- Biotechnology

- CAR T-Cell Therapy Market

CAR T-Cell Therapy Market Size, Share, and Growth Forecast, 2025 - 2032

CAR T-Cell Therapy Market By Drug Type (Yescarta, Kymriah, Breyanzi, Abecma, Carvykti, Tecartus, Others), Target Antigen (CD19, BCMA, CD22, CD33, HER2, HER1, Others), Disease Indication (Lymphoma, Leukemia, Multiple Myeloma, Others), and Regional Analysis for 2025 - 2032

CAR T-Cell Therapy Market Share and Trends Analysis

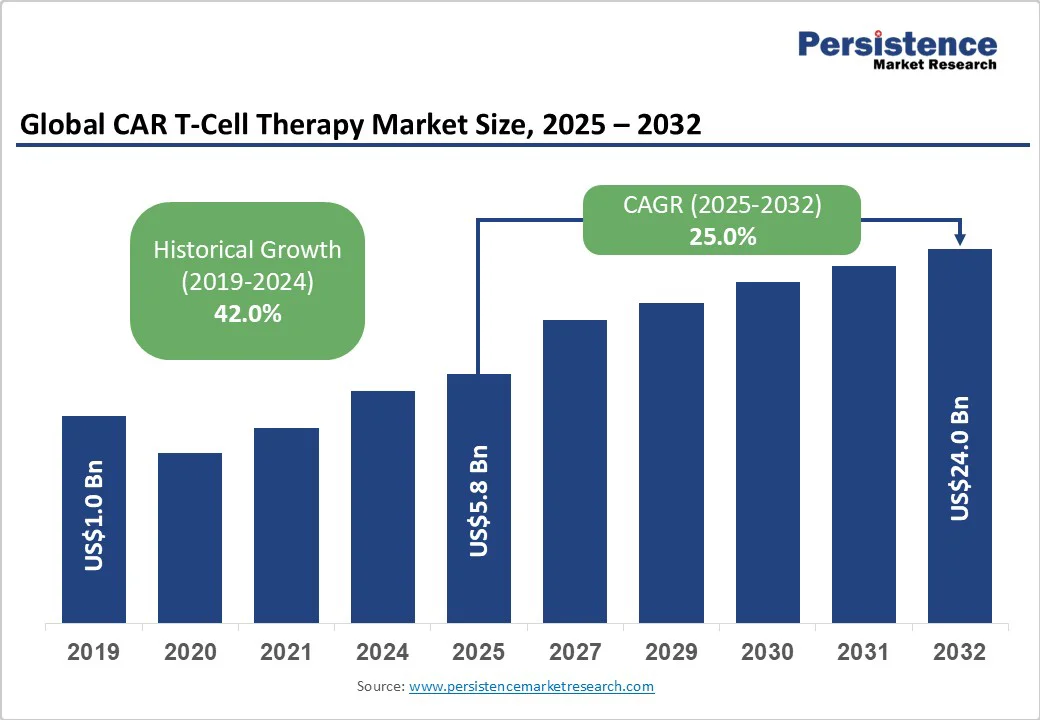

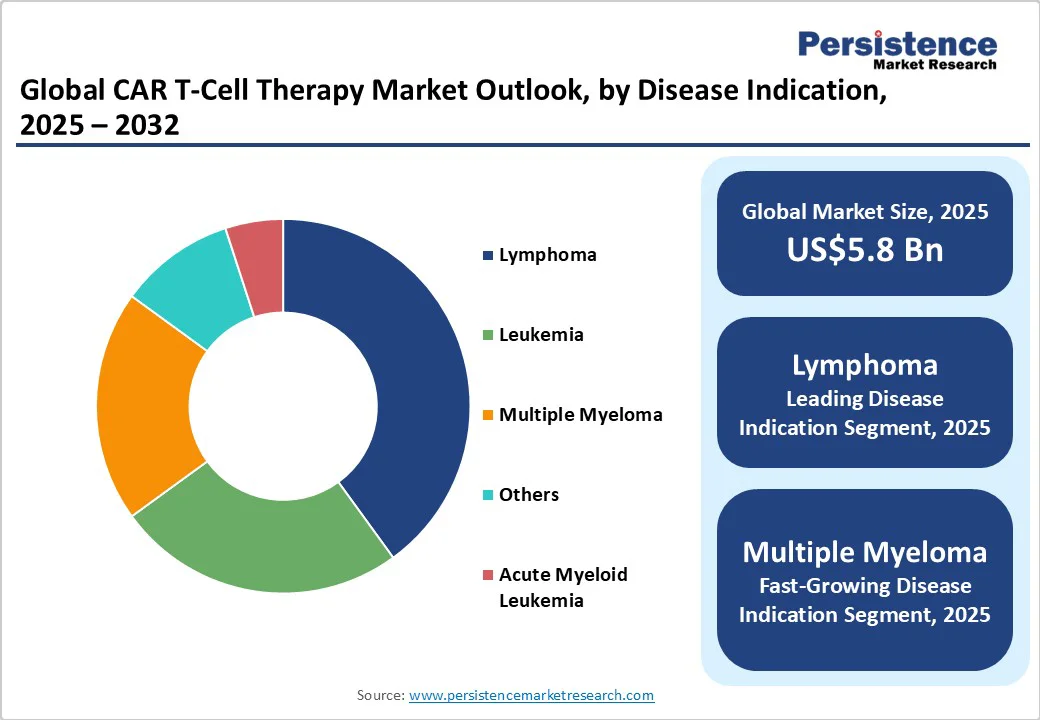

The global CAR T-cell therapy market size is likely to be valued at US$5.8 Billion in 2025, and is estimated to reach US$24 Billion by 2032, growing at a CAGR of 25% during the forecast period 2025−2032, driven by the increasing prevalence of hematological malignancies and expanding indications in oncology.

