- Food Ingredients & Additives

- Cheese Enzymes Market

Cheese Enzymes Market Size, Share, and Growth Forecast, 2026 - 2033

Cheese enzymes market by Source (Plant-Based, Animal-Based, Microorganisms-Based), Enzyme Type (Rennet, Lipases, Proteases, Others), Application (Cheese Production, Dairy Products, Yogurt, Milk, Infant Formula, Others), and Regional Analysis for 2026 – 2033

Cheese Enzymes Market Size and Trends Analysis

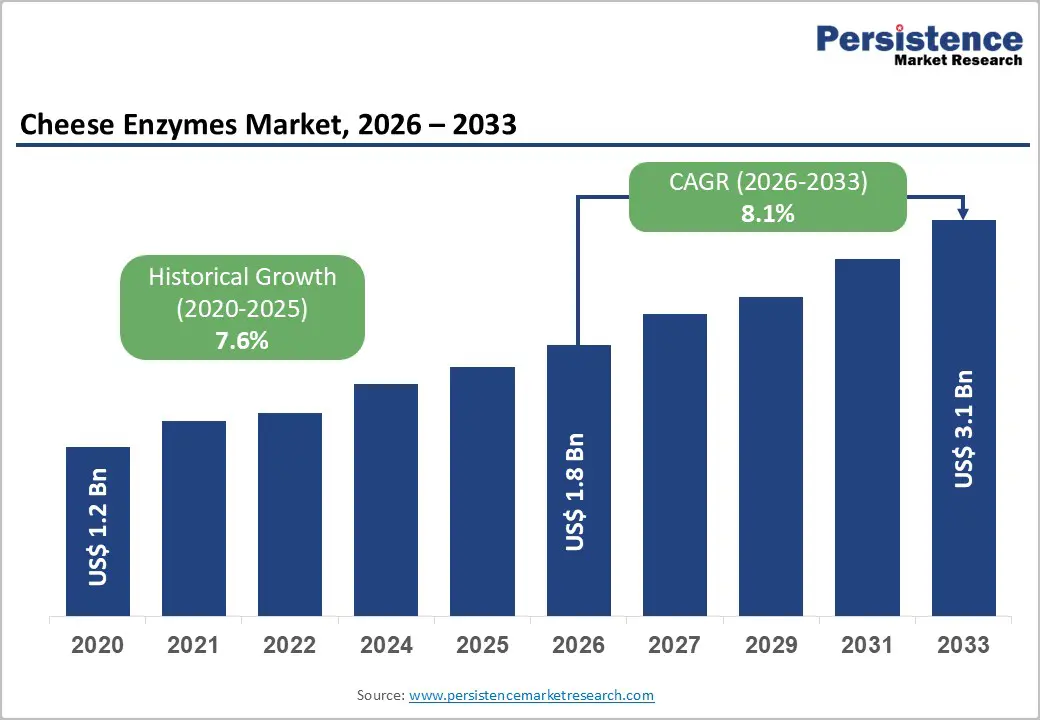

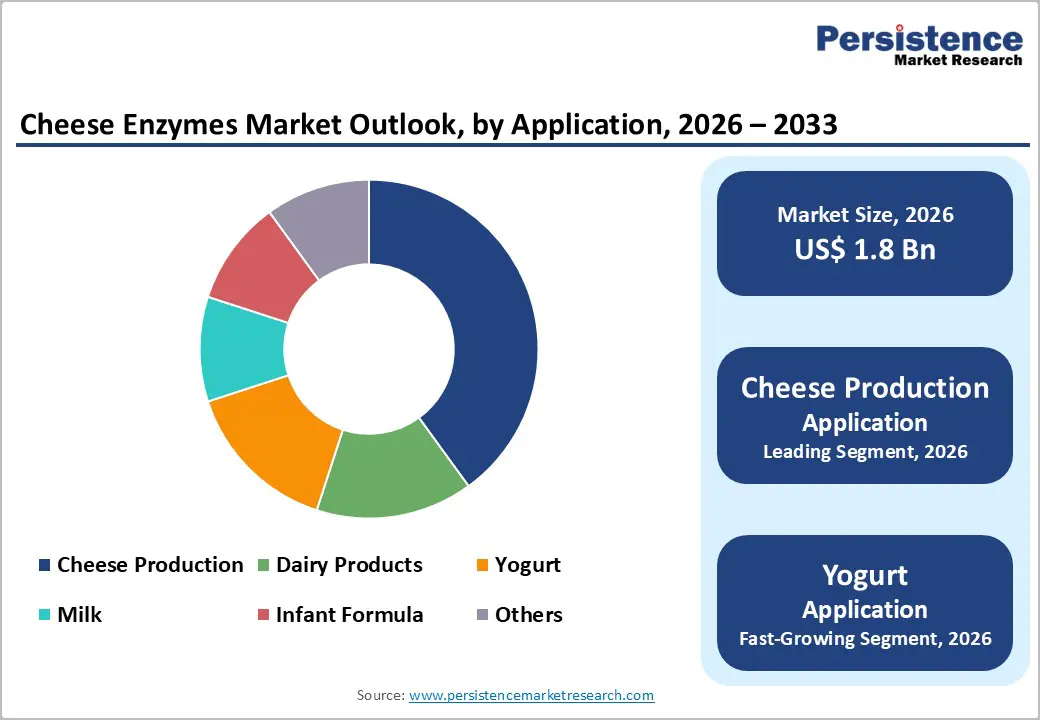

The global cheese enzymes market size is likely to be valued at US$1.8 billion in 2026, and is expected to reach US$3.1 billion by 2033, growing at a CAGR of 8.1% during the forecast period from 2026 to 2033, driven by the increasing prevalence of cheese consumption worldwide, rising demand for consistent texture and flavor in industrial cheese production, and growing adoption of microbial rennet alternatives due to cost, ethical, and halal/kosher considerations.

Rising demand for high-performance cheese enzymes, particularly microbial rennet and lipases, is driving adoption among dairy processors. GMO-free strains and enzyme immobilization technologies enhance yield, reduce bitterness, and support clean-label claims. Growing awareness of their role in texture control, faster maturation, cost efficiency, and vegetarian-friendly cheese options is further fueling market growth, especially in emerging dairy markets.

Key Industry Highlights:

