- Semiconductor Materials & Components

- Digital Shipyard Market

Digital Shipyard Market Size, Share, and Growth Forecast, 2026 - 2033

Digital Shipyard Market by Ship Type (Commercial Vessels, Naval Vessels, and Offshore Vessels), Technology (Digital Twin & Simulation, Artificial Intelligence & Advanced Analytics, Industrial Internet of Things (IIoT), Cloud Computing & Data Management, Robotics & Automation, and Misc.), Application (Ship Design & Engineering, Construction Management & Manufacturing Planning, Maintenance, Repair & Support) and Regional Analysis for 2026 - 2033

Digital Shipyard Market Size and Trends Analysis

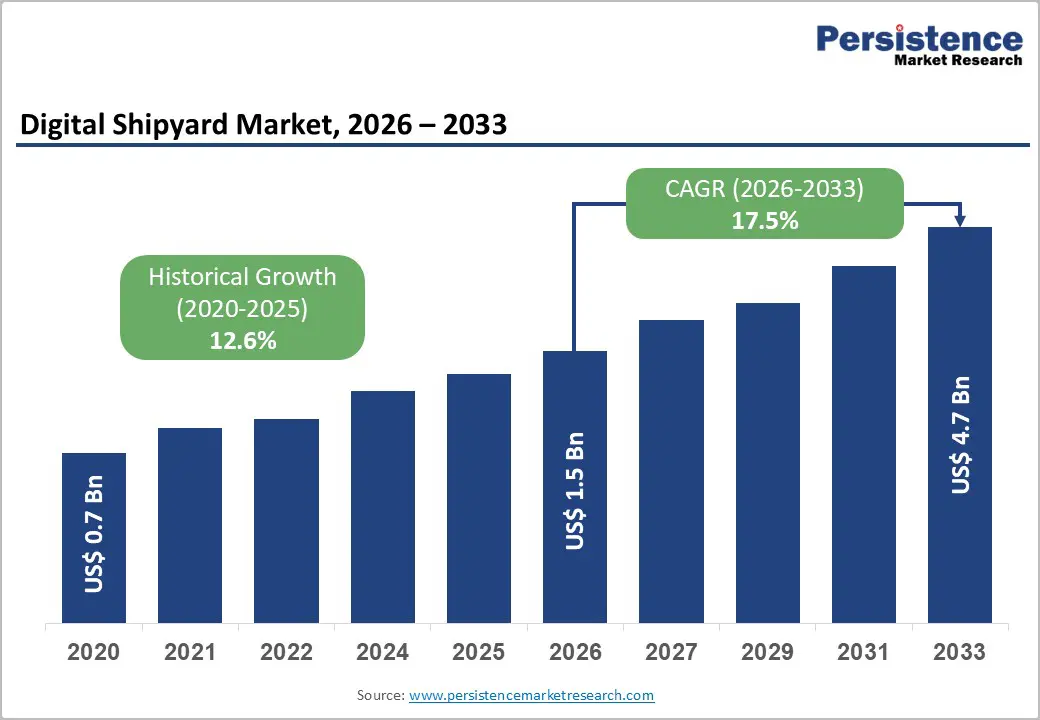

The global digital shipyard market size is likely to be valued at US$1.5 billion in 2026 and is projected to reach US$4.7 billion by 2033, growing at a CAGR of 17.5% between 2026 and 2033. This acceleration from the historical CAGR of 12.6% reflects intensifying demand for digital transformation across global shipbuilding operations.

The market expansion is driven by three primary catalysts: the urgent necessity to address skilled labour shortages, mounting pressure to reduce production costs and timelines, and the rise in regulatory requirements for environmental compliance and defense modernization.

More than 68% of global shipbuilders have adopted digital transformation strategies, and 72% report measurable productivity improvements following digital twin implementation. The market's strategic importance extends beyond shipbuilding efficiency; it now serves as a critical enabler for naval modernisation programs across NATO nations and supports the transition toward autonomous, sustainable vessels equipped with alternative-fuel systems.