Advances in gene-editing technologies, supportive regulatory frameworks, and rising healthcare investments are enabling broader clinical access and expedited product development. These factors have created a robust growth environment underscored by increasing clinical approvals and expanding patient populations requiring personalized immunotherapies.

Key Industry Highlights

- Leading & Fastest-growing Disease Indications: Lymphoma is expected to constitute the largest market share of about 40%, with multiple myeloma emerging as the fastest-growing segment at an from 2025 to 2032.

- Leading & Fastest-growing Drug Types: Yescarta is set to lead with an estimated market share of approximately 35% in 2025, owing to early regulatory approvals across the U.S. and Europe, while Abecma is expected to exhibit the highest CAGR through 2032.

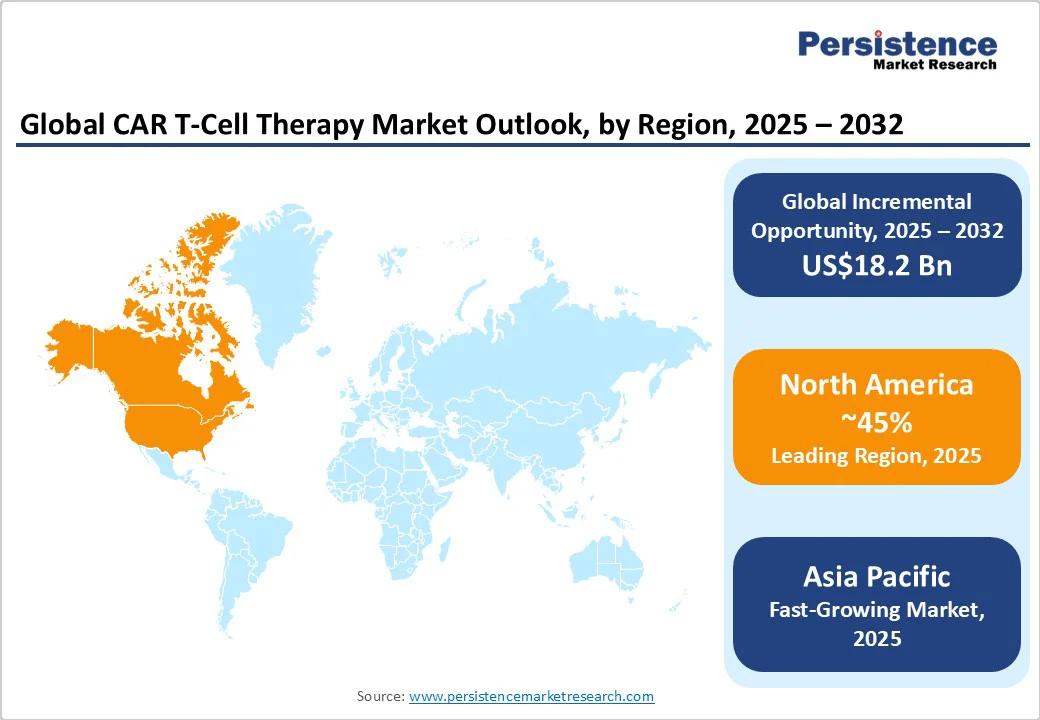

- Dominant Region: North America will dominate with an approximate 45% share in 2025, supported by the U.S. innovation ecosystem and regulatory framework.

