- Hardware & Software IT Services

- Business Process Management Market

Business Process Management Market Size, Share, and Growth Forecast, 2026 - 2033

Business Process Management Market by Component Type (Software, Services), Deployment Mode (On-Premises, Cloud-Based), Organization Size (Large Enterprises, Small & Medium Enterprises (SMEs)), Industry (Banking, Financial Services & Insurance (BFSI), IT & Telecommunications, Healthcare & Life Sciences, Manufacturing, Others), and Regional Analysis for 2026 - 2033

Business Process Management Market Size and Trends Analysis

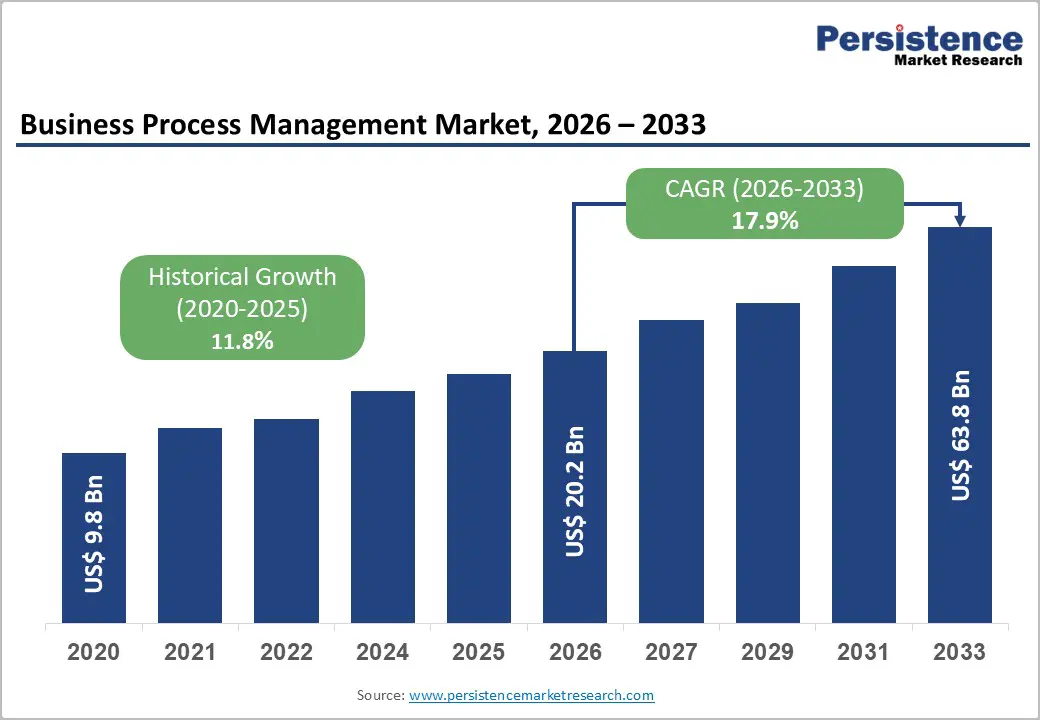

The global business process management market size is likely to be valued at US$ 20.2 billion in 2026 and is projected to reach US$ 63.8 billion by 2033, growing at a CAGR of 17.9% between 2026 and 2033. This substantial expansion reflects the accelerating convergence of artificial intelligence, cloud infrastructure, and enterprise automation technologies, which are reshaping organisational operations. The market's trajectory demonstrates structural shifts across all major industries, with automation of mission-critical processes, regulatory compliance automation, and integration of AI-powered decision-making serving as primary catalysts.

Enterprise spending on process optimization reached record levels, with 59% of C-suite executives committing increased capital allocation toward intelligent automation initiatives. The market's heterogeneous growth across segments and regions, ranging from mature digital economies in North America to rapidly digitizing sectors in Asia-Pacific, underscores the universal imperative for operational modernization and efficiency gains in an increasingly complex business environment.

