- HVAC

- Cooling Tower Market

Cooling Tower Market Size, Share, and Growth Forecast 2026 - 2033

Cooling Tower Market by Flow Type (Cross-Flow, Counter-Flow), Tower Type (Evaporative, Dry, Hybrid), Capacity Range (Below 5 MW, 5 to 20 MW, Above 20 MW), Application (Oil and Gas), and Regional Analysis, 2026 - 2033

Cooling Tower Market Size and Trends Analysis

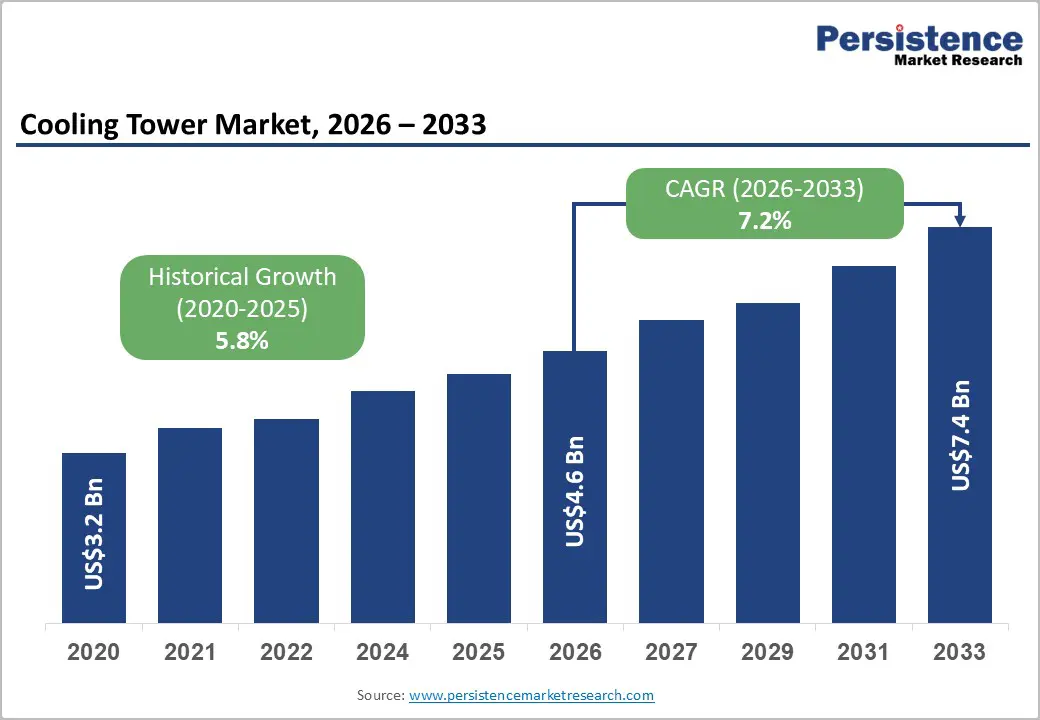

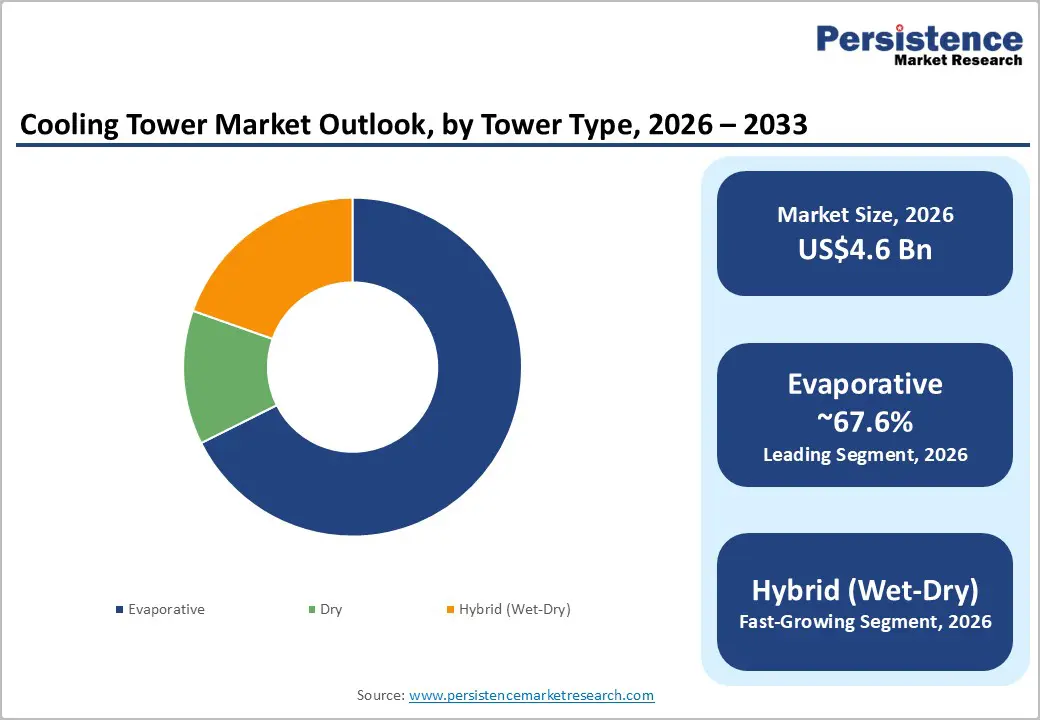

The global cooling tower market size is likely to be valued at US$4.6 billion in 2026 and is predicted to reach US$7.4 billion by 2033, growing at a CAGR of 7.2% during the forecast period from 2026 to 2033, driven by the rising deployment of data centers that require continuous and efficient heat rejection systems. Increasing adoption of district cooling projects across urban developments is further fueling demand for centralized cooling infrastructure.

Key Industry Highlights:

