- Technology

- Cloud Microservices Market

Cloud Microservices Market Size, Share, and Growth Forecast, 2025 - 2032

Cloud Microservices Market By Component (Platforms, Services), Deployment Mode (Public Cloud, Private Cloud, Hybrid Cloud), End-user Industry (BFSI, IT & ITeS, Telecommunications, Healthcare, Retail & E-Commerce, Others), and Regional Analysis for 2025 - 2032

Cloud Microservices Market Share and Trends Analysis

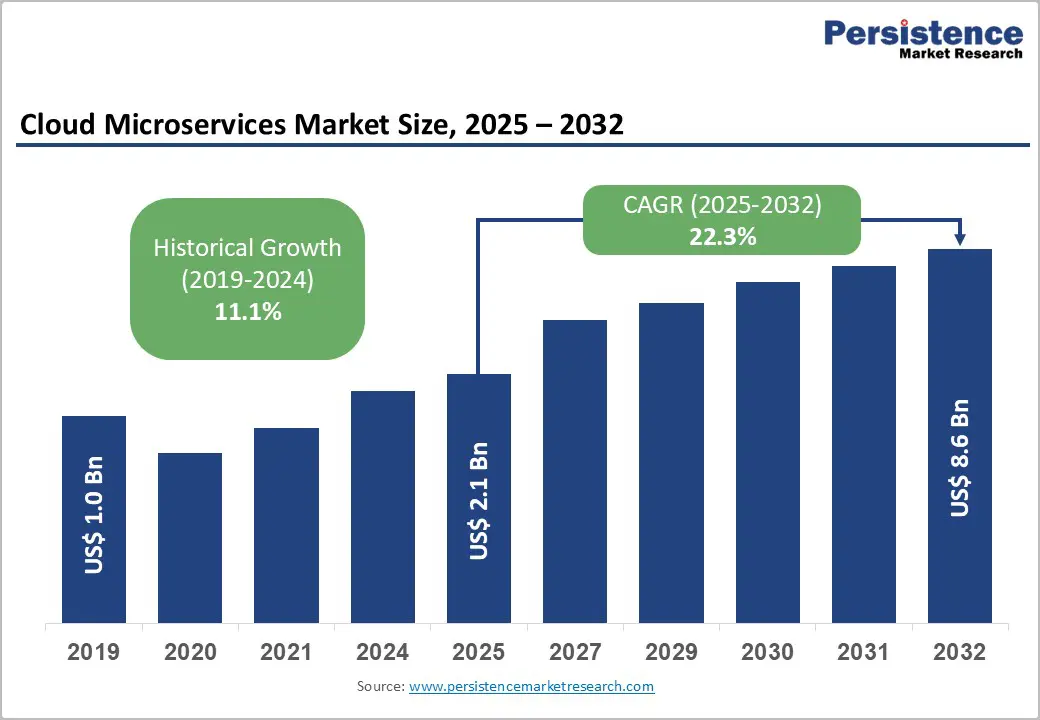

The global cloud microservices market size is likely to be valued at US$2.1 Billion in 2025, and is estimated to reach US$8.6 Billion by 2032, growing at a CAGR of 22.3% during the forecast period 2025 - 2032, driven by accelerating enterprise demand for application modernization, the proliferation of containerized deployment models, and the shift toward distributed cloud-native architectures across BFSI, healthcare, and retail sectors.

Organizations are rapidly adopting microservices to break down monolithic applications, reduce operational friction, and independently scale critical services. Hybrid cloud expansion, serverless integration, and AI-driven observability are boosting efficiency, while competition, data privacy regulations, and faster time-to-market needs further accelerate market growth.

Key Industry Highlights

- Dominant Components: Platforms dominate the market share at 60%, while services segments represent the fastest-growing category through 2032, indicating organizational reliance on external expertise to manage microservices architecture complexity.

- Leading Deployment Mode: Public cloud deployment remains the market leader at 70% share, whereas hybrid cloud emerges as the fastest-growing deployment mode, driven by regulatory data residency requirements.

