- Food Ingredients & Additives

- Cheese Powder Market

Cheese Powder Market Size, Share, and Growth Forecast 2026 - 2033

Cheese Powder Market by Cheese Type (Cheddar, Mozzarella, Parmesan, American, Others), Application (Snacks, Bakery & Confectionery, Sauces, Dips & Dressings, Soups & Ready Meals, Others), Distribution Channel (Supermarkets/Hypermarkets, Convenience & Specialty Stores, Online Retail, Foodservice), and Regional Analysis, 2026 - 2033

Cheese Powder Market Share and Trends Analysis

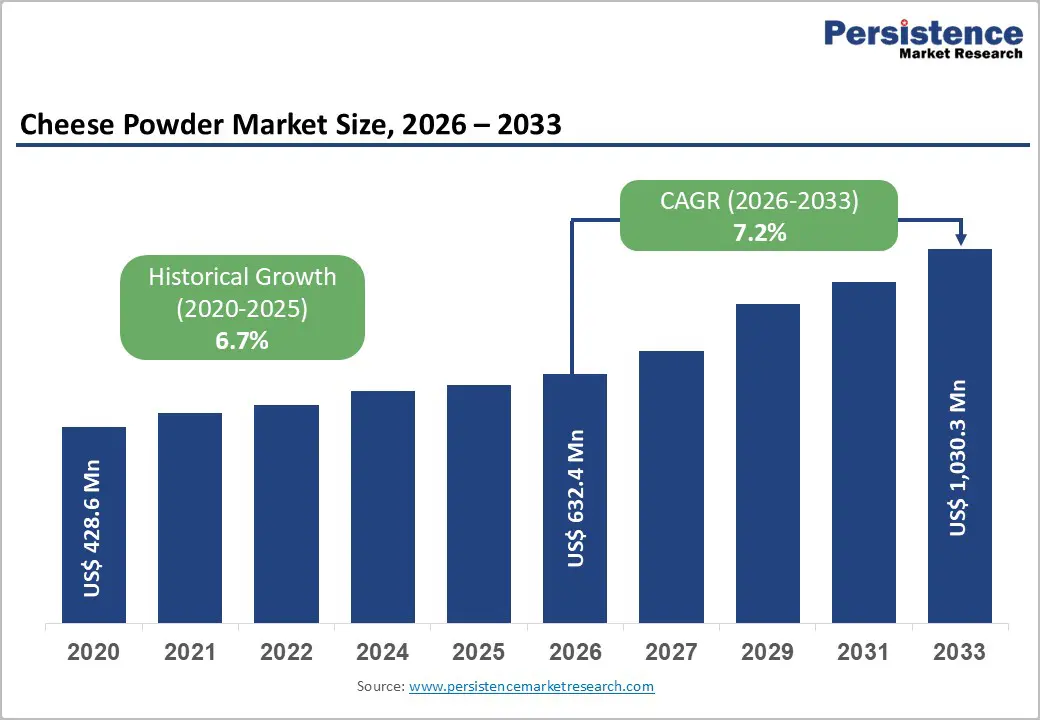

The global cheese powder market size is expected to be valued at US$ 632.4 million in 2026 and projected to reach US$ 1,030.3 million by 2033, growing at a CAGR of 7.2% between 2026 and 2033.

Market growth is underpinned by accelerating consumption of processed and convenience foods, especially cheese-flavoured snacks, ready meals, and instant sauces, where cheese powder offers flavour intensity, shelf stability, and formulation flexibility. Rising per capita cheese consumption in developed and emerging markets, supported by data from organizations such as the OECD-FAO and national dairy boards, reflects strong consumer preference for dairy-based flavours in packaged foods, quick-service restaurant offerings, and retail snacks. In parallel, technological advances in spray-drying and encapsulation are allowing manufacturers to deliver better solubility, controlled fat content, and clean-label variants, which align with regulatory and retailer demands for ingredient transparency and nutritional improvement in processed foods.

Key Industry Highlights:

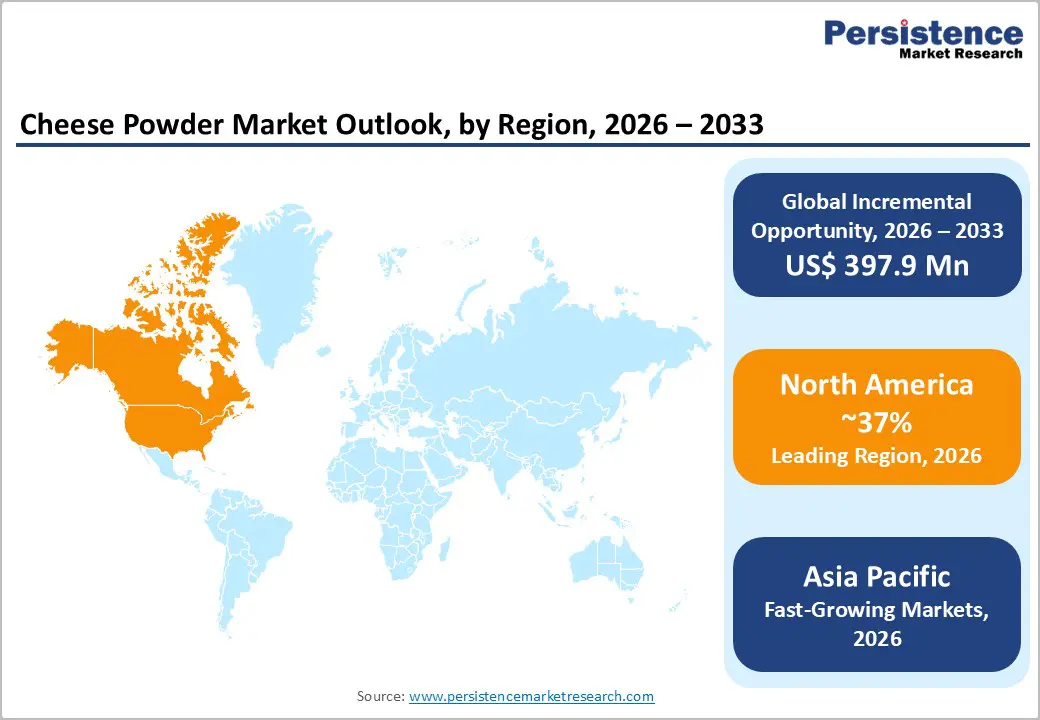

- Leading Regional Market: North America holds around 37% of global cheese powder revenue in 2025, supported by high per capita cheese consumption, a well-developed processed food and snack industry, and extensive use of cheese powders in retail and foodservice applications.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, driven by the rapid expansion of QSR chains, modern retail, and processed food manufacturing in countries such as China, India, and ASEAN markets, where Western-style cheese-flavoured products are gaining popularity.

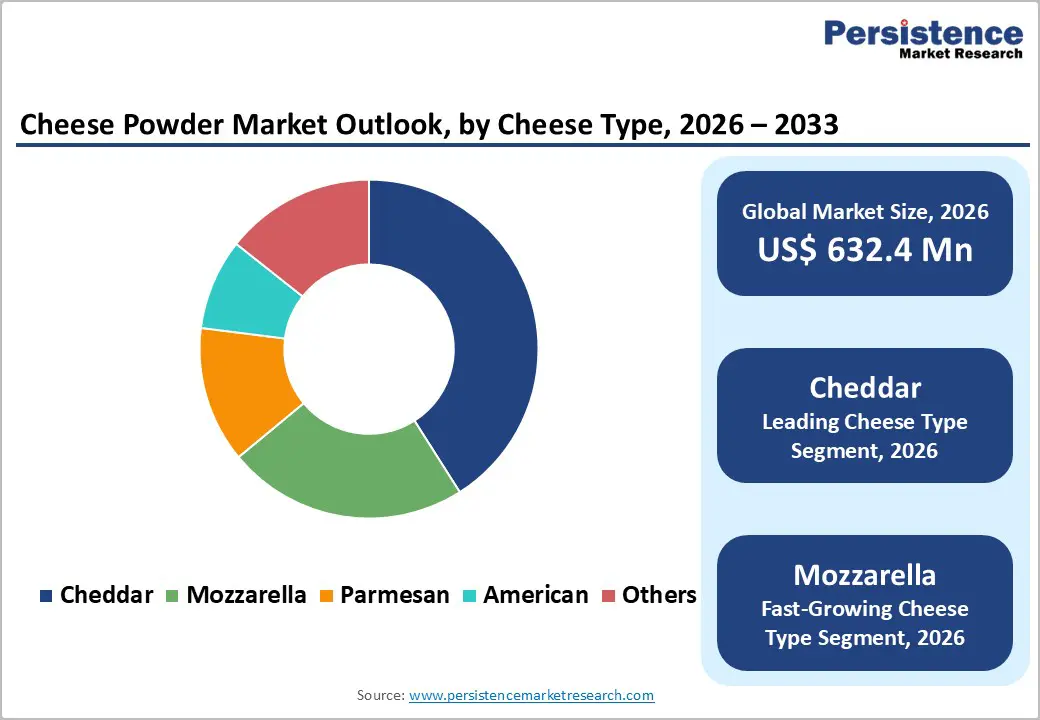

- Cheddar as Dominant Cheese Type Segment: Cheddar leads the cheese type category with about 41% share in 2025, owing to its versatile, familiar flavour profile and its entrenched use in cheese-flavoured snacks, dry sauces, seasonings, and macaroni and cheese-style products worldwide.