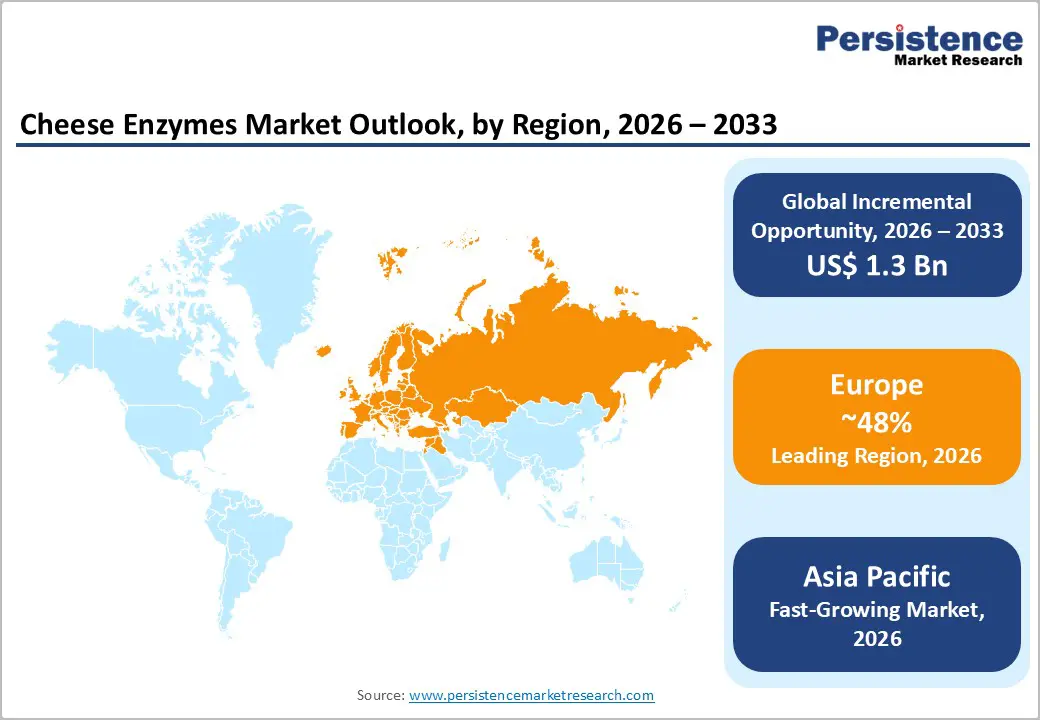

- Leading Region: Europe, anticipated to account for a 48% market share in 2026, driven by strong cheese production heritage, high per-capita consumption, and premium artisanal & industrial demand in Germany, France, Italy, and the Netherlands.

- Fastest-growing Region: Asia Pacific, fueled by a rapid rise in western-style cheese consumption, expanding processed cheese & pizza industry, and growing investments in dairy processing in China and India.

- Leading Enzyme Type: Rennet, to contribute nearly 58% of the market revenue, due to its indispensable role in milk coagulation.

- Leading Application: Cheese production is expected to dominate the market, generating nearly 72% of revenue in 2026, fueled by the extensive use of enzymes in the cheese-making process.

| Key Insights | Details |

|---|---|

| Cheese Enzymes Market Size (2026E) | US$1.8 Bn |

| Market Value Forecast (2033F) | US$3.1 Bn |

| Projected Growth CAGR (2026-2033) | 8.1% |

| Historical Market Growth (2020-2025) | 7.6% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Increasing the Global Cheese Consumption and Industrial Production

The global consumption of cheese has been steadily rising due to changing dietary habits, urbanization, and the growing popularity of Western-style diets in emerging economies. Cheese is increasingly being incorporated into fast food, ready-to-eat meals, and restaurant offerings, which has significantly boosted its demand. Rising awareness of protein-rich diets and calcium intake is encouraging consumers to include cheese as part of their daily nutrition. Urban populations, particularly in Asia and Latin America, are now seeking convenient, processed, and flavored cheese varieties, further driving consumption.

Cheese production is becoming more mechanized and scalable, allowing manufacturers to meet growing demand efficiently. Modern technologies in pasteurization, fermentation, and packaging have improved shelf life and safety, enabling wider distribution both domestically and internationally. Large-scale dairies are investing in automated production lines to optimize yield and reduce production costs. Specialty cheeses, such as mozzarella, cheddar, and processed cheese slices, are seeing high demand from foodservice and retail sectors, pushing industrial production to expand. Increasing trade between countries has facilitated the supply of cheese to regions with previously low domestic production.

Demand for Microbial & Vegetarian-Compatible Enzyme Solutions

The demand for microbial and vegetarian-compatible enzyme solutions is growing rapidly as consumer preferences shift toward ethically produced, allergen-friendly, and sustainable food products. Traditional animal-derived enzymes, commonly used in food processing, for example, in cheese making and baking, are increasingly being replaced by enzymes produced through microbial fermentation. These microbial enzymes are perceived as more consistent in quality and supply, and they avoid ethical concerns related to animal use, aligning with the preferences of vegetarian, vegan, and flexitarian consumers.

In addition to ethical considerations, microbial enzymes often offer technical advantages such as enhanced stability, specificity, and efficiency, making them attractive to food manufacturers looking to improve process yields and product quality. Regulatory acceptance of microbial enzymes in many regions has also facilitated their broader adoption, as producers seek solutions that meet safety and labeling requirements. The trend toward clean-label and plant-based foods further drives the demand for vegetarian-compatible enzymes, as these ingredients support the creation of products that appeal to health-conscious and environmentally aware consumers.

Barrier Analysis – Regulatory Complexity and Regional Approval Delays

Regulatory complexity and regional approval delays are significant challenges for companies developing and launching new products, especially in sectors such as food ingredients, pharmaceuticals, and biotechnology. Each region or country has its own regulatory framework, with distinct requirements for safety testing, manufacturing standards, and labeling. Navigating these varied systems requires companies to prepare multiple, often lengthy dossiers that demonstrate compliance with local laws. This not only increases administrative workload but also demands deep expertise in regulatory science and legal interpretation, raising costs for businesses of all sizes.

