- Medical Devices

- Dental Lights Market

Dental Lights Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

Dental Lights Market Product Type (LED, Halogen, Xenon), Mounting (Ceiling Mounted, Mobile, Wall Mounted), by End Use (Academic Institutes, Dental Clinics, Hospitals), Application (Examination, Operatory), and Regional Analysis for 2025 - 2032

Dental Lights Market Size and Trends Analysis

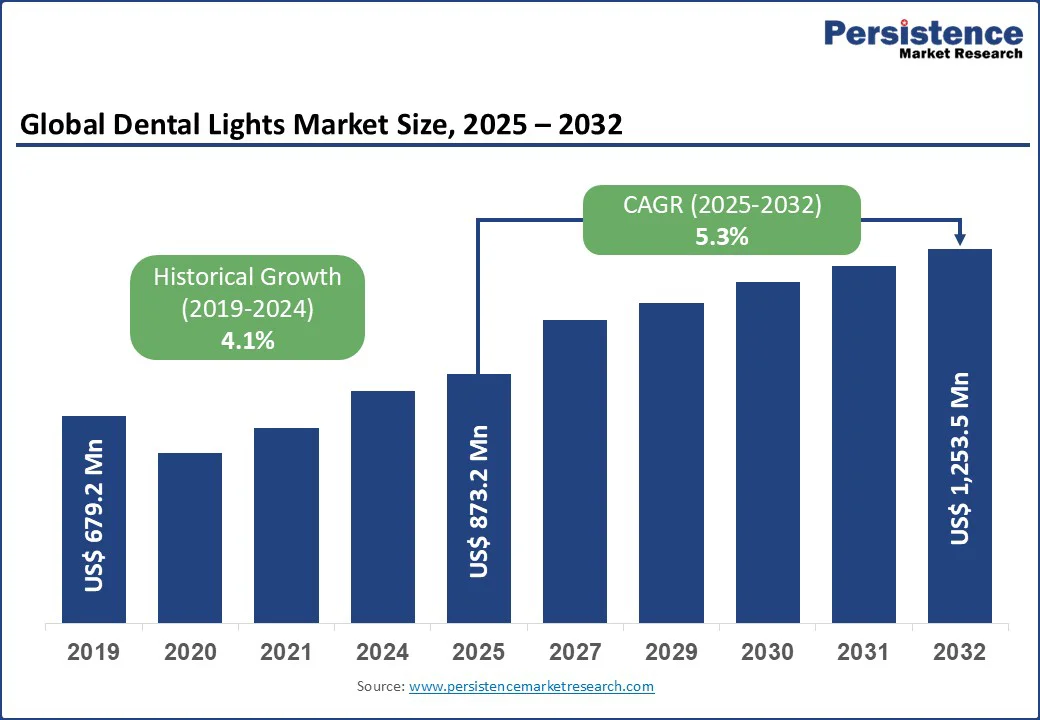

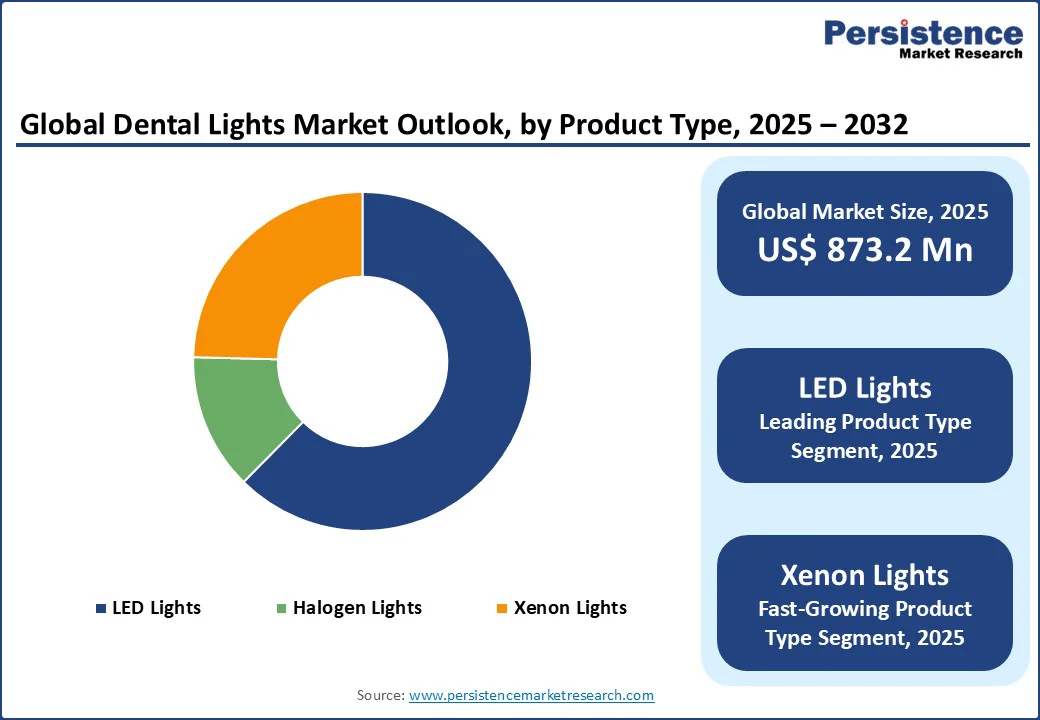

The dental lights market size is likely to be valued at US$ 873.2 Mn in 2025 and is expected to reach US$ 1,253.5 Mn in 2032, growing at a CAGR of 5.3% during the forecast period 2025 - 2032.

Key Industry Highlights

- Latest Research: Researchers at Griffith University investigated how the Nuralyte device improved mitochondrial respiration and stimulated gene expression in bone-forming stem cells. Results revealed that Nuralyte has the potential to change how dentists manage patients with pain and improve healing.

