- Medical Devices

- Clinical Electronic Thermometer Market

Clinical Electronic Thermometer Market Size, Share and Growth Forecast, 2026-2033

Clinical Electronic Thermometer Market by Product Type (Oral Thermometers, Ear Thermometers, Rectal Thermometers, Temporal Thermometers, Others), End-User (Hospitals, ASCs, Clinics, Homecare Settings), and Regional Analysis for 2026-2033

Clinical Electronic Thermometer Market Share and Trends Analysis

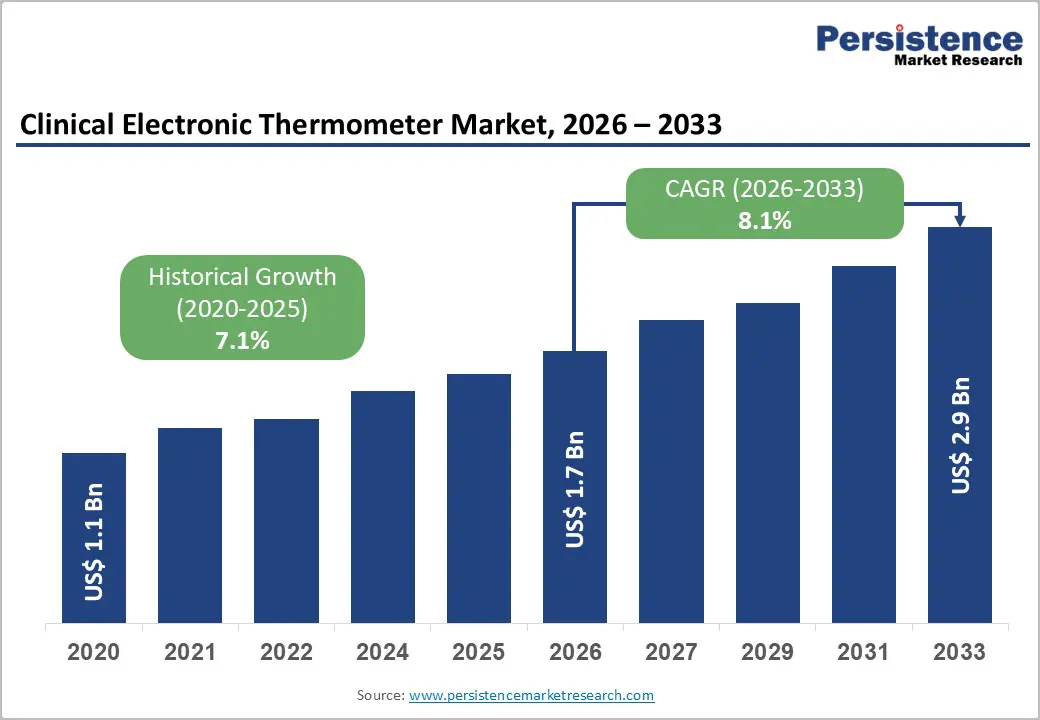

The global clinical electronic thermometer market size is likely to be valued at US$ 1.7 billion in 2026, and is projected to reach US$ 2.9 billion by 2033, growing at a CAGR of 8.1% during the forecast period 2026 – 2033.

The market is being significantly driven by increased investment in healthcare infrastructure across both developed and emerging economies, which facilitates the adoption of advanced diagnostic devices. The ongoing shift toward digital diagnostics and connected healthcare solutions is encouraging hospitals, clinics, and homecare providers to upgrade from traditional mercury thermometers to non-mercury, fast-response electronic devices.

This trend is further amplified by heightened post-pandemic awareness of infection control, prompting institutions to adopt safer, hygienic, and non-contact temperature measurement solutions. Innovations such as Bluetooth connectivity, mobile app integration, and compatibility with electronic health record systems are further expanding usability and data management, supporting sustained market growth across clinical and homecare settings.

