- Animal Feed & Additives

- Corn Steep Liquor Market

Corn Steep Liquor Market Size, Share, Growth, and Regional Forecast, 2025 - 2032

Corn Steep Liquor Market by Nature (Organic, Conventional), by Form (Liquid, Powder), by End-user (Fertilizers, Fermentation, Animal Feed), and Regional Analysis from 2025 - 2032

Corn Steep Liquor Market Share and Trends Analysis

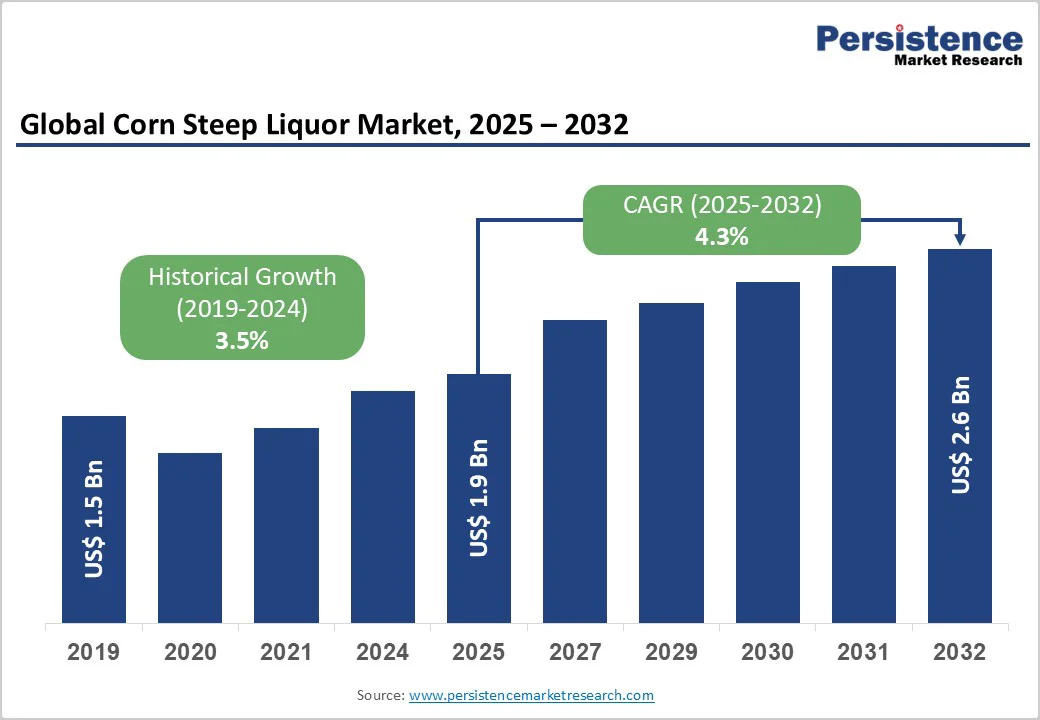

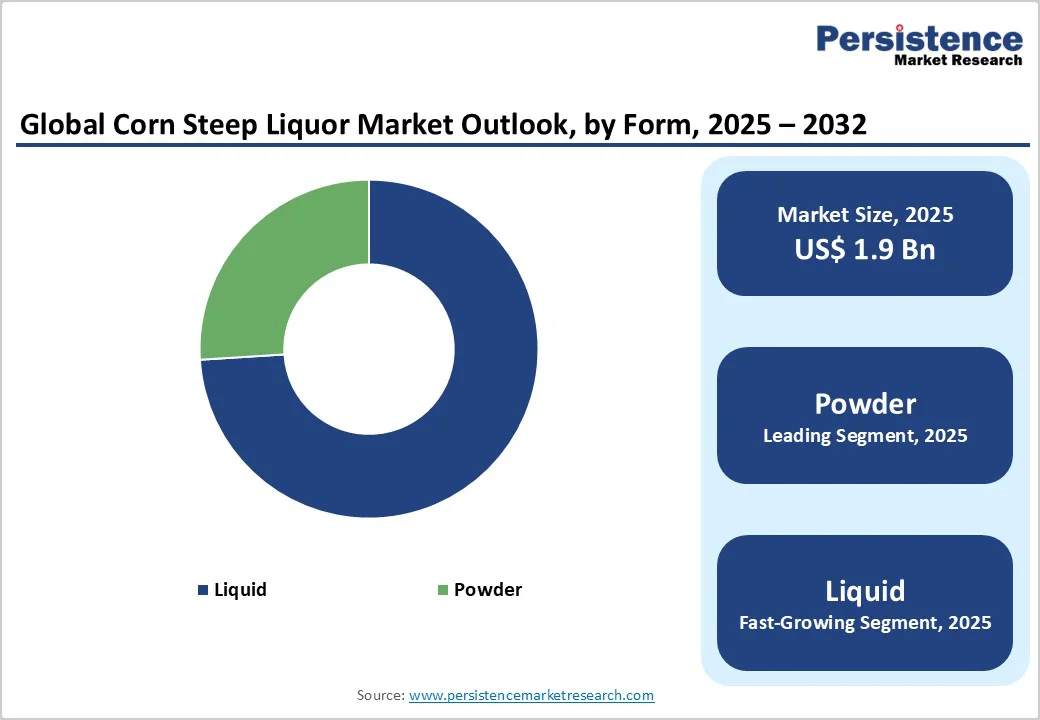

The global corn steep liquor market size is valued at US$ 1.9 billion in 2025 and is projected to reach US$ 2.6 billion, growing at a CAGR of 4.3% during the forecast period from 2025 to 2032. A rapidly evolving corn-processing landscape, combined with rising feed and fermentation demand, is reshaping strategic priorities across the ecosystem. Producers, distributors, and ingredient innovators are adjusting their playbooks as wet-milling upgrades, organic transitions, and feedstock volatility redefine competitive positioning.

