- Marine

- Connected Ship Market

Connected Ship Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

Connected Ship Market by Ship Type (Commercial Ships, Defense & Naval Ships), Installation (Onboard, Onshore), Fit Type (Line Fit, Retro Fit, Hybrid Fit), Application (Fleet Operations, Vessel Traffic Management, Fleet Health Monitoring/Predictive Maintenance, Navigation & Bridge Systems, Cargo & Performance Monitoring), and Region Analysis for 2026 to 2033

Connected Ship Market Trends & Analysis

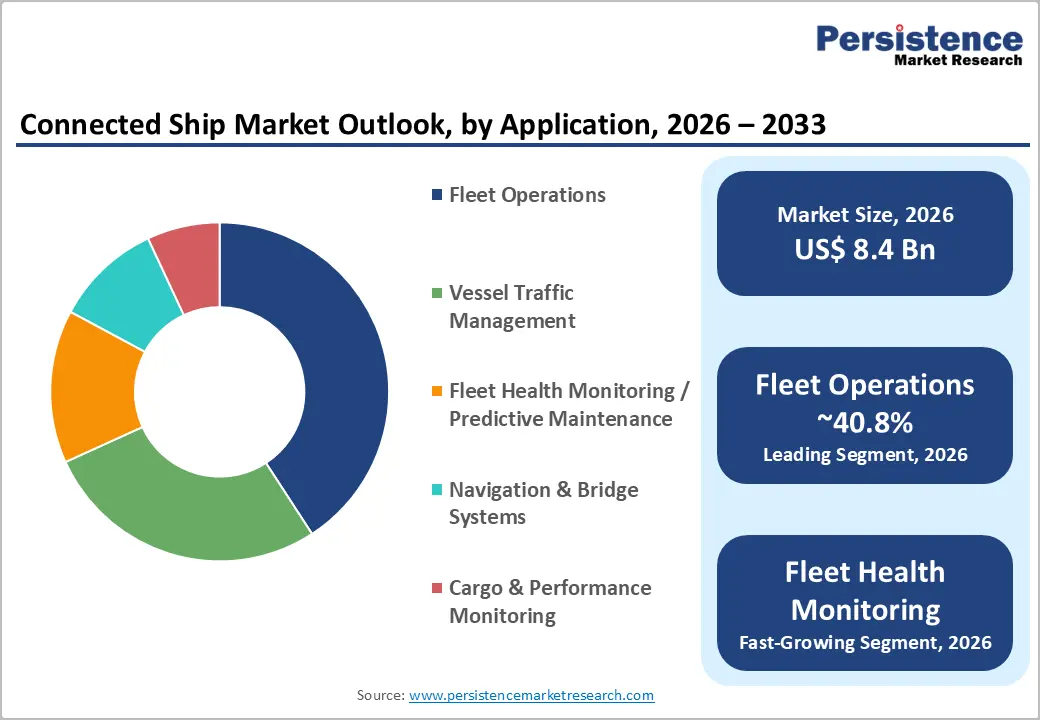

The global connected ship market size is anticipated at US$ 8.4 billion in 2026 and is projected to reach US$ 14.6 billion by 2033, growing at a CAGR of 8.1% between 2026 and 2033. IMO CII and e-navigation mandates are accelerating digital compliance adoption across 45,000+ globally tracked vessels; LEO satellite bandwidth costs declined 38% between 2022 and 2024; maritime IoT device deployments exceeded 8 million units in 2024; and 52% of shipping companies reported 12% fuel savings from real-time connectivity investments.

IMO regulatory compliance frameworks, declining LEO satellite connectivity costs, and AI-powered predictive maintenance adoption are the primary structural growth drivers for the Connected Ship Market. The historical 7.7% CAGR from 2020 to 2026 reflects consistent technology investment by commercial and naval fleet operators seeking operational efficiency and decarbonization alignment.

Key Industry Highlights:

- Leading Ship Type: Commercial Ships lead at 64.4% share (US$ 5.43 Bn); Defense & Naval Ships to achieve a fast-growth at a leading CAGR, driven by NATO digital interoperability mandates and Indo-Pacific naval fleet connectivity expansion globally.

- Leading Application: Fleet Operations leads at 40.8% share (US$ 3.44 Bn); Fleet health monitoring at 10% CAGR, with IoT sensor installations growing 26% YoY in 2023 - 2024 at tanker and bulk carrier predictive maintenance programs.

