- Off-Road Equipment & Machinery

- Concrete Batching Plant Market

Concrete Batching Plant Market Size, Share, and Growth Forecast 2026 - 2033

Concrete Batching Plant Market by Product Type (Stationary Batch Plant, Mobile Batch Plant), Mix Type (Wet Concrete Mix, Dry Concrete Mix), Application (Residential Construction, Others), End-user (Construction Companies, Government Agencies), and Regional Analysis for 2026 - 2033

Concrete Batching Plant Market Size and Trend Analysis

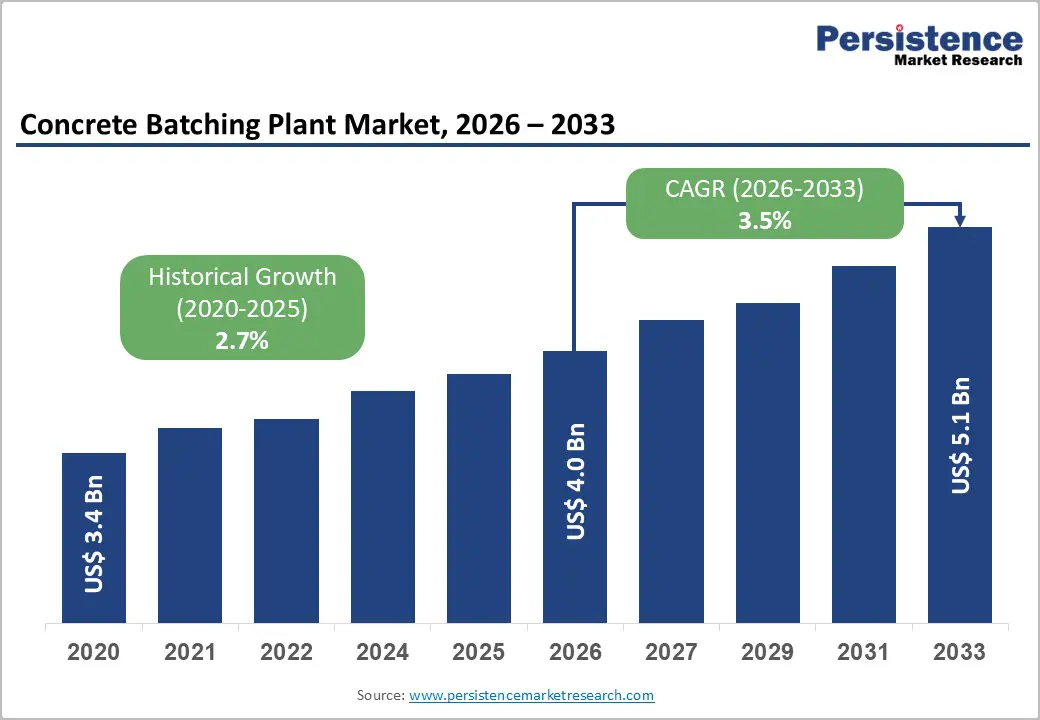

The global concrete batching plant market size is likely to be valued at US$4.0 billion in 2026 and is expected to reach US$5.1 billion by 2033, growing at a CAGR of 3.5% during the forecast period from 2026 to 2033, driven by rising public and private infrastructure spending, rapid urbanization across Asia Pacific and the Middle East, and the increasing shift toward ready-mix concrete for large-scale residential, commercial, and infrastructure developments.

Growing emphasis on construction quality, consistency, and regulatory compliance is accelerating the adoption of automated and high-capacity batching plants. Smart-city programs, transport corridor expansion, and renewable energy projects are supporting sustained demand for both stationary and mobile plants.