Key Industry Highlights:

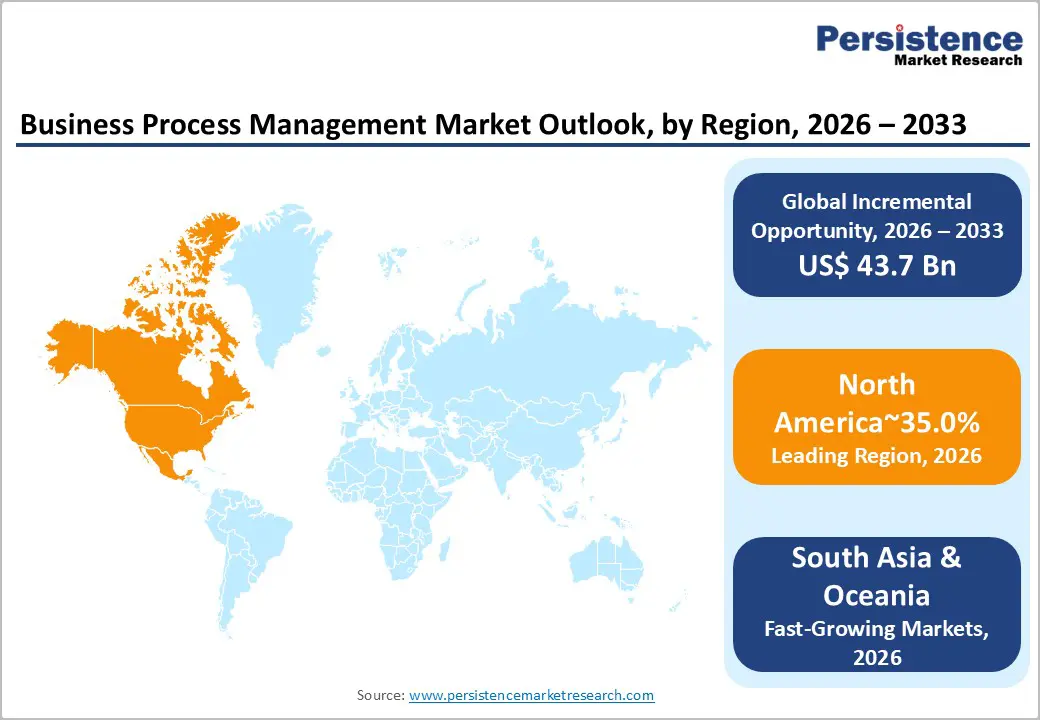

- Regional Leadership: North America dominates the global Business Process Management Market with ~35% share, supported by mature enterprise digital transformation, high cloud BPM adoption, and strong presence of leading vendors such as IBM, Oracle, Appian, and Pegasystems.

- High-Growth Region: East Asia holds ~20% share and represents the fastest-growing regional market, fueled by rapid digital transformation in banking and manufacturing, expanding cloud adoption, and government-led digitalization initiatives across China and Southeast Asia.

