- Healthcare IT

- Clinical Communication and Collaboration Market

Clinical Communication and Collaboration Market Size, Share, and Growth Forecast 2026 - 2033

Clinical Communication and Collaboration Market by Component (Hardware, Software, Services), by Content Type (Text, Video, Voice), by End User (Clinical Labs, Hospitals, Physicians, Hotels, Retail, Correctional Facilities, Others), by Regional Analysis, 2026-2033

Clinical Communication and Collaboration Market Size and Trend Analysis

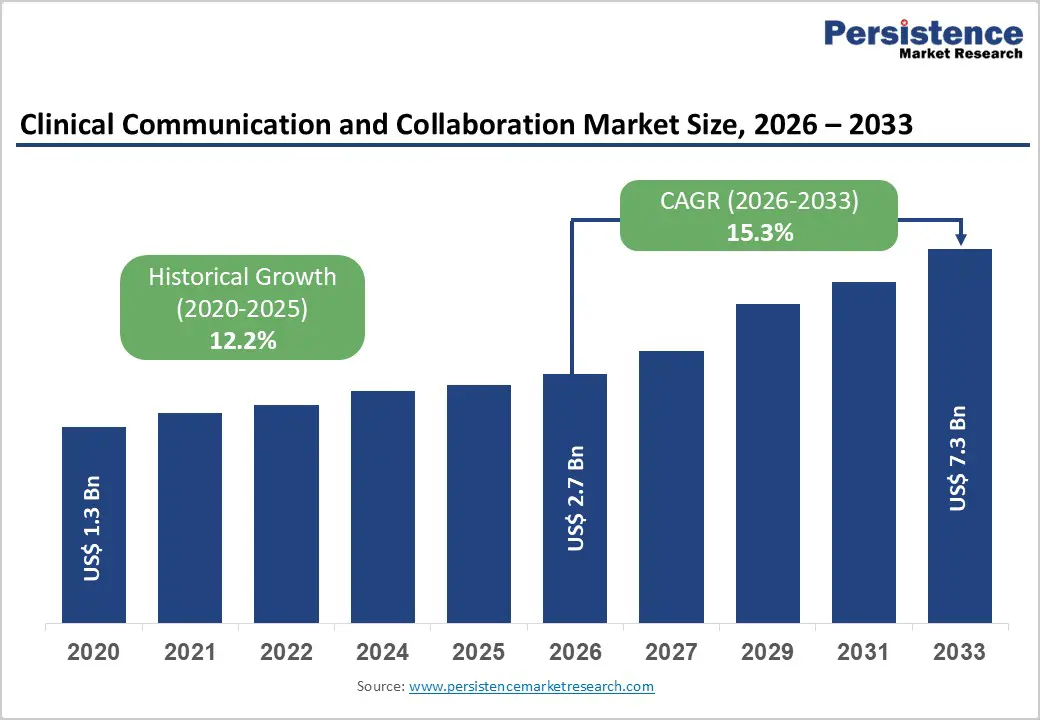

The global clinical communication and collaboration market size is expected to be valued at US$ 2.7 billion in 2026 and projected to reach US$ 7.3 billion by 2033, growing at a CAGR of 15.3% between 2026 and 2033.

The primary driver is the rising demand for real-time, secure communication among healthcare professionals to enhance patient safety and care coordination. This is supported by the increasing adoption of digital health solutions, as hospitals face growing patient volumes and complex multidisciplinary teams, necessitating tools that reduce response times and medical errors. Additionally, regulatory pressures from bodies like the FDA and HIPAA compliance requirements are accelerating the shift from legacy systems like pagers to integrated platforms.

