- Home Appliances

- Connected TV Market

Connected TV Market Size, Share, and Growth Forecast 2026 - 2033

Connected TV Market by Screen Size (Below 30 Inches, 30 to 50 Inches, 50 to 70 Inches, Above 70 Inches), Distribution Channel (Online, Offline), Technology (LED, OLED, Others), End Use (Entertainment, Education, Home Use, Others), and Regional Analysis for 2026 - 2033

Connected TV Market Size and Trend Analysis

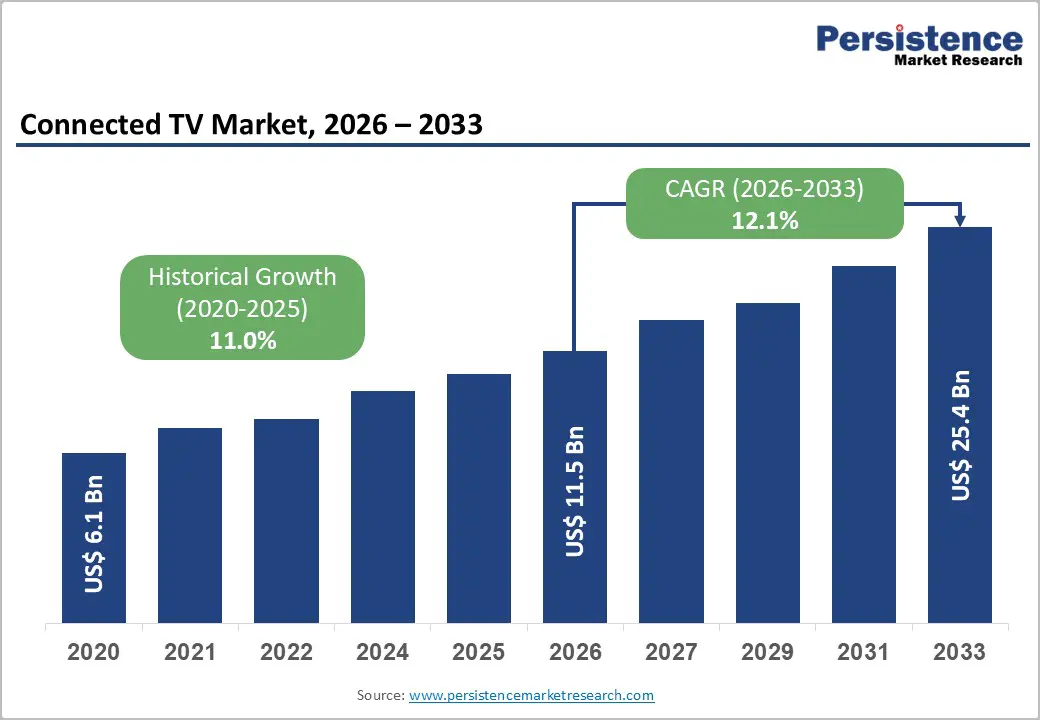

The global Connected TV Market size is valued at US$ 11.4 billion in 2026 and is projected to reach US$ 25.4 billion by 2033, growing at a CAGR of 12.1% between 2026 and 2033.

This robust growth is primarily fueled by the accelerating global shift from traditional linear broadcasting to internet-enabled on-demand streaming ecosystems, alongside rapid advances in display technology, including OLED, QLED, and Mini-LED panels. The proliferation of high-speed broadband and 5G networks across both developed and emerging economies is enabling seamless, high-definition content delivery, making connected TVs increasingly indispensable in modern households.