- Leading Flow Type: Cross-flow, approximately 57.3% share in 2026, as its open basin design allows better tolerance to poor water quality and scaling.

- Dominant Tower Type: Evaporative towers, nearly 67.6% in 2026, because they provide efficient heat rejection with low electricity consumption.

- Latest Contract: In December 2025, John Cockerill signed a contract with Elsewedy Electric Power Systems Projects and its partner POWERCHINA for the design and supply of two large HAMON cooling towers for the Al Mourjan Rabigh 2 Power Plant Extension in Saudi Arabia. The agreement marks a significant milestone in the companies' long-term collaboration, with John Cockerill's HAMON cooling technology expected to play a key role in optimizing plant performance.

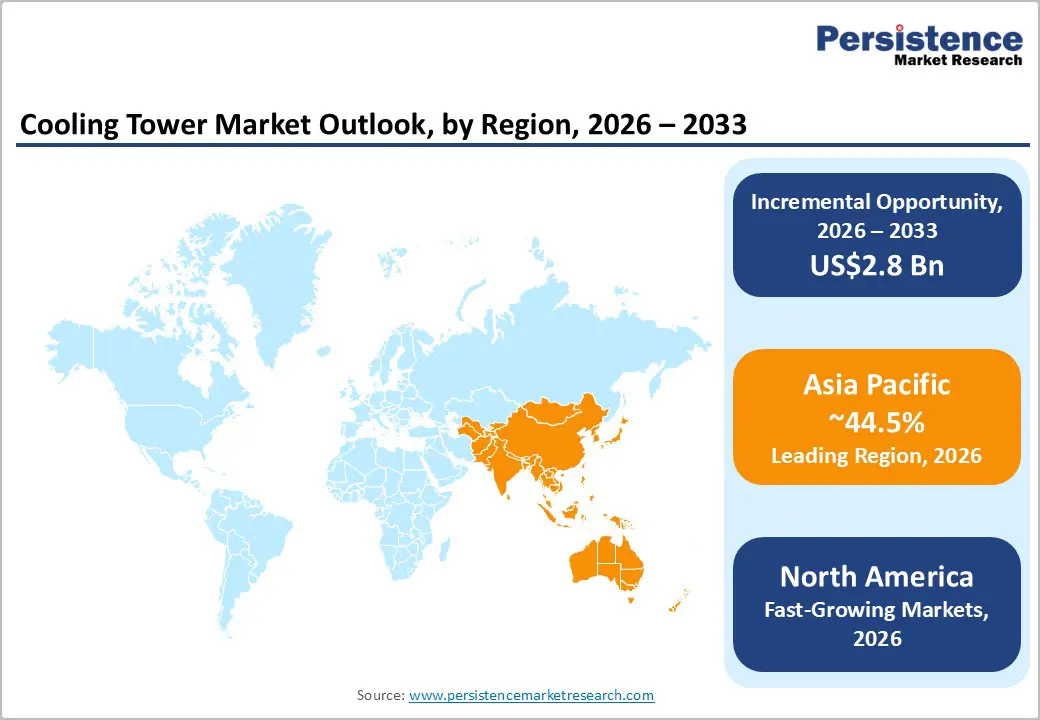

- Leading Region: Asia Pacific, with about 44.5% share in 2026, owing to expanding power generation capacity and large-scale commercial construction projects.