Key Market Highlights

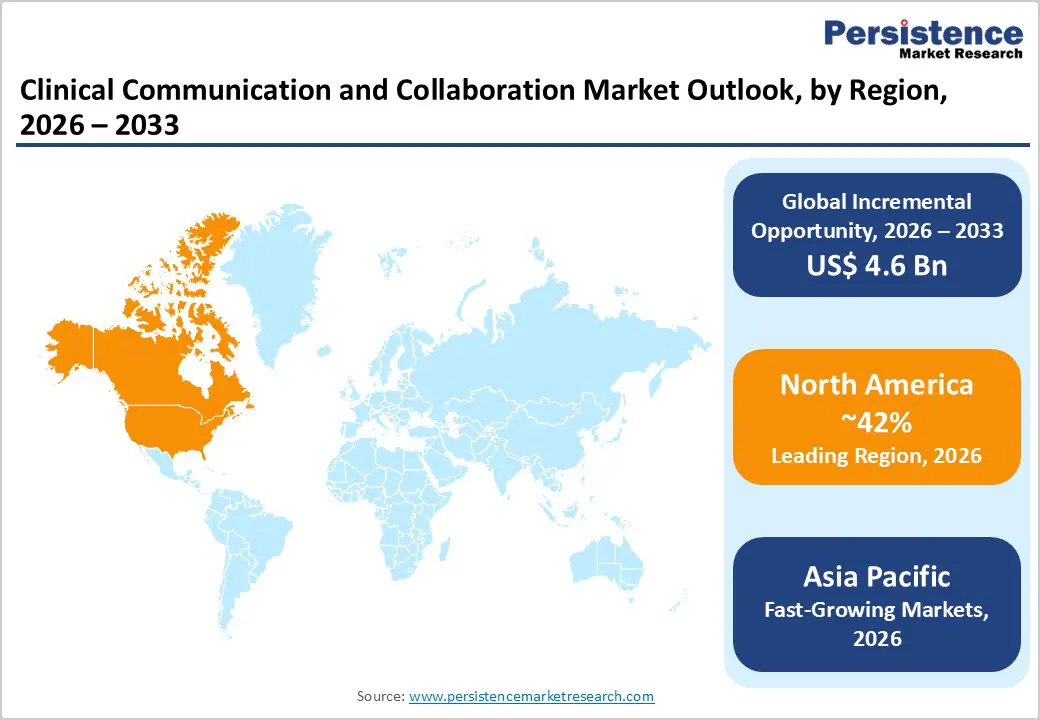

- North America dominates the clinical communication and collaboration market, supported by advanced healthcare IT infrastructure, high digital-health spending, strong regulatory frameworks, and widespread EHR integration.

- Asia Pacific is the fastest-growing region, driven by hospital digitalization programs, telemedicine expansion, government healthcare initiatives, rising chronic disease burden, and workforce shortages.

- Software platforms represent the largest product segment due to recurring subscription models, secure messaging adoption, alarm-management systems, and growing demand for workflow automation.

- Hospitals and integrated delivery networks remain the leading end users, fuelled by patient-safety mandates, value-based care models, clinician coordination needs, and emergency-department throughput optimization.

| Key Insights | Details |

|---|---|

|

Clinical Communication and Collaboration Market Size (2026E) |

US$ 2.7 billion |

|

Market Value Forecast (2033F) |

US$ 7.3 billion |

|

Projected Growth CAGR (2026-2033) |

15.3% |

|

Historical Market Growth (2020-2025) |

12.2% |

Market Dynamics

Driver: Demand for Real-Time Care Coordination

Healthcare systems are increasingly prioritizing real-time clinical communication platforms to improve coordination among physicians, nurses, pharmacists, and allied staff. Fragmented workflows and delayed information exchange remain major contributors to treatment errors, prompting hospitals to replace legacy paging systems with secure, mobile-first solutions. These platforms enable instant alerts, escalation pathways, and team-based messaging, allowing clinicians to respond rapidly to changes in patient conditions. Integration with electronic health records further streamlines workflows by embedding clinical context into conversations, reducing duplication and minimizing handoff gaps across departments.

High-acuity environments such as emergency rooms, ICUs, and surgical units are major adopters, where seconds can directly influence patient outcomes. Faster clinical decisions, reduced length of stay, and improved throughput strengthen the business case for investment. As hospitals pursue operational efficiency and quality benchmarks, real-time communication tools are becoming a foundational layer of modern digital health infrastructure.

Regulatory Compliance and Patient Safety Mandates

Regulatory frameworks governing data protection and clinical documentation are accelerating adoption of compliant communication platforms. Laws such as HIPAA in the U.S. and evolving FDA digital health guidance require healthcare organizations to ensure secure transmission of patient information, audit trails, and traceable clinical decisions. Global health agencies continue to highlight communication breakdowns as major contributors to adverse events, reinforcing the need for encrypted messaging systems that meet regulatory scrutiny.

These mandates align closely with value-based care models, where hospitals must demonstrate quality outcomes and coordinated treatment pathways to secure reimbursement. Platforms that support documentation, escalation logs, and interoperability with hospital IT systems enable organizations to meet compliance obligations while strengthening patient safety initiatives. As accreditation standards tighten worldwide, regulatory pressure will remain a long-term structural driver for market expansion.

