- Construction & Engineering

- Precast Concrete Market

Precast Concrete Market Size, Share, and Growth Forecast 2025 - 2032

Precast Concrete Market Analysis By Product Type (Columns & Beams, Walls & Barriers, Floors & Roofs, Girders, Utility Vaults, Pipes), Construction Type (Elemental Construction, Permanent Modular Buildings, Relocatable Buildings), Concrete Type (We Concrete, Dry/Semi - dry Concrete), and Regional Analysis 2025 - 2032

Precast Concrete Market Share and Trends Analysis

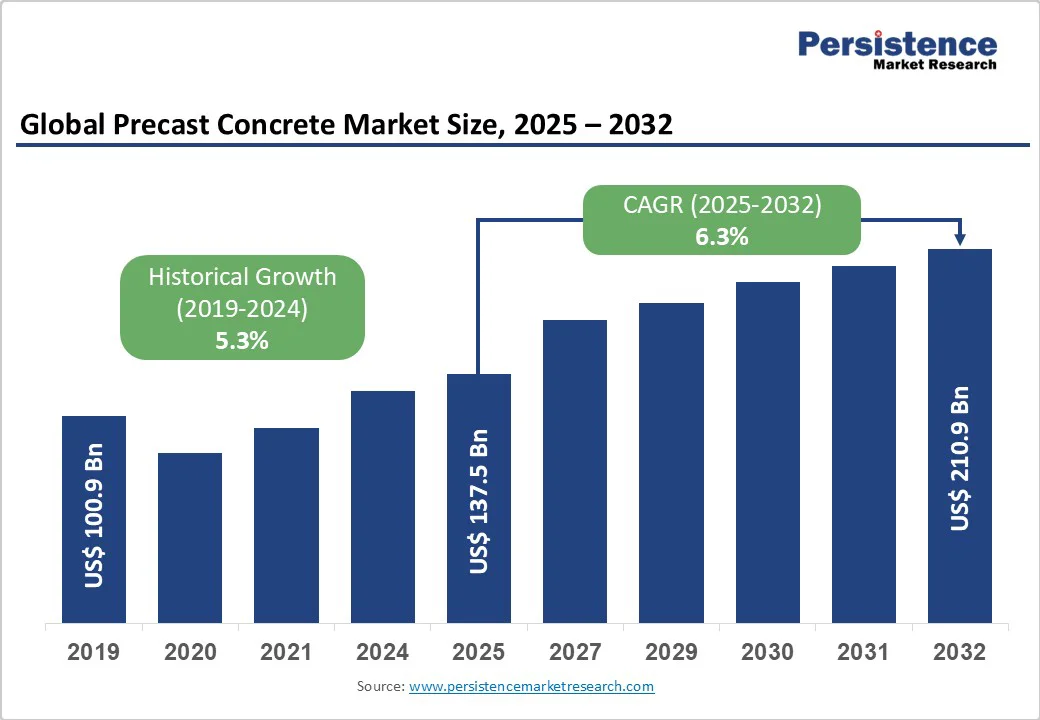

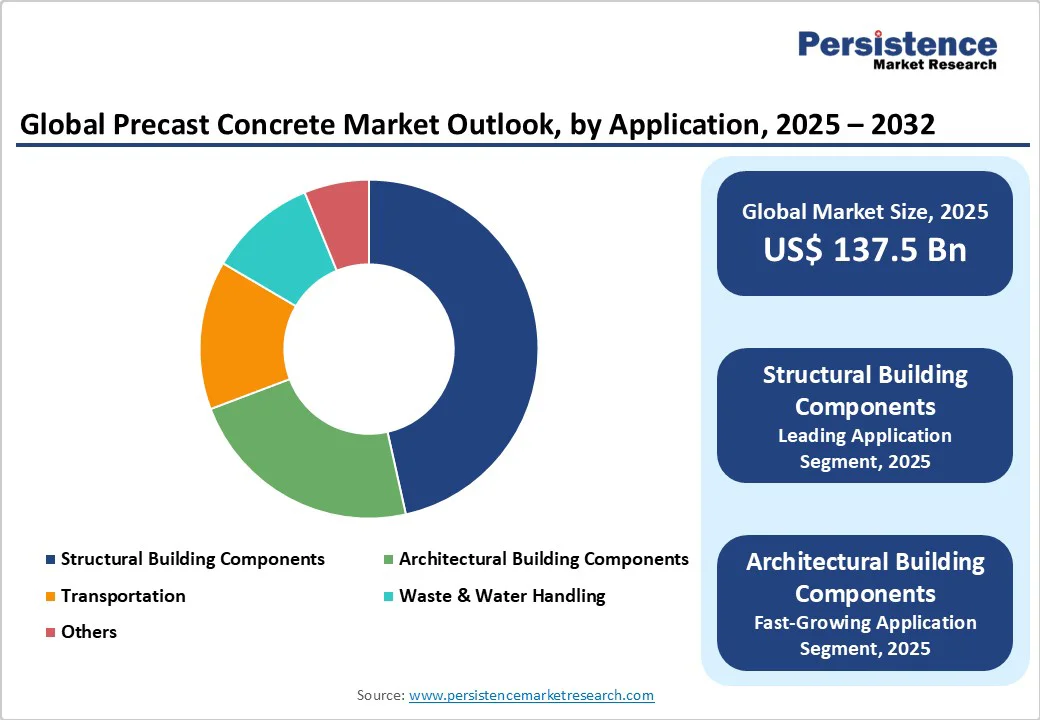

The global precast concrete market size is likely to value US$ 137.5 billion in 2025 and is projected to reach US$ 210.9 billion by 2032, growing at a CAGR of 6.3% between 2025 and 2032.