Key Market highlights

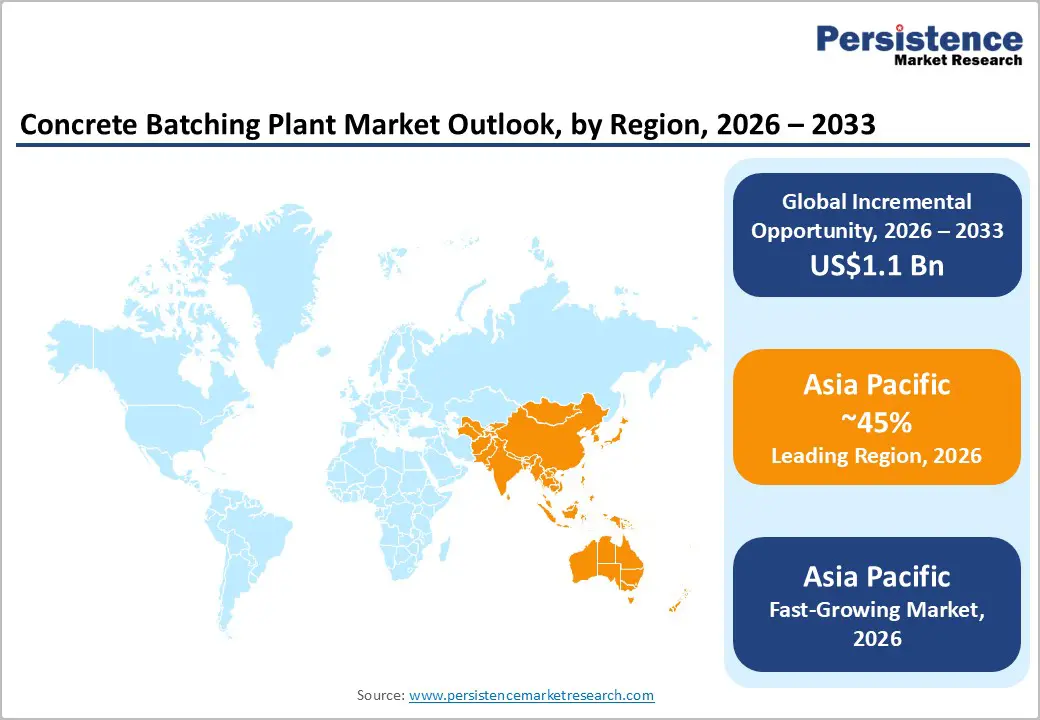

- Leading Region: Asia Pacific is anticipated to be the leading region, accounting for a market share of 45% in 2026, driven by extensive urbanization and high construction spending across China, India, Japan, and ASEAN.

- Fastest-Growing Region: Asia Pacific is likely to be the fastest-growing region in the concrete batching plant market in 2026, driven by massive infrastructure expansion, smart-city development, and rapid urbanization across emerging economies.

- Leading Product Type: Stationary batching is projected to be the leading product type in 2026, accounting for 60% of revenue share, driven by its high-capacity output, suitability for continuous operation, and strong demand from urban RMC producers and large infrastructure hubs.

- Leading Mix Type: Wet concrete mix is expected to be the leading mix type, accounting for over 68% of revenue share, owing to superior quality control, greater consistency, and strong adoption in urban, infrastructure, and precast applications.