Key Industry Highlights:

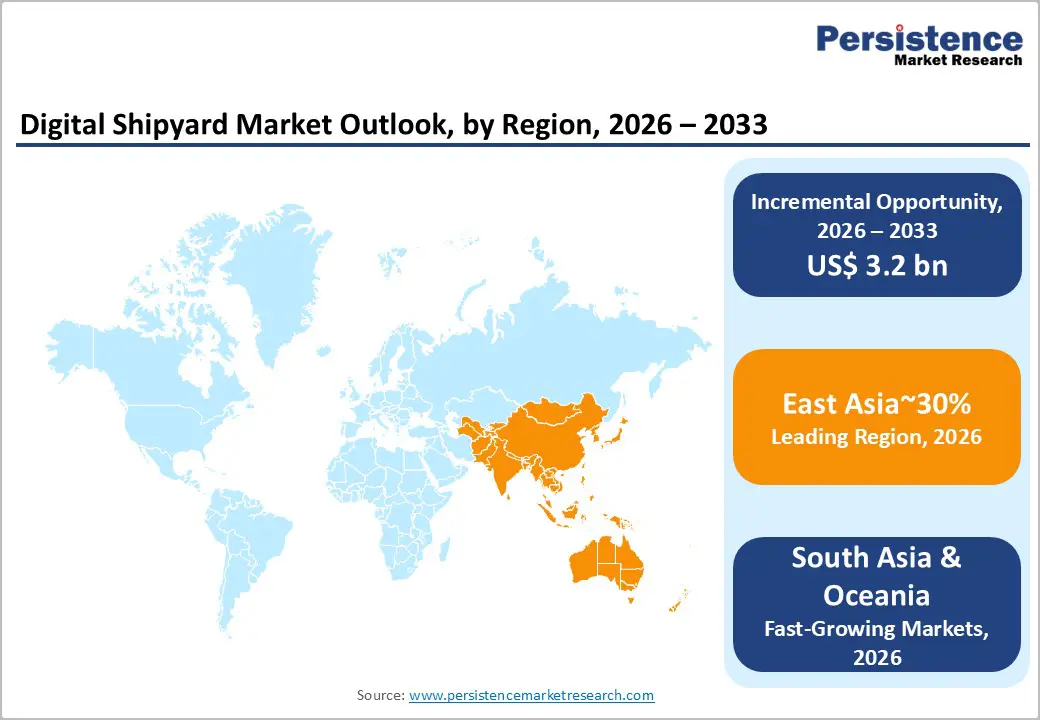

- Regional Leadership: East Asia leads the global digital shipyard market with ~30% share, driven by South Korea and China’s dominance in commercial shipbuilding, large-scale LNG carrier production, and aggressive deployment of digital twins, automation, and AI-enabled shipyard platforms.

- Fast-growing Market: Europe accounts for ~23% of the market, driven by rising defence budgets, the EDINAF program, and strong adoption of digital shipyard platforms for naval and specialised vessel construction.

- Leading Ship Type: Commercial vessels dominate the market, reflecting high-volume construction of container ships, tankers, and LNG carriers, where digital shipyards deliver cost control, schedule reliability, and productivity gains.

- Fastest-Growing Ship Type: Naval vessels represent the fastest-growing segment, driven by defence modernisation, digital continuity requirements, and secure lifecycle management mandates.