The growth trajectory is driven by accelerating urbanization and infrastructure development across emerging economies, coupled with the construction industry's increasing preference for time-efficient and cost-effective building methods.

Government initiatives promoting sustainable construction practices and the growing adoption of modular construction technologies are further propelling market expansion globally.

Key Market Highlights

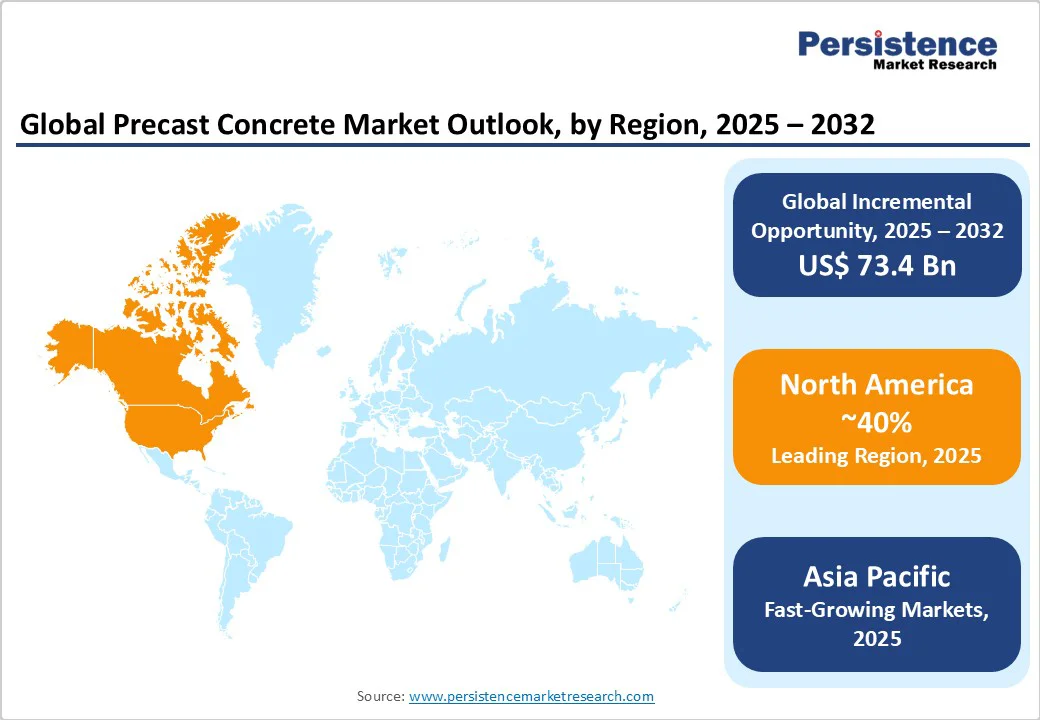

- Leading Region: North America dominates global precast concrete consumption with approximately 40% share in 2025 driven by infrastructure modernization programs and advanced manufacturing capabilities.