Approval timelines can differ substantially from one market to another. For instance, some regulatory bodies operate with fixed review cycles and rapid decisions, while others have less predictable processes, leading to uncertainty for product developers. These discrepancies can delay market entry, slow revenue generation, and disadvantage companies trying to compete internationally. Delays also create logistical challenges: products cleared in one region may be held back in others, complicating supply chain planning and marketing strategies. Further complicating the landscape is the evolving nature of regulations themselves. As new scientific evidence emerges, for example, on ingredient safety or environmental impact, regulators update standards, sometimes requiring additional data or revised testing.

Price Sensitivity in Dairy Markets

Price sensitivity in dairy markets refers to how consumer demand changes in response to price fluctuations of dairy products. Many consumers, especially in price-conscious regions, make purchasing decisions based on the cost of milk, cheese, butter, and other dairy items. When prices rise due to factors such as feed costs, transportation expenses, or supply shortages, some consumers cut back on non-essential dairy purchases or switch to lower-cost alternatives such as plant-based milks or imported products. Conversely, when prices are stable or declining, demand tends to strengthen, encouraging households to buy more or trade up to premium dairy varieties.

This sensitivity is particularly pronounced among low and middle-income consumers for whom dairy staples represent a significant share of food expenditure. Price elasticity in this segment means even modest price changes can lead to noticeable shifts in consumption patterns. Retailers and producers must therefore balance pricing strategies carefully to maintain volume sales without eroding profit margins. Dairy markets are influenced by seasonal supply variations, government subsidies, and international trade tariffs, all of which can affect price levels.

Opportunity Analysis – Expanding the Microbial Fermentation-Derived Rennet and Specialty Enzymes

Expanding the use of microbial fermentation-derived rennet and specialty enzymes reflects a broader shift in how the food industry sources critical processing agents. Traditionally, rennet, the enzyme used to coagulate milk in cheese production, was extracted from the stomach lining of young ruminants, which posed supply limitations, ethical concerns, and variability in activity. Microbial fermentation-derived rennet, produced by cultivating specific fungi, bacteria, or genetically tailored microbes, offers a scalable and more consistent alternative. As global cheese consumption grows and dairy producers seek reliable sources of coagulating agents, fermentation-derived rennet has gained traction because it can be manufactured in controlled conditions, providing steady supply volumes without dependence on animal sources.

Specialty enzymes beyond rennet, such as lipases, proteases, and lactases, are similarly being produced through fermentation. These enzymes perform targeted functions such as flavor development, texture modification, and lactose breakdown, enhancing both traditional and innovative dairy products. Fermentation production allows enzyme properties to be fine-tuned for specific applications, improving efficiency in processing and product outcomes.

Expansion in Plant-Based and Analog Cheese Applications

Expansion in plant-based and analog cheese applications is being driven by changing consumer preferences, innovation in food technology, and growing demand for sustainable, ethical alternatives to traditional dairy. As more people adopt vegetarian, vegan, or flexitarian diets, the cheese market that does not rely on animal milk has expanded beyond niche to mainstream shelves. This includes products made from ingredients such as nuts (especially cashews), soy, coconut oil, oats, and pea protein. These bases are being reformulated to mimic the texture, meltability, and flavor of conventional cheese, which helps widen their appeal among consumers who enjoy dairy but want plant-derived options.

Food technologists are playing a critical role in improving sensory qualities such as stretch in pizzas or creaminess in sauces that were once challenging for plant-based cheeses. Advances in fermentation, texturizing agents, and blending of plant proteins have elevated the performance of analog cheeses, making them suitable for both home cooking and foodservice use. Brands are increasingly targeting specific use applications such as shreds for topping, slices for sandwiches, and spreads for snacks, broadening consumer choice.