Key Industry Highlights:

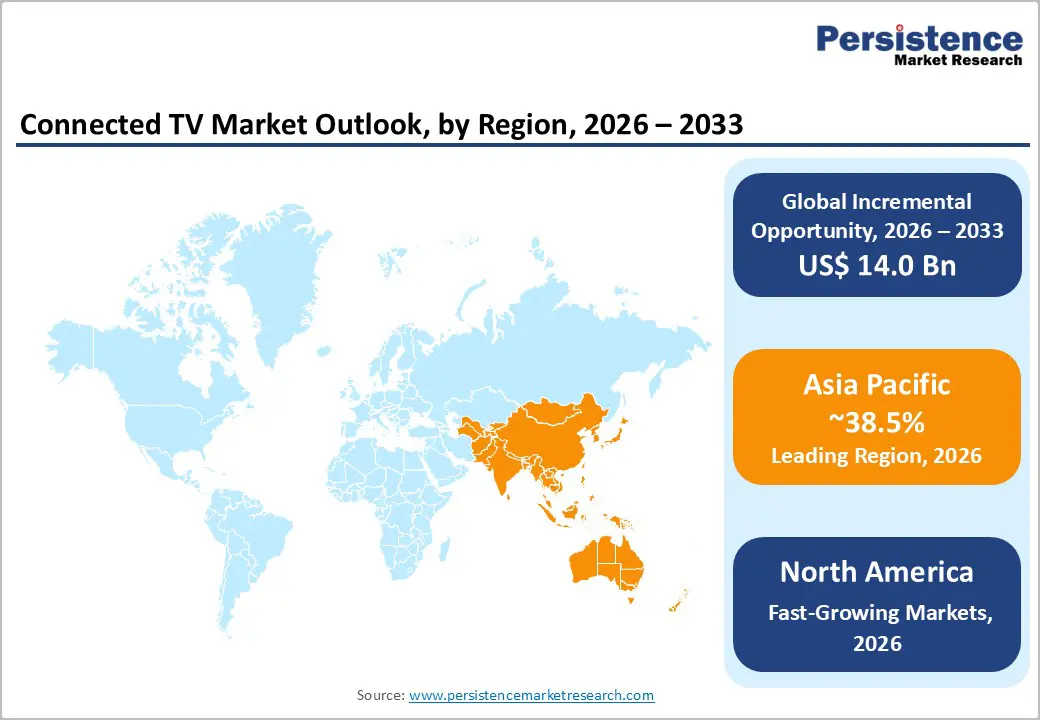

- Leading Region - Asia Pacific is the leading regional market, fueled by India's internet user base surpassing 954 million, aggressive 5G rollout in China, and affordable smart TV adoption across ASEAN markets, projected at a CAGR exceeding 14% through 2030.

- Fastest Growing Region - North America is fastest-growing region for the global Connected TV Market in revenue value, driven by 90% household penetration, the world's most mature OTT advertising ecosystem, and U.S. CTV ad spend reaching US$ 28.79 Bn in 2024.