- Dominant End-user Industry: The BFSI sector commands market leadership with 28% revenue share, with healthcare growing the fastest through 2032, reflecting regulatory compliance imperatives.

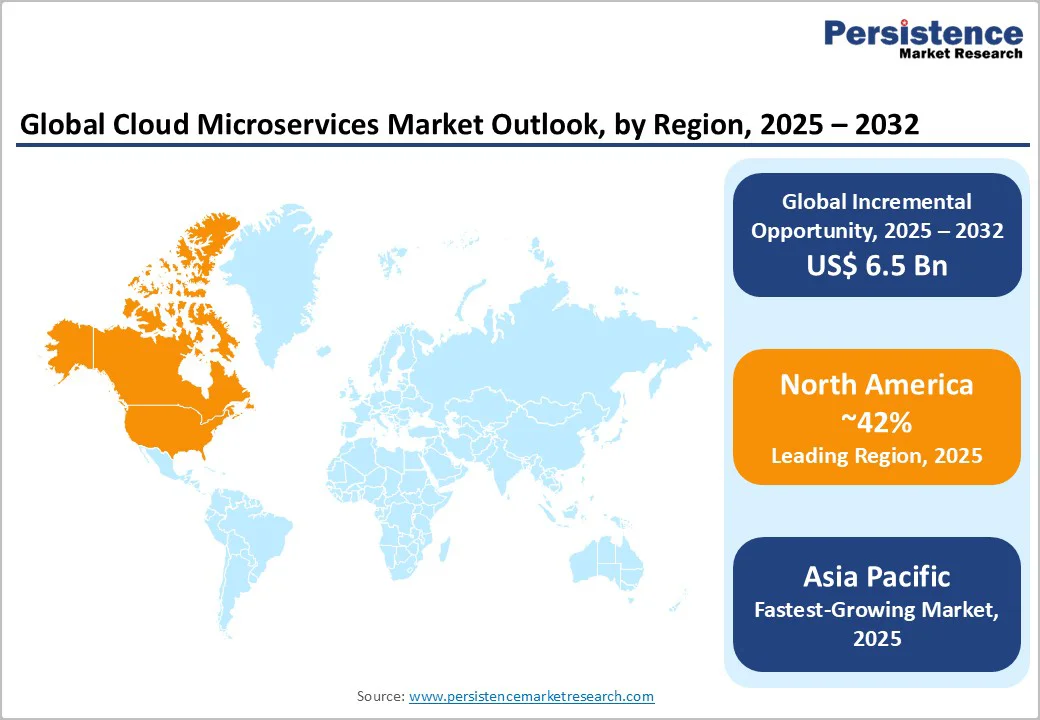

- Regional Leadership: North America leads with 42% market share in 2025, while Asia Pacific emerges as the fastest-growing regional market, driven by rapid digital transformation and expanding cloud infrastructure availability.

- Competitive Environment: Hyperscale cloud providers control market revenues, while the growing presence of specialized providers and regional integrators creates opportunities for companies addressing specific industry verticals or geographies.

- Major Opportunity: AI-driven observability represents the most attractive opportunity, reflecting the organizational imperative to reduce microservices operational complexity and incident response burden.

- September 2025: HPE and Juniper Networking expanded their collaboration in Saudi Arabia by deploying AI-native cloud infrastructure, aiming to accelerate digital transformation and enhance network automation and performance across the region.

| Key Insights | Details |

|---|---|

| Cloud Microservices Market Size (2025E) | US$2.1 Bn |

| Market Value Forecast (2032F) | US$8.6 Bn |

| Projected Growth (CAGR 2025 to 2032) | 22.3% |

| Historical Market Growth (CAGR 2019 to 2024) | 11.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Enterprise Legacy Modernization and Application Refactoring Momentum

Enterprise organizations in North America and Europe are actively modernizing legacy systems to overcome technical debt, reduce vendor lock-in, and regain operational agility.