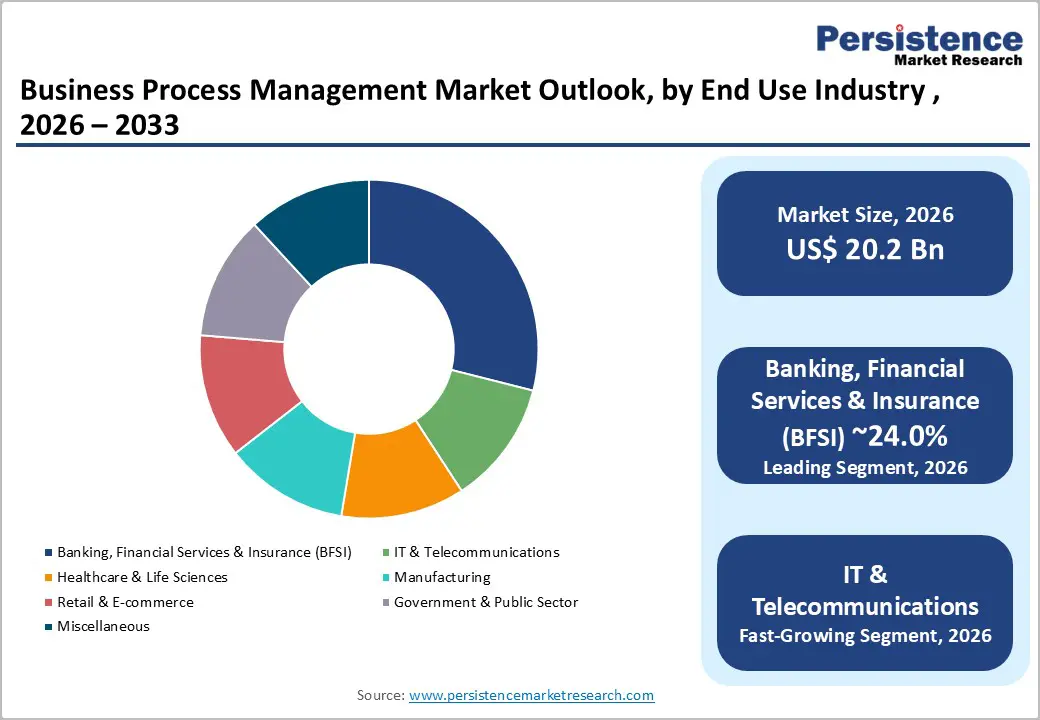

- Leading End-user: BFSI leads the BPM market with ~24% share in 2026, underpinned by high transaction volumes, complex regulatory compliance requirements, and widespread adoption of BPM for KYC, AML, fraud detection, and risk management automation.

- Dominant Component Segment: BPM solutions capture ~68% market share, reflecting enterprise preference for integrated, AI-enabled platforms offering end-to-end workflow automation, orchestration, and analytics.

| Key Insights | Details |

|---|---|

|

Business Process Management Market Size (2026E) |

US$ 20.2 Bn |

|

Market Value Forecast (2033F) |

US$ 63.8 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

17.9% |

|

Historical Market Growth (CAGR 2020 to 2025) |

11.8% |

Market Dynamics

Drivers - Digital Transformation Imperative and Enterprise Operational Modernization

Digital transformation has evolved from a competitive advantage to an existential business requirement, with 53% of organizations deploying Business Process Management solutions as the foundational infrastructure for this transition. The Business Process Management Market experiences demand acceleration from organizations seeking to replace legacy, siloed systems with integrated, end-to-end process ecosystems.

Post-pandemic organizational structures have normalised remote and hybrid work models, necessitating robust process visibility and orchestration capabilities that traditional infrastructure cannot provide. Enterprise systems are increasingly requiring real-time data integration, automated decision-making workflows, and seamless cross-departmental collaboration capabilities that are native to modern BPM platforms.

The shift from product-centric to process-centric organizational thinking has fundamentally reshaped capital allocation patterns. Enterprises allocating budget toward BPM implementation report operational efficiency improvements of approximately 38%, translating to measurable cost reductions and enhanced competitive positioning. This transformation extends across industries, with banking, financial services, and insurance sectors leading initial adoption due to stringent regulatory requirements and high transaction volumes.

Integration of Artificial Intelligence and Intelligent Automation in BPM Platforms

The integration of generative AI and machine learning within Business Process Management platforms represents the most significant technological inflexion point in the sector's evolution. AI-driven orchestration capabilities enable BPM systems to transition from prescriptive, rule-based automation to adaptive, learning-based systems that optimize workflows in real-time based on contextual data and historical performance patterns.

The market is witnessing convergence between robotic process automation (RPA), process mining, advanced analytics, and artificial intelligence creating hyper-automation ecosystems that address end-to-end process complexity. Organizations implementing AI-augmented BPM solutions report 60-70% reduction in processing times for mission-critical workflows such as KYC verification and loan origination, alongside 45% operational cost reductions.

The BPM market is experiencing accelerated adoption of agentic automation where AI agents autonomously execute complex multi-step processes with minimal human intervention. Technology leaders, including IBM, Oracle, and Blue Prism, have announced enterprise-grade AI integration capabilities, positioning intelligent orchestration as the industry standard. Predictive analytics embedded within BPM platforms enable proactive risk identification, compliance violation prevention, and process bottleneck detection before operational impact occurs.

Regulatory Compliance Complexity and Risk Management Requirements

Regulatory environments have become progressively more demanding, with organizations operating across multiple jurisdictions facing overlapping compliance frameworks spanning data privacy (GDPR, CCPA), financial services (Basel III, Dodd-Frank), healthcare (HIPAA), and industry-specific standards.