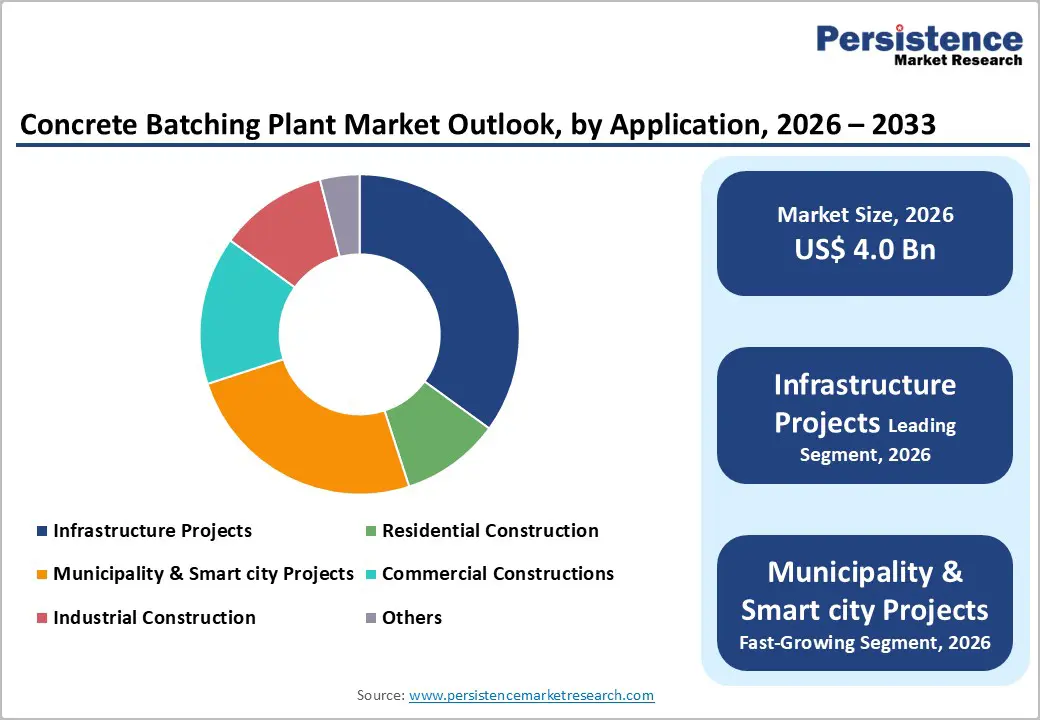

- Leading Application Type: Infrastructure projects are expected to represent the leading application type in 2026, accounting for 40% revenue share, driven by high-volume requirements across highways, metros, airports, bridges, and major public works.

- Leading End-user Type: Construction companies are anticipated to be the leading end-user, accounting for over 75% revenue share, driven by EPC contractors, RMC producers, and large private developers that prioritize productivity, automation, and networked plant operations.

| Key Insights | Details |

|---|---|

|

Concrete Batching Plant Market Size (2026E) |

US$4.0 Bn |

|

Market Value Forecast (2033F) |

US$5.1 Bn |

|

Projected Growth CAGR (2026-2033) |

3.5% |

|

Historical Market Growth (2020-2025) |

2.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Shift to Ready-Mix and Quality Compliance

Construction stakeholders are placing greater emphasis on consistency, speed, and quality assurance. Ready-mix concrete production allows precise control over mix designs, water–cement ratios, and admixture dosing, which is essential for meeting the performance demands of modern infrastructure, high-rise structures, and large commercial projects. Centralized batching plants reduce reliance on manual labor, limit variability, and deliver uniform strength and durability across large volumes, making them the preferred choice for schedule-driven and quality-critical developments.

Tighter quality and regulatory standards are also influencing procurement decisions. Governments, developers, and EPC contractors are increasingly adopting performance-based specifications, durability benchmarks, and traceability requirements for concrete used in both public and private projects. This shift is boosting demand for automated batching plants with digital controls, real-time monitoring, batch data logging, and compliance reporting capabilities. Environmental regulations addressing dust emissions, material waste, and sustainable construction practices further support this transition. Together, the rising adoption of ready-mix concrete and stricter quality compliance requirements are driving increased investment in advanced, high-performance concrete batching plants across global markets.

High Upfront Capital and Lifecycle Costs

Modern concrete batching plants are increasingly equipped with advanced automation, high-accuracy weighing systems, automated material handling, dust-suppression technologies, and digital monitoring platforms to meet stringent quality and regulatory standards. While these innovations improve productivity, consistency, and compliance, they also substantially raise initial capital requirements, making plant ownership difficult for small and mid-sized contractors. Significant upfront investment is needed for site development, foundations, power infrastructure, and commissioning, particularly for large-capacity stationary plants. As a result, high entry barriers persist, restricting adoption mainly to large construction firms and well-established ready-mix producers with strong financial capacity.

Lifecycle costs limit the broader deployment of batching plants. Ongoing expenses for regular calibration, preventive maintenance, mixer wear components, conveyor systems, and software upgrades are essential to sustain quality and performance. Operating automated plants also requires skilled personnel to manage systems and comply with safety and environmental regulations. Escalating energy prices, spare-part replacements, and tighter dust and emission norms further increase operating costs over time. For short-term projects or markets with variable demand, extended payback periods weaken returns on investment, prompting many contractors to opt for plant rentals, outsourced ready-mix supply, or conventional on-site mixing rather than owning batching plants outright.