- Fast-growing Region: North America, backed by replacement demand and expansion in high-tech infrastructure.

DRO Analysis

Driver - Rising Deployment of Cooling Systems in Commercial Buildings

The growth of large commercial spaces is directly increasing demand for cooling towers. Offices, malls, airports, and hospitals rely on centralized Heating, Ventilation, and Air Conditioning (HVAC) systems that require efficient heat rejection. Cooling towers are preferred as they reduce electricity use compared to air-cooled systems.

A 2023 report from the U.S. Energy Information Administration highlighted that space cooling remains one of the most prominent electricity uses in commercial buildings, especially in warm regions. In India, the Bureau of Energy Efficiency has also promoted district cooling projects in cities such as Amaravati and Gujarat International Finance Tec (GIFT) City, where cooling towers are a core component. This shift toward centralized cooling infrastructure is creating a steady demand across real estate and urban development projects.

Strict Norms Revolving Around Water Consumption and Energy Performance

Environmental regulations are pushing industries to upgrade to efficient cooling systems. Cooling towers are being redesigned to reduce water loss and energy use. Governments are enforcing strict norms on water discharge, drift, and thermal pollution. For instance, the U.S. Environmental Protection Agency (EPA) enforces guidelines under the Clean Water Act that impact industrial cooling systems.

In Europe, the European Commission promotes water reuse and efficiency under its circular economy policies. This has led to the adoption of closed-loop and hybrid cooling towers. Companies are investing in unique drift eliminators and smart controls to meet compliance. These regulatory pressures are not slowing demand but are instead pushing the replacement of aging systems with modern towers.

Restraint - High Costs Linked to Emission Control and Water Drift Reduction Systems

Compliance with plume visibility and water drift norms is becoming expensive for operators. Cooling towers release visible vapor plumes, which are now regulated in urban and sensitive industrial zones. To control this, companies must install plume-abatement coils and novel drift eliminators. These additions increase both capital and maintenance costs.

The Centers for Disease Control and Prevention (CDC) has also issued strict guidelines to control Legionella growth in cooling towers, requiring better water treatment and monitoring systems. Guidance from the Health and Safety Executive also stresses regular inspection and upgrades. These compliance requirements can increase project complexity and discourage small operators, especially in cost-sensitive markets.

Opportunity - Increasing Demand for Process Cooling in Hydrogen Production Projects

Green hydrogen plants are emerging as a new demand area for cooling towers. Electrolyzers generate significant heat during hydrogen production and require stable cooling systems. Cooling towers are used to maintain temperature and improve efficiency. In 2024, the International Energy Agency noted that large-scale electrolyzer projects are expanding across Europe and the Middle East.

Projects such as NEOM in Saudi Arabia are integrating advanced cooling systems to support continuous hydrogen output. These plants operate at scale and require reliable thermal management, further creating long-term demand for industrial cooling towers.

Expansion of Large-scale Data Center Infrastructure

The rapid growth of cloud computing is augmenting demand for cooling towers in data centers. These facilities generate high heat loads and require efficient cooling solutions to maintain uptime. Water-based cooling towers are increasingly used on hyperscale campuses due to their superior energy performance.

In 2023, the International Energy Agency (IEA) reported that data centers account for a rising share of global electricity use, with cooling forming a key part of that demand. Companies such as Google and Microsoft are adopting hybrid cooling systems that combine towers with unique controls to reduce water use. This trend is creating new opportunities for cooling tower manufacturers, especially in regions with large data center investments.

Category-wise Analysis

Flow Type Insights

The cross-flow segment is predicted to lead with a share of approximately 57.3% in 2026. Cross-flow cooling towers remain widely used because of their simple structure and low operating pressure. Water flows downward by gravity while air moves horizontally, which reduces pumping energy. This makes them suitable for commercial HVAC systems where cost and ease of maintenance matter. The U.S. Department of Energy notes that gravity-fed designs help reduce auxiliary energy use in cooling systems. Several building operators prefer cross-flow towers as they are quiet and easy to service. This is important for hospitals, malls, and office buildings located in urban areas.