- Leading Fit Type: Line Fit leads at 57.5% share (US$ 4.85 Bn); Hybrid Fit grow fast at 9% CAGR, driven by mixed-age fleet operators modernizing partially equipped vessels with LEO and AI analytics upgrades by 2033.

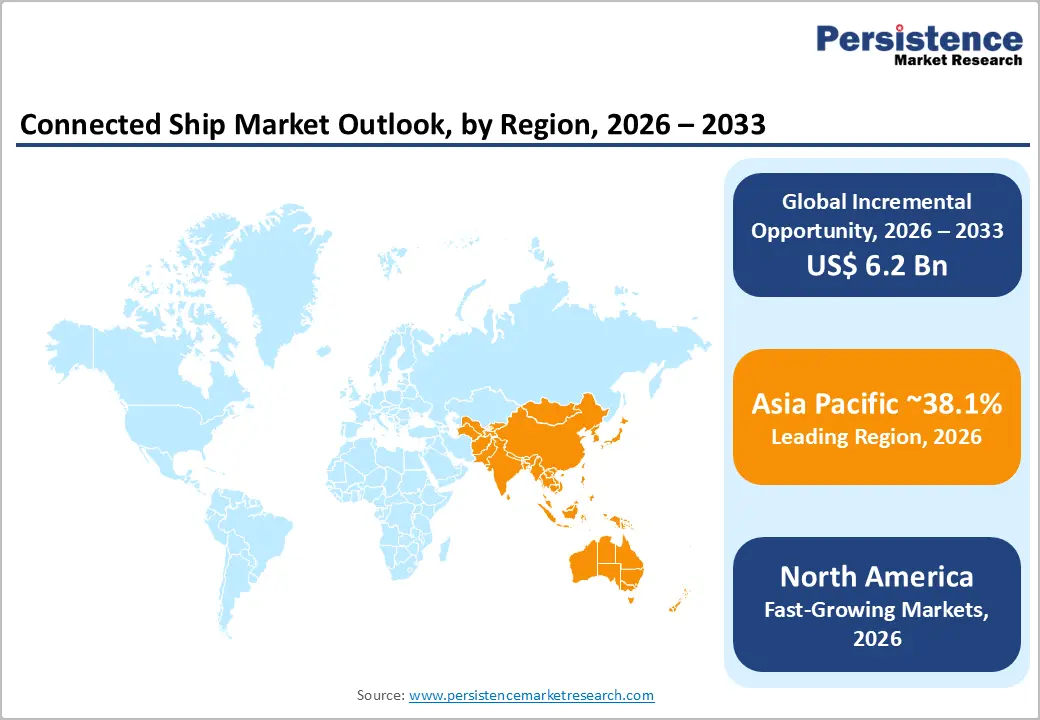

- Regional Leader: Asia Pacific leads at 38.5% share (China US$ 1.5 Bn, India US$ 335 Mn) at 9% CAGR by 2033.

- Strategic Milestone: Northrop Grumman's US$ 420 Mn U.S. Navy DDG-51 C4ISR contract (February 2025) and Wärtsilä's Fleet Intelligence EU ETS compliance platform launch (March 2025) signal regulatory compliance and naval digitalization as twin structural growth catalysts through 2033.

Market Dynamics Analysis

Drivers - IMO e-Navigation, CII Carbon Intensity Reporting, and Maritime Single Window Compliance Mandating Real-Time Digital Connectivity

The International Maritime Organization's Carbon Intensity Indicator (CII) regulation, effective January 2023 and enforceable across all vessels above 5,000 GT operating internationally, mandates annual fuel consumption, distance sailed, and emissions reporting that requires continuous onboard sensor data collection, automated voyage reporting systems, and shore-based analytics dashboards directly linked to ships in real time. IMO's e-Navigation Strategic Implementation Plan and the Maritime Single Window framework, requiring standardized electronic port entry reporting across 168 IMO member states by 2025, are making baseline digital connectivity infrastructure a regulatory compliance prerequisite rather than an operational enhancement across all commercial and naval fleet categories globally.

