- Technology

- Cloud Security Market

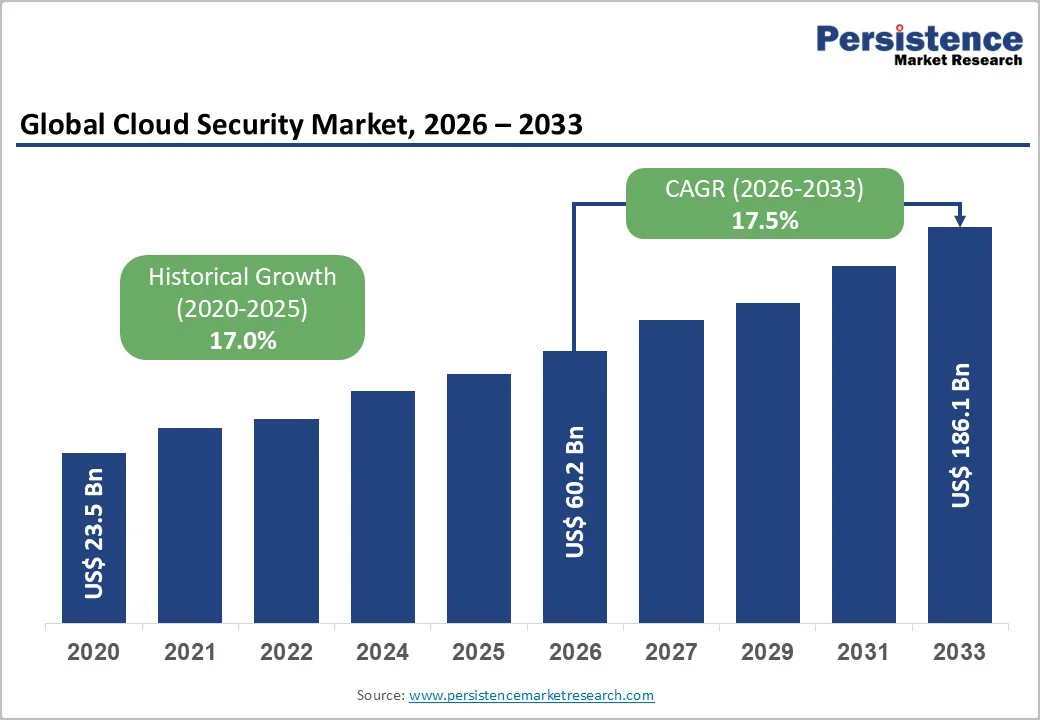

Cloud Security Market Size, Share, and Growth Forecast, 2026 - 2033

Cloud Security Market By Security Type (Identity and Access Management, Security Information and Event Management (SIEM), Others), Enterprise Size (Large Enterprises, SMEs), End-user (IT and Telecommunications, Others), and Regional Analysis for 2026 - 2033

Cloud Security Market Size and Trends Analysis

The global cloud security market size is likely to be valued at US$60.2 billion in 2026, and is expected to reach US$186.1 billion by 2033, growing at a CAGR of 17.5% during the forecast period from 2026 to 2033, driven by escalating cyber threats, widespread cloud adoption across enterprises, and stringent data protection regulations such as GDPR and CCPA.

The cloud security market is propelled by AI-based threat detection, multi-cloud management, and growing adoption in BFSI and healthcare. Rising ransomware threats are accelerating demand for zero-trust architectures and automated compliance tools. Despite integration challenges, cloud security remains essential for protecting sensitive data in an increasingly digital landscape.

Key Industry Highlights:

- Leading Region: North America, anticipated to hold 40% market share in 2026, driven by advanced cloud infrastructure, high cybersecurity investments, and regulatory mandates in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by rapid digitalization, SME cloud uptake, and government initiatives in India and China.

- Dominant Security Type: Identity and Access Management (IAM), anticipated to capture about 35% of the market, due to its role in enforcing zero-trust access controls.

- Leading Enterprise Size: Large Enterprises, likely to account for over 70% of the revenue, as they prioritize comprehensive multi-cloud protection.

