand drivers include regulatory mandates requiring Qualified Electronic Signatures (QES) under the EU eIDAS Regulation, accelerating remote work and distributed workforce adoption, government digitalization initiatives across emerging markets, digital transformation imperatives, cost reduction through paperless processes, and escalating cybersecurity and fraud prevention requirements.

Advanced Electronic Signatures (AES) currently lead the market with approximately 52% market share, though Qualified Electronic Signatures (QES) represent the fastest‑growing segment at 35% CAGR, driven by increasing regulatory mandates and high‑value transaction requirements in regulated industries.

North America, particularly the United States, dominates the global Digital Signature Market with approximately 40% of worldwide revenue, driven by large financial services sector, advanced technology adoption, stringent regulatory requirements, and concentration of major digital signature vendors and enterprise adoption.

Major players include DocuSign, Inc. Adobe Inc., OneSpan Inc. SIGNiX, Inc., GlobalSign, IdenTrust, Inc., PrimeKey AB, Visma, and Weisign.