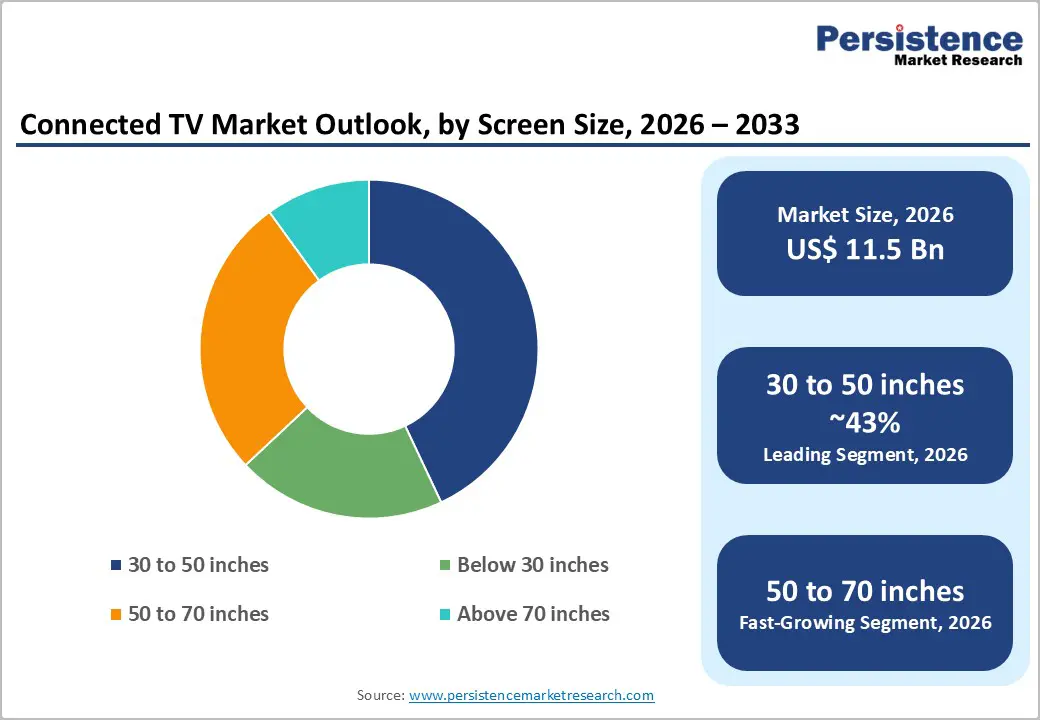

- Dominant Segment - The 30 to 50-inch screen size segment dominates the Connected TV Market with approximately 61% revenue share in 2024, benefiting from its balance of immersive viewing experience, broad compatibility with 4K content, and affordability across income segments.

- Fastest Growing Segment - The Online distribution channel is the fastest-growing segment, expanding at a CAGR of 12.9% through 2030, driven by e-commerce platform growth, competitive pricing transparency, and accelerating digital purchasing behaviour in markets including India, China, and Southeast Asia.

- Key Market Opportunity - The convergence of AVOD expansion and programmatic advertising infrastructure represents the market's most significant monetization opportunity, with U.S. CTV ad spend projected to reach US$ 46.89 Bn by 2029, drawing advertising budgets away from linear television at an accelerating rate.

| Key Insights | Details |

|---|---|

|

Connected TV Market Size (2026E) |

US$ 11.4 Bn |

|

Market Value Forecast (2033F) |

US$ 25.4 Bn |

|

Projected Growth CAGR (2026–2033) |

12.1% |

|

Historical Market Growth (2020–2025) |

11.0% CAGR |

Market Dynamics

Drivers - Surge in Global Streaming Adoption and Cord-Cutting

One of the most powerful catalysts reshaping the Connected TV Market is the unprecedented acceleration of streaming service adoption paired with mass cord-cutting from traditional pay-tv. According to data from Nielsen, streaming accounted for approximately 44.8% of total U.S. television viewership as of mid-2025, surpassing the combined share of broadcast (20.1%) and cable (24.1%) for the first time in history. U.S. pay-tv households have plunged from over 100 million a decade ago to below 70 million in 2024, with projections pointing toward further erosion to 47.8 million by 2027. This structural shift is compelling tens of millions of households worldwide to invest in connected TV hardware, including smart TVs and streaming sticks to access platforms such as Netflix, Disney+, Amazon Prime Video, and Hulu. The Interactive Advertising Bureau (IAB) reported that U.S. CTV ad spending reached US$ 23.6 Bn in 2024, registering 16% year-over-year growth, underscoring advertiser confidence in the platform's reach and targeting precision.

Rapid Advances in Display Technology and AI Integration

Technological innovation in display technologies is significantly elevating the consumer value proposition of connected TVs, driving replacement cycles and market expansion. The transition from conventional LCD panels to advanced OLED, QLED, and next-generation Micro RGB Mini-LED displays is delivering unprecedented levels of contrast, colour accuracy, and brightness. According to Omdia, the global OLED TV market grew 6% in 2025, reaching 6.43 million units, with Samsung Electronics recording its best-ever OLED TV year at approximately 2 million units sold, representing a 38% increase year-over-year. Furthermore, the integration of artificial intelligence (AI) into TV operating systems enabling personalized content recommendations, voice-command navigation, and real-time image enhancement, is transforming connected TVs from passive displays into intelligent home entertainment hubs.