Emerging Markets and Smart City Programs

Rapid urbanization, population growth, and rising infrastructure investments are driving demand for consistent, high-quality concrete across residential, commercial, and public projects. Governments and private developers are prioritizing safety, structural durability, and faster project execution, which favors the adoption of ready-mix concrete supplied through stationary and mobile batching plants. As construction scales up in these regions, batching plants play a critical role in ensuring uniform quality, reducing material wastage, and supporting compliance with evolving building standards.

Smart city programs and decentralized infrastructure planning are creating new avenues for growth. Many countries are empowering state and municipal authorities to execute urban development projects, increasing the number of mid-scale and distributed construction sites. These include satellite cities, peri-urban transport corridors, industrial parks, and utility networks, all of which require reliable and localized concrete supply. This trend is boosting demand for both flexible mobile plants and compact stationary units. Emerging markets and smart city initiatives offer growth opportunities for batching plant manufacturers and operators focused on scalable, efficient, and technology-enabled solutions.

Category-wise Analysis

Product Type Insights

Stationary batching plants are expected to lead the concrete batching plant market, accounting for approximately 60% revenue share in 2026, supported by their high-capacity output, stable operation, and suitability for long-duration projects. These plants are widely used by ready-mix producers, EPC contractors, and urban infrastructure developers who require continuous concrete supply with tight quality control. Their integrated high-capacity storage, advanced mixers, and automated monitoring make them the preferred choice for major cities, industrial hubs, and large infrastructure corridors. For example, large metro rail and airport expansion projects commonly deploy high-capacity stationary plants, while urban ready-mix leaders operate centralized batching hubs to serve dense metropolitan construction zones.

Mobile batching plants are likely to represent the fastest-growing product type in 2026, driven by the expansion of projects into remote, dispersed, or fast-changing locations. The latest mobile and containerized models offer higher output, compact modular designs, and quick setup, enabling contractors to operate profitably on shorter-duration or geographically distributed sites. Strongest growth comes from highways, renewable energy sites, mining zones, and large greenfield projects where mobility cuts logistics and transport costs. For example, national highway packages often use mobile plants relocated along corridors, while wind and solar farm foundations rely on mobile batching units deployed close to project sites.

Mix Type Insights

Wet concrete mix is projected to lead the market, capturing around 68% revenue share in 2026, driven by its ability to consistently deliver high-quality, high-strength concrete for critical applications such as high-rise buildings, metro systems, expressways, bridges, and precast manufacturing. As mixing occurs inside the plant, producers maintain precise control over workability, strength, and durability parameters essential for projects requiring strict compliance, digital traceability, and repeatable performance. For example, metro rail projects and urban flyover construction typically mandate wet mix plants to meet durability and uniformity standards. Precast concrete yards supplying bridge and tunnel segments rely heavily on wet mix plants to ensure dimensional accuracy and consistent strength.

Dry mix is likely to be the fastest-growing segment in 2026, as it continues to be used by regional ready-mix suppliers serving small towns and peri-urban markets, where shorter haul distances and lower production volumes make transit mixing economical. Dry mix systems are also commonly deployed in temporary infrastructure works, such as rural road widening, drainage upgrades, and utility trenching, where project duration is limited and permanent plant installation is not viable. In several emerging markets, small municipal contractors rely on dry mix plants to support local housing schemes and basic public works due to the lower capital requirements of these plants. Performance-based specifications, durability standards, and digital batch traceability become more widespread, investment momentum continues to shift toward wet mix plants.

Application Type Insights

Infrastructure projects are expected to dominate the application segment in 2026, contributing approximately 40% of revenue, driven by strong demand for concrete and government initiatives focused on long-term asset creation. Major national programs, such as India’s Bharatmala and Sagarmala initiatives for highways, logistics parks, and ports, as well as China’s high-speed rail and expressway expansion, rely heavily on high-capacity stationary and on-site batching plants to maintain a consistent supply and ensure quality compliance. The increasing adoption of performance-based specifications, durability-focused mix designs, and digital quality verification is further boosting demand for advanced batching solutions across highways, metro systems, dams, and airports.