Key Industry Highlights

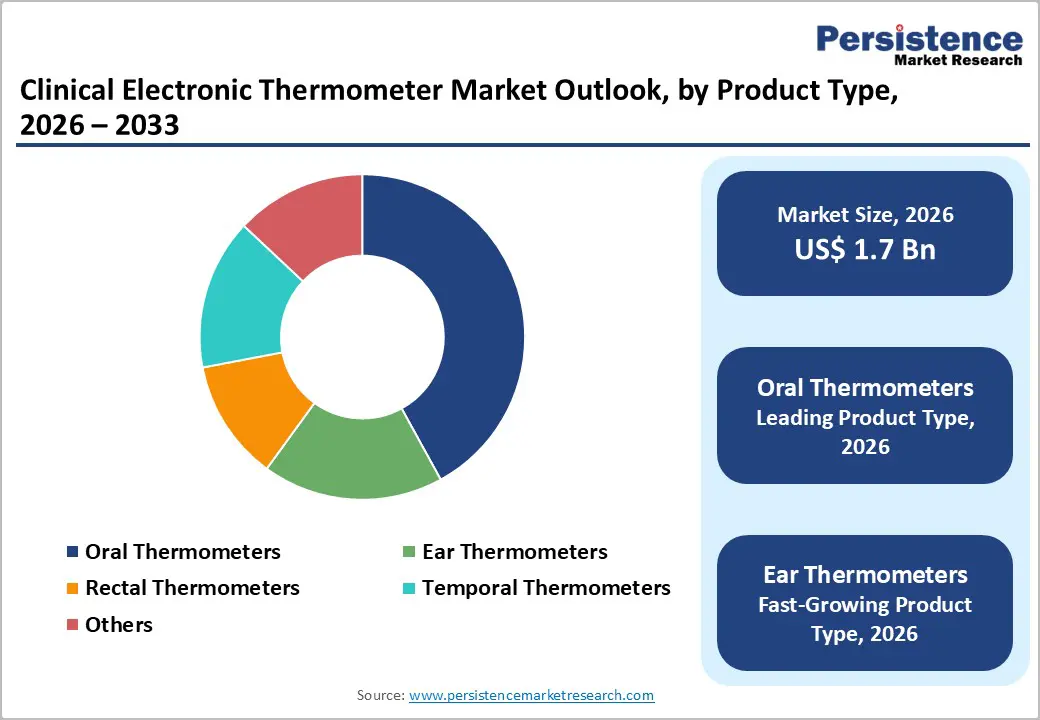

- Dominant Product Types: Oral thermometers are set to command around 42% revenue share in 2026, while ear thermometers are likely to grow the fastest through 2033, driven by hygiene and rapid-response preferences.

- Leading End-Users: Hospitals are expected to hold approximately 55% of revenue in 2026, while homecare settings are projected to grow the fastest during 2026–2033, fueled by telehealth adoption.

- Regional Leadership: North America is anticipated to lead with an estimated 38% share in 2026, while Asia Pacific is poised to record the highest growth at about 11.2% CAGR through 2033, supported by healthcare infrastructure expansion.

- Strategic Trends: Regulatory updates and digital connectivity partnerships are shaping competitive advantages and accelerating adoption across clinical and homecare environments.

- Innovation Focus: Integration with health platforms, mobile apps, and smart analytics enhances market attractiveness and enables real-time monitoring and predictive insights.

| Key Insights | Details |

|---|---|

| Substation Automation Market Size (2026E) | US$ 1.7 Bn |

| Market Value Forecast (2033F) | US$ 2.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Demand for Accurate Clinical Diagnostics in Hospitals

Healthcare systems are increasingly prioritizing evidence-based diagnosis, with body temperature remaining one of the most critical vital signs for medical decision-making. Clinical electronic thermometers offer rapid, precise measurements, enabling clinicians to monitor patients effectively, particularly in critical care, emergency wards, and surgical units. Hospitals are adopting stringent infection-monitoring protocols, ensuring that temperature measurement aligns with global guidelines for standardized patient assessment. This heightened focus on patient safety and care quality has significantly contributed to the steady adoption of advanced thermometry solutions in healthcare facilities.

The U.S. Food and Drug Administration (FDA) amended medical device regulations to limit premarket notification exemptions for certain clinical electronic thermometers, requiring formal review for advanced and novel technologies such as infrared thermometers with telethermographic functions. This regulatory update underscores the importance of accuracy, safety, and performance validation in clinical settings, reinforcing the adoption of advanced electronic thermometers in hospitals. It further highlights the role of these devices in meeting modern standards for precision diagnostics and infection control.

Expansion of Home Healthcare and Technological Advancements

The home healthcare space is experiencing rapid growth, driven by rising consumer awareness of preventive care, chronic disease management, and telemedicine adoption. Patients increasingly rely on user-friendly, digital thermometers to monitor body temperature at home, supporting real-time communication with healthcare providers. The convenience of portable, accurate devices encourages households to invest in reliable clinical thermometers, bridging the gap between institutional care and remote monitoring. This trend is particularly pronounced in regions where home-based healthcare programs are expanding and telehealth services are becoming widely accessible.