- Leading Product Type: LED lights hold nearly 62.4% share in 2025, owing to features such as long lifespan, low heat emission, and precise color.

- Dominant Mounting Type: Ceiling mounted lights, approximately 48.2% of the dental lights market share in 2025, as ergonomic installation saves chairside space and improves operator comfort.

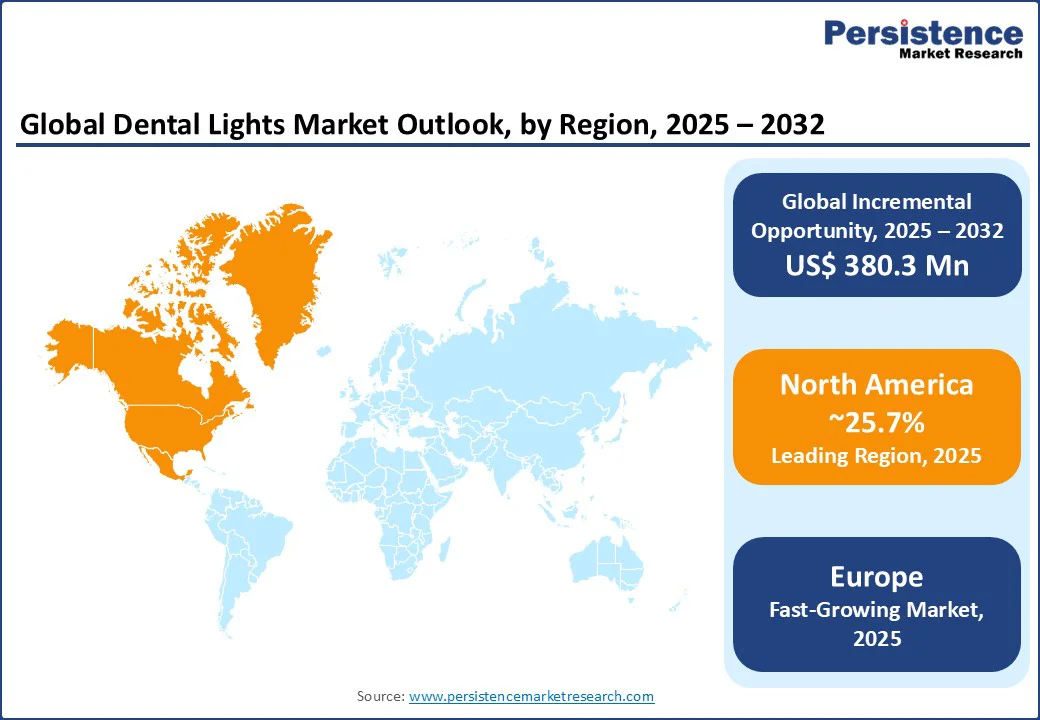

- Leading Region: North America with about 25.7% share in 2025, backed by increasing investments in dental service organizations.

- Fastest-growing Region: Europe, propelled by surging focus on sustainable and low-emission lighting systems.

| Global Market Attribute | Key Insights |

|---|---|

| Dental Lights Market Size (2025E) | US$ 873.2 Mn |

| Market Value Forecast (2032F) | US$ 1,253.5 Mn |

| Projected Growth (CAGR 2025 to 2032) | 5.3% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.1% |

The dental lights market growth is fueled by the global shift toward LED technology, sustainability mandates, and the rising number of cosmetic and restorative dental procedures.