- Fastest-Growing Region: Asia Pacific represents the fastest-growing regional market with projected CAGR of 6.8% through 2032, supported by rapid urbanization and massive infrastructure investments across China, India, and Southeast Asian nations.

- Leading Application: Structural Building Components maintain market leadership with 45% segment share due to fundamental requirements for engineered building systems across all construction sectors.

- Fastest-Growing Construction Type: Elemental Construction emerges as the fastest-growing construction type with CAGR of 7.2%, driven by demand for flexible, component-based building approaches enabling design customization.

- Key Market Opportunity: Smart city development represents the primary market opportunity with potential to reach $180 billion globally by 2030 as governments prioritize rapid, sustainable urban infrastructure deployment.

| Key Insights | Details |

|---|---|

| Precast Concrete Market Size (2025E) | US$ 137.5 billion |

| Market Value Forecast (2032F) | US$ 210.9 billion |

| Projected Growth CAGR (2025-2032) | 6.3% |

| Historical Market Growth (2019-2024) | 5.3% |

Market Dynamics

Driver - Rapid Urbanization and Infrastructure Development Initiatives

The unprecedented pace of global urbanization, particularly in developing economies, is fundamentally transforming the precast concrete market landscape. According to United Nations data, the global urban population is projected to increase by 2.5 billion people by 2050, with approximately 68% of the world's population expected to live in urban areas.

This massive demographic shift is driving substantial infrastructure requirements across residential, commercial, and public utility sectors. Countries like India, China, and Brazil are implementing ambitious smart city initiatives that prioritize rapid construction methodologies to address housing shortages and infrastructure gaps.

The precast construction market is particularly benefiting from government-led programs such as India's Smart Cities Mission, which has allocated US$15 billion for urban infrastructure development across 100 cities. Modern precast concrete solutions enable construction speeds up to 60% faster than traditional methods, making them ideal for large-scale housing projects and commercial developments.

The technology's ability to facilitate concurrent manufacturing and site preparation activities significantly reduces project timelines, a critical advantage in meeting the urgent infrastructure demands of rapidly expanding urban centers.

Enhanced Quality Control and Sustainable Construction Practices

The construction industry's increasing focus on environmental sustainability and quality standardization is driving widespread adoption of precast concrete technologies. Precast manufacturing occurs in controlled factory environments that ensure consistent quality parameters while reducing material waste by up to 50% compared to conventional on-site construction. The International Organization for Standardization (ISO) has established comprehensive guidelines for precast concrete production that emphasize durability, energy efficiency, and environmental performance.

Modern precast facilities incorporate advanced automation technologies and Building Information Modeling (BIM) systems that optimize material utilization and minimize carbon emissions. The production process enables precise control over concrete curing conditions, resulting in superior structural integrity and longevity.

Additionally, precast concrete products typically achieve 25-30% better thermal performance than traditional construction materials, contributing significantly to building energy efficiency ratings. The ability to incorporate recycled materials and supplementary cementitious materials in precast production supports circular economy principles while meeting stringent green building certification requirements such as LEED and BREEAM standards.

Restraint - High Initial Capital Investment and Infrastructure Requirements

The substantial upfront investment required for establishing precast concrete manufacturing facilities remains a significant barrier to market entry, particularly for small and medium-scale enterprises. Setting up a modern precast plant with automated production lines typically requires capital investment ranging from US$15-50 million, depending on capacity and technology sophistication.

The infrastructure demands include specialized molds, curing chambers, lifting equipment, and transportation logistics, creating substantial financial barriers for potential market participants. Many developing regions lack the necessary industrial infrastructure and skilled workforce required for efficient precast operations, limiting market penetration in emerging economies.

Transportation and Logistics Constraints

Precast concrete components face inherent limitations due to their size, weight, and transportation requirements, which can restrict project feasibility and increase overall costs. The need for specialized heavy-duty transportation equipment and route planning for oversized loads creates logistical challenges, particularly for projects located in remote areas or urban centers with traffic restrictions. Transportation costs can account for up to 25-30% of total precast component prices, making the technology less competitive for projects beyond the optimal delivery radius from manufacturing facilities.