- Fastest-growing Regional Market: Asia Pacific is likely to be the fastest-growing regional market, propelled by expanding healthcare infrastructure and regulatory modernization.

- May 2025: The University of Pennsylvania developed an enhanced CAR T-cell therapy, engineered to improve T-cell persistence and tumor-targeting capabilities, addressing challenges such as relapse and incomplete responses.

| Key Insights | Details |

|---|---|

|

CAR T-Cell Therapy Market Size (2025E) |

US$5.8 Bn |

|

Market Value Forecast (2032F) |

US$24 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

25% |

|

Historical Market Growth (CAGR 2019 to 2024) |

42% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Widening Prevalence of Hematologic Malignancies

Globally, cancer prevalence is rising, particularly hematologic malignancies such as non-Hodgkin lymphoma (NHL), acute lymphoblastic leukemia, and multiple myeloma, key targets for CAR T-cell therapies. In 2022, the International Agency for Research on Cancer reported 553,389 NHL cases worldwide, with a mortality rate of about 50%, reflecting a growing patient population in need of advanced oncological treatments. The American Cancer Society estimates over 80,000 new lymphoma diagnoses annually in the U.S., further driving demand for innovative therapies. This increasing disease burden, alongside the limited effectiveness of conventional treatments, is accelerating clinical adoption and commercial growth of CAR T-cell therapies.

Advancements in CAR T-cell technology, such as novel antigen targeting, integrated safety switches, and improved manufacturing processes, are boosting efficacy and safety, enhancing clinician confidence and patient access. Emerging innovations, including gene-editing tools such as CRISPR and the development of allogeneic (off-the-shelf) CAR T-cell products, promise to reduce production time and costs, enabling broader scalability. Regulatory bodies such as the U.S. FDA and European Medicines Agency have established accelerated approval pathways, signaling strong confidence in these therapies. This regulatory support, combined with technological progress, is fostering pipeline diversification and investment, positioning CAR T-cell therapy as a transformative approach in oncology.

Exorbitant Treatment Costs Slowing Patient Acceptance

The CAR T-cell therapy market faces significant challenges due to its high treatment costs, often exceeding US$400,000 per patient, creating substantial reimbursement and access barriers worldwide. Many healthcare systems, especially in emerging markets, lack adequate reimbursement frameworks to cover the extensive expenses of therapy production, administration, and post-treatment care. A National Health Service (U.K.) study highlights growing scrutiny of cost-effectiveness thresholds for innovative treatments, placing economic pressure on CAR T-cell therapies. These financial constraints limit widespread adoption, particularly in lower-income regions, restricting market penetration and slowing revenue growth. To address this, companies and policymakers are exploring innovative payment models, such as outcomes-based reimbursement, to reduce financial risks and improve accessibility.

Additionally, CAR T-cell therapies involve highly specialized, autologous manufacturing processes that require patient-specific cell harvesting, engineering, and reinfusion. This complexity, combined with limited manufacturing sites, specialized logistics, and strict quality controls, creates bottlenecks in timely delivery. COVID-19 disruptions exposed supply chain vulnerabilities, increasing delays and operational costs. Many manufacturers report capacity and scalability issues, impacting their ability to meet growing global demand. These supply constraints result in shortages and longer patient wait times, thereby creating commercial challenges.

Development of Cutting-Edge CAR T-Cell Therapies

The embedding of artificial intelligence (AI), machine learning (ML), and advanced biomarker discovery into CAR T-cell development is opening new frontiers to improve therapy personalization, efficacy, and safety. Predictive analytics are helping identify optimal patient candidates and anticipate adverse events, thereby improving clinical outcomes and reducing costs. Furthermore, evolving gene-editing platforms are facilitating the engineering of CAR T-cells with dual targeting capabilities and reduced immunogenicity. These advancements could substantially increase the addressable patient population by enabling therapy use in solid tumors and resistant cancer forms, potentially adding multiple billion dollars to the market by 2032. Industry collaboration with biotech startups and academic institutions focused on these convergent technologies is pivotal to capturing this emerging high-growth segment.

Capitalizing on unmet oncological needs of an expanding patient pool in the emerging economies of Asia Pacific, Latin America, and the Middle East is a high-value business avenue for market players. For instance, projections from the IARC show that there will be around 5.1 million cancer cases in China and 1.5 million in India in 2025. These, along with other developing economies of the region, are witnessing rising governmental healthcare expenditures. Enhancing regulatory frameworks and increasing local reimbursement coverage in these regions are facilitating clinical trial approvals and therapy accessibility, producing unprecedented opportunities in the years to come.