Key Industry Highlights:

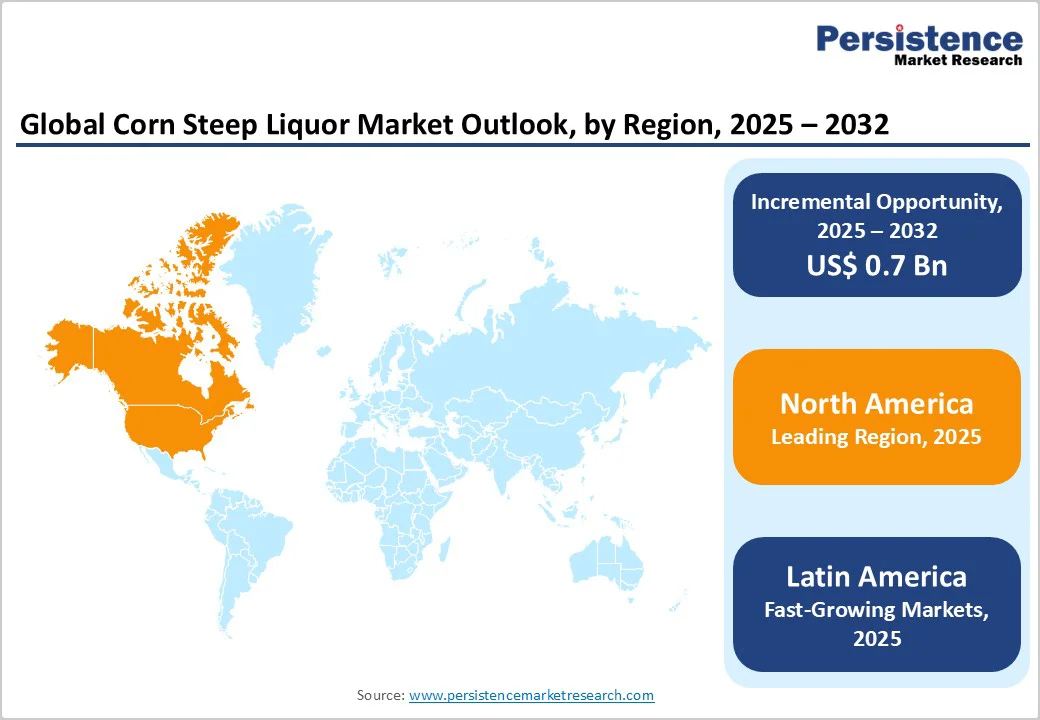

- Leading Region: North America, holding 37% market share, driven by large-scale wet-milling, advanced filtration systems, and rising demand from feed and fermentation industries.

- Fastest-Growing Region: Latin America, fueled by expanding corn output, investments in wet-milling capacity, and increasing adoption of CSL in poultry, dairy, and bioethanol production.

- Fastest-Growing Segment by Nature: Organic CSL, propelled by increasing organic farming practices, clean production trends, and residue-free feed requirements.

- Market Drivers: Rising global livestock and poultry feed demand and expanding fermentation applications are boosting CSL consumption across multiple industrial sectors.