Opportunities - Smart City Development and Digital Construction Integration

The global smart cities movement presents unprecedented opportunities for precast concrete market expansion, with worldwide smart city investments projected to reach US$ 1.25 trillion by 2032. Smart city projects require rapid construction of integrated infrastructure, including transportation systems, utility networks, and digital connectivity frameworks that align perfectly with precast construction capabilities.

Countries like Singapore, South Korea, and the United Arab Emirates are implementing comprehensive smart city programs that prioritize modular construction methodologies for faster deployment and future adaptability.

Advanced precast systems are increasingly integrating Internet of Things (IoT) sensors and smart building technologies directly into concrete elements, enabling real-time monitoring of structural performance and environmental conditions.

The convergence of precast technology with digital construction tools such as AI-powered design optimization and robotics-assisted manufacturing is creating new value propositions for contractors and developers.

Major infrastructure projects, including metro rail systems, airport expansions, and renewable energy facilities, are increasingly specifying precast solutions to achieve aggressive construction schedules while maintaining quality standards. Government initiatives supporting digital construction adoption are providing financial incentives and regulatory frameworks that favor innovative precast applications.

Sustainable Construction and Green Building Mandates

The construction industry's transition toward carbon-neutral building practices is creating substantial growth opportunities for environmentally sustainable precast concrete solutions. Global green building market growth, valued at $265 billion in 2023 and projected to reach US$610 billion by 2027, is driving demand for precast products that support sustainability objectives.

European Union regulations under the Green Deal and Fit for 55 package are mandating significant reductions in construction sector carbon emissions, positioning precast technology as a preferred solution due to its energy efficiency and waste reduction capabilities.

Innovative precast formulations incorporating industrial byproducts such as fly ash, slag cement, and recycled aggregates are achieving up to 40% carbon footprint reduction compared to traditional concrete. The development of carbon-negative concrete technologies using captured CO2 during manufacturing is opening new market segments focused on climate-positive construction.

Major construction companies are establishing sustainability commitments that prioritize precast solutions, with organizations like LafargeHolcim and CEMEX investing heavily in low-carbon precast manufacturing technologies. Government carbon pricing mechanisms and green building incentives are creating favorable economics for sustainable precast adoption across both public and private construction projects.

Category-wise Insights

Product Type Analysis

Columns & beams dominate the precast concrete market with approximately 42% share in 2025, driven by their critical structural importance and widespread application across all construction sectors. These fundamental load-bearing components are essential for commercial buildings, industrial facilities, and infrastructure projects where structural integrity and speed of construction are paramount. The standardization of precast column and beam designs enables efficient mass production while maintaining precise engineering specifications for various load capacities and span requirements.

Modern precast columns and beams incorporate advanced reinforcement technologies including post-tensioning systems and fiber-reinforced concrete that enhance structural performance while reducing material consumption. The segment benefits from increasing adoption in high-rise construction projects where traditional formwork becomes cost-prohibitive due to height and access challenges.

Prefabricated volumetric construction techniques utilizing precast columns and beams are gaining traction in residential tower developments, reducing construction time by up to 50% compared to conventional methods. The growing complexity of modern architectural designs requires customized structural solutions that precast manufacturing can deliver with consistent quality and precision.

Construction Type Analysis

Elemental Construction holds the leading market position with approximately 58% share, reflecting the construction industry's preference for flexible, component-based building approaches. This construction methodology allows architects and engineers to combine standardized precast elements in diverse configurations, optimizing both design flexibility and manufacturing efficiency.

Elemental construction enables greater customization capabilities while maintaining the speed and quality advantages of precast manufacturing, making it ideal for complex commercial and institutional projects. The approach facilitates concurrent engineering where building systems can be designed and manufactured simultaneously with site preparation activities, significantly reducing overall project timelines.

Modern elemental construction increasingly incorporates Building Information Modeling (BIM) technologies that optimize component integration and minimize on-site coordination challenges. The methodology supports sustainable construction practices by enabling precise material calculation and waste minimization throughout the design and construction process.