The BPM market's growth is substantially driven by the critical compliance requirements across regulated industries, particularly in the BFSI sectors, where non-compliance penalties reach millions of dollars. BPM solutions enforce regulatory adherence through standardised, auditable workflows that generate real-time compliance alerts, maintain comprehensive audit trails, and enable rapid adaptation to regulatory changes. Financial institutions leverage BPM platforms to automate complex workflows, including Know-Your-Customer (KYC) verification, Anti-Money Laundering (AML) screening, fraud detection, and regulatory reporting processes where compliance failures carry existential financial consequences.

The BFSI sector's operational complexity, characterised by high-volume transaction processing, stringent regulatory oversight, and critical risk management requirements, has established this vertical as the largest Business Process Management Market segment at 24% market share in 2026. Manufacturing and healthcare sectors similarly drive BPM adoption through compliance automation, supply chain traceability requirements, and quality management standardization needs.

Restraint - Implementation Complexity and Total Cost of Ownership Barriers

Despite compelling efficiency gains, BPM implementation projects exhibit significant complexity and capital intensity that constrain adoption, particularly among resource-constrained organizations. Integration with legacy enterprise systems including mainframe-based banking platforms, bespoke manufacturing execution systems, and historically isolated departmental systems requires substantial custom development, extended testing cycles, and substantial data migration efforts that increase project timelines and costs. Organizations implementing comprehensive BPM initiatives report implementation expenditures ranging from hundreds of thousands to tens of millions of dollars, depending on process scope and system complexity.

The hidden costs associated with organizational change management, employee retraining, process re-engineering, and system maintenance create ongoing expense burdens that extend well beyond initial platform deployment. The Market's restraints include the scarcity of specialised implementation expertise, with qualified BPM architects and process optimization consultants commanding premium compensation and remaining in constrained supply.

Small and medium-sized enterprises, despite representing the highest-growth segment, face disproportionate implementation burden due to limited internal IT resources and the inability to absorb extended project timelines.

Opportunity - Expansion of 5G Private Networks and Enterprise IoT Deployments

The convergence of advanced AI capabilities and Business Process Management platforms is creating unprecedented opportunities for process intelligence that transcends traditional rule-based automation. Generative AI applications within BPM enable intelligent document processing, natural language extraction from unstructured business communications, predictive workflow routing based on contextual factors, and exception handling that adapts dynamically to changing conditions.

Organizations are deploying AI agents that autonomously manage end-to-end processes spanning finance from procure-to-pay through order-to-cash cycles, supply chain from demand forecasting through inventory optimization, and customer operations from inquiry management through dispute resolution.

The integration of process mining with AI analytics within Business Process Management platforms enables organizations to identify optimization opportunities at granular levels discovering hidden process variants, bottleneck patterns, and automation-suitable subprocesses that manual process analysis cannot detect. Vendors including TIBCO, Infosys, and Newgen are launching AI-first BPM platforms that embed autonomous agents, enabling organizations to automate complex, multi-step processes without extensive manual workflow configuration. The financial impact is substantial, with organizations projecting 30-50% cost reduction through AI-augmented process automation and measurable quality improvements through error elimination.

Low-Code and No-Code BPM Platform Democratization and Citizen Developer Adoption

The low-code/no-code movement represents a fundamental transformation in BPM accessibility, enabling business users and citizen developers to design, deploy, and modify workflows without requiring specialized programming expertise. This opportunity within the Business Process Management Market is accelerating adoption among small and medium-sized enterprises that lack large IT departments but face identical process optimization requirements as enterprise organizations.

Platform vendors, including Kissflow, Newgen, and Red Hat, are building intuitive drag-and-drop interfaces, pre-built workflow templates, and visual process designers that lower technical barriers to BPM adoption. Industry analysis indicates that organisations implementing low-code BPM solutions achieve 50-60% faster deployment timelines and 40% lower implementation costs compared to traditional code-heavy approaches. Business users gain authority to modify processes rapidly in response to changing market conditions, regulatory requirements, or operational constraints without IT bottleneck constraints that historically delayed process improvements.