Category-wise Analysis

Drug Type Insights

Currently, in 2025, Yescarta, marketed by Gilead Sciences via its Kite Pharma subsidiary, is the leading drug type segment in the market, capturing an estimated market share of approximately 35%. This leadership position is underpinned by Yescarta's early regulatory approvals across the U.S. and Europe, alongside robust clinical efficacy in treating relapsed or refractory large B-cell lymphoma and other hematologic malignancies. Its commercial success is further supported by a well-established distribution network, payer reimbursement acceptance, and ongoing label expansions. Yescarta’s strong presence in key oncology treatment centers globally has made it a preferred option for clinicians and patients requiring targeted immunotherapy, thereby driving significant revenue generation.

The highest CAGR is likely to be registered by Abecma, being the first FDA-approved CAR T-cell therapy targeting multiple myeloma, a rapidly growing oncology indication with increasing incidence globally. Abecma's robust clinical data demonstrating significant efficacy and an expanding label for multiple myeloma treatment in both the U.S. and international markets are key growth drivers. The rising prevalence of multiple myeloma, especially in aging populations, along with ongoing clinical trials for Abecma’s use in earlier disease stages and combinations with other therapies, contributes to this rapid uptake. Regulatory advances and increased reimbursement support have further accelerated Abecma's adoption.

Target Antigen Insights

CD19-targeted CAR T-cell therapies will continue to dominate the market with an estimated 2025 revenue share of approximately 55%, principally due to their efficacy in treating B-cell malignancies such as non-Hodgkin lymphoma and acute lymphoblastic leukemia. These therapies benefit from robust and extensive clinical data supporting durable remission rates in relapsed or refractory cases where conventional treatments often fail, reinforcing broad regulatory approvals across multiple geographies. The established safety profile and expanding indication labels further solidify their clinical adoption. Moreover, CD19 therapies have been integrated into many oncology treatment guidelines, enabling widespread clinical use in specialized cancer centers.

The BCMA (B-cell maturation antigen)-targeted CAR T-cell therapy segment is poised as the fastest-growing, driven by the rising global incidence of multiple myeloma, a disease primarily affecting plasma cells that exhibit high BCMA expression, making it an optimal target for CAR T-cell immunotherapies. BCMA-targeted therapies such as Abecma (idecabtagene vicleucel) and Carvykti (ciltacabtagene autoleucel) have demonstrated compelling clinical efficacy, characterized by high response rates and durable remissions in relapsed or refractory multiple myeloma patients. Regulatory approvals granted by the FDA and EMA have further catalyzed adoption, encouraging rapid market penetration.

Disease Indication

Lymphoma is predicted to hold the largest revenue share at an estimated 40% in 2025. The dominance of the segment is sustained by its high global prevalence and the well-established efficacy of CAR T therapies targeting aggressive and relapsed/refractory forms such as diffuse large B-cell lymphoma (DLBCL). The durable remission rates demonstrated in pivotal trials and inclusion in global treatment guidelines reinforce widespread clinical adoption. Factors such as increasing incidence of lymphoma subtypes, improved diagnostic capabilities, and expanded healthcare coverage in key markets are bolstering demand.

Multiple myeloma is the fastest expanding indication, driven by rising disease incidence, particularly in aging populations, with the U.S. estimating over 36,000 new cases in 2025 alone and a global market for multiple myeloma treatments projected to reach nearly US$42 Billion by 2032. Enhanced survival rates due to novel therapeutics, including CAR T-cell and bispecific antibodies, are transforming multiple myeloma into a more chronic condition, increasing patient pools eligible for advanced therapies. Ongoing approvals and clinical trials targeting earlier treatment lines and combinational regimens are expanding therapeutic applications.

Regional Insights

North America CAR T-Cell Therapy Market Trends

North America is projected to hold an approximate 45% market share in 2025, driven predominantly by the U.S., which commands high healthcare expenditure and an established advanced therapy ecosystem. The regional market benefits from a well-developed innovation landscape with numerous biotechnology hubs, strong venture capital funding, and a comprehensive regulatory framework provided by the FDA that supports accelerated approvals for novel therapies. Key factors fueling market growth include high disease awareness, early adoption of CAR T-cell therapies, and favorable reimbursement policies for cancer treatments.