Advancements in connected health technologies are enhancing remote patient monitoring (RPM) programs and supporting evolving Current Procedural Terminology (CPT) reimbursement codes for connected care in 2026. In line with this trend, Smart Meter launched a cellular-enabled thermometer in December 2025, capable of transmitting temperature data directly via cellular networks without requiring Bluetooth, Wi-Fi, or additional hub devices. This solution enables seamless, real-time monitoring at home, offering reliable, user-friendly, and fully integrated temperature tracking. Such innovations highlight the growing role of digital health tools in homecare, validating market expansion driven by technological integration and increasing consumer demand for accessible, precise at-home diagnostics.

Regulatory Hurdles and Compliance Costs

The clinical electronic thermometer market faces significant challenges due to stringent medical device regulations such as FDA 510(k) requirements in the U.S. and the European Union (EU) Medical Device Regulation (MDR). Manufacturers must comply with rigorous testing, documentation, and quality protocols, which ensure safety and accuracy but substantially increase operational complexity. For small and medium-sized original equipment manufacturers (OEMs), meeting these regulatory standards can elevate production costs and extend the time-to-market for new devices, potentially limiting competitiveness. These requirements also demand dedicated resources for regulatory affairs, adding overhead and stretching operational budgets.

Adding to the regulatory burden, amendments to the EU MDR now require manufacturers to notify authorities and downstream stakeholders of foreseeable supply interruptions, increasing compliance complexity and administrative workload. Such requirements can delay product launches, particularly for innovative or advanced devices, and reinforce the need for careful planning and investment to maintain market readiness while meeting evolving regulatory expectations. Companies must also continuously monitor regulatory updates across regions to avoid penalties and ensure uninterrupted market access.

Competitive Pricing Pressure and Supply Chain Constraints

Competition from low-cost manufacturers, especially in Asia, continues to put pressure on average selling prices (ASPs), compressing margins for established brands. Branded players must balance maintaining quality and compliance with market pricing expectations, which can be particularly challenging in cost-sensitive regions. Companies must differentiate through innovation, service, or digital health integration to retain market share and sustain profitability. These pressures are particularly acute when launching new products, as initial costs are often higher due to R&D and regulatory compliance.

Supply chain vulnerabilities further exacerbate challenges. The renewed tariff policies on medical device imports, including labeling tariffs on European devices entering the U.S., were reported to increase costs and strain international supply chains. Combined with the limited availability of critical components such as precision sensors and semiconductors, manufacturers face heightened risk of production delays and price volatility. Companies may adopt vertical integration or inventory buffer strategies, which increase fixed costs but are necessary to maintain continuity in a highly competitive and globally connected market. Planning for multiple contingencies has become essential to mitigate disruptions and maintain customer trust.

Healthcare Infrastructure Development in Emerging Economies

Rapid urbanization and healthcare development in regions such as Asia Pacific, Latin America, and the Middle East & Africa are creating significant opportunities for clinical electronic thermometers. Governments in these regions are increasing healthcare facility counts, investing in diagnostic infrastructure, and expanding reimbursement schemes, particularly as universal health coverage goals accelerate procurement. Rising awareness of preventive care and patient monitoring is also driving demand in both public and private healthcare settings, creating untapped markets for advanced thermometry solutions.

These emerging markets are expected to register higher-than-average growth rates, reflecting evolving healthcare infrastructure, expanding clinical capacity, and increasing disposable income among urban populations. In November 2025, for instance, the FDA cleared a new AI-powered “thermometer of the future” that integrates temperature measurement with cardiac and pulmonary monitoring. This regulatory endorsement demonstrates growing confidence in next-generation diagnostic tools and highlights opportunities to introduce multifunctional, precise thermometers in expanding healthcare markets.

Digital Integration, Wearables, and Product Diversification

The integration of clinical thermometers with digital health ecosystems presents strong growth potential. Devices that sync with mobile health apps, electronic health records (EHRs), and telehealth platforms enable continuous patient monitoring, data analytics, and seamless communication between patients and healthcare providers. This trend aligns with the broader expansion of connected care solutions and creates opportunities for collaborations with software developers, telehealth networks, and hospital IT systems.

Wearable and continuous body temperature monitoring is also creating new avenues for market growth. Real-time wearable systems capable of continuous monitoring can detect fever early and alert caregivers, enabling proactive intervention and improved patient outcomes. These technologies extend thermometry beyond traditional spot checks to ongoing health surveillance, offering opportunities for innovative products in hospitals, homecare, and remote monitoring programs. When combined with customized designs for pediatrics, geriatrics, and non-contact use, these devices provide both differentiation and access to high-value niche segments.