Restraint: High Implementation and Integration Costs

Despite strong demand, the market faces challenges from the high cost of deploying enterprise-grade clinical communication platforms. Hospitals often incur significant expenditures on software licensing, mobile hardware, network upgrades, cybersecurity frameworks, and staff training programs. Integrating these solutions with legacy EHR systems and nurse call platforms adds further complexity, requiring lengthy customization cycles and IT consulting support.

Smaller hospitals and rural facilities are particularly constrained by budget limitations, slowing adoption in price-sensitive markets. For many institutions, replacing existing pager systems or siloed tools requires substantial capital approval, delaying digital modernization initiatives. Unless vendors develop modular, cloud-based, and subscription-driven offerings that reduce upfront investment, cost barriers may continue to restrain penetration in emerging healthcare systems.

Data Security and Privacy Concerns

Cybersecurity risks present a major restraint in the adoption of clinical communication platforms, as hospitals increasingly become targets for ransomware and data breaches. These systems handle highly sensitive patient data, making security failures potentially catastrophic from both regulatory and reputational standpoints. Compliance with global data privacy frameworks such as GDPR further complicates deployments, requiring sophisticated encryption, access controls, and monitoring protocols.

Healthcare executives remain cautious about migrating communications to mobile or cloud environments without robust safeguards. Breaches can lead to financial penalties, legal exposure, and operational disruptions, eroding confidence in digital transformation strategies. Vendors that cannot clearly demonstrate security certifications and incident-response readiness may struggle to gain trust, particularly among large hospital networks and public healthcare institutions.

Opportunity: Expansion in Telemedicine and Virtual Care

Rapid growth in telemedicine and hybrid care delivery models is opening new opportunities for clinical communication platforms. Hospitals increasingly rely on virtual consultations, remote monitoring, and decentralized care teams, creating demand for tools that support voice, video, and cross-site collaboration. Government digitization initiatives and post-pandemic care reforms have further accelerated this transition, especially across Asia Pacific and emerging healthcare markets.

As care delivery extends beyond physical hospital walls, interoperable communication systems capable of connecting clinicians, home-care providers, and patients become essential. Vendors that design scalable platforms supporting telehealth workflows, multilingual interfaces, and cloud deployment models are well positioned to capture expanding demand. This shift toward distributed care ecosystems represents one of the most attractive long-term growth avenues in the market.

AI and 5G-Enabled Innovations

Technological advancements in artificial intelligence, 5G connectivity, and IoT are reshaping the competitive landscape of clinical communication solutions. AI-driven alert prioritization, predictive analytics, and workflow automation enable clinicians to focus on high-risk cases, reducing alarm fatigue and accelerating clinical decisions. High-speed 5G networks further support real-time video collaboration and data-heavy applications, particularly in emergency and critical care environments.

Healthcare providers are increasingly investing in digital infrastructure, favoring platforms that can leverage these emerging technologies. Solutions incorporating intelligent triaging, clinical decision support, and analytics dashboards are expected to gain preference among large hospital systems. As innovation becomes a key differentiator, vendors that embed AI and connectivity into their platforms will likely dominate next-generation deployments across high-acuity clinical settings.

Category-wise Insights

Component Analysis

Healthcare providers are working hard to deliver better patient care, complete tasks more quickly, and reduce unnecessary spending. They are seeking solutions that may transform interaction and teamwork into production processes and higher-quality patient care. The needs of advanced communications in the international healthcare sector can be met by compliant secure mobile messaging systems

With the use of a regulation-compliant messaging service, a number of advantages can be realized, including workflow efficiency and improved collaboration. These factors will likely result in increased sales for the clinical communications and collaboration software segment over the course of the projected year.

In 2022, the clinical communications and collaboration software market share was estimated to dominate the global market and account for 39.1% of the total market value share.

Content Analysis

In 2026, it was estimated that the text clinical communications and collaboration segment will account for 42% of the market share.

Most healthcare organizations are implementing clinical communication and collaboration solutions to improve patient care and satisfaction. Also, using content such as text, voice, and video, helps to improve communication capabilities by providing secure, traceable, and HIPAA-compliant communication between carers, physicians, and nurses.