- Leading End-user: BFSI, anticipated to contribute nearly 25% of the market share in 2026, amid rising fintech vulnerabilities and compliance needs.

| Key Insights | Details |

|---|---|

|

Cloud Security Market Size (2026E) |

US$60.2 Bn |

|

Market Value Forecast (2033F) |

US$186.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

17.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

17.0% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Adoption of Advanced Technologies (AI/ML and DevSecOps) to Strengthen Cloud Security

The adoption of advanced technologies such as artificial intelligence (AI), machine learning (ML), and DevSecOps is becoming a major driver of the cloud security market as organizations seek more proactive and automated protection. AI and ML help security systems analyze massive volumes of cloud data in real time, allowing them to detect anomalies, identify unusual behaviors, and predict emerging threats before they cause damage. These technologies also support automated incident response, reducing reliance on manual monitoring and enabling faster containment of attacks. As cloud environments become more dynamic, AI- and ML-powered tools provide continuous visibility across distributed workloads, improving accuracy in identifying misconfigurations and vulnerabilities.

DevSecOps integrates security directly into the development and deployment pipeline, ensuring cloud applications are secured from the earliest stages. This approach embeds automated testing, code scanning, and configuration validation into continuous integration and continuous delivery (CI/CD) workflows. As businesses increasingly adopt cloud-native architectures, DevSecOps reduces security bottlenecks and helps teams release features faster without compromising protection.

Complexities in Managing Multi-Cloud and Hybrid Environments

Managing security across multi-cloud and hybrid environments has become one of the biggest restraints in the cloud security market as organizations distribute workloads across different providers and on-premise systems. Each cloud platform, whether public, private, or hybrid, comes with its own tools, configurations, APIs, and security controls. This lack of uniformity makes it difficult for security teams to enforce consistent policies, monitor threats, or maintain visibility across all environments. In many cases, organizations must use multiple dashboards or tools to track activity, which increases operational complexity and raises the risk of blind spots.

Hybrid setups add another layer of difficulty because companies must synchronize security between traditional data centers and cloud workloads. Differences in network architectures, identity systems, and compliance requirements often lead to misconfigurations, one of the most common causes of cloud breaches. As workloads shift dynamically between environments, maintaining real-time control becomes even more challenging. These complexities not only create technical obstacles but also increase costs, as businesses need specialized expertise and additional security solutions to manage the fragmented environment.

Rising Demand for AI-Driven and Automation-Based Cloud Security Solutions

The growing demand for AI-driven and automation-based cloud security solutions is creating a major opportunity in the global cloud security market, as organizations look for faster, smarter, and more efficient ways to protect increasingly complex cloud environments. Traditional security tools struggle to keep pace with dynamic workloads, high-volume data flows, and constantly evolving cyber threats. AI and machine learning (ML) address this gap by analyzing large datasets in real time, identifying unusual patterns, and detecting threats that may be difficult for humans to recognize. These technologies enable predictive threat detection, automated risk scoring, and continuous monitoring across distributed cloud resources.

Automation enhances this capability by reducing human intervention in routine security tasks such as patching, log analysis, identity verification, and incident response. Automated workflows ensure that threats are contained quickly, often within seconds, minimizing damage and preventing lateral movement within the cloud. For organizations facing a shortage of skilled cybersecurity professionals, AI and automation provide a scalable and cost-efficient solution.

Category-wise Analysis

Security Type Insights

Identity and Access Management (IAM) is expected to lead the market, with a 35% share in 2026. IAM solutions help organizations control user access to cloud applications and data, ensuring that only authorized personnel can access sensitive resources. This is particularly critical as enterprises adopt multi-cloud and hybrid environments, where managing user identities and permissions becomes complex. For example, Microsoft Azure Active Directory enables secure single sign-on, multi-factor authentication, and conditional access policies, helping businesses prevent unauthorized access and reduce the risk of data breaches. The growing emphasis on data protection and regulatory compliance further drives IAM adoption.