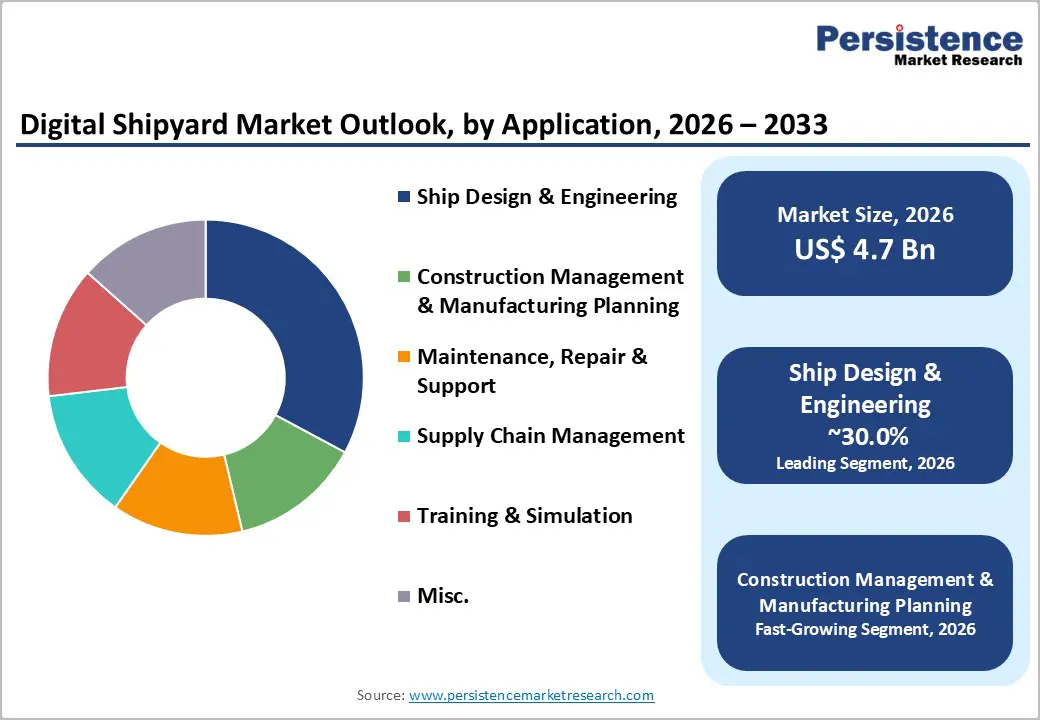

- Key Application Leader: Ship Design & Engineering leads the market, as digital twins, MBSE, and AI-driven optimisation significantly reduce design cycles and downstream construction risk.

| Key Insights | Details |

|---|---|

| Digital Shipyard Market Size (2026E) | US$ 1.5 Bn |

| Market Value Forecast (2033F) | US$ 4.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 17.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 12.6% |

Market Dynamics

Drivers - Workforce Capacity Constraints and Labour Productivity Imperatives

The global shipbuilding sector confronts acute demographic challenges stemming from an ageing workforce and diminishing interest in skilled maritime trades. Shipyards face critical labour shortages precisely when vessel complexity has increased, requiring integration of advanced propulsion systems, automated controls, and hybrid energy platforms. Digital shipyard technologies directly address this challenge through automation, predictive analytics, and workforce augmentation tools.

The implementation of digital twins, automated welding systems, and AI-driven quality assurance enables shipyards to accomplish complex construction tasks with reduced manual intervention while simultaneously improving structural precision. Real-time monitoring systems powered by Internet of Things (IoT) sensors provide immediate feedback on production status, enabling supervisors to optimise labour allocation and identify bottlenecks before they cascade into delays.

Augmented reality (AR) systems guide workers through complex assembly sequences, effectively transferring knowledge from experienced craftspeople to newer personnel. In the Digital Shipyard Market, these technologies represent not merely cost-reduction mechanisms but essential infrastructure for maintaining production capacity amid demographic transition.

Regulatory Mandates for Defense Modernization and Naval Fleet Renewal

Defence budgets across developed economies are undergoing structural expansion, with 16 of 23 NATO members now allocating 2% or more of gross domestic product toward military procurement, double the number from 2014. This geopolitical recalibration has directly translated into record defence-industrial investments in naval modernisation. The European aerospace and defence industry recorded €325.7 billion in total turnover in 2024, representing a 10.1% year-on-year increase, with defence-specific segments expanding by 13.8%.

The United States maintains similarly robust defense spending, with the aerospace and defence sector generating $995 billion in total business activity in 2024 and supporting 2.2 million workers. These investments mandate integration of advanced digital infrastructure into naval shipyards. Government contracts now explicitly require model-based systems engineering (MBSE), digital continuity across vessel lifecycles, and secure collaborative environments, thereby effectively mandating digital shipyard platforms.

The EDINAF project, funded by the European Defence Fund and involving 31 partners across eight countries, exemplifies this regulatory trajectory, establishing unified digital architectures for future European military vessels. Digital shipyard adoption in the Global Digital Shipyard Market has become a compliance requirement rather than an optional optimisation, driving sustainable demand regardless of commercial shipping cycles.

Restraint - Capital Investment Requirements and Technology Integration Complexity

Implementing enterprise-grade digital shipyard platforms requires substantial capital expenditure spanning software licensing, hardware infrastructure, cybersecurity frameworks, and workforce retraining programs. For large yards operating multiple production lines, system integration costs frequently exceed US$50-100 million, with implementation timelines spanning 2-3 years.