- Mozzarella as Fastest-Growing Cheese Type Segment: Mozzarella is the fastest-growing cheese type segment, benefiting from expanding consumption of pizza, pasta, and Italian-inspired ready meals and snacks, especially in the Asia Pacific and other emerging markets where Western foodservice formats are proliferating.

- Premium, Clean-Label, and Functional Cheese Powders as Key Opportunity: The development of clean-label, reduced-sodium, organic, and specialty cheese powders tailored to health-conscious consumers and premium product lines represents a major opportunity, enabling ingredient suppliers to capture higher-value business with global brands and private labels.

| Key Insights | Details |

|---|---|

| Cheese Powder Market Size (2026E) | US$ 632.4 million |

| Market Value Forecast (2033F) | US$ 1,030.3 million |

| Projected Growth CAGR (2026-2033) | 7.2% |

| Historical Market Growth (2020-2025) | 6.7% |

Market Dynamics

Drivers - Rising Demand for Convenience Foods and Cheese-Flavoured Snacks

A primary growth driver for the cheese powder market is the global shift towards convenience foods and snackification of diets, especially among younger and urban populations. Industry and trade data show that retail sales of savoury snacks, instant noodles, and ready-to-eat meals have increased steadily in regions such as North America, Europe, and Asia Pacific, supported by changing lifestyles, higher employment rates, and on-the-go consumption patterns. Cheese powder is a critical functional ingredient in extruded snacks, popcorn, coated nuts, crackers, and instant pasta or macaroni, delivering intense cheese flavour with consistent quality, long shelf life, and easy dry blending. Major food manufacturers and quick-service restaurant suppliers use cheddar and other cheese powders in seasoning blends and dry mixes, enabling scalable production without the storage and microbiological challenges associated with natural cheese. As global snack volumes expand and foodservice operators expand cheese-flavoured offerings, cheese powder demand is expected to grow in tandem.

Growing Global Cheese Production and Dairy Ingredient Utilization

Expanding cheese production and broader use of dairy ingredients in processed foods provide structural support to the cheese powder market. According to international dairy and agricultural statistics, world cheese production has been rising steadily, with Europe and North America accounting for a significant share of output, and production growing in the Asia Pacific as well. This expansion increases the availability of cheese streams suitable for drying and value addition. Cheese powder allows dairies and ingredient companies to utilise cheese in forms that are easier to ship, store, and incorporate into processed foods, thereby capturing additional value from dairy supply chains. Government and industry programmes promoting dairy exports in countries such as the United States, New Zealand, and EU member states often emphasize the role of high-value ingredients like cheese powders in penetrating emerging markets. As food manufacturers seek to differentiate products with authentic dairy flavours and nutritional cues, cheese powder becomes a strategic ingredient choice.

Restraints - Health Concerns Related to Sodium, Fat, and Ultra-Processed Foods

A key restraint for the cheese powder market arises from growing consumer and regulatory scrutiny of sodium, saturated fat, and ultra-processed food intake. Public health agencies and nutrition guidelines in many countries recommend limiting the consumption of high-salt and high-fat foods to reduce risks of obesity, cardiovascular disease, and hypertension. Conventional cheese powders used in snacks and sauces can contribute meaningful amounts of sodium and fat, and their frequent use in highly processed products may deter health-conscious consumers. Retailers and foodservice operators are increasingly pressured to reformulate to meet voluntary and mandatory targets for salt and fat reduction, which can constrain the use rate or require development of lower-salt, reduced-fat cheese powders. Additionally, the broader movement towards minimally processed foods and “kitchen cupboard” ingredients creates challenges for some cheese powder formulations that rely on emulsifying salts, anti-caking agents, or flavour enhancers.

Price Volatility Linked to Dairy Markets and Input Costs

The cheese powder market is also exposed to price volatility stemming from fluctuations in milk and cheese prices, as well as energy and logistics costs for spray-drying and distribution. International dairy market reports regularly highlight periods of volatility driven by changes in milk supply, feed costs, weather events, and trade policy shifts. When raw cheese or milk prices increase sharply, the cost of producing cheese powder rises, compressing margins for ingredient suppliers and potentially raising prices for food manufacturers. High energy costs affect drying operations, while transport disruptions and container shortages can impact exports. In cost-sensitive applications or in emerging markets where consumer purchasing power is limited, end-product manufacturers may respond to elevated input costs by reducing cheese content, switching to alternative flavouring systems, or regionalising supply, thereby dampening growth prospects for cheese powder in those periods.