Concrete Type Analysis

Wet Concrete maintains market leadership with approximately 67% segment share due to its superior workability and finishing characteristics essential for architectural applications. Wet concrete formulations provide enhanced surface quality and detailed texture reproduction capabilities that are crucial for decorative and exposed concrete applications in commercial and residential construction. The production process enables better integration of admixtures and supplementary materials that enhance performance characteristics such as durability, water resistance, and thermal properties.

Modern wet concrete precast operations utilize advanced batching and mixing technologies that ensure consistent quality parameters while accommodating complex architectural specifications. The segment benefits from growing demand for architectural precast elements including facade panels, ornamental features, and interior design components that require superior aesthetic finishing. Self-consolidating concrete technologies within wet concrete production are eliminating vibration requirements and improving production efficiency while maintaining superior surface characteristics.

Application Analysis

Structural Building Components represent the largest application segment with approximately 45% market share, driven by the fundamental requirements of modern construction projects for reliable, engineered building systems. This category encompasses load-bearing elements essential for building integrity including foundations, walls, floors, and roofing systems that must meet stringent structural performance standards. The segment benefits from increasing adoption of precast solutions in high-rise construction where structural precision and speed are critical for project success.

Modern structural precast components incorporate advanced reinforcement technologies including carbon fiber and basalt fiber systems that provide superior strength-to-weight ratios compared to traditional steel reinforcement. The growing complexity of seismic design requirements is driving demand for engineered precast structural systems that provide predictable performance during extreme loading events. Performance-based design methodologies are increasingly favoring precast solutions due to their consistent material properties and controlled manufacturing quality.

End-use Analysis

The Infrastructure sector leads market consumption with approximately 38% market share, reflecting massive global investment in transportation, utilities, and public works projects. Infrastructure applications include bridges, tunnels, highways, railways, water treatment facilities, and energy infrastructure that require durable, long-lasting construction solutions. The segment benefits from government infrastructure spending programs worldwide, with the Global Infrastructure Hub estimating US$94 trillion in infrastructure investment requirements through 2040.

Precast concrete's ability to withstand harsh environmental conditions while maintaining structural integrity makes it ideal for critical infrastructure applications with extended service life requirements. Modern infrastructure precast projects increasingly utilize modular construction approaches that enable rapid deployment and future expansion capabilities. The growing emphasis on resilient infrastructure design is driving demand for precast solutions that can withstand climate change impacts including extreme weather events and rising sea levels.

Regional Insights

North America Precast Concrete Market Trends

North America maintains its position as the largest regional market, with the United States accounting for approximately 78% of regional demand, driven by robust construction activity and advanced manufacturing infrastructure. The region benefits from well-established precast manufacturing capabilities with over 890 precast producers operating across the continent according to the National Precast Concrete Association (NPCA). The Infrastructure Investment and Jobs Act allocated US$1.2 trillion for infrastructure modernization, providing substantial opportunities for precast concrete applications in highways, bridges, and transit systems.

Recent regulatory developments include updated American Concrete Institute (ACI) standards for precast manufacturing that emphasize sustainability and performance requirements. The Federal Highway Administration (FHWA) has been promoting accelerated bridge construction techniques using precast elements to minimize traffic disruption while improving structural performance. Major projects such as the New York Metropolitan Transportation Authority subway expansion and California High-Speed Rail are extensively utilizing precast components to achieve aggressive construction schedules while ensuring long-term durability.

Europe Precast Concrete Market Trends

European markets demonstrate strong growth momentum with Germany, France, and the United Kingdom leading regional adoption through comprehensive regulatory frameworks and sustainability initiatives. The European Union's Green Deal mandates significant reductions in construction sector carbon emissions, positioning precast technology as a preferred solution for meeting 2030 climate targets. Germany's precast industry benefits from advanced automation technologies and strict quality standards established by Deutscher Beton- und Bautechnik-Verein (DBV).

The region's emphasis on circular economy principles is driving innovation in precast manufacturing, with companies developing closed-loop recycling systems for concrete waste. France's national building codes increasingly favor precast solutions for social housing projects under the Action Coeur de Ville program.