Category-wise Analysis

Component Type Insights

The Solutions component represents the dominant Business Process Management Market segment, capturing 68% of market share in 2026, reflecting enterprise preference for comprehensive platform functionality, vendor support, and integrated technology ecosystems. BPM solutions encompass software platforms, cloud-based systems, and integrated suites that provide workflow automation, process modelling, analytics, and orchestration capabilities. Enterprise solutions including offerings from Oracle Fusion Cloud, SAP S/4HANA process modules, and specialised BPM platforms bundle extensive functionality addressing diverse process requirements across finance, supply chain, human resources, and customer operations domains.

The solutions segment benefits from enterprise attachment dynamics, where customers implementing comprehensive systems require supporting BPM capabilities to optimize process execution and achieve integration objectives. Major vendors have consolidated their product portfolios, with IBM integrating process automation into enterprise asset management solutions, Oracle embedding AI agents across Fusion Cloud applications, and specialized vendors enhancing platform capabilities through continuous AI and analytics integration.

The services component represents the fastest-growing Business Process Management Market segment, with professional services, managed services, and managed automation gaining market share as organizations require specialized expertise for successful BPM implementation, system integration, and ongoing optimization. Service providers, including Infosys, HCLTech, Deloitte, and Accenture, are expanding BPM consulting and implementation capabilities, particularly around AI-driven process automation, legacy system transformation, and cloud migration initiatives.

Industry Insights

The BFSI sector dominates the Business Process Management Market with 24% market share in 2026, driven by inherent process complexity, stringent regulatory requirements, high transaction volumes, and critical risk management imperatives. Banks and financial institutions operate thousands of discrete processes spanning loan origination, account opening, transaction processing, fraud detection, compliance reporting, claims management, and customer service all of which require standardization, monitoring, and continuous optimization. BFSI organizations leverage BPM to automate labour-intensive workflows with dramatic efficiency gains: loan approval processes reduced from multi-day cycles to hours, KYC verification automated from manual document review to instantaneous validation, and compliance reporting eliminated from resource-intensive manual compilation to automated generation from transaction systems.

Regulatory pressure including Basel III capital requirements, GDPR data protection mandates, AML/KYC compliance obligations, and financial crime prevention standards creates non-negotiable BPM adoption requirements. The sector's capital-intensive nature and profitability pressures incentivise aggressive process optimization investment. India's BFSI sector expansion to INR 91 lakh crore (US$ 1 trillion) is driving BPM adoption across banks, non-bank financial companies (NBFCs), insurance providers, and asset management companies managing increasingly complex digital customer interfaces and regulatory requirements.

The IT & Telecommunications sector represents the business process management market's fastest-growing industry vertical, driven by rapid digital service expansion, 5G network deployment, increasing operational complexity, and competitive pressure from agile fintech and digital-native competitors.

India's telecommunications sector, with 1.21 billion subscribers and 86.09% tele-density in 2025, is driving BPM adoption to support rapid 4G and 5G network expansion, improve customer experience, and manage complex wholesale and retail operations. The IT & Telecommunications sector's talent mobility challenges, geographic distribution requirements, and operational complexity create compelling BPM adoption drivers distinct from BFSI's regulatory imperatives.

Regional Insights and Trends

North America Business Process Management Market Trends

North America commands 35% of the global business process management market, representing the most mature and advanced adoption ecosystem, driven by large enterprise concentration, sophisticated technology infrastructure, and aggressive digital transformation investment. The region's BFSI institutions, with trillions in assets under management and mission-critical process requirements, have led global BPM adoption for two decades, creating sophisticated process optimization cultures and established vendor relationships.

United States enterprises continue to drive BPM market growth through enterprise automation spending targeting operational efficiency in finance operations, supply chain management, customer service, and manufacturing execution. The region exhibits the highest adoption of cloud-based BPM solutions, with enterprises balancing on-premises security requirements for sensitive data with cloud deployment benefits including scalability, rapid provisioning, and reduced infrastructure capital requirements.

East Asia Business Process Management Market Insights

East Asia commands 20% of the global business process management market with China and emerging Southeast Asian economies driving rapid adoption growth through accelerating digital transformation and increasing regulatory sophistication. China's banking and insurance sectors, with total banking assets reaching RMB 467.3 trillion (up 7.9% YoY) in Q2 2025, are driving extensive BPM adoption to support massive transaction volumes, regulatory compliance with Chinese banking commission requirements, and competitive responses to fintech innovation.