Municipality and smart city projects are projected to be the fastest-growing application segment in 2026, driven by integrated urban master plans that combine mobility, housing, utilities, and sustainability objectives. Programs such as India’s Smart Cities Mission and Saudi Arabia’s NEOM and Vision 2030 urban developments increasingly require certified concrete mixes, automated documentation, and low-carbon formulations. These initiatives favor modern batching plants equipped with IoT-based monitoring, automated dosing, and eco-efficient designs, particularly for stormwater management, green mobility corridors, affordable housing, and utility infrastructure, thereby supporting sustained demand at both city and municipal levels.

End-user Type Insights

Construction companies are expected to lead the end-user segment, accounting for approximately 75% revenue share in 2026, driven by large EPC contractors, infrastructure developers, and ready-mix concrete (RMC) producers that operate multi-plant batching networks. These players prioritize uptime, automation, and lifecycle efficiency to support continuous concrete supply across parallel projects. For example, L&T Construction operates captive and project-based batching plants across metro rail, highway, and industrial projects in India, while UltraTech Concrete, the RMC arm of UltraTech Cement, runs one of the largest batching networks supplying urban infrastructure and commercial construction. Such companies consistently invest in high-capacity stationary plants and advanced mobile units to optimize logistics, quality, and cost control.

Government agencies are likely to represent the fastest-growing segment in 2026, driven by rising public infrastructure spending and stronger in-house execution capabilities. Many public bodies now deploy their own batching plants to ensure quality compliance and timely delivery. For example, the National Highways Authority of India (NHAI) and its EPC partners use dedicated on-site batching plants for expressway and corridor projects, while state irrigation and water resources departments operate captive plants for dam and canal construction. Similarly, metro rail corporations across Asia increasingly rely on government-controlled batching facilities to meet strict performance, durability, and traceability standards.

Regional Insights

North America Concrete Batching Plant Market Trends

North America’s batching plant market is characterized by the modernization of an aging infrastructure and strong demand for technology-driven solutions. The U.S. and Canada are increasingly deploying automated and IoT-enabled batching plants to meet rigorous quality standards, regulatory pressure, and sustainability goals. A significant portion of recent growth is driven by mobile batching plants, particularly for highway expansion, wind-energy foundations, and construction in remote locations. For example, CEMEX USA has been upgrading and deploying automated and mobile batching plants across multiple states to support large transportation and infrastructure projects while improving operational efficiency and quality consistency.

North American operators are also investing heavily in energy-efficient systems, low-emission mixers, and water-recycling technologies to reduce environmental impact and comply with tightening regulations. The market benefits from sustained federal infrastructure funding, including U.S. infrastructure programs, alongside rising adoption of performance-based mix designs. Retrofit activity remains strong, as many legacy batching plants are being modernized with advanced controls, remote monitoring, and emission-reduction systems to extend asset life and improve productivity.

Europe Concrete Batching Plant Market Trends

Europe is likely to be a significant market for concrete batching plants, due to its strong focus on sustainability, stringent regulatory frameworks, and continued investments in infrastructure modernization. The region is heavily influenced by EU environmental policies, which mandate lower emissions, energy efficiency, and improved dust and wastewater management. As a result, demand is shifting toward advanced, eco-efficient batching plants with precise dosing, optimized material handling, and reduced carbon footprints. For example, Ammann Group has expanded its range of environmentally optimized batching plants in Europe, emphasizing energy efficiency, low-emission operation, and modular designs to meet EU compliance standards.

Digitalization is transforming plant operations across Europe. The adoption of IoT-enabled batching, predictive maintenance, and mix traceability is becoming standard as contractors aim to reduce waste, improve consistency, and achieve higher certification levels. Manufacturers such as Liebherr and Ammann are supporting this shift by offering modular, digitally integrated plants that comply with EU sustainability and automation standards. Eastern Europe is emerging as a strong growth pocket, supported by EU-funded infrastructure projects, road expansion, and industrial development. Rising cross-border logistics hubs and urban redevelopment programs are accelerating demand for modern, compliant batching solutions across the region.