European Union's Fit for 55 legislative package, incorporating FuelEU Maritime regulation mandating GHG intensity reduction of 2% by 2025, 6% by 2030, and 80% by 2050, is creating structured investment demand for connected ship monitoring platforms at EU-flagged and EU port-calling vessels requiring real-time fuel blending, emissions tracking, and regulatory reporting system integration. The EU's Emissions Trading System (ETS) maritime inclusion from January 2024, charging shipping companies for 50% of verified CO2 emissions on EU voyages in 2024, scaling to 100% by 2026, is creating direct financial incentives for real-time fuel efficiency monitoring connectivity investments that reduce ETS liability exposure through voyage optimization.

LEO Satellite Connectivity Proliferation and IoT Maritime Data Platform Expansion Enabling Cost-Effective Fleet Digitalization

Starlink Maritime's global expansion, achieving commercial maritime service coverage across 100+ countries by 2024 at bandwidth costs 60-70% below legacy VSAT geostationary satellite pricing, is fundamentally restructuring the economic viability of always-on, high-bandwidth connected ship data services for mid-tier and smaller commercial fleet operators previously unable to justify VSAT investment at legacy pricing levels. SpaceX Starlink Maritime, OneWeb, and Telesat Lightspeed LEO constellation services collectively reduced round-trip latency for maritime broadband from 600-800 ms (GEO) to 20-40 ms (LEO), enabling cloud-based real-time vessel monitoring, AI-powered bridge navigation assistance, and high-definition video conferencing for seafarer crew welfare at production-grade quality levels.

The global maritime satellite communications market, valued at US$ 3.2 Bn in 2024 at 9.1% CAGR, represents the connectivity infrastructure investment layer upon which connected ship IoT monitoring, performance analytics, and autonomous navigation platforms are built. Marlink's December 2024 deployment of Sealink NextGen across 24 Thoresen Shipping vessels, integrating VSAT and Starlink LEO services for hybrid connectivity with network security management, exemplifies the fleet-scale digitalization investment pattern LEO cost reduction is enabling across mid-tier commercial shipping operators globally.

Restraints - Maritime Cybersecurity Threat Escalation Constraining Connected Ship Technology Adoption Velocity

The International Maritime Organization's MSC-FAL.1/Circ.3 cybersecurity guidelines, requiring cyber risk management integration into Safety Management Systems by January 2021, have created compliance complexity at shipping companies where over 60% of maritime organizations reported at least one significant cyber incident in 2023 (BIMCO Cybersecurity Survey, 2024), with connected ship IoT sensor networks expanding vessel attack surfaces across navigation, propulsion, and cargo handling systems. Nation-state GPS spoofing incidents affecting over 1,300 vessels in the Black Sea and Eastern Mediterranean in 2023-2024 demonstrate operational safety risks that create fleet operator hesitancy toward full IoT connectivity deployment across legacy vessel bridge and navigation system architectures.

Interoperability Fragmentation Across Connected Ship Platform Standards and Legacy Onboard System Integration

The global commercial fleet encompasses over 55,000 vessels operating heterogeneous bridge, engine room, and cargo management systems, spanning IEC 61162 NMEA 2000, NMEA 0183, and proprietary OEM protocols from ABB, Wärtsilä, MAN, and Rolls-Royce Marine, creating integration complexity that extends connected ship platform deployment timelines by 8-18 months per vessel when retrofitting legacy automation architectures.

IHO S-100 universal hydrographic data standard and IEC 63173 SECOM maritime communication standard adoption remains incomplete across port authority and vessel traffic management systems, with fewer than 35% of global port authorities operating fully S-100-compatible vessel traffic management infrastructure as of 2024, constraining end-to-end connected ship data ecosystem interoperability.

Opportunities - Autonomous and Semi-Autonomous Vessel Development Creating Comprehensive Connected Ship System Integration Demand

Over 20% of new ship orders in 2024 included provisions for autonomous navigation and remote-operation systems (DNV GL, Maritime Forecast to 2050, 2024 Edition), requiring comprehensive onboard IoT sensor arrays, AI-powered decision support systems, high-bandwidth LEO satellite connectivity, and shore-based remote vessel monitoring infrastructure that collectively represent the highest-specification connected ship technology procurement programs in the market. Rolls-Royce Marine's Intelligent Awareness System, Kongsberg's K-Bridge autonomous navigation, and Wärtsilä's Fleet Operations Centre remote monitoring, each targeting commercial ferry, ro-pax, and offshore supply vessel autonomous operation programs, are creating end-to-end connected ship system integration contracts valued at US$ 8-25 Mn per vessel in full autonomy-ready specification.