East Asian enterprises are rapidly adopting cloud-based BPM solutions, with regional cloud spending projected to grow significantly as compliance frameworks mature and data security confidence increases. The region's manufacturing sector, spanning automotive, electronics, pharmaceuticals, and heavy industry, is deploying advanced BPM for supply chain visibility, production optimization, and quality management. Government digitalization initiatives across China, India, and Southeast Asia are creating process automation opportunities in tax administration, regulatory enforcement, and citizen services delivery sectors, historically slower to adopt technology, but facing acceleration pressures from digital-first citizen expectations.

Europe Business Process Management Market Trends

Europe represents 25% of the global business process management market, characterized by conservative digital adoption patterns, stringent regulatory requirements, and strong emphasis on data privacy and security. The European Union's regulatory environment including GDPR, NIS2 cybersecurity requirements, and sector-specific regulations spanning financial services (PSD2), telecommunications (BEREC), and healthcare (eHealth Directive) creates immediate BPM adoption drivers as organizations mandate process standardization and automated compliance monitoring.

The region's €0.9 trillion financial and insurance sector value added in 2022, employing 5 million people across 867,000 enterprises, represents substantial BPM market potential. Banking sector structural transformation, with 5,304 credit institutions in 2023 (driven by digitalization efficiency pressures, necessitates significant process optimization and systems modernization investments.

Competitive Landscape

The global business process management (BPM) market is consolidated, dominated by a few major players who offer comprehensive, AI-enabled platforms and command significant market share. IBM leads with its intelligent automation and end-to-end process orchestration across industries, while Oracle strengthens its position through AI-embedded Fusion Cloud Applications that optimize finance, HR, and supply chain workflows. TIBCO Software differentiates itself with its AI-ready BPM MCP Server and unified TIBCO Platform, enabling seamless process automation and observability.

HCLTech drives BPM adoption with digital process outsourcing solutions like Toscona and digitalCOLLEAGUE, enhancing operational efficiency and customer experience. Infosys BPM leverages autonomous AI agents to transform accounts payable and other workflows, while Red Hat provides low-code, cloud-native BPM solutions for collaborative business-IT operations. Market competition is characterised by high technology integration, AI adoption, and platform scalability, making it challenging for smaller vendors to compete and reinforcing the consolidated nature of the market.

Key Industry Developments

- In November 2024, SS&C Blue Prism outlined the future direction of the Business Process Management (BPM) market, highlighting the evolution of BPM platforms toward AI-driven orchestration, agentic automation, and unified ecosystems integrating BPM with RPA, APIs, and AI to improve governance, scalability, and measurable AI ROI across enterprise workflows.

- In October 2025, Oracle advanced enterprise Business Process Management by embedding new AI agents across Oracle Fusion Cloud Applications, enabling intelligent automation, orchestration, and optimization of core business processes spanning finance, human capital management, supply chain, and customer operations, thereby improving straight-through processing, decision intelligence, compliance, and end-to-end workflow efficiency within enterprise BPM-driven digital transformation initiatives.

Companies Covered in Business Process Management Market

- IBM Corporation

- Software AG (Software GmbH)

- Oracle Corporation

- Red Hat, Inc.

- Kissflow Inc.

- Tibco Software Inc.

- OTRS AG

- Infosys Limited

- HCL Technologies Limited

- Newgen Software Technologies Limited

- PolariseMe

- Appian Corporation Inc.

- OpenText, Inc.

- Microsoft Corporation

- Accenture

Frequently Asked Questions

The global business process management market is projected to be valued at US$ 20.2 Bn in 2026.

The Solutions segment is expected to account for approximately 68.0% of the global Business Process Management Market by Component Type in 2026.

The market is expected to witness a CAGR of 17.9% from 2026 to 2033.

The Business Process Management Market growth is driven by enterprise digital transformation and operational modernization, rapid integration of AI-driven intelligent automation, and increasing regulatory compliance and risk management requirements across industries, particularly BFSI.

Key market opportunities in the Business Process Management Market include AI-driven intelligent and agentic automation for end-to-end process optimization, integration of process mining with advanced analytics for deep operational insights, and rapid adoption of low-code/no-code BPM platforms enabling faster deployment and broader SME and citizen-developer participation.