Mid-size and regional shipyards often lack the internal IT expertise required for platform deployment and ongoing optimisation, necessitating expensive consulting and systems integration services. The technical risk of incompatibility between legacy manufacturing systems, enterprise resource planning (ERP) infrastructure, and new digital platforms create organizational friction and project delays. Furthermore, return on investment timelines stretch across 5-7 years for commercial shipyards and extend further when accounting for uncertain utilisation rates in cyclical shipping markets.

These capital barriers effectively exclude smaller yards and developing-market shipyards from adopting comprehensive digital ecosystems, fragmenting the market and limiting addressable customer bases for software vendors.

Opportunity - Autonomous and Unmanned Vessel Development Ecosystem

The convergence of autonomous navigation systems, advanced sensor suites, and edge artificial intelligence is catalyzing development of unmanned surface vessels and autonomous cargo carriers. Regulatory frameworks are evolving to permit autonomous operation in controlled environments such as inland waterways and coastal shipping corridors, with expectations for expanded autonomy in international waters within the 2028-2032 timeframe.

The Digital shipyard market constitutes essential infrastructure for autonomous vessel development, providing digital twins for navigation-algorithm testing, virtual-reality environments for remote operator training, and integrated design platforms that accommodate novel sensors and propulsion architectures.

India has launched its first autonomous vessel development project ("Swayat") through a partnership involving the Indian Register of Shipping and Cochin Shipyard, establishing regulatory precedent and building domestic expertise in autonomous maritime systems. These initiatives expand the addressable market beyond traditional shipyard operations toward specialised vessel design and construction, particularly in emerging maritime economies investing in autonomous cargo and offshore support vessels.

Decarbonization and Alternative Fuel Propulsion Architecture Integration

Global maritime decarbonization initiatives, including the International Maritime Organisation's 2050 net-zero emissions target and increasingly stringent regional emission-control regulations, mandate vessel designs that incorporate alternative fuel systems (LNG, ammonia, hydrogen, biofuels) and advanced energy-efficiency technologies. These propulsion system transitions require integration of novel engine architectures, heat recovery systems, energy storage components, and propulsion management electronics spanning multiple engineering disciplines and subcontractors.

Digital shipyard platforms enable integrated design optimisation across thermal, propulsive, structural, and control systems, thereby accelerating the development of commercially viable alternative-fuel vessels while managing complexity and cost. Samsung Heavy Industries' collaboration with Dassault Systèmes explicitly targets design optimisation of next-generation LNG carriers and alternative-fuel vessels through advanced model-based systems engineering.

The regulatory timeline for compliance creates sustained, multi-year demand across Asia-Pacific and European shipyards serving global shipping fleets. India's announced investment of INR 47,800 crore in new shipbuilding orders, aligned with the objectives of Maritime India Vision 2030, explicitly prioritizes modernization toward advanced, digitally enabled vessels capable of meeting decarbonization standards. These structural regulatory requirements translate into durable market demand that is independent of shipping-cycle dynamics.

Category-wise Analysis

Ship Type Insights

Commercial Vessels command 40.0% market share in 2026, representing the dominant segment by revenue volume. This leadership position reflects the sheer scale of global commercial shipping operations encompassing container ships, bulk carriers, tankers, LNG carriers, and specialised vessels serving petrochemical and offshore industries. Commercial shipyards operate on compressed margins, creating intense pressure to adopt efficient technologies that reduce construction timelines, material waste, and rework costs.

Digital shipyard solutions enable commercial yards to optimize labor utilization, reduce scheduling risk, and improve cost predictability, thereby enhancing competitiveness and profitability. The cyclical nature of commercial shipping markets creates volatility in order volumes, making digital platforms valuable for rapidly scaling production during demand upswings while managing capacity efficiently during downturns.

Large integrated shipyards, including South Korean yards companies such as Samsung, Hyundai, DSME) Dominant LNG carrier construction by Chinese yards, leading container ship production by Chinese yards, and European yards specialising in specialised commercial vessels are accelerating digital platform investments to maintain technological leadership. The commercial segment's large volume and competitive intensity will sustain market growth in the Digital Shipyard Market throughout the forecast period.

Naval Vessels represent the fastest-growing segment within the Digital Shipyard Market, driven by defence budget expansion and naval modernisation programs across developed economies. Military shipbuilding operates under fundamentally different economic and technical constraints than commercial shipbuilding.