The autonomous shipping market, estimated at US$ 135 Bn by 2030 at 12.6% CAGR (DNV GL), requires every autonomous vessel to operate as a fully connected node within a shore-based vessel management network, making connected ship technology platforms a mandatory infrastructure prerequisite for autonomous shipping program deployment globally through 2033. This creates a US$ 2.8-3.5 Bn connected ship technology opportunity concentrated at autonomous and semi-autonomous commercial vessel programs in Nordic, Japanese, and South Korean shipbuilding markets through 2033.

Category-wise Analysis

Ship Type Insights

Commercial ships lead the ship type segment with a 64.4% market share in 2026, estimated at approximately US$ 5.43 Bn, anchored by the global commercial fleet of 55,000+ vessels requiring IMO CII compliance monitoring, LEO satellite connectivity upgrades, and AI fleet performance optimization across container shipping, tanker, bulk carrier, and ro-ro vessel categories generating the largest absolute connected ship technology procurement volume globally.

Commercial ships' IMO regulatory compliance investment obligations, ETS, CII, and Maritime Single Window, create non-discretionary connected ship platform procurement at fleet operator level that sustains commercial segment revenue leadership versus defense applications. No structural dominance shift is anticipated through 2033, as commercial fleet connected ship compliance-driven demand remains structurally mandated by IMO and EU regulatory frameworks.

Defense & Naval Ships are the fastest-growing ship type at 8.5% CAGR through 2033. NATO digital interoperability mandates, Indo-Pacific naval fleet expansion programs, and AI-powered tactical awareness system integration driving 18% YoY naval connectivity investment growth in 2024 collectively sustain defense segment's accelerating connected ship market share gain through 2033 globally.

Installation Insights

Onboard installation leads with a 68.9% share in 2026, estimated at approximately US$ 5.81 Bn, reflecting the fundamental requirement for integrated onboard IoT sensor networks, bridge navigation systems, engine room monitoring platforms, and VSAT/LEO antenna hardware as the primary hardware and software investment concentration point for connected ship technology deployments.

Onboard installation's lead reflects the physical necessity of vessel-side hardware deployment for any connected ship system, navigation sensors, emission monitors, predictive maintenance IoT nodes, and communication antenna arrays each requiring onboard installation as the primary procurement category. Onshore monitoring infrastructure is growing faster but remains structurally secondary to onboard deployment investment at fleet operator procurement level through 2033.

Onshore installation is the fast-growing segment at 8.4% CAGR through 2033. Shore-based fleet operations centers, port vessel traffic management AI platforms, remote vessel monitoring dashboards, and cloud-based maritime analytics infrastructure, expanding as fleet operators centralize multi-vessel operational oversight, are driving onshore connected ship investment acceleration at shipping company and port authority procurement programs globally through 2033.

Fit Type Insights

Line fit leads the fit type segment with a 57.5% share in 2026, estimated at approximately US$ 4.85 Bn, driven by new vessel orders incorporating factory-integrated connected ship technology specifications at design stage, where Hyundai Heavy Industries, Daewoo, Samsung Heavy Industries, and CSSC shipyards are standardizing IoT sensor arrays, bridge navigation connectivity, and VSAT antenna factory installation as default new-build specifications across container ship, LNG carrier, and naval vessel programs.

Line fit's dominance reflects the growing newbuild specification trend where connected ship capability is a baseline classification requirement at DNV, Lloyd's Register, and Bureau Veritas, with line fit installations commanding 25-35% cost efficiency advantages over equivalent retrofit configurations due to integrated installation at build stage.

Hybrid Fit is the fast-growing fit type at 9% CAGR by 2033. Hybrid fit configurations, combining factory-integrated sensor infrastructure with field-retrofitted AI analytics and LEO satellite communication upgrades, enable fleet operators to modernize mixed-age vessel fleets cost-effectively by upgrading connectivity and analytics capabilities on partially equipped line-fit vessels, driving adoption across large tanker and bulk carrier fleets globally through 2033.