- Opportunities: Asia Pacific’s increasing wet-milling capacity provides scope for regional production, reducing import dependence and enabling customized nutrient blends.

- Key Developments: In May 2024, KPS Capital Partners acquired Tate & Lyle’s remaining 49.7% stake in Primient, enhancing CSL production capabilities and regional supply infrastructure.

| Key Insights | Details |

|---|---|

|

Global Corn Steep Liquor Market Size (2025E) |

US$ 1.9 Bn |

|

Market Value Forecast (2032F) |

US$ 2.6 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

4.3% |

|

Historical Market Growth (CAGR 2019 to 2024) |

3.5% |

Market Dynamics

Driver - Growing Global Livestock and Poultry Feed Consumption Boosts Corn Steep Liquor (CSL) Usage

A noticeable shift in global protein production is quietly pushing Corn Steep Liquor (CSL) deeper into livestock nutrition strategies. As feed manufacturers intensify efforts to meet rising demand for poultry, dairy, and swine outputs, CSL is gaining traction as a cost-efficient, nutrient-dense liquid supplement rich in amino acids, vitamins, and organic nitrogen. Its high digestibility supports improved gut function and better feed conversion ratios, making it particularly valuable in regions scaling intensive farming systems. Producers also favour CSL for enhancing palatability and supporting microbial activity in fermented and silage-based diets. The expanding global feed footprint driven by population growth, higher meat consumption, and precision-feeding practices is steadily elevating CSL’s role as a reliable performance enhancer in modern animal nutrition programs.

Restraints - Price Volatility in Global Corn Markets Disrupts CSL Cost Stability

Price swings in the global corn trade are increasingly undermining cost predictability for Corn Steep Liquor (CSL) manufacturers, creating a challenging restraint for the market. Since CSL production is tightly linked to wet-milling economics, any surge in raw corn prices driven by climate stress, export restrictions, biofuel demand, or geopolitical disruptions directly inflates input costs and squeezes operating margins. This instability makes it difficult for feed producers and fermentation-based industries to commit to long-term procurement contracts. Sudden spikes also force smaller processors to reduce output or alter formulations, weakening supply consistency. As volatility becomes more frequent, buyers face unpredictable pricing cycles that complicate budget planning and push them to explore alternative nutrient sources or diversify suppliers.

Opportunity - Increasing Corn Wet-Milling Capacity in Asia Pacific

A wave of new wet-milling projects across the Asia Pacific is quietly unlocking one of the strongest growth avenues for Corn Steep Liquor suppliers. Countries such as China, India, and Vietnam are rapidly scaling starch processing and biorefinery operations to support expanding food, feed, and fermentation industries. This surge in capacity is creating a larger and more consistent supply of CSL, opening doors for ingredient companies and startups to build regionally anchored procurement and distribution models. Local CSL availability reduces import dependence and lowers logistics costs for feed manufacturers, bio-fertilizer formulators, enzyme producers, and microbial fermentation plants. As Asian mills upgrade to higher-efficiency extraction systems, CSL quality is improving, giving innovators room to design premium nutrient blends, tailored fermentation media, and specialized feed additives.

Category-wise Analysis

By Form Insights

Liquid corn steep liquor accounts for. 71% share as of 2024, and its lead stems from how efficiently it integrates into large-scale feed, fermentation, and bio-based manufacturing systems. Producers prefer liquid CSL because it delivers a rich mix of amino acids, peptides, organic acids, and minerals in a ready-to-use format that requires no rehydration or solubility adjustments. Its consistency supports stable microbial growth in enzymes, antibiotics, and industrial fermentation processes, while feed manufacturers value its ease of blending and uniform nutrient distribution. Powder corn steep liquor plays a steady supporting role, particularly in applications demanding extended shelf life, reduced transport weight, or simplified storage. However, its higher processing costs and handling steps limit broader adoption compared with the fluid form.

By Nature Insights

Organic corn steep liquor is projected to grow at a CAGR of 6.7% during the forecast period, and this momentum reflects how quickly organic agriculture, bio-fermentation, and natural feed systems are scaling worldwide. Farmers, feed makers, and fermentation companies are shifting toward inputs free from chemical residues, pushing demand for organically sourced nutrient-rich CSL that supports soil health, microbial efficiency, and cleaner production cycles. Its strong amino acid and mineral profile makes it an attractive input for organic fertilizers, biostimulants, and microbial inoculants used in high-value horticulture. In livestock and poultry nutrition, organic CSL is gaining traction as producers upgrade their feed formulations to meet premium certification standards. Conventional CSL remains dominant, but rising regulatory scrutiny and eco-conscious purchasing patterns are accelerating the organic segment’s expansion.