Data Loss Prevention (DLP) is the fastest-growing due to the increasing volume of sensitive data stored in cloud environments and the rising risk of accidental or malicious data leaks. Organizations across industries are under pressure to protect customer information, intellectual property, and financial records while complying with strict regulations such as GDPR and HIPAA. For example, Symantec DLP provides content discovery, real-time monitoring, and policy enforcement to prevent data exfiltration across cloud applications and endpoints. As businesses prioritize data protection, demand for robust DLP solutions continues to accelerate rapidly.

Enterprise Size Insights

Large Enterprises are estimated to dominate at a 70% share in 2026. Their dominance is driven by the extensive use of cloud services, complex IT infrastructures, and the need to protect large volumes of sensitive data across multiple locations and departments. Large organizations also face stricter regulatory compliance requirements and higher exposure to cyber threats, prompting significant investment in advanced cloud security solutions. For example, IBM Cloud Security helps enterprises implement identity management, threat detection, and encryption across hybrid and multi-cloud environments, enabling robust protection and continuous monitoring at scale.

Small and Medium-Sized Enterprises (SMEs) are likely to be the fastest-growing, due to their rapid adoption of cloud services and limited in-house security expertise. As SMEs migrate critical workloads to the cloud, they face increasing risks from cyber threats, data breaches, and compliance requirements. Cloud security solutions that are affordable, scalable, and easy to deploy are highly attractive to this segment. For example, CrowdStrike Falcon offers lightweight, cloud-native endpoint protection and threat detection, enabling SMEs to secure their cloud environments efficiently without requiring extensive IT staff or complex infrastructure, driving rapid adoption.

End-user Insights

The BFSI segment is expected to lead with a 25% share in 2026, due to the sector’s heavy reliance on cloud-based applications for transactions, customer data management, and digital banking services, which makes it a prime target for cyberattacks. Financial institutions require robust security to protect sensitive financial data and comply with strict regulations such as PCI DSS and GDPR. For example, AWS Security Services help banks implement encryption, access control, and threat detection across cloud workloads, enabling secure, compliant, and reliable financial operations.

The healthcare and life sciences segment is likely to be the fastest-growing, due to the increasing adoption of cloud-based electronic health records (EHRs), telemedicine, and digital patient management systems. With highly sensitive patient data at stake, healthcare organizations face stringent regulatory requirements such as HIPAA and rising cyber threats, including ransomware attacks. Cloud security solutions help ensure data privacy, secure access, and continuous monitoring. For example, Microsoft Azure for Healthcare provides encrypted storage, identity management, and compliance tools, enabling hospitals and research organizations to securely store and share patient data while accelerating digital transformation.

Regional Insights

North America Cloud Security Market Trends

North America is projected to lead, accounting for 40% of the market share in 2026, driven by the region’s rapid digital transformation, high cloud adoption, and increasing cyber threat landscape. Organizations across sectors such as BFSI, healthcare, retail, and government are migrating critical workloads to public, private, and hybrid cloud environments, creating demand for advanced security solutions. Multi-cloud and hybrid deployments are particularly common, prompting the need for unified platforms that provide visibility, compliance monitoring, and threat management across diverse environments.

AI and machine learning technologies are being increasingly integrated into cloud security platforms in the region, enabling real-time threat detection, anomaly identification, and automated incident response. The adoption of zero-trust architectures and identity-centric security approaches is accelerating, as businesses seek to control access to sensitive data while preventing breaches. Regulatory compliance, including GDPR, CCPA, and industry-specific standards, continues to drive investments in data protection and governance tools. The growing focus on managed security services and cloud-native security solutions is especially evident among SMEs lacking in-house expertise.

Europe Cloud Security Market Trends

Growth in Europe is fueled by increasing cloud adoption across enterprises, government organizations, and SMEs. Organizations are increasingly moving critical workloads to public, private, and hybrid cloud environments to achieve scalability, flexibility, and cost efficiency. As these deployments expand, businesses require robust cloud security solutions to protect sensitive data, ensure regulatory compliance, and maintain operational continuity.