Opportunity - Innovation in Clean-Label, Reduced-Sodium and Specialty Cheese Powders

One of the most attractive opportunities in the cheese powder market lies in formulating clean-label, nutritionally improved, and specialty cheese powders targeted at health-conscious and premium segments. Food manufacturers are increasingly seeking ingredients that support “no artificial flavours or colours”, “reduced sodium”, and “natural” claims, while maintaining taste and functionality. Advances in processing, use of natural anti-caking agents, and flavour optimisation allow producers to launch cheese powders with lower sodium levels, improved fat profiles, and shorter ingredient lists. Specialty variants-such as organic cheese powder, non-GMO offerings, or powders derived from specific origin cheeses (e.g. Italian-style hard cheese, goat cheese) provide differentiation for premium snacks, bakery products, and sauces. These innovations align with retailer commitments to cleaner labels and with regulatory and public health initiatives targeting reformulation, giving ingredient suppliers scope to command higher margins and secure long-term partnerships with global brand owners.

Category-wise Analysis

Cheese Type Insights

Cheddar is the leading cheese type segment, accounting for about 41% of the global cheese powder market in 2025, reflecting its broad acceptance, versatile flavour profile, and deep integration into snacks and processed food formulations. Cheddar-style cheese has long been the default flavour for many extruded snacks, potato chips, cheese balls, and macaroni and cheese, particularly in North America and Europe, where consumer familiarity and preference are high. Industry breakdowns frequently show cheddar cheese powder contributing the largest share of revenue among cheese types, as it offers a robust, easily recognisable taste that pairs well with a variety of carriers and seasonings. Moreover, cheddar cheese production volumes are substantial worldwide, ensuring reliable raw material availability for powder manufacture. Mozzarella, by contrast, is the fastest-growing cheese type segment, propelled by the spread of pizza, pasta, and Italian-style ready meals in both developed and emerging markets, where mozzarella-style stretch and mild flavour are increasingly desired in dry mixes and sauces.

Application Analysis

Within applications, snacks represent the logical leading segment and can be reasonably estimated to hold a substantial share of the cheese powder market in 2025, given the longstanding use of cheese powder as a key flavouring in savoury snacks. Cheese-flavoured extruded products, baked snacks, popcorn, corn chips, and coated nuts rely on spray-dried cheese blends to provide consistent flavour and visual appeal, and snack manufacturers across North America, Europe, and Asia Pacific have steadily increased their cheese-based offerings. Global snack consumption data show double-digit growth in some emerging markets, while mature markets continue to trade up to premium and novel flavour variants, many of which include combinations of cheddar, mozzarella, parmesan, and other cheese notes. Sauces, dips & dressings, and soups & ready meals also represent important and growing application areas, but snacks maintain leadership due to scale and frequency of consumption. The fastest-growing application segment is often associated with ready meals and processed meal kits, where cheese powder enables convenient, shelf-stable cheese sauces and fillings that fit modern meal-preparation behaviours.

Distribution Channel Insights

Supermarkets and hypermarkets constitute the leading distribution channel for cheese powder-containing products and for retail cheese powder offerings, and can be considered to hold the largest segment share in 2025. Large-format retailers dominate grocery sales in many countries and are the primary point of sale for packaged snacks, dry sauce mixes, instant meals, and home-use cheese powder products sold under both manufacturer brands and private labels. Shelf space for cheese-flavoured snacks and ready meals has expanded in response to consumer demand, and supermarkets use promotions and in-store displays to drive trial of cheese-flavoured innovations. At the same time, foodservice is a structurally important channel for cheese powder utilisation, as QSR and restaurant supply chains rely heavily on industrial packs of cheese powders and blends for sauces, toppings, coatings, and batters, even though these volumes are not always visible to end consumers. Online retail is the fastest-growing channel in terms of percentage growth, driven by the rise of e-commerce grocery and direct-to-consumer snack brands, but supermarkets/hypermarkets remain the largest in absolute terms.

Regional Insights

North America Cheese Powder Market Trends and Insights

North America is the leading regional market, accounting for around 37% of global cheese powder value in 2025, supported by high per capita cheese consumption, a mature processed food industry, and strong presence of leading dairy and ingredient manufacturers. The United States is among the world’s largest cheese producers and consumers, with annual per capita cheese consumption exceeding 17-18 kg according to national dairy statistics, providing a solid base for cheese-flavoured product development. Cheese powder is widely used in iconic American snack categories such as flavoured corn chips, cheese puffs, boxed macaroni and cheese, and seasoning blends for QSR and foodservice. Well-established regulatory frameworks managed by bodies like the U.S. Food and Drug Administration (FDA) and the U.S. Department of Agriculture (USDA) define standards of identity for cheeses and dairy ingredients, while labelling rules drive transparency in ingredient listings and nutrition information.