The counter-flow towers segment is anticipated to remain in the second position in 2026, as they deliver high thermal efficiency. Air moves upward against falling water, which improves heat transfer. This design reduces water consumption and improves cooling performance. The Cooling Technology Institute notes that counter-flow towers achieve lower approach temperatures than cross-flow systems. Industries such as power plants and data centers are shifting to this design to meet strict energy and water targets. Their compact size also helps in space-constrained industrial sites.

Tower Type Insights

The evaporative segment is projected to account for nearly 67.6% of the market share in 2026, owing to its high cooling efficiency and comparatively lower energy consumption. These cooling towers use evaporative cooling to dissipate heat more effectively than air-based systems. According to the U.S. Environmental Protection Agency, evaporative cooling systems can substantially reduce energy use compared to dry-cooling alternatives. Their widespread adoption across power plants, oil refineries, and HVAC applications further supports segment growth. In addition, their ability to manage high heat loads cost-effectively makes them a preferred solution across multiple industrial sectors.

The hybrid (wet-dry) cooling towers segment is expected to remain in second place in 2026, as industries seek to reduce water use and plume visibility. These systems combine dry and wet cooling, allowing operators to switch modes based on weather and demand. The International Energy Agency has highlighted increasing focus on water-efficient cooling technologies in energy-intensive sectors. Companies are adopting hybrid towers in regions facing water scarcity and strict environmental rules. This flexibility helps meet both performance and compliance requirements.

Regional Insights

Asia Pacific Cooling Tower Market Trends

In 2026, Asia Pacific is expected to dominate with a share of around 44.5%, owing to industrial expansion, urban construction, and rising cooling demand from climate conditions. Countries such as China, India, Indonesia, and Vietnam are adding large power plants, refineries, and commercial hubs that depend on cooling towers. The Asian Development Bank has highlighted that infrastructure spending in the region remains one of the highest globally, with the main focus on energy and urban utilities. Several cities are also adopting district cooling systems.

For example, India’s GIFT City project integrates centralized cooling plants that rely on cooling towers. High humidity and temperature levels across the region further make evaporative cooling more effective, thereby supporting adoption.

China Cooling Tower Market Trends

China’s growth is accelerated by its large-scale industrial operations and energy transition projects. Heavy industries such as petrochemicals, steel, and power generation require continuous process cooling. The National Bureau of Statistics of China has consistently reported expansion in industrial output and energy production capacity. The country is also investing in nuclear power and green hydrogen projects, both of which require advanced cooling systems. Another key factor is the steady rise of data centers. Government-backed initiatives under its digital economy strategy are increasing server capacity, which directly raises demand for high-efficiency cooling towers.

India Cooling Tower Market Trends

India is moving toward steady and diversified growth in cooling tower demand. Urban expansion, rising middle-class consumption, and increasing government push for infrastructure are key drivers. The Bureau of Energy Efficiency is promoting district cooling systems that can reduce peak electricity demand in cities. Projects in Amaravati and GIFT City are early examples. India’s data center capacity is also expanding at a steady pace, especially in Mumbai and Chennai, due to data localization rules. The country is further adding thermal and renewable power capacity, both of which require cooling systems. However, water scarcity is pushing industries to adopt hybrid and water-efficient towers, influencing the type of demand.

North America Cooling Tower Market Trends

North America is anticipated to be the fastest-growing region over the forecast period, backed by replacement demand and expansion in high-tech infrastructure. Various industrial facilities and commercial buildings are upgrading aging cooling systems to meet new efficiency standards. The U.S. Energy Information Administration notes that cooling remains a key contributor to electricity use in buildings, especially during peak seasons. Hyperscale data centers are also expanding across states such as Virginia, Texas, and Arizona. These facilities require large-scale and reliable cooling systems. Water management is also a concern in parts of the U.S., which is encouraging the use of hybrid cooling towers.

U.S. Cooling Tower Market Trends

The U.S. is expected to maintain high demand due to continuous investments in digital infrastructure and industrial modernization. Data center operators such as hyperscale cloud providers are focusing on energy-efficient and water-smart cooling systems. The U.S. Department of Energy has been supporting novel cooling technologies through research and funding programs. There is also increased adoption of closed-loop and hybrid systems to comply with environmental regulations. Sectors such as pharmaceuticals, food processing, and chemicals are further upgrading facilities, which supports long-term demand for cooling towers.

Europe Cooling Tower Market Trends

Europe is witnessing stable but regulation-driven growth in cooling tower adoption. The focus is less on volume expansion and more on system upgrades and sustainability. The European Commission has introduced strict climate and water policies under the Green Deal, pushing industries to reduce emissions and water use. This is leading to the replacement of aging cooling towers with advanced and efficient models. District cooling is also gaining traction in cities such as Paris and Stockholm, where centralized systems are used to improve energy efficiency. Industrial sectors are investing in cooling technologies that comply with circular economy goals.