The Construction Products Regulation (CPR) provides harmonized standards across EU member states, facilitating cross-border precast trade and technology transfer. Major infrastructure investments, including HS2 high-speed rail in the UK and Grand Paris Express metro expansion, are showcasing advanced precast construction capabilities.

Asia Pacific Precast Concrete Market Trends

Asia Pacific represents the fastest-growing regional market, with China and India driving demand through massive urbanization and infrastructure development programs. China's precast concrete market benefits from government mandates requiring 30% precast adoption in new construction projects by 2025, supported by the 14th Five-Year Plan emphasizing sustainable construction practices. India's growing precast adoption is accelerated by the National Infrastructure Pipeline investing US$1.4 trillion in infrastructure development through 2030.

Japan's advanced precast technology focuses on seismic resistance and disaster resilience, with innovations in ductile concrete and fiber-reinforced systems setting global standards for earthquake-resistant construction. The region's manufacturing advantages include lower labor costs and proximity to raw material sources, enabling competitive precast production for both domestic and export markets.

ASEAN countries are implementing regional infrastructure connectivity projects that extensively utilize precast construction for rapid deployment across diverse geographical conditions. Government initiatives supporting Belt and Road infrastructure projects are creating substantial demand for standardized precast solutions across emerging Asian markets.

Competitive Landscape

The global precast concrete market exhibits a moderately fragmented structure with the top ten companies collectively accounting for approximately 45% of total market share. The competitive landscape is characterized by a mix of large multinational corporations and specialized regional players, each leveraging distinct competitive advantages including geographic presence, technological capabilities, and vertical integration strategies.

Leading companies are pursuing aggressive expansion strategies through strategic acquisitions, joint ventures, and greenfield investments to capture growing opportunities in emerging markets. Innovation remains a key differentiator with major players investing heavily in automation technologies, sustainable materials development, and digital construction solutions. The industry is witnessing increased consolidation as companies seek to achieve economies of scale and expand their geographic footprint to serve large infrastructure projects effectively.

Key Market Developments

- In September 2024, Larsen & Toubro announced completion of India's first 12-story precast residential tower constructed in just 96 days, demonstrating the company's advanced Precast Large Concrete Panel System technology and establishing new benchmarks for rapid construction in the residential sector.

- In July 2025, Boral Ltd. officially opened a state-of-the-art precast manufacturing facility at Emu Plains, Sydney, supporting the Western Harbour Tunnel project with capacity to produce over 13,000 tunnel segments and demonstrating the company's commitment to major infrastructure developments.

- In April 2023, Holcim acquired HM Factory in Poland to enter the precast construction market, expanding the company's solutions portfolio and strengthening its position in the European modular construction segment with innovative 3D printing capabilities.

Companies Covered in Precast Concrete Market

- Boral Ltd

- LafargeHolcim Ltd

- Gulf Precast Concrete Co. LLC

- Olson Precast Company

- CEMEX S.A.B. de C.V.

- Forterra Pipe and Precast LLC

- Tindall Corporation

- Spancrete

- Elementbau Osthessen GmbH & Co.,

- ELO KG

- Gülermak A.S.,

- STECS, LAING O'Rourke, Larsen & Toubro Ltd.

- Balfour Beatty Plc,

- Bouygues Group

Frequently Asked Questions

The global precast concrete market is projected to reach US$ 210.9 billion by 2032, growing from US$ 137.5 billion in 2025 at a CAGR of 6.3%.

Key growth drivers include rapid urbanization and infrastructure development initiatives, enhanced quality control and sustainable construction practices, and government investments in smart city projects across emerging economies.

Columns & Beams lead the market with approximately 42% market share due to their critical structural importance and widespread application across commercial, residential, and infrastructure construction sectors.

Asia Pacific dominates the global market with approximately 40% market share, driven by massive urbanization, infrastructure investments, and government mandates promoting precast adoption in China and India.

Primary opportunities include smart city development initiatives with potential to reach $180 billion globally by 2030, sustainable construction mandates under green building programs, and digital construction integration with IoT and automation technologies.

Key market players include LafargeHolcim Ltd., CEMEX S.A.B. de C.V., Larsen & Toubro Ltd., Boral Ltd., Tindall Corporation, and Bouygues Group, with these companies maintaining strong positions through comprehensive product portfolios and global manufacturing capabilities.