End Use Industry Insights

Ship Design & Engineering holds 30.0% market share in 2026, representing the foundational application segment within the Digital Shipyard Market. This dominance reflects the strategic importance of design optimisation in determining downstream manufacturing costs, quality outcomes, and vessel operational performance. Advanced design platforms that integrate 3D parametric modelling, clash detection, structural analysis, hydrodynamic simulation, and integrated cost estimation enable shipyards to reduce design cycles from 12-18 months to 6-9 months while improving design quality and manufacturability.

The convergence of MBSE methodologies, digital twin technologies, and AI-driven design optimisation makes sophisticated design capabilities accessible to smaller yards previously dependent on expensive external engineering consulting. Leading software providers, including AVEVA Hull & Outfitting, NAPA design environments, CADMATIC integrated platforms, and Dassault Systèmes 3DEXPERIENCE platform, collectively serve this segment through cloud-based and on-premises deployment options.

Construction Management & Manufacturing Planning is the fastest-growing application segment in the digital shipyard market, driven by acute labor productivity challenges and pressure to compress on-yard construction timelines. Manufacturing execution systems, production planning optimisation algorithms, and real-time workshop monitoring platforms enable shipyards to achieve structural improvements in schedule adherence, resource utilisation, and quality outcomes.

Regional Insights

North America Digital Shipyard Market Trends

North America accounts for 27% of the global digital shipyard market, positioning the region as a major investment and deployment centre, driven by U.S. naval modernisation and commercial shipyard modernisation initiatives. The U.S. government's explicit focus on maintaining technological superiority in naval capabilities against great-power competitors has led to record defence investments.

The Navy's Columbia-class submarine program, Gerald R. Ford-class carrier continuity, and destroyer production programs collectively represent multi-trillion-dollar commitments that explicitly incorporate digital infrastructure as a foundational requirement. Private shipbuilders serving the U.S. Navy, Huntington Ingalls, General Dynamics Bath Iron Works, and Austal, are simultaneously modernising facilities with advanced digital technologies and automation systems. The U.S. Coast Guard's modernisation initiatives and commercial shipbuilding for specialised vessels add secondary demand drivers within the region.

Commercial shipyard modernisation in North America is accelerating as operators confront extreme labour productivity pressures and compressed margins. U.S. shipyards have lost substantial commercial vessel construction market share to Asian competitors over the past two decades, but recent policy initiatives, including domestic vessel construction incentives and protectionist policies, are catalyzing investment in digitalisation to improve competitiveness. Strategic partnerships between international shipbuilding leaders and U.S. yards exemplify this dynamic: HD Hyundai's partnership with Vigour Marine Repair and integration of Samsung Heavy Industries' digital shipyard expertise into U.S. operations represent direct technology transfer and capability building.

East Asia Digital Shipyard Market Trends

East Asia dominates the digital shipyard market with a 30% global market share, establishing the region as the primary growth engine, driven by South Korea and China's combined dominance in global commercial shipbuilding and by advancing naval modernisation programs. South Korea's three major shipbuilders, Samsung Heavy Industries, HD Hyundai Heavy Industries (including Mipo and Samho subsidiaries), and Daewoo Shipbuilding & Marine Engineering collectively operate the world's most advanced shipyards and lead in LNG carrier, ultra-large container ship, and specialised vessel construction. These yards are aggressively deploying digital technologies to differentiate themselves.

Samsung Heavy Industries' partnership with Dassault Systèmes to implement a comprehensive 3DEXPERIENCE-based digital shipyard infrastructure demonstrates the strategic commitment to advanced digitalisation. HD Hyundai's integrated design-to-production digital platform development project, collaborating with Siemens, AVEVA, NAPA, and CADMATIC, targets full-scale deployment by 2028 as a foundational element of its Future of Shipyard vision. DSME's robotics programs, including the AI-powered "Goknuri" metalworking robot, exemplify the convergence of advanced manufacturing and digital intelligence.

China's shipbuilding sector, commanding 40% plus of global commercial vessel construction, is simultaneously pursuing digital modernisation despite slower public disclosure of technology initiatives. Government policy, through the 14th Five-Year Plan, explicitly mandates industrial digitalisation across advanced manufacturing sectors and provides sustained funding for digital infrastructure investments in shipyards.