Traditional monolithic applications, which are tightly coupled and inflexible, no longer meet the demands of rapid feature delivery and autonomous deployment. Modernization efforts focus on gradually replacing these monoliths with microservices through incremental refactoring, known as the "strangler fig" approach, which minimizes disruption while delivering value step-by-step.

Microservices enable distinct engineering teams to own and operate individual services end-to-end, fostering accountability, operational excellence, and investment in automation.

This shift has increased deployment frequency from quarterly releases to weekly or bi-weekly cycles, while also cutting infrastructure costs through more efficient resource allocation and independent scaling. Enterprises are hence significantly boosting feature development speed and shifting IT budgets toward cloud-native infrastructure, observability tools, and managed container platforms.

Integration Complexity and Legacy System Interoperability Constraints

Transitioning from monolithic to microservices architectures entails significant challenges related to decoupling tightly integrated business logic, managing distributed transactions, and implementing asynchronous communication patterns. Legacy systems often contain opaque data dependencies, undocumented APIs, and tightly coupled modules, making service decomposition complex and prone to hidden dependencies that require re-architecture mid-project.

Migrating entails redesigning APIs, decomposing data schemas, and adopting eventual consistency over traditional ACID transactional models, which complicates data management and consistency. These complexities are often compounded by technical debt embedded in legacy codebases with intricate interdependencies across stored procedures and modules.

Regulatory constraints add another layer of risk as integration errors could lead to compliance violations or data loss.

This combination of technical and regulatory hurdles creates substantial project risk, discouraging risk-averse organizations from committing capital to microservices initiatives and limiting market growth, particularly in highly regulated sectors. Successfully navigating these challenges requires comprehensive codebase analysis, robust observability, and strategic planning to mitigate disruptions and align organizational structures.

Serverless Microservices and Event-Driven Architecture Integration

Serverless computing platforms such as AWS Lambda, Google Cloud Functions, and Azure Functions are increasingly integrating with microservices architectures to simplify infrastructure management and reduce operational overhead.

By automatically scaling function instances in response to workload demands and charging only for actual execution time rather than reserved capacity, serverless platforms allow organizations to implement event-driven microservices without the complexity of managing underlying infrastructure.

Such an approach supports hybrid architectures where serverless functions handle bursty or variable workloads alongside containerized microservices optimized for steady-state processing.

This convergence enhances operational efficiency by minimizing infrastructure costs and accelerating time-to-market. Cloud providers are investing heavily in expanding serverless functionality, including development frameworks, service mesh integration, and advanced monitoring tools, making serverless particularly attractive in the Asia Pacific market, where rapid development and cost efficiency are prioritized.

The serverless microservices segment is projected to grow substantially, offering a robust and flexible architecture option that accelerates innovation while reducing infrastructure complexity and expenses.

Category-wise Analysis

Component Insights

The platform component is the largest and most mature segment, accounting for about 60% of the cloud microservices market revenue share in 2025. This segment includes container orchestration platforms such as Kubernetes, Amazon ECS/EKS, Google GKE, and Azure Container Instances, along with API gateways, service discovery tools, and infrastructure-as-code solutions.

Kubernetes stands out as the prevailing standard, with most organizations running it in production or pilot as of 2024. Managed Kubernetes services from public cloud providers dominate adoption due to their operational simplicity, integration with cloud ecosystems, and vendor-managed security and updates. Platform growth is moderate, reflecting a shift from initial deployment and standardization to more incremental platform optimization.

In contrast, the services segment is the fastest-growing component through 2032, fueled by increasing organizational dependency on external expertise to navigate the complexities of microservices architecture, reduce migration risks, and accelerate adoption timelines.

Consulting and systems integration services offer higher margins and recurring revenue potential, with global integrators such as Accenture, Deloitte, and IBM Global Services experiencing strong demand and full engagement capacity. Managed services are also critical, providing outsourcing for platform management, deployment pipeline optimization, and incident response.