Region-wise Insights

North America Corn Steep Liquor Market Trends

North America holds approximately 37% market share in the global corn steep liquor (CSL) market, largely fueled by strong wet-milling capacity in the U.S. and Canada. In the U.S., corn planted acreage has surged to 95.2 million acres in 2025, up 5% from the previous year, supporting a rising CSL supply. Canada’s corn sector is expanding, with production projected at around 15.1 million tonnes despite volatility, reinforcing local CSL feedstock availability. Across the region, CSL demand is strengthening as livestock producers push for nutrient-dense, cost-efficient feed additives that improve gut health and growth performance. Fermentation industries' bio-ethanol, enzymes, and organic acids are increasing CSL uptake as a reliable nitrogen source. Manufacturers are also enhancing product consistency through better filtration, pH control, and storage systems, positioning North America as a technologically advanced CSL ecosystem.

Latin America Corn Steep Liquor Market Trends

Latin America corn steep liquor market is expected to achieve a CAGR of 6.4%, propelled by expanding livestock production systems and rapid adoption of fermentation-based industries across the region. Mexico is increasing its reliance on CSL as poultry and swine integrators shift toward nutrient-rich liquid feed inputs to improve weight gain efficiency. Brazil’s booming corn surplus and its aggressive investments in wet-milling facilities are strengthening domestic CSL availability for bioethanol plants, enzyme producers, and amino acid manufacturers. Argentina is accelerating demand as dairy and beef operations integrate CSL into feed rations to reduce input costs amid fluctuating grain prices. Across the region, suppliers are focusing on enhanced storage stability, odor-reduced formulations, and customized nutrient profiles to align with intensifying industrial and agricultural requirements.

Competitive Landscape

The global corn steel liquor market remains moderately consolidated, creating a space where established wet-milling companies, fermentation specialists, and vertically integrated feed producers compete through scale, consistency, and innovation. Leading players are expanding production lines, upgrading steeping efficiency, and adopting odor-controlled processing to deliver higher-purity CSL tailored for feed, bioethanol, and microbial fermentation. Several manufacturers are shifting toward organic-compliant formulations to align with rising demand from sustainable farming systems, prompting investments in residue-free steeping protocols and certification upgrades. Vertical integration is gaining momentum as corn processors tighten control over feedstock sourcing to reduce volatility and ensure traceability. Regulatory pressure around effluent management and byproduct utilization is accelerating the adoption of cleaner technologies, while new entrants explore enzymatic pretreatment and nutrient-optimized CSL variants to differentiate in the global market.

Key Industry Developments:

- In May 2024, KPS Capital Partners announced an agreement to acquire Tate & Lyle's remaining 49.7% ownership interest in Primient for $350 million. This transaction, expected to close by the end of July 2024, makes KPS the sole owner of Primient and fully completes Tate & Lyle's transformation into a focused specialty food and beverage solutions business.

- Cargill, Inc. provides corn steep liquor as an additive for compound feed. It helps to improve the organoleptic properties of the feed along with adding nutritional value. The company supply corn step liquor to feed industry that is rich in amino acid that supports digestion in animals.

- ADM emphasizes on partnerships with ingredient-based research & development companies, which will enable it to develop and commercialize products that have a higher margin. With this move, the company also aims at expansion in the food ingredients market.

Companies Covered in Corn Steep Liquor Market

- ADM

- Cargill, Inc

- Gulshan Polyols Ltd.

- Ingredion Incorporated

- Tate & Lyle PLC

- Tereos S.A

- Sanstar Bio-Polymers Ltd.

- Maize Products

- Juci Biological

- Others

Frequently Asked Questions

The global Corn Steep Liquor market is projected to be valued at US$ 1.9 Bn in 2025.

Growing global livestock and poultry feed consumption is fueling the demand for Corn Steep Liquors in the global market.

The global Corn Steep Liquor market is poised to witness a CAGR of 4.3% between 2025 and 2032.

The increasing corn wet milling capacity in the Asia Pacific region presents a significant market opportunity for key industry players.

Major players in the global Corn Steep Liquor market include ADM, Cargill, Inc, Gulshan Polyols Ltd., Ingredion Incorporated, Tate & Lyle PLC, Tereos S.A, Sanstar Bio-Polymers Ltd., and others.