Restraint - High Product Cost and Price Sensitivity in Emerging Markets

Despite strong global momentum, affordability remains a significant barrier to connected TV penetration, particularly in price-sensitive emerging economies across South Asia, Latin America, and Sub-Saharan Africa. Premium display technologies such as OLED and QLED command substantial price premiums over conventional LED sets, placing them out of reach for a broad segment of the global consumer base. Even in mature markets, the high upfront costs of connected TVs with advanced features such as 8K resolution and integrated smart home capabilities can deter budget-conscious consumers. This cost barrier limits the addressable market for premium manufacturers and creates significant headwinds for revenue growth in regions that represent the largest pools of untapped consumers, constraining the overall pace of global market expansion.

Platform Fragmentation and Content Delivery Complexity

The Connected TV ecosystem is increasingly fragmented across competing operating systems including Tizen OS (Samsung), webOS (LG), Google TV, Roku OS, and Fire OS (Amazon)creating substantial operational complexity for content providers and advertisers. Each platform requires distinct software development kits (SDKs), separate certification processes, and independent regression testing cycles, significantly raising development costs for over-the-top (OTT) service operators. Industry data indicates that platform-specific ad-tech implementations are multiplying operational burdens, concentrating market power among a handful of incumbents capable of supporting multi-platform development. This fragmentation also undermines cross-platform measurement, complicating return-on-investment (ROI) attribution for advertisers and limiting the scalability of data-driven advertising strategies, both of which are critical to the market's long-term monetization potential.

Opportunities - Expansion of Ad-Supported Streaming and Programmatic CTV Advertising

The rapid mainstreaming of ad-supported video on demand (AVOD) and free ad-supported streaming TV (FAST) models represents a transformative revenue opportunity for participants across the Connected TV Market ecosystem. According to the IAB, U.S. CTV advertising expenditure was projected to surpass US$ 26.6 Bn in 2025, with independent forecasts pointing toward US$ 46.89 Bn by 2028–2029. A landmark data point underscoring this opportunity: Netflix's ad-supported tier reached 94 million monthly global users in 2025, demonstrating that mainstream audiences actively embrace ad-funded models when given the option. By Q1 2025, ad-supported subscriptions accounted for 57% of new subscriber additions globally. As programmatic advertising infrastructure matures with measurement innovations from organizations such as the IAB and OpenAP, enabling cross-platform, deduplicated audience measurement, connected TV is rapidly emerging as the preferred premium video advertising channel, generating compelling opportunities for hardware manufacturers, streaming platform operators, and advertising technology providers alike.

Rising Demand in Asia Pacific and Integration with Smart Bathroom and Connected Home Ecosystems

The Asia Pacific region represents perhaps the single most significant growth opportunity in the Connected TV Market, propelled by expanding middle-class populations, rapid urbanization, and aggressive 5G infrastructure deployment across China, India, Japan, and Southeast Asia. India's Ministry of Communications reported that internet users increased from 251.59 million in 2014 to 954.40 million in 2024, with rural penetration reaching 398.35 million a vast underserved audience increasingly gaining access to affordable connected TV devices. Chinese brands, including Hisense Group, TCL Technology, and Xiaomi Corporation, are aggressively capturing this demand through competitively priced smart TV portfolios supported by local streaming ecosystems such as iQIYI and Tencent Video. Beyond traditional entertainment, the convergence of connected TVs with broader smart home technologies including the growing Smart Bathroom Market, which is integrating entertainment screens and IoT-enabled devices signals a profound expansion of connected TVs' total addressable market as the central node of the digital home.

Category-wise Analysis

Screen Size Insights

Within the Connected TV Market, the 30 to 50 inches screen size segment commands the dominant revenue position, accounting for approximately 55% of total market revenue in 2026, according to industry data. This segment's leadership is underpinned by its compelling value proposition: it delivers a genuinely immersive viewing experience suitable for most living room configurations while remaining accessible across a broad spectrum of price points. As streaming platforms have proliferated with high-definition and ultra-high-definition content libraries, consumers have gravitated toward mid-large screen formats that maximise the value of 4K and HDR content without the space constraints or cost premiums associated with ultra-large panels. The growing prevalence of dual-use setups where televisions simultaneously serve as home office displays and entertainment screens further reinforces demand within this size bracket.