Deployment Mode Insights

Public cloud deployment dominates, accounting for 70% of the cloud microservices market value in 2025. Leading providers, such as Amazon Web Services (AWS), Google Cloud Platform, and Microsoft Azure, have captured about 90% of this segment by leveraging hyperscale infrastructure, comprehensive managed service ecosystems, and strong enterprise customer bases.

Public cloud microservices provide elastic resource scaling without capacity provisioning, seamless integration with cloud-native services, and vendor-managed security and infrastructure maintenance. Hyperscalers continuously enhance their microservices platforms through managed container orchestration, serverless platforms, and advanced observability tools.

Hybrid cloud is set to be the fastest-growing deployment mode through 2032. Hybrid architectures distribute workloads across public cloud, private on-premises environments, and edge computing based on regulatory mandates, performance requirements, and organizational policies. For instance, financial institutions use hybrid models to keep sensitive data in private infrastructure while leveraging public cloud for analytics and AI workloads.

Driving hybrid cloud adoption are data residency regulations such as GDPR, PIPL, and India’s cloud residency mandates, alongside strategic imperatives to diversify cloud vendors. Enterprise interest in hybrid cloud is high, and the resultant demand for orchestration platforms, multi-cloud service meshes, and observability tools presents substantial market opportunities.

End-user Industry Insights

The BFSI sector represents the largest end-user industry for cloud microservices, commanding 28% of the total market value in 2025. Financial institutions face acute competitive pressures from fintech disruption, regulatory mandates for rapid regulatory change implementation, and customer demands for real-time payments, seamless digital experiences, and personalized financial services.

Traditional monolithic banking platforms are incompatible with contemporary competitive dynamics, requiring weekly or bi-weekly feature velocity and dynamic resource scaling. Banking institutions are systematically decomposing monolithic payment processing, lending, and trading platforms into independent microservices, enabling isolated team ownership, independent deployment cycles, and granular resource scaling.

Healthcare represents the fastest-growing end-user industry for cloud microservices through 2032. Healthcare organizations are deploying microservices to support digital health transformation, electronic health record modernization, telehealth infrastructure, and real-time clinical analytics.

The COVID-19 pandemic accelerated healthcare digital transformation, generating sustained demand for telehealth platforms, remote patient monitoring solutions, and interoperable healthcare data exchange infrastructure that microservices architecture enables.

Regulatory drivers, including the 21st Century Cures Act, HIPAA interoperability mandates, and Fast Healthcare Interoperability Resources (FHIR) standards adoption, are creating strong imperatives for healthcare organizations to adopt microservices-based architectures.

Regional Insights

North America Cloud Microservices Market Trends

North America commands a substantial 42% of the cloud microservices market share in 2025, supported by the presence of hyperscale cloud providers such as AWS and Google Cloud, a mature enterprise IT infrastructure, and advanced DevOps and automation practices. Key microservices adoption hubs are concentrated in U.S. technology and financial centers such as Silicon Valley, Seattle, New York, and Boston.

The widespread adoption of microservices in the region spans major sectors such as BFSI, healthcare, retail, and technology, with enterprises progressing from initial microservices deployments toward advanced patterns such as serverless computing, service mesh, and event-driven architectures.

Regulatory mandates such as the California Consumer Privacy Act (CCPA), HIPAA for healthcare, and the Gramm-Leach-Bliley Act for financial services continue to actively promote microservices adoption for compliance workloads.

Europe Cloud Microservices Market Trends

Europe plays a significant role in the cloud microservices market in 2025, with adoption led by Western European countries such as Germany, France, the U.K., Benelux, and the Scandinavian region.

Adoption across Europe is strongly influenced by stringent regulatory frameworks such as the European Union (EU)’s General Data Protection Regulation (GDPR), the Digital Services Act, digital taxation rules, and emerging digital sovereignty initiatives that incentivize hybrid cloud and regional cloud infrastructure usage.

Germany is a key player with its strong manufacturing and industrial software sectors driving Industry 4.0 transformations alongside major financial institutions and automotive companies. In France, cloud providers such as OVHcloud and Scaleway are encouraged through digital sovereignty policies, with increasing uptake by government, finance, and large enterprises.