Application Insights

Fleet operations leads the application segment with a 40.8% market share in 2026, estimated at approximately US$ 3.44 Bn, anchored by voyage optimization, fuel management, port call scheduling, and cargo loading optimization applications that deliver the most immediately quantifiable ROI for connected ship investment, with fleet operators reporting average 12% fuel cost reduction per voyage through real-time telemetry and route optimization platforms. Fleet operations' application leadership reflects the commercial fleet operator's primary connected ship value driver, operational cost reduction through real-time voyage analytics, which sustains procurement priority over other application categories. No dominance shift is anticipated, as fuel efficiency ROI remains the primary fleet operator connected ship investment justification through 2033.

Fleet health monitoring/predictive maintenance is the fast-growing application at 10% CAGR through 2033. Fleet health monitoring IoT sensor installations grew 26% YoY between 2023 and 2024, driven by predictive maintenance adoption at tanker and bulk carrier operators reducing unscheduled dry-docking costs by an estimated 15-22% per maintenance cycle, sustaining application segment's accelerating growth through 2033 globally.

Regional Insights

North America Connected Ship Market Trends

North America is likely to achieve a prominent 7.7% CAGR holding approximately 23.4% of global share in 2026. Major trends include U.S. Navy digital fleet modernization programs, U.S. Coast Guard vessel traffic management infrastructure investment, and commercial shipping operators adopting LEO satellite and AI-powered fleet monitoring platforms aligned with U.S. DOT Maritime Administration digital transformation initiatives.

U.S. Connected Ship Market: Navy C4ISR Leadership, USCG VTS Investment, and LEO Maritime Connectivity

The United States holds approximately US$ 1.9 Bn in 2026, driven by U.S. Navy's US$ 4.2 Bn annual C4ISR and naval connectivity procurement (U.S. DoD FY2025 Budget), Northrop Grumman's ship integration systems, and L3Harris tactical maritime communication platforms. USCG Nationwide AIS Network expansion and DOT MARAD's Maritime Transportation System digitalization investments sustain structured federal connected ship procurement. Canada contributes through Royal Canadian Navy fleet connectivity upgrades and Transport Canada AIS-linked vessel traffic management infrastructure across Pacific and Atlantic maritime zones.

North America's growth is sustained by U.S. Navy C4ISR digital fleet integration, USCG vessel traffic management AI platform investment, and Starlink Maritime commercial fleet adoption across Gulf of Mexico energy sector and Pacific container shipping operator connectivity upgrade programs through 2033.

Europe Connected Ship Market Trends

Europe holds a 24.2% share of the global connected ship market in 2026, estimated at approximately US$ 2.04 Bn, driven by EU FuelEU Maritime and ETS regulatory compliance investment demand, EMSA vessel tracking infrastructure, Kongsberg and Wärtsilä Nordic maritime technology OEM leadership, and BIMCO industry standard harmonization facilitating pan-European connected ship platform adoption at EU-flagged and EU port-calling commercial fleet operators.

Germany Connected Ship Market: ETS Compliance, Nordic OEM Leadership, and Smart Port Integration

Germany holds approximately US$ 405.3 Mn in 2026, anchored by Hamburg Port Authority smart port VTS infrastructure, Thyssenkrupp Marine Systems naval connectivity programs, and German flagged tanker and container fleet ETS compliance monitoring investments. The U.K. sustains Inmarsat (now Viasat) maritime SATCOM leadership and Royal Navy connected platform upgrades. France contributes through CMA CGM fleet digitalization and Marine Nationale naval modernization. Spain expands through Navantia naval shipbuilding connected system integration and Barcelona port smart VTS investment.

Europe's EU ETS maritime compliance driving fleet connectivity investment, EMSA digital maritime infrastructure expansion, and Nordic OEM connected ship platform innovation sustain structured high-value connected ship procurement across European commercial and defense maritime markets through 2033.

Asia Pacific Connected Ship Market Trends

Asia Pacific is the fast-growing market at 9% CAGR by 2033, commanding approximately 38.5% of global Connected Ship Market share in 2025, driven by China's world-largest commercial fleet connected ship upgrade program, Japan's autonomous shipping technology leadership, South Korean shipbuilding newbuild line-fit connected specification integration, and India's expanding coast guard and naval fleet digitalization investments.