Distribution Channel Insights

The Online distribution channel holds the dominant position in the Connected TV Market, capturing approximately 37% of total revenue share in 2024 and is projected to grow at a CAGR of 12.9% through 2030. The channel's leadership is driven by several structural advantages: e-commerce platforms enable consumers to access a far broader assortment of models, facilitate direct price comparison across competing brands, and offer transparent user reviews factors that are particularly valued when purchasing high-consideration consumer electronics. The COVID-19 pandemic permanently accelerated online purchasing habits globally, and continued improvements in logistics infrastructure, flexible return policies, and digital payment options have sustained this behavioural shift. Leading e-commerce platforms including Amazon, Flipkart, and JD.com, are serving as primary discovery and purchase channels for connected TVs across developed and developing markets alike.

Technology Insights

LED technology retains commanding leadership within the Connected TV Market's technology segmentation, accounting for approximately 54% of global revenue share in 2025. This dominance stems from LED's superior cost efficiency, energy-saving profile, broad manufacturing scalability, and availability across the widest range of screen sizes and price points from entry-level to mid-premium segments. LED's extensive production ecosystem enables manufacturers such as TCL Technology, Hisense Group, and Xiaomi Corporation to deliver competitively priced products that meet the needs of price-sensitive consumers in high-volume markets across Asia Pacific, Latin America, and parts of Europe. While OLED technology is gaining significant traction in the premium segment with the global OLED TV market reaching 6.43 million units in 2025LED's combination of affordability and performance continues to define the market's volume dynamics, ensuring its sustained category leadership through the forecast period.

End Use Analysis

The home use segment leads the connected TV Market by end-use category, representing approximately 84% of global market share in 2024. This dominance reflects the fundamental role of connected television as the cornerstone of household entertainment infrastructure globally. The growing penetration of multiple connected devices per household. homes average 3.5 connected streaming devices combined with rising time spent on connected TV platforms (exceeding 2 hours and 45 minutes per day on average among U.S. adults in 2025 per available consumption data) reinforces the home segment's structural leadership. The proliferation of affordable smart TV options, pre-installed streaming applications, and integrated voice assistants has made connected TVs increasingly accessible to a broader demographic.

Regional Insights

North America Connected TV Market Share and Trends

North America stands as the highest-value regional market for connected TVs globally, underpinned by the United States' position as the world's most mature OTT ecosystem and its leadership in connected TV advertising infrastructure. CTV penetration in the U.S. reached a record 90% of households in 2025, with industry tracker Comscore counting 96.4 million connected TV households. U.S. CTV advertising spending reached US$ 28.79 Bn in 2025 and is projected to reach US$ 46.9 Bn by 2029, reflecting the channel's growing primacy in national advertising budgets.

The U.S. innovation ecosystem, anchored by technology giants including Google, Apple, and Amazon, continues to push the frontier of AI-powered content personalization, voice-interface design, and cloud gaming integration through connected TVs. Canada represents an important secondary market within the region, with strong broadband penetration and a highly connected consumer base tracking closely behind U.S. adoption rates.

Europe Connected TV Market Share and Trends

Europe accounted for approximately 18.8% of global Connected TV Market revenue in 2025, with Germany, the United Kingdom, France, and Spain collectively representing the region's most significant demand centres. The U.K. market has been particularly active, with major broadcasters including the BBC, ITV, Channel 4, and Channel 5 partnering with Amazon in October 2024 to integrate their Freely streaming service into the Fire TV operating system, a landmark development marking the mainstream normalization of internet-delivered public broadcasting.

Germany is expected to register the highest CAGR in the region through 2030, driven by expanding broadband infrastructure, a large technology-oriented consumer base, and growing ecosystem partnerships between broadcasters and smart TV platform operators. The European Union's Ecodesign Regulation 2019/2024 imposes strict on-mode wattage ceilings that constrain the proliferation of power-intensive 8K panels, representing a meaningful regulatory headwind for ultra-premium display segments. Meanwhile, Spain and France are experiencing robust growth in streaming subscriptions, fueling replacement demand for connected TV hardware.