Market Factors - Growth, Barrier, and Opportunity Analysis

Shift to LED and Wireless Technology Improves Dental Light Efficiency

The market is experiencing transformation, spurred by fast-paced technological developments and evolving regulations. The move from halogen to LED lights has gained momentum as manufacturers focus on improving energy efficiency, heat dissipation, and light output.

Novel COB LED arrays now deliver superior lumen intensity with more consistent illumination, while SMD LED setups provide versatile beam control and low-power use. At the same time, developments in wireless power and battery technology are making portable lighting solutions feasible. It allows smooth operations across multiple treatment rooms without compromising on brightness or performance.

International regulatory authorities have further implemented strict safety and performance requirements to ensure consistent operation in clinical settings. These updates focus on areas such as electromagnetic compatibility, heat management, and photobiological safety.

They help in encouraging manufacturers to integrate novel sensors and automated calibration systems. Additionally, linking dental lights with digital imaging tools and real-time analytics is creating new functional advantages. It is enabling clinicians to develop illumination according to specific procedures or patient requirements.

Excessive Blue Light Exposure and Heat from Curing Lights Raise Health Concerns

Concerns over health risks are affecting the adoption of dental lights, primarily regarding excessive blue light exposure. Prolonged or intense exposure often leads to eye strain or retinal damage for both dental professionals and patients, while sensitive skin may react to certain wavelengths. These risks make clinics more cautious about investing in high-intensity lighting without proper protective measures.

Heat generation during procedures, mainly with curing lights, also contributes to patient discomfort. If a light produces noticeable warmth, patients can experience irritation or anxiety, which tends to limit its use in time-consuming treatments. Manufacturers are responding with heat-reducing designs and protective shields. However, these challenges still slow adoption in clinics that prioritize patient comfort and safety.

Strategic Partnerships and Digital Integration Propel Competitive Positioning

Key players in the field of dental lights are actively pursuing strategic moves to strengthen their market presence and encourage collaboration. Several international manufacturers are broadening their product lines by teaming up with optics and electronics experts.

They are also incorporating specialized LED modules and sensor systems to stand out in terms of efficiency and safety. In addition, a few companies are forming joint ventures with clinical research institutions to test new features across varied dental procedures, speeding up product adoption.

Competition is increasing as manufacturers focus on digital integration and novel software solutions that support remote monitoring and predictive maintenance. By incorporating control panels and data-tracking functions into lighting systems, they are providing improved solutions that go beyond basic illumination. Leading companies are also broadening their expertise through strategic acquisitions of specialized lighting firms.

Category-wise Analysis

Product Type Insights

By product type, the market is divided into LED, halogen, and xenon lights. Among these, LED lights are speculated to record nearly 62.4% of share in 2025 owing to their superior energy efficiency and longevity compared to traditional halogen or xenon lights.

They consume less power while producing bright and consistent illumination, which lowers heat generation and improves patient comfort during procedures. Modern LED lights allow adjustable beam shapes, intensity, and color temperature, thereby enabling dentists to customize lighting for specific procedures.

Xenon dental lights are gaining impetus as they provide exceptionally bright, white light that closely mimics natural daylight. This feature helps in improving visibility and color accuracy during procedures. It makes them ideal for precise restorative and cosmetic dental work where distinguishing subtle shades is important. Another factor bolstering their adoption is the instant-on capability and stable light output of xenon bulbs. This eliminates warm-up time and ensures consistent illumination throughout long procedures.

Mounting Insights

Based on mounting, the market is trifurcated into ceiling mounted, mobile, and wall mounted. Out of these, ceiling mounted dental lights are expected to hold around 48.2% of share in 2025 as they provide superior flexibility and coverage without cluttering the operatory space.

By being suspended above the treatment area, they can be easily positioned and angled to illuminate specific regions of the mouth. These lights also reduce shadows and provide uniform illumination, which is important for restorative, cosmetic, and surgical treatments. Modern ceiling-mounted lights often come with adjustable arm lengths, multi-joint articulation, and LED technology.

Mobile dental lights are gaining popularity owing to their ability to provide unmatched flexibility in modern dental clinics. Unlike fixed ceiling or wall-mounted systems, mobile units can be easily repositioned across multiple operatories. This makes them ideal for practices with limited space or shared treatment rooms.

These lights also support multi-functional workflows as they can be used for both general dentistry and specialized procedures without requiring separate installations. Recent models, including those from Midmark and Planmeca, incorporate battery operation and wireless controls to enable clinicians to move them freely.