Clinical communication and collaboration solution providers are working to address this issue by including the text clinical communications schedule in a comprehensive and unified smartphone directory. As a result, text clinical communications have a large market share.

Regional Insights

North America Clinical Communication and Collaboration Market Trends and Insights

North America remains the largest market for clinical communication and collaboration solutions, supported by highly developed healthcare infrastructure and early adoption of digital health technologies. Hospitals across the region are actively replacing legacy paging systems with secure, mobile-first platforms that integrate messaging, voice, and alarm management into unified workflows. The U.S. dominates regional demand, driven by strong hospital IT spending and frequent regulatory clearances that accelerate commercialization of advanced cloud-native systems. These tools enable rapid clinical escalation, reduce alarm fatigue, and embed real-time coordination directly into electronic health record environments, making them essential in high-acuity care settings such as emergency departments and intensive care units.

A mature innovation ecosystem further strengthens market leadership, with health technology startups, established vendors, and academic medical centers collaborating on next-generation platforms. Compliance requirements around data privacy and security encourage adoption of HIPAA-aligned solutions featuring encryption, audit trails, and role-based access controls. Rising clinician shortages and increasing patient volumes also push hospitals to rely on digital coordination tools to optimize workforce efficiency, sustaining long-term growth across the region.

Asia Pacific Clinical Communication and Collaboration Market Trends and Insights

Asia Pacific represents the fastest-growing regional market, fueled by widespread healthcare digitalization and rapid expansion of telemedicine services across major economies such as China, Japan, and India. Governments are investing heavily in hospital modernization programs, creating opportunities for vendors offering cloud-based and mobile-friendly communication platforms. In India, large-scale public healthcare initiatives are accelerating technology adoption in secondary and tertiary hospitals, while domestic manufacturing ecosystems are enabling cost-effective deployment models. China continues to integrate smart hospital frameworks, incorporating AI-driven alerts and workflow automation to manage growing patient volumes and rising chronic disease burdens.

Southeast Asian nations are also emerging as attractive growth markets due to population expansion, urbanization, and improving access to healthcare services. Japan, meanwhile, focuses on addressing workforce shortages and an aging population through advanced digital solutions that enhance care coordination and remote monitoring. These regional dynamics collectively position Asia Pacific as a high-growth opportunity for global and regional clinical communication platform providers.

Competitive Landscape

Market Structure Analysis

The clinical communication and collaboration market is moderately consolidated, with leading players strengthening their positions through continuous product innovation and international expansion. Vendors are launching cloud-based, mobile-first platforms with advanced alarm management, AI-driven prioritization, and deep EHR integration to differentiate offerings and capture hospital contracts. Strategic partnerships with digital health firms, telecom providers, and hospital IT vendors remain a core growth strategy, enabling faster deployment and enhanced interoperability. Collaborations also support regulatory compliance and cybersecurity enhancements. As healthcare systems accelerate digital transformation initiatives, companies combining strong technology portfolios, global reach, and ecosystem partnerships are expected to dominate competitive dynamics over the forecast period.

Key Market Developments

- In August 2023, TigerConnect, a leading provider of clinical collaboration solutions for healthcare, announced that its Physician Scheduling platform had been validated by KLAS Research within the Physician Scheduling category.

- In May 2022, Mobile Heartbeat announced an integration partnership with Stryker Corporation, enabling its Inbound Alerting API to receive bed-exit notifications and enhance real-time clinical response capabilities.

Companies Covered in Clinical Communication and Collaboration Market

- Vocera Communications

- TigerConnect

- Intelligent Business Communication – AGNITY

- Cisco Systems Inc.

- Jive Software

- Microsoft Corporation

- Everbridge

- PerfectServe, Inc.

- Uniphy Health Systems LLC

- UDG Healthcare PLC

- Ascom

- NEC Corporation

- Spok Inc.

- Voalte

- Others

Frequently Asked Questions

The global clinical communication and collaboration market is valued at US$ 2.7 billion in 2026.

Rising need for real-time multidisciplinary coordination, EHR integration, regulatory compliance, patient safety improvements, and faster response times across hospitals.

North America leads with 42% share in 2025.

Expanding telemedicine adoption, hybrid care models, AI-enabled workflows, 5G connectivity, and scalable cloud platforms across emerging healthcare markets globally.

Vocera Communications, TigerConnect, Intelligent Business Communication AGNITY, Cisco Systems Inc., Jive Software, and Microsoft Corporation.