Competitive intensity is marked by several major biopharma companies headquartered in the U.S., leveraging technological advances to expand product portfolios and enter new therapeutic indications. Investment trends spotlight increasing government and private sector funding for cell and gene therapy manufacturing facilities and R&D centers, enabling scalable production and clinical pipeline expansion. Regulatory evolution, facilitating breakthrough therapy designations and expanded access programs, further enhances patient uptake and market penetration.

Europe CAR T-Cell Therapy Market Trends

Europe is expected to capture approximately 30% of the global market by 2025, with Germany, the U.K., France, and Spain being the key contributors. Regulatory harmonization under the EMA, alongside initiatives such as the European Advanced Therapy Medicinal Products (ATMPs) framework, is facilitating streamlined clinical trials and market entry.

The regional market is accelerating due to increasing oncology incidence, government-backed healthcare financing reforms, and growing clinical infrastructure dedicated to cell therapies. Germany leads in investment with strong reimbursement policies for CAR T-cell therapies, supporting adoption. Market growth is further propelled by expanding clinical trial activities and collaborations between academia and industry to advance therapy development. However, varying national regulatory processes and reimbursement landscapes require tailored market access strategies.

Asia Pacific CAR T-Cell Therapy Market Trends

Asia Pacific is anticipated to emerge as the fastest-growing regional market. Key growth markets include China, Japan, India, and the ASEAN countries, where rising cancer prevalence, expanding healthcare infrastructure, and increasing government healthcare spending are driving demand. Regulatory agencies in China and Japan are adapting more flexible approval processes to accelerate access to innovative therapies.

Manufacturing advantages, including lower labor and production costs combined with growing biopharmaceutical investments, are attracting global and local companies to expand their presence. Strategic partnerships are enhancing clinical research capabilities, and domestic players are emerging with pipeline candidates tailored for regional patient populations. Even though variable reimbursement systems and market access challenges necessitate adaptive pricing models, the large patient populations and improving infrastructure of the region underscore its strategic importance for business expansion.

Competitive Landscape

The global CAR T-cell therapy market structure is moderately consolidated, with leading companies collectively holding an estimated 70% market share as of 2025. Dominant players include Gilead Sciences (via Kite Pharma), Novartis AG, and Bristol-Myers Squibb, each leveraging established CAR T-cell products and diversified pipelines.

Market positioning is characterized by differentiation through product portfolios, strategic partnerships, and geographical presence. Smaller biotechs and emerging firms contribute innovation but have limited commercial scale. Continued consolidation through mergers and acquisitions is anticipated as companies seek technological synergies and expanded market footprints.

Key Industry Developments

- In October 2025, the ZUMA-24 study showed that outpatient Yescarta treatment for DLBCL is safe and feasible, reducing hospital stays through early toxicity management and corticosteroids, with efficacy maintained, low-grade side effects, and improved quality of life at three to six months.

- In June 2025, Kite reported CIBMTR registry data showing outpatient Yescarta administration for R/R LBCL matched inpatient safety and effectiveness. Comparable cytokine release and neurologic event rates were observed, with many outpatient patients avoiding hospital admission within 30 days post-infusion.

- In March 2025, Cellogen Therapeutics launched the first indigenously developed Bi-Specific 3rd Gen CAR T-cell therapy in India, targeting dual antigens to boost efficacy and cut resistance, while reducing treatment costs by over 90% through local production and partnerships.

Companies Covered in CAR T-Cell Therapy Market

- Gilead Sciences, Inc.

- Novartis AG

- Bristol-Myers Squibb Company

- Legend Biotech Corporation

- Cellectis S.A.

- Autolus Therapeutics Plc

- Adaptimmune Therapeutics plc

- Mustang Bio, Inc.

- Bellicum Pharmaceuticals, Inc.

- MaxCyte, Inc.

- Tessa Therapeutics

- Caribou Biosciences, Inc.

- Takeda Pharmaceutical Company Limited

- Sorrento Therapeutics, Inc.

- Poseida Therapeutics, Inc.

Frequently Asked Questions

The CAR T-cell therapy market is projected to reach US$5.8 Billion in 2025.

The increasing prevalence of hematological malignancies, such as lymphoma, and expanding indications in oncology are driving the market.

The CAR T-cell therapy market is poised to witness a CAGR of 25% from 2025 to 2032.

Advances in gene-editing technologies, supportive regulatory frameworks, and the rise in clinical approvals for novel cancer therapies are key market opportunities.

Gilead Sciences, Inc., Novartis AG, and Bristol-Myers Squibb Company are some of the key players in the CAR T-cell therapy market.