Category-wise Analysis

Enzyme Type Insights

Rennet is expected to dominate the market, contributing nearly 58% of revenue in 2026, fueled by its essential role in coagulating milk during cheese production. Its widespread use across traditional and industrial cheese varieties, including cheddar, mozzarella, and specialty cheeses, ensures steady demand. The shift toward microbial and fermentation-derived rennet has further strengthened market growth by offering consistent quality, vegetarian-friendly alternatives, and scalable production. Increasing global cheese consumption, coupled with expanding dairy processing infrastructure, is supporting rennet’s dominant position. Chy-Max® is a brand of genetically modified (GMO) rennet used in cheese production. It is produced using recombinant DNA technology, which involves transferring the gene responsible for producing the enzyme chymosin from animal cells into microbial cells, such as yeast or fungi.

Lipases represent the fastest-growing enzyme type, as they deliver unique functional benefits that producers increasingly value. These enzymes catalyze the breakdown of fats into free fatty acids, which significantly enhance flavor, aroma, and texture, especially in specialty and aged cheeses where nuanced profiles are important. Their ability to modify milk fats accelerates cheese ripening and enriches sensory qualities that consumers seek in premium products. Lipases are also used across other food segments such as bakery and confectionery to improve dough properties, extend freshness, and replace synthetic additives, aligning with demand for natural ingredients. Chr.Hansen A/S is a major dairy enzyme producer. The company offers SpiceIT MPlus, a microbial lipase developed specifically to enhance cheese flavor during ripening, helping producers intensify taste in varieties such as provolone without using animal-derived enzymes.

Application Insights

Cheese production is projected to lead the market, accounting for nearly 72% of revenue in 2026, driven by the widespread use of enzymes in the cheese-making process. Cheese requires multiple enzymatic processes, including milk coagulation, flavor development, and texture modification, making it one of the most enzyme-intensive dairy products. Rising global consumption of processed, specialty, and convenience cheese products is strengthening production volumes across both industrial and artisanal sectors. Leprino Foods Company is one of the world’s largest cheese manufacturers. Leprino Foods produces massive volumes of mozzarella, cheddar, and other cheeses used by major pizza chains and foodservice brands globally. Their scale supplying cheese to over 85% of the U.S. pizza market underscores how cheese processing dominates dairy enzyme and milk coagulation applications that generate the bulk of industry revenue.

Yogurt represents the fastest-growing application, driven by shifting consumer preferences toward healthy, protein-rich, and gut-friendly foods. Unlike many other dairy products, yogurt benefits from both traditional fermentation and innovations such as drinkable, Greek, plant-based, and probiotic-fortified variants, attracting a broad range of consumers from health enthusiasts to busy urban shoppers. Its versatility as a breakfast item, snack, or ingredient in smoothies and desserts expands its everyday use. Chobani LLC is a leading yogurt producer that has significantly expanded its market reach. Chobani’s Greek yogurt, high in protein and aligned with health-focused consumer trends, grew from a tiny share of the U.S. yogurt market to over 20% market share, making it one of the top-selling yogurt brands in the country.

Regional Insights

North America Cheese Enzymes Market Trends

North America is witnessing stable growth owing to the region’s advanced dairy processing, strong research and development capabilities, and high public awareness of clean-label and vegetarian-compatible enzymes. Production systems in the U.S. and Canada provide extensive support for cheese enzyme programs, ensuring wide accessibility across microorganism-based, rennet, and cheese production populations. Increasing demand for high-performance, convenient, and easy-to-integrate forms is further accelerating adoption, as these formats improve yield and reduce barriers associated with animal rennet.

Innovation in cheese enzymes technology, including stable microbial, improved lipase delivery, and targeted vegan enhancement, is attracting significant investments from both public and private sectors. Government initiatives and FDA/USDA campaigns continue to promote use against, creating sustained market demand. The growing focus on yogurt grades and specialty uses, particularly for cheese production and others, is expanding the target applications for cheese enzymes.