Regulatory compliance remains a key trend in Europe, with strict data protection laws such as GDPR compelling organizations to adopt advanced encryption, access control, and monitoring tools. Companies are increasingly deploying identity and access management (IAM), data loss prevention (DLP), and cloud workload protection platforms to secure multi-cloud and hybrid environments. AI and machine learning technologies are being integrated into security platforms to provide automated threat detection, real-time monitoring, and predictive analytics. A growing focus on zero-trust security models, secure remote work solutions, and cloud-native security for emerging technologies such as IoT, edge computing, and containerized applications.

Asia Pacific Cloud Security Market Trends

Asia Pacific is likely to be the fastest-growing region, driven by the region’s accelerated digital transformation and widespread adoption of cloud technologies across industries such as BFSI, healthcare, IT, manufacturing, and retail. Organizations are increasingly shifting critical workloads to public, private, and hybrid cloud environments to enhance operational efficiency, scalability, and cost-effectiveness. This expansion creates a strong demand for cloud security solutions that can safeguard sensitive data, manage access, and ensure business continuity.

Regulatory compliance is becoming a significant factor, with countries implementing strict data protection and privacy regulations, prompting businesses to invest in advanced encryption, identity management, and monitoring solutions. The integration of AI and machine learning into cloud security platforms is a notable trend, enabling real-time threat detection, automated response, and predictive analytics to combat sophisticated cyberattacks. The adoption of zero-trust architectures, secure remote access solutions, and cloud-native security practices for emerging technologies such as IoT, edge computing, and containerized applications.

Competitive Landscape

The global cloud security market is highly competitive, characterized by the presence of established technology giants, emerging startups, and specialized security providers. Key players compete across product innovation, service offerings, geographic expansion, and strategic partnerships. Established companies leverage their extensive experience in cybersecurity, cloud infrastructure, and enterprise solutions to provide comprehensive platforms that combine identity and access management (IAM), data loss prevention (DLP), threat detection, and compliance management.

Innovation is a major differentiator in the market, with firms investing heavily in AI-driven threat intelligence, automated response, zero-trust frameworks, and cloud-native security solutions. Smaller vendors and startups focus on niche solutions, such as container security, serverless protection, and managed cloud security services, enabling them to quickly address emerging threats and specific industry requirements. Strategic collaborations, mergers, and acquisitions are common, allowing companies to expand their product portfolios, enter new regional markets, and strengthen cloud security capabilities.

Key Industry Developments

- In February 2025, Palo Alto Networks launched a strategic initiative to strengthen its cloud security leadership with the introduction of Cortex® Cloud—an advanced evolution of Prisma Cloud. This initiative unifies enhanced cloud detection and response (CDR) and industry-leading CNAPP capabilities on the Cortex platform, leveraging AI and automation to move beyond traditional passive security models and deliver real-time threat prevention for modern cloud environments.

- In April 2025, CrowdStrike unveiled a series of advanced innovations, such as AI Model Scanning and Shadow AI detection, designed to address the full spectrum of cloud risks within the CrowdStrike Falcon® platform. These new capabilities accelerate secure AI development, enhance runtime protection for cloud data, mitigate SaaS-based threats, and strengthen hybrid identity security. With these enhancements, CrowdStrike further expands its platform advantage, delivering unified visibility and robust protection across hybrid and multi-cloud environments.

Companies Covered in Cloud Security Market

- Trend Micro Incorporated

- Cisco Systems Inc.

- McAfee Inc.

- Palo Alto Networks Inc.

- Check Point Software Technologies

- Microsoft Corporation

- IBM Corporation

- Splunk Inc.

- Alphabet Inc.

Frequently Asked Questions

The global cloud security market is projected to reach US$60.2 billion in 2026.

Broad digital transformation efforts, including the migration of legacy systems to the cloud and the growing adoption of SaaS, PaaS, and IaaS, are key drivers prompting organizations of all sizes to modernize and invest in cloud security.

The cloud security market is projected to grow at a compound annual growth rate (CAGR) of 17.5% between 2026 and 2033.

The shift toward zero-trust architectures, where every user, device, and access request is continuously verified, presents a major opportunity.

Prominent players include Palo Alto Networks Inc., Microsoft Corporation, Cisco Systems Inc., and IBM Corporation.