Regional Insights

North America Dental Lights Market Trends- New U.S. Tariffs Compel Manufacturers to Rethink Sourcing Strategies

In 2025, North America is predicted to account for approximately 25.7% of share owing to the surging adoption of LED dental lights due to benefits such as energy efficiency and reduced heat emission. In the same year, new tariff measures implemented by the U.S. added layers of complexity to the international trade of dental lighting equipment.

These duties applied to both imported components and fully assembled units. It further increased landed costs for specific halogen and xenon products, leading procurement teams to reconsider their sourcing strategies.

To cope, manufacturers targeting the U.S. dental lights market have diversified their supply chains, relocated assembly operations closer to end markets, and adjusted pricing structures to protect profit margins. The tariff changes have also prompted companies to rethink vertical integration strategies.

Several companies are partnering with domestic suppliers capable of producing essential optical and electronic parts. At the same time, some overseas vendors are using bonded warehouses to hedge against tariff volatility while maintaining reliable delivery timelines.

Europe Dental Lights Market Trends- Phase-out of Fluorescent Lamps Boosts Shift toward Full-spectrum LEDs

In Europe, dental light manufacturing companies are striving to manage two important regulatory areas, namely, Medical Device Regulation (MDR) and stringent energy-efficiency mandates. With the introduction of EU MDR, devices that previously qualified under old frameworks now require full re-certification.

This applies even to well-known dental lighting systems, compelling manufacturers to conduct comprehensive documentation overhauls, reinforce risk assessments, and improve post-market surveillance systems.

MDR imposes new expectations such as clearly defined regulatory roles across firms, unique device identifiers for traceability, and frequent audits from notified bodies. These often compel producers to upgrade internal processes and technical data structures.

On the energy front, the EU has phased out fluorescent lamps from dental use altogether. Hence, clinics must shift to full-spectrum LEDs. Recent updates under the Ecodesign Directive and Energy Labelling regulations now mandate that lighting products sold in the EU meet minimum efficiency thresholds.

Asia Pacific Dental Lights Market Trends- Wireless LED and Micro-LED Technologies Gain Traction in New Clinics

Asia Pacific is emerging as a key market for dental lights due to booming dental tourism, rising middle-class demand for cosmetic and general dentistry, and investments in dental infrastructure. Private clinics dominate India and China as patients often pay out-of-pocket and clinics prefer compact, battery-powered, or portable lights.

Asia Pacific is also witnessing the adoption of wireless LED and micro-LED lights, specifically in new clinics where flexibility and energy efficiency are priorities.

Smart lighting features are increasingly embraced. Adaptive brightness, touchless or gesture control, and AI-enabled functions are entering the market. LED lights are becoming the preferred choice in the region as they are energy efficient, produce less heat, and have flexible designs suitable for different procedures.

At the same time, access is uneven across Asia Pacific. Urban clinics in metro cities are quick to adopt novel lighting, while rural areas still struggle with high upfront costs.

Competitive Landscape

The dental lights market consists of both established players and emerging companies vying for high share. This competition often leads to price pressures, primarily for commodity-type LED lights. Manufacturers must constantly experiment and deliver differentiated value propositions to maintain profitability and market position.

Leading companies such as Dentsply Sirona Inc. and Danaher Corporation are focusing on technological developments, strategic partnerships, and targeted product development initiatives to strengthen their position.

Key Industry Developments

- In February 2025, Royal Philips collaborated with Tend, an in-demand full service dental practice, to bring Philips Zoom! to Tend's national network of dental offices. Tend's clinicians will now be able to provide their patients with Philips Zoom! WhiteSpeed, a light-accelerated treatment capable of whitening teeth up to eight shades in 45 minutes.

- In November 2024, Garrison Dental Solutions launched its new breakthrough in light curing technology called the Loop Curing Light. The novel curing light delivers superior precision and consistency to restorative dentistry, improving clinician confidence with every cure.

Companies Covered in Dental Lights Market

- Danaher Corporation

- A-dec Inc.

- Midmark Corporation

- PLANMECA Oy

- DentalEZ

- TPC Advanced Technology, Inc.

- Flight Dental Systems

- Dr. Mach GmbH & Co. KG

- Advin Health Care

- Apollo Lighting Ltd.

- Others

Frequently Asked Questions

The dental lights market is projected to reach US$ 873.2 Mn in 2025.

Shift from halogen to LED lights and integration of smart features, such as motion sensors, are the key market drivers.

The dental lights market is poised to witness a CAGR of 5.3% from 2025 to 2032.

Key market opportunities include the expansion of dental tourism hubs and the surging adoption of digital dentistry.

Danaher Corporation, A-dec Inc., and Midmark Corporation are a few key market players.