Category-wise Analysis

Product Type Insights

Oral thermometers are anticipated to hold an estimated 42% of the clinical electronic thermometer market revenue share in 2026, due to their balance of accuracy, reliability, and cost-effectiveness across hospitals, clinics, and homecare settings. Trusted for routine vital checks, fever monitoring, and post-operative care, these devices integrate with digital displays and data logging to enhance workflow efficiency and patient record management. Mercury-free, fast-response models are increasingly replacing older units, aligning with infection control standards and regulatory expectations. In 2025, advanced digital oral thermometers, including non-contact and connected models, were widely adopted, offering rapid readings, hygiene improvements, and compatibility with EHRs. These developments reinforce oral thermometers’ leadership while supporting growing clinical and homecare demand.

Ear thermometers are the fastest-growing product types, projected at 8.5% CAGR through 2033, driven by non-invasive, rapid, and hygienic designs. Portable and user-friendly, these devices suit both clinical and homecare settings, and their digital connectivity enables integration with remote patient monitoring and EHR systems. Pediatric and geriatric populations benefit from comfort-focused designs, supporting broad adoption. Industry trends show increasing uptake of connected, fast-response thermometers for clinical and consumer use, complementing telehealth and preventive care initiatives. This combination of hygiene, convenience, and digital integration underpins strong long-term growth.

End-User Insights

Hospitals are poised to lead in 2026 with an estimated 55% of the clinical electronic thermometer market share, driven by high patient volumes and regulatory requirements for precise, reliable thermometry. Critical care, emergency, and surgical departments rely on accurate devices for continuous monitoring and evidence-based decision-making. Institutional procurement favors units compatible with EHRs and connected platforms, ensuring workflow integration. Remote patient monitoring adoption in U.S. hospitals expanded significantly, linking bedside temperature data to centralized digital systems. This integration strengthens demand for advanced thermometers that combine speed, accuracy, and digital connectivity, reinforcing hospitals’ dominance.

Homecare settings are the fastest-growing end-user segment, projected at 9% CAGR through 2033, as consumers adopt self-monitoring and connected health solutions. Smart thermometers enable real-time tracking, trend analysis, and data sharing with healthcare providers, supporting preventive care and chronic disease management. Ease of use, rapid readings, and digital compatibility drive adoption among tech-savvy households and aging populations. Hospital-at-home and virtual ward programs deployed connected thermometers as part of remote care kits, reducing readmissions and improving outcomes. These developments highlight the segment’s strong growth potential and the expanding role of telehealth-integrated devices.

Regional Insights

North America Clinical Electronic Thermometer Market Trends

North America is likely to be the largest regional market for clinical electronic thermometers, contributing an estimated 38% of the global revenues in 2026, supported by advanced healthcare infrastructure, widespread telehealth adoption, and robust digital health initiatives. U.S. healthcare providers continue integrating RPM solutions, linking temperature and other vital signs to electronic systems as part of chronic care and hospital-at-home programs. During 2025–2026, the Department of Health & Human Services (HHS) and DEA extended telemedicine flexibilities, allowing continued virtual care, while Congress reinstated telehealth reimbursements, creating a stable environment for digital device adoption. Federal telehealth bills and rural health program funding further encourage deployment of connected diagnostic tools across hospitals and homecare.

The expansion of IoT-enabled temperature monitoring solutions, capable of real-time tracking and cloud integration, reinforces the adoption of clinical electronic thermometers. With strong healthcare investment, high digital health penetration, and supportive reimbursement frameworks under federal programs, North America leads adoption of connected devices. As RPM becomes a core component of care delivery strategies, encompassing continuous temperature and vital sign monitoring, demand for smart thermometers in hospitals and homecare settings is projected to grow steadily, backed by both policy support and market readiness.

Europe Clinical Electronic Thermometer Market Trends

Europe remains a substantial regional market for clinical electronic thermometers, driven by strong clinical demand across Germany, the U.K., France, and Spain. A key enabler is the European Health Data Space (EHDS) regulation, which came into force in March 2025 to facilitate secure exchange and use of electronic health data, supporting digital health adoption and integration of diagnostic devices. Hospitals and clinics are increasingly linking temperature and other vital signs data with unified health records, improving clinical decision-making, workflow efficiency, and cross-border continuity of care. Public health initiatives and hospital modernization programs further encourage adoption of advanced monitoring technologies.