China Connected Ship Market: Fleet Scale, Autonomous Shipping, and Naval Modernization

China holds US$ 1.5 Bn in 2026, driven by COSCO Shipping's IoT fleet management platform across 1,300+ vessels, China Classification Society (CCS) smart ship notation requirements mandating connected monitoring at newbuilds, and Beidou satellite navigation maritime adoption expanding domestic connectivity. India at US$ 335 Mn expands through Indian Navy's US$ 6.8 Bn acquisition program and Sagarmala port digitalization. Japan sustains NYK Line's autonomous ferry program and Mitsui OSK Lines connected ship leadership. ASEAN grows through PSA Singapore and Port Klang smart port VTS deployments.

Asia Pacific's China fleet-scale IoT connectivity upgrades, Japan autonomous shipping connected infrastructure investment, South Korean newbuild line-fit integration, and India naval digitalization program collectively sustain the region's dual leadership and growth trajectory by 2033.

Competitive Landscape

The global connected ship market is moderately consolidated, with Wärtsilä, Kongsberg, Northrop Grumman, L3Harris, and Inmarsat (Viasat) collectively holding approximately 45-52% of global revenue share, while specialized maritime IoT platform providers including Marlink, Nauticus Robotics, and ABB Marine compete on application-specific fleet analytics and communication service differentiation. Satellite communication bandwidth partnerships with LEO providers, IMO compliance platform certification, and AI-powered digital twin vessel analytics are primary competitive differentiation levers.

AI-powered fleet performance analytics deepening, autonomous vessel connectivity platform development, defense C4ISR maritime integration, and Asia Pacific commercial fleet digitalization program expansion define the dominant competitive strategic investment themes for all connected ship market participants.

Strategic Developments

- In December 2024, Marlink deployed its Sealink NextGen hybrid VSAT and Starlink LEO connectivity solution across 24 Thoresen Shipping vessels, delivering enhanced network security, application performance management, and fleet digitalization across Thoresen's Asia Pacific commercial tanker and cargo fleet operations.

- In February 2025, Northrop Grumman secured a US$ 420 Mn U.S. Navy contract for integrated ship system C4ISR connectivity upgrades across the DDG-51 Arleigh Burke-class destroyer fleet, delivering encrypted tactical data link, multi-domain sensor fusion, and real-time naval network interoperability aligned with U.S. Navy Distributed Maritime Operations doctrine.

Connected Ship Market - Key Insights & Scope

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 5.4 Bn |

| Current Market Value (2026) | US$ 8.4 Bn |

| Projected Market Value (2033) | US$ 14.6 Bn |

| CAGR (2026 - 2033) | 8.1% |

| Leading Region | Asia Pacific |

| Dominant Ship Type | Commercial Ships - 64.4% |

| Top-ranking Application | Fleet Operations - 40.8% |

| Incremental Opportunity | US$ 6.2 Bn |

Companies Covered in Connected Ship Market

- Wärtsilä Corporation

- Kongsberg Gruppen AS

- Northrop Grumman Corporation

- L3Harris Technologies Inc.

- Inmarsat (Viasat Inc.)

- Marlink Group

- ABB Ltd. (Marine & Ports)

- Thales Group

- Raytheon Technologies (RTX)

- General Electric (GE Vernova)

- Rolls-Royce Marine (Automated Ships)

- ORBCOMM Inc.

- Garmin International Inc.

- Nauticus Robotics Inc.

- Furuno Electric Co., Ltd.

Frequently Asked Questions

The connected ship market is likely to be valued at US$ 8.43 Bn in 2026, projected to reach US$ 14.58 Bn by 2033, delivering an incremental opportunity of US$ 6.15 Bn through 2033.

IMO CII and EU ETS compliance mandating real-time emissions monitoring, LEO satellite bandwidth cost reduction of 60-70% enabling affordable fleet connectivity, and AI-powered predictive maintenance delivering 15-22% dry-docking cost savings are the primary growth drivers.

The connected ship market is likely to reach a CAGR of 8.1% from 2026 to 2033, building on a historical CAGR of 7.7% from 2020 to 2026.

Autonomous vessel connected infrastructure representing US$ 2.8-3.5 Bn opportunity through 2033 and NATO-aligned naval fleet digitalization with defense programs generating 3-5x higher contract value per vessel versus commercial applications are the highest-value growth opportunity pools.

Wärtsilä, Kongsberg, Northrop Grumman, L3Harris, Inmarsat (Viasat), Marlink, ABB Marine, Thales, RTX, GE Vernova, Rolls-Royce Marine, ORBCOMM, Garmin, Nauticus Robotics, and Furuno Electric are the leading global Connected Ship market participants.