The U.K. maintains robust financial services microservices adoption centered in London’s banking sector. The Europe market growth is forecasted to grow steadily through 2032, driven by regulatory compliance and legacy system modernization.

Asia Pacific Cloud Microservices Market Trends

Asia Pacific stands out as the fastest-growing regional market with a projected 27% CAGR from 2025 to 2032. This exceptional growth is driven by robust enterprise digital transformation, expanding cloud infrastructure, a growing developer talent pool, and strong government investments in the digital economy.

China, representing about 38% of the regional market, is accelerating cloud-native adoption powered by domestic tech giants and strict data residency rules. India, as the second-largest market in the region, benefits from a booming IT services sector and national digital initiatives, supporting microservices adoption, while Japan reflects more mature adoption led by the automotive and financial sectors.

The ASEAN region is rapidly progressing due to expanding tech talent and advancements in digital payments infrastructure. The market share of Asia Pacific is expected to rise at a sizable pace owing to digital transformation, infrastructure growth, and decreasing implementation barriers, presenting substantial opportunities for managed services providers, integrators, and infrastructure firms catering to the region’s expanding demand.

Competitive Landscape

The global cloud microservices market structure is highly fragmented, with leadership concentrated among hyperscale cloud providers but competitive opportunities dispersed across specialized platform vendors, system integrators, and managed services providers.

The top five companies, AWS, Microsoft Azure, Google Cloud, IBM, and Red Hat/Kubernetes, jointly hold approximately 45-50% of the platform market share. Amazon Web Services leads by leveraging its dominant public cloud infrastructure, managed Kubernetes (EKS), serverless platform (Lambda), and integrated container services.

Microsoft Azure comes in second on the back of strong enterprise relationships, DevOps tooling, managed Kubernetes (AKS), and a hybrid cloud focus. Google Cloud has strengthened its position with Kubernetes origins, container registry, and AI/ML workloads. The open-source Kubernetes ecosystem exerts significant influence by establishing it as the orchestration standard, fostering platform-agnostic competition.

Key Industry Developments

- In September 2025, Ateme used Google Cloud’s generative AI and Kubernetes Engine to automate multilingual subtitle production, reducing costs and turnaround times. Its containerized TITAN File integrates with Cloud Storage and Vertex AI, improving accessibility and enabling scalable, high-quality media distribution.

- In June 2025, Minna Bank announced that its cloud-native core banking system, built by Zerobank Design Factory with Accenture on Google Cloud, will be adopted by MUFG’s new digital bank. The system uses multi-cloud, microservices, and DevSecOps to boost scalability and efficiency.

- In June 2025, NVIDIA partnered with European model builders and cloud providers to create sovereign LLMs tailored to Europe’s languages and regulations. These open models will run on DGX Cloud Lepton and integrate into platforms such as Perplexity, strengthening Europe’s AI ecosystem and accelerating innovation across key industries.

Companies Covered in Cloud Microservices Market

- Amazon Web Services, Inc.

- Microsoft Corporation

- Alphabet Inc.

- IBM Corporation

- Red Hat, Inc.

- Datadog, Inc.

- New Relic, Inc.

- Dynatrace SE

- HashiCorp, Inc.

- Accenture plc

- Deloitte Consulting LLP

- Infosys Limited

- Tata Consultancy Services (TCS)

- IBM Global Services

Frequently Asked Questions

The global cloud microservices market is projected to reach US$2.1 Billion in 2025.

Accelerating enterprise demand for application modernization, the proliferation of containerized deployment models, and the shift toward distributed cloud-native architectures across BFSI, healthcare, and retail sectors are driving the market.

The cloud microservices market is poised to witness a CAGR of 22.3% from 2025 to 2032.

The convergence of hybrid cloud adoption, serverless computing integration, and AI-driven observability solutions, and tightening regulatory mandates for data privacy compliance are key market opportunities.

Amazon Web Services, Inc., Microsoft Corporation, Alphabet Inc., and IBM Corporation are some of the key players in the cloud microservices market.