Asia Pacific Concrete Batching Plant Market Trends

Asia Pacific is expected to be the leading region in the concrete batching plant market, accounting for 45% of market share in 2026, driven by massive construction activity, rapid urbanization, and sustained government investment in transport, energy, and industrial infrastructure. Countries such as China, India, Japan, South Korea, and ASEAN members continue to undertake long-term programs involving highways, metros, airports, industrial corridors, and mass-housing initiatives, all of which require high-capacity and reliable batching operations. For example, Schwing Stetter India continues to supply high-capacity stationary and mobile batching plants for major metro rail and highway projects across India, supporting large-scale infrastructure execution.

Technological adoption is accelerating across the region. Manufacturers are increasingly offering automated, IoT-enabled, and energy-efficient plants to meet rising expectations for quality control, digital documentation, and productivity optimization. Environmental regulations are tightening as well, prompting investments in dust-suppression systems, water-recycling units, and lower-carbon mix capabilities. Contractors are prioritizing modular and scalable plant designs that can be expanded in line with project phasing and demand growth. Rising consolidation among ready-mix producers is also encouraging standardized batching systems to improve operational consistency and regional supply integration. Mobile batching plants are gaining momentum in remote, fast-expanding construction zones, while urban markets favor high-throughput stationary installations.

Competitive Landscape

The global concrete batching plant market exhibits a moderately fragmented structure, driven by rising infrastructure spending, rapid urbanization, and growing demand for high-performance, automated batching technologies. Manufacturers are expanding portfolios with energy-efficient, low-emission, and digitally integrated plants to meet strict environmental norms and evolving construction quality requirements.

With key leaders including Ammann Group, Schwing Stetter, Liebherr, MEKA, ELKON, Wirtgen Group (Vögele), and Astec Industries. These players compete through continuous product innovation, automation upgrades, and IoT-enabled monitoring systems that improve mix precision, fuel efficiency, and predictive maintenance. Additionally, companies differentiate through custom plant configurations, stronger after-sales networks, and compliance with regional carbon-reduction policies.

Key Market Developments:

- In February 2025, Liebherr showcased its new Mobilmix mobile concrete mixing plant at Bauma, featuring a modular design with mixer sizes from 2.5 to 4.0 m³, an output capacity of up to 170 m³/hour, and advanced frequency-converter drives that reduce power consumption by up to 30% while improving weighing accuracy to save cement. The new generation emphasizes fast installation without special transport, higher energy efficiency, precise dosing, and improved maintenance access, reinforcing Liebherr’s focus on sustainable, high-performance mobile batching solutions.

- In September 2025, Nuvoco Vistas Corporation announced a US$24 million investment to expand its cement grinding capacity in eastern India by 4 MTPA, including a new grinding mill at its Arasmeta plant in Chhattisgarh and debottlenecking upgrades at Jojobera (Jharkhand), Panagarh (West Bengal), and Odisha facilities, with phased commissioning planned between FY26 and FY27.

Concrete Batching Plant Market Scope

| Report Attribute | Details |

|---|---|

|

Historical Data/Actuals |

2020 - 2025 |

|

Forecast Period |

2026 - 2033 |

|

Market Analysis |

Value: US$ Bn |

|

Geographical Coverage |

|

|

Segmental Coverage |

|

|

Competitive Analysis |

|

|

Report Highlights |

|

Companies Covered in Concrete Batching Plant Market

- AIMIX Group

- Ammann

- Astec

- Cemco

- Elkon

- JEL Concrete Plants

- Liebherr

- Meka

- Putzmeister

- Sany

- SCHWING Stetter

- Semix

- Stephens Mfg

- Vince Hagan

- XCMG

Frequently Asked Questions

The global concrete batching plant market is projected to reach US$5.1 billion in 2033, reflecting robust growth.

Key demand drivers include sustained infrastructure and urban development, the shift from site-mixed to ready-mix concrete under stricter quality and safety regulations, and technology-led improvements in plant productivity and sustainability.

Stationary batching plants lead the market with 60% share, driven by their high-capacity output, continuous operation suitability, and strong demand from urban RMC producers and large infrastructure hubs.

Asia Pacific dominates the market, driven by large-scale infrastructure and urbanization in China, India, and fast-growing ASEAN economies.

A key opportunity lies in mobile and digitalized plants serving remote infrastructure, renewable energy, and smart city projects, where fast deployment, real-time monitoring, and high-quality output are critical differentiators.