Asia Pacific Cheese Powder Market Trends and Insights

Asia Pacific is the fastest-growing regional market for cheese powder, driven by rising disposable incomes, urbanisation, Westernisation of diets, and rapid expansion of food processing and foodservice industries in countries such as China, Japan, India, Indonesia, and other ASEAN economies. Traditionally, cheese consumption in many Asian markets was relatively low compared with Europe or North America, but recent decades have seen strong growth as consumers embrace pizza, burgers, cheese-flavoured snacks, and dairy-based bakery items. Quick-service restaurant chains and café concepts, both international and domestic, have expanded aggressively in major cities, stimulating demand for cheese and cheese-flavoured ingredients in toppings, fillings, sauces, and snack products. Cheese powder plays a crucial role as a stable, easy-to-handle flavouring component that can be transported and stored under challenging climatic conditions prevalent in parts of the region.

Food processing industries in China and India are investing heavily in capacity to supply packaged snacks, instant noodles, and ready meals tailored to local tastes, often incorporating cheese flavours to appeal to younger consumers. Regional dairy and ingredient companies, as well as global players like Fonterra Co-operative Group Limited and other multinational ingredient suppliers, are increasingly targeting Asia Pacific with cheese powder portfolios designed for local applications. Manufacturing cost advantages, favourable demographics, and government initiatives supporting food industry development are further strengthening Asia Pacific’s role as the key growth engine for the global cheese powder market over the coming decade.

Competitive Landscape

The cheese powder market is moderately consolidated, with a mix of global dairy ingredient manufacturers and regional specialty producers competing on product quality, flavor innovation, and pricing. Companies focus on expanding production capacity, improving spray-drying technologies, and developing customized formulations for snack, bakery, and ready-meal applications. Strategic partnerships with food processors and private-label brands are common to strengthen distribution networks. Clean-label trends and demand for natural ingredients are driving innovation in organic and preservative-free variants. Competitive intensity is increasing in emerging markets due to rising processed food consumption, while established markets emphasize premiumization and value-added functional blends to maintain margins and brand differentiation.

Key Market Developments

- In November 2025, MCT Manufacturing LLC-Bella Pak, a Wisconsin-based producer of dry grated cheeses, launched a new addition to its Mac Yourself powdered cheese sauce portfolio, Queso Blanco. The Mac Yourself brand had originally debuted in 2011 with its Cheddar Cheese powder, which gained strong popularity due to its creamy texture, rich flavor, and versatile use across a variety of applications.

Companies Covered in Cheese Powder Market

- Land O’Lakes, Inc.

- Kerry Group PLC

- The Kraft Heinz Company

- Archer Daniels Midland Company (ADM)

- Lactosan A/S

- Aarkay Food Products Ltd

- All American Foods, Inc.

- Commercial Creamery Company

- Kanegrade Limited

- Fonterra Co-operative Group Limited

- Glanbia plc

- Saputo Inc

- Ingredion Incorporated

- FrieslandCampina Ingredients

- IFF (International Flavors & Fragrances Inc.)

Frequently Asked Questions

The global cheese powder market is expected to reach approximately US$ 632.4 million in 2026, supported by growing use in snacks, sauces, ready meals, and foodservice applications worldwide.

Demand growth is primarily driven by rising consumption of convenience foods and cheese-flavoured snacks, increasing global cheese production, and greater use of cheese powders as stable, versatile flavouring ingredients in processed foods and quick-service restaurant offerings.

North America currently leads the cheese powder market, reflecting high per capita cheese consumption, a mature processed food and snack sector, and strong foodservice demand for cheese-flavoured products utilizing cheese powder-based solutions.

The most significant opportunity lies in developing clean-label, reduced-sodium, specialty, and regionally tailored cheese powders that meet health, regulatory, and premiumisation trends, particularly in fast-growing markets across Asia Pacific, Latin America, and the Middle East & Africa.

Key players include Land O’Lakes, Inc., Kerry Group PLC, The Kraft Heinz Company, Archer Daniels Midland Company (ADM), Lactosan A/S, Aarkay Food Products Ltd., All American Foods, Inc., Commercial Creamery Company, Kanegrade Limited, Fonterra Co-operative Group Limited, Glanbia plc, and Saputo Inc., among others.