European healthcare providers are also prioritizing non-contact, rapid-reading, and infection-control-friendly thermometers, aligning with broader EU digital health and patient safety strategies. The digital health and telemedicine conferences across Europe highlighted connected devices, wearable biosensors, and remote monitoring platforms, demonstrating strong momentum for embedding smart temperature monitoring in routine clinical care. This combination of regulatory support, innovation hubs, and technology adoption underpins ongoing demand for connected and advanced thermometry solutions throughout the region.

Asia Pacific Clinical Electronic Thermometer Market Trends

Asia Pacific is projected to be the fastest-growing regional market, exhibiting an estimated 2026-2033 CAGR of 9%, fueled by substantial investments in digital health infrastructure, rising smartphone and broadband penetration, and expanded access to remote care models. Governments and regional bodies are increasingly aligning strategy around digital health and innovation, recognizing technology as a critical tool to strengthen healthcare systems amid demographic shifts and aging populations. At the APEC health ministers’ forum in 2025, leaders emphasized the importance of leveraging innovative technologies and data systems to bolster health system effectiveness, long-term health security, and digital health cooperation across the region.

Accelerated adoption of digital health platforms across Asia Pacific is contributing to uptake of advanced temperature monitoring technologies in both hospital and homecare settings, as part of broader remote patient monitoring and connected care strategies. The World Health Organization (WHO) Western Pacific Office published a Regional Action Framework on Digital Health, aimed at empowering countries to harness digital tools to improve service delivery and expand access to quality healthcare. These initiatives, combined with national programs integrating telehealth, interoperable data architectures, and AI-enabled health solutions, are creating fertile conditions for smart clinical thermometers that can feed real-time data into national digital health ecosystems.

Competitive Landscape

The global clinical electronic thermometer market structure is moderately consolidated, led by global medical device companies such as Omron Healthcare, Braun GmbH, Exergen Corporation, Microlife Corporation, and Thermo Fisher Scientific. These players leverage strong brand recognition, established hospital and homecare distribution networks, and regulatory approvals to maintain broad adoption. They invest heavily in R&D for digital connectivity, IoT-enabled devices, and integrated data management, ensuring alignment with clinical and consumer needs. Their products are increasingly integrated into hospital EHRs and remote patient monitoring systems, reinforcing adoption in both institutional and homecare settings.

Smaller and niche competitors, including iProven, Beurer GmbH, A&D Medical, and Tecnimed Srl, focus on cost-effective, advanced sensor technologies targeting specialized segments. Market dynamics favor connected thermometers with real-time data reporting, mobile app integration, and multi-user capabilities, responding to rising demand for remote patient monitoring and digital health platforms. Regulatory compliance and interoperability remain barriers for new entrants, but partnerships with telehealth providers and healthcare networks are expanding market participation. Innovation, digital integration, and connectivity are key differentiators shaping competitive strategies in this sector.

Key Industry Developments

- In January 2026, Nextemp enhanced modern health monitoring with its single-use thermometers and a new smart tracking app that helps users record and manage temperature data digitally. This combination aims to streamline self-care and improve symptom tracking for patients and caregivers.

- In December 2025, Smart Meter launched the first handheld cellular-connected thermometer designed for effortless patient monitoring, enabling real-time vital sign tracking without Wi-Fi. The device is aimed at enhancing remote care workflows by automatically transmitting temperature data to clinicians and caregivers.

- In June 2025, the U.S. FDA issued a final rule exempting certain Class II clinical electronic thermometers from premarket notification (510(k)) requirements, provided they exclude telethermographic and continuous monitoring functions and meet validated performance standards. The amendment reduces regulatory burden while maintaining safety oversight under established standards such as ISO 80601-2-56 and applicable ASTM specifications.

Companies Covered in Clinical Electronic Thermometer Market

- Omron Healthcare

- GE Healthcare

- Philips Healthcare

- A&D Company Ltd.

- Contec Medical Systems Co., Ltd.

- Nonin Medical, Inc.

- Masimo Corporation

- Hill Rom Holdings, Inc.

- Nihon Kohden Corporation

- Braun

- Microlife Corporation

- 3M Healthcare

Frequently Asked Questions

The global clinical electronic thermometer market is projected to reach US$ 1.68 billion in 2026.

Growth is driven by rising healthcare infrastructure investment, digital diagnostics adoption, and home-based health monitoring.

The market is poised to witness a CAGR of 8.1% from 2026 to 2033.

Opportunities exist in emerging markets, integration with digital health ecosystems, and development of smart or wearable thermometers.

Leading players include Omron Healthcare, Braun GmbH, Exergen Corporation, Microlife Corporation, Thermo Fisher Scientific, iProven, Beurer GmbH, A&D Medical, and Tecnimed Srl.