Germany Cooling Tower Market Trends

Germany stands out for its strong industrial base and growing focus on the energy transition. Industries such as automotive manufacturing, chemicals, and engineering rely heavily on process cooling. The Federal Statistical Office of Germany shows that industrial production remains a key part of the economy, supporting consistent demand for cooling infrastructure. Germany is also investing in hydrogen projects and renewable energy systems, both of which require efficient cooling. The push for energy efficiency and strict environmental standards is encouraging industries to adopt modern cooling towers with better performance and lower water use.

U.K. Cooling Tower Market Trends

The U.K. is anticipated to see gradual growth propelled by digital infrastructure and sustainability targets. Data centers are expanding in cities such as London and Manchester due to rising cloud demand. The U.K. Department for Energy Security and Net Zero is promoting energy-efficient and low-carbon technologies, including improvements to cooling systems. There is also increasing focus on retrofitting aging buildings with efficient HVAC systems. Water management and environmental compliance are key concerns, leading to the adoption of hybrid and low-drift cooling towers.

Competitive Landscape

The global cooling tower market is moderately fragmented, with a few multinational leaders controlling large utility and industrial projects. Companies such as SPX Cooling Technologies, Baltimore Aircoil Company, EVAPCO, Johnson Controls, and Paharpur Cooling Towers dominate high-value contracts because of their engineering expertise, installed service networks, and ability to handle large-scale thermal management systems. Competition is increasingly shifting away from only tower manufacturing toward smart cooling ecosystems.

Key companies are integrating AI, IoT monitoring, predictive maintenance, and water-saving technologies to differentiate themselves. The competitive intensity is strong in the data center segment, where hyperscale operators are demanding hybrid cooling, low-drift systems, and digitally connected infrastructure. Vendors are competing on lifecycle operating costs rather than upfront pricing. Novel features such as EC fan motors, intelligent hybrid controls, and cloud-based thermal monitoring are becoming prominent differentiators.

Key Industry Developments:

- In February 2026, Dubai Electricity and Water Authority (DEWA) acquired Dubai Holding's entire 24% stake in Emirates Central Cooling Systems Corporation (Empower) for approximately US$1.41 billion. The transaction increased DEWA's ownership in Empower from 56% to 80%.

- In February 2026, Brentwood Industries published a case study on a key cooling tower retrofit at the 300-megawatt Treasure Coast Energy Center in Florida. In collaboration with International Cooling Tower, Inc., Brentwood's ShockWave fill was selected for its superior heat transfer capabilities, while new high-efficiency fans were installed to reduce energy consumption.

- In December 2025, Fermi America, in partnership with the Texas Tech University System, signed a Memorandum of Understanding (MoU) with MVM EGI Zrt. to engineer a next-generation hybrid cooling system for its planned 11-gigawatt private energy campus in West Texas. The proposed 450-foot hybrid dry-wet cooling towers are designed to deliver more than 80% less evaporative loss than conventional all-wet towers.

Companies Covered in Cooling Tower Market

- Babcock & Wilcox Enterprises, Inc.

- Baltimore Aircoil Company

- Cenk Endüstri Tesisleri İmalat Ve Taahhüt A.Ş.

- Cooling Tower Systems, Inc.

- Delta Cooling Towers Inc.

- Engie Refrigeration GmbH

- EVAPCO, Inc.

- S.A. Hamon

- Johnson Controls International Plc.

- Kelvion Holdings GmbH

- Liang Chi Industry Co., Ltd.

- Mesan Group

- Paharpur Cooling Towers Ltd.

- SPX Corporation

- Torraval Cooling S.L.

- Others

Frequently Asked Questions

The global cooling tower market is projected to reach US$4.6 billion in 2026.

The market is expected to reach US$7.4 billion by 2033.

Key market trends include the adoption of hybrid wet-dry cooling systems and the integration of IoT-based monitoring.

Cross-flow is expected to be the leading flow type with a share of nearly 57.3% in 2026, as it delivers easy maintenance, low pumping energy, and quiet operations.

The market is expected to grow at a CAGR of 7.2% from 2026 to 2033.

Babcock & Wilcox Enterprises, Inc., Baltimore Aircoil Company, and Cenk Endüstri Tesisleri Imalat Ve Taahhüt A.Åž. are a few key market players.