Asia Pacific Connected TV Market Share and Trends

Asia Pacific is both the dominant regional market accounting for approximately 38% of global Connected TV Market revenue in 2025, and the fastest-growing region, driven by the demographic and economic dynamism of China, India, Japan, and the broader ASEAN bloc. China remains the single largest national market within the region, propelled by a colossal consumer base, world-class electronics manufacturing capacity, dominant local streaming platforms including iQIYI and Tencent Video (which alone invests over US$ 2 Bn annually in content), and government-backed digital transformation programs.

India represents the region's most compelling growth frontier. The country's internet user base expanded from 251.59 million in 2014 to 954.40 million in 2024, including 398.35 million rural users, according to the Ministry of Communications. Operator-subsidized bundles from Reliance Jio and Airtel are driving smart TV penetration into tier-2 and tier-3 cities. Japan and South Korea anchor the region's premium connected TV segments, with proprietary OLED and QLED panel technologies from LG Display and Samsung Display commanding outsized revenue contributions.

Competitive Landscape

The connected TV market exhibits a moderately consolidated competitive structure, with the top four manufacturers Samsung Electronics, LG Electronics, TCL Technology, and Hisense Group collectively accounting for approximately 50% of global unit shipments in 2025, according to industry data. This concentration coexists with a dynamic and competitive mid-tier comprising brands such as Sony Corporation, Xiaomi Corporation, Panasonic Corporation, Philips, Sharp Electronics, Skyworth, and Haier Group.

Leading players are differentiating through proprietary operating systems, AI-powered display processing engines, and control of CTV advertising ecosystems. Key strategic trends include aggressive expansion into ad-supported platform revenue, forging pre-installation partnerships with major streaming services, and accelerating investment in next-generation display technologies including Micro RGB Mini-LED and advanced OLED panels.

Key Market Developments

- January 2025: Samsung Electronics unveiled its 2025 TV lineup at CES 2025, featuring Neo QLED and flagship OLED models powered by the next-generation AI processor, alongside major enhancements to personalized content delivery through its Tizen OS smart platform.

- February 2025: Mediaocean acquired Innovid to consolidate CTV advertising measurement infrastructure, a landmark transaction reflecting the accelerating migration of advertising budgets from traditional cable television to programmatic connected TV platforms.

Companies Covered in Connected TV Market

- Samsung Electronics

- LG Electronics

- Sony Corporation

- Panasonic Corporation

- Philips

- TCL Technology

- Xiaomi Corporation

- Hisense Group

- Sharp Electronics

- Roku, Inc.

- Skyworth

- Haier Group

Frequently Asked Questions

The global Connected TV Market is valued at US$ 11.4 Bn in 2026 and is projected to reach US$ 25.4 Bn by 2033, expanding at a CAGR of 12.1% during the forecast period. Historically, the market grew at an 11.0% CAGR between 2020 and 2025.

The primary demand drivers include the accelerating global shift from linear pay-TV to on-demand streaming platforms, rapid broadband and 5G network expansion enabling high-quality content delivery, technological advancements in OLED, QLED, and AI-powered display systems, and the explosive growth of CTV advertising ecosystems as marketers redirect budgets from traditional linear television.

The 30 to 50 Inches screen size segment is the dominant category in the Connected TV Market, accounting for approximately 61% of total revenue in 2024. This segment's leadership reflects consumer preference for immersive yet space-efficient displays that are compatible with 4K and HDR streaming content at accessible price points.

North America leads the global Connected TV Market in revenue value, driven by 90% household CTV penetration in the U.S. as of 2025, a deeply mature OTT content ecosystem, and the world's largest CTV advertising market. Asia Pacific, however, holds the largest share by unit volume and is the fastest-growing region in the forecast period.

The leading companies operating in the global Connected TV Market include Samsung Electronics, LG Electronics, Sony Corporation, TCL Technology, Hisense Group, Xiaomi Corporation, Panasonic Corporation, Philips, Roku, Inc., Sharp Electronics, Haier Group, and Skyworth, among others. Samsung and LG collectively dominate premium segments, while TCL and Hisense lead in volume-driven mid-range categories.