Europe Digital Shipyard Market Trends

Europe commands 23% of the global digital shipyard market, with distinctive market characteristics that reflect a dominant naval and specialised vessel focus rather than commercial bulk production. The European aerospace and defence industry recorded €183.4 billion in defence-specific turnover in 2024, representing 13.8% year-on-year growth driven by geopolitical tensions and strategic autonomy priorities.

The EDINAF project, the European Defence Fund's flagship initiative defining a unified digital architecture for future European military vessels, represents the continent's strategic commitment to comprehensive digital transformation. This multi-year, 31-partner program spanning eight countries collectively establishes interoperable digital standards for European naval construction, creating market tailwinds for digital platform vendors serving military requirements.

European defence budgets are expanding structurally, with the EU's ReArm program mobilising €800 billion for defence procurement and mandating the integration of modern digital infrastructure. Commercial shipyard activity remains concentrated in specialised vessel categories where digital design optimisation and advanced manufacturing deliver meaningful competitive advantages.

Competitive Landscape

The global digital shipyard market is moderately consolidated, driven by a limited number of global technology providers and large shipbuilding groups that control a significant share of advanced digital platforms. Leading players focus on integrated solutions covering digital twins, PLM, AI-driven production planning, automation, and lifecycle management, creating high entry barriers for new participants. Siemens Digital Industries Software and Dassault Systèmes dominate the software layer through their Xcelerator and 3DEXPERIENCE platforms, widely adopted across commercial and naval shipyards.

Major shipbuilders such as HD Hyundai and Samsung Heavy Industries are key market leaders, actively deploying and co-developing smart digital shipyard ecosystems. Specialized maritime software providers, including NAPA and SSI (ShipConstructor Software Inc.), strengthen the competitive landscape with deep domain expertise in design and manufacturing workflows. Strategic partnerships between shipyards, software companies, and system integrators are intensifying, reinforcing consolidation while enabling continuous innovation.

Key Industry Developments:

- In Nov, 2025, HD Hyundai and Siemens signed a strategic MOU to modernise the U.S. shipbuilding industry through end-to-end digital shipyard transformation. The collaboration focuses on digital ship design, automation of block assembly, production optimisation, and quality enhancement using advanced digital platforms, alongside workforce training programs. This partnership accelerates the development of smart, fully integrated shipyards and reinforces global adoption of digital shipyard ecosystems.

- In August, 2025, Vigour Marine Group and Samsung Heavy Industries formed a strategic partnership to enhance U.S. shipbuilding and forward-deployed MRO capabilities. Leveraging SHI’s expertise in digital shipyard technology, automation, and advanced engineering, the collaboration aims to streamline repair operations, improve fleet readiness, and explore revitalisation of U.S. shipyards for new construction, strengthening the U.S. maritime industrial base and supporting Navy and Military Sealift Command operations in the Indo-Pacific.

Companies Covered in Digital Shipyard Market

- Siemens

- Dassault Systèmes

- Accenture

- SAP

- BAE Systems

- AVEVA Group plc (Schneider Electric SE)

- BAE Systems Plc

- IFS AB

- Inmarsat Global Limited (Viasat Inc.)

- Navantia

- Pemamek Oy Ltd.

- Wärtsilä Oyj Abp

Frequently Asked Questions

The global digital shipyard market is projected to be valued at US$ 1.5 Bn in 2026.

The Commercial Vessels Segment is expected to account for approximately 40% of the global Digital Shipyard Market by Ship Type in 2026.

The market is expected to witness a CAGR of 17.5% from 2026 to 2033.

The global digital shipyard market is being driven by acute workforce shortages, rising vessel complexity, and stringent defense modernization mandates, making digital twins, automation, AI, IoT, AR, and MBSE essential for sustaining productivity, regulatory compliance, and naval fleet renewal.

The global Digital Shipyard Market presents significant opportunities driven by autonomous vessel development and decarbonization mandates, as digital twins, AI-driven design, and integrated engineering platforms enable shipbuilders to support unmanned vessels and complex alternative-fuel propulsion systems while ensuring regulatory compliance and long-term sustainability.

The key players in the Digital Shipyard Market include Siemens Digital Industries Software, Dassault Systèmes, HD Hyundai, Samsung Heavy Industries, SSI (ShipConstructor Software Inc.), and NAPA.