Europe Cheese Enzymes Market Trends

Europe is projected to lead with a market share of 48% in 2026, supported by increasing awareness of traditional and clean-label cheese benefits, strong regulatory systems, and government-led dairy heritage programs. Countries such as Germany, France, Italy, and the Netherlands have well-established cheese production frameworks that support routine cheese enzymes use and encourage adoption of innovative enzyme delivery methods, including microbial and vegetarian-compatible solutions. These high-quality formulations are particularly appealing for cheese production populations, regulation-conscious processors, and yogurt users, improving yield and coverage rates.

Technological advancements in cheese enzyme development, such as enhanced fermentation, application-targeted delivery, and improved lipase grades, are further boosting market potential. European authorities are increasingly supporting research and trials for enzymes against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, ethical options is aligned with the region’s focus on preventive, GMO-free, and vegetarian demand. Public awareness campaigns and promotion drives are expanding reach in both industrial and artisanal segments, while suppliers are investing in production and novel variants to increase efficacy.

Asia Pacific Cheese Enzymes Market Trends

Asia Pacific is likely to be the fastest-growing market for cheese enzymes in 2026, driven by rising Western food consumption awareness, increasing government initiatives, and expanding application programs across the region. Countries such as China, India, Japan, and South Korea are actively promoting enzyme campaigns to address cheese growth and emerging processed dairy needs. Cheese enzymes are particularly attractive in these regions due to their cost-effective administration, ease of integration, and suitability for large-scale cheese production and yogurt drives in both urban and rural populations.

Technological advancements are supporting the development of stable, effective, and easy-to-deploy cheese enzymes, which can withstand challenging processing conditions and minimize flavor dependence. These innovations are critical for reaching domestic dairy processors and improving overall product coverage. Growing demand for microorganism-based, rennet, and cheese production applications is contributing to market expansion. Public-private partnerships, increased dairy expenditure, and rising investment in enzyme research and production capacity are further accelerating growth. The convenience of enzyme delivery, combined with improved yield and reduced risk of inconsistency, positions it as a preferred choice.

Competitive Landscape

The global cheese enzymes market features competition between established enzyme specialists and emerging microbial-focused suppliers. In North America and Europe, Chr. Hansen and Novozymes lead through strong R&D, distribution networks, and dairy-processor ties, bolstered by innovative microbial rennet and lipase programs. In Asia Pacific, local players advance with cost-competitive solutions, enhancing accessibility. Microbial delivery boosts consistency, cuts ethical risks, and enables mass integrations across cheese lines. Strategic partnerships, collaborations, and acquisitions merge expertise, expand portfolios, and speed commercialization. Vegetarian formulations solve ethical issues, aiding penetration in clean-label segments.

Key Industry Developments:

- In March 2025, DSM-Firmenich unveiled MaxirenEVO, a next-generation coagulant enzyme designed to improve cheese texture, flavor, and processing flexibility. Using advanced fermentation, it precisely targeted αs1-casein, enabling faster curd knitting, better moisture distribution, enhanced emulsification, and improved shelf-life stability.

- In October 2024, Chobani launched the Chobani® High Protein line, featuring Greek yogurt cups and drinkable options. Made with natural ingredients, real fruit, and 0 g added sugar, the range addressed rising demand for convenient, protein-rich dairy products.

Companies Covered in Cheese Enzymes Market

- DSM Nutritional Products

- Dow

- DuPont Inc.

- Chr. Hansen A/S

- Advanced Enzyme Technologies

- Novozymes

- Biocatalysts Limited

- SternEnzym GmbH & Company KG

- Amano Enzyme Inc.

Frequently Asked Questions

The global cheese enzymes market is projected to reach US$1.8 billion in 2026.

Increasing demand for processed, specialty, and convenience cheeses across retail and foodservice sectors is driving the need for efficient, high-performance coagulant enzymes that improve yield, texture, and consistency.

The cheese enzymes market is poised to witness a CAGR of 8.1% from 2026 to 2033.

Growing investments in large-scale dairy processing and rising demand for premium, region-specific, and functional cheeses create opportunities for advanced enzyme solutions that enhance flavor, texture, and processing efficiency.

Chr. Hansen A/S, Novozymes, DSM Nutritional Products, Biocatalysts Limited, and Amano Enzyme Inc. are the key players.