- Hardware & Software IT Services

- Business Productivity Software Market

Business Productivity Software Market Size, Share, and Growth Forecast 2026 – 2033

Business Productivity Software Market by Software Type (Office Suites, Collaboration Tools, Project & Task Management Software, Document Management Software, Workflow Automation Software, Business Intelligence & Reporting Tools, Time Tracking & Workforce Management Tools), by Deployment (On-premise, Cloud), by Enterprise Size (Large Enterprises, Small & Medium-sized Enterprises, Micro Businesses), by End Use (BFSI, IT & Telecom, Healthcare, Travel & Hospitality, Retail & e-Commerce, Manufacturing, Others), by Regional Analysis, 2026–2033

Business Productivity Software Market Size and Trend Analysis

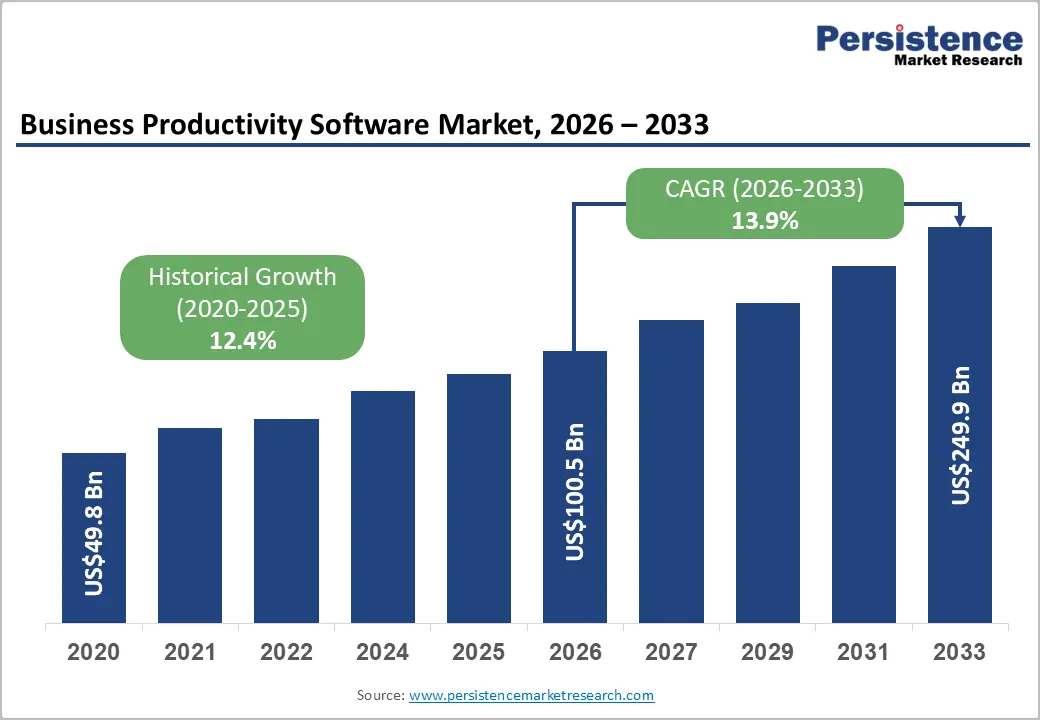

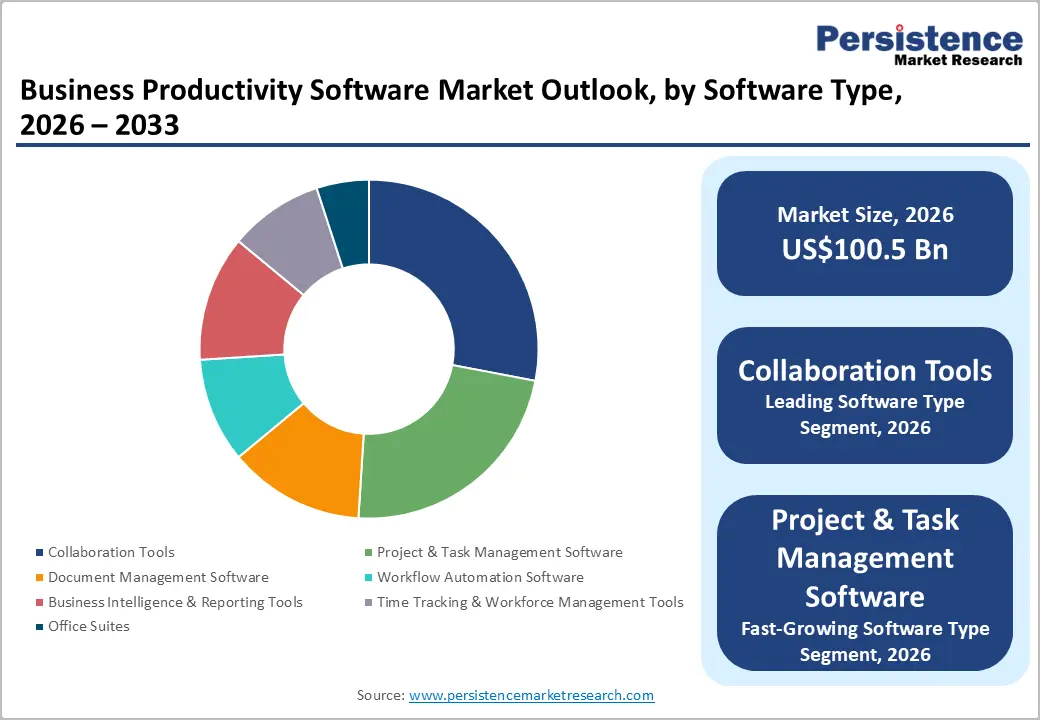

The global Business Productivity Software market size is likely to be valued at US$ 100.5 Billion in 2026 and is expected to reach US$ 249.9 Billion by 2033, growing at a CAGR of 13.9% during the forecast period from 2026 and 2033. The strong outlook is underpinned by accelerated digital transformation across enterprises, rapid adoption of cloud-based collaboration tools, and structural shifts toward hybrid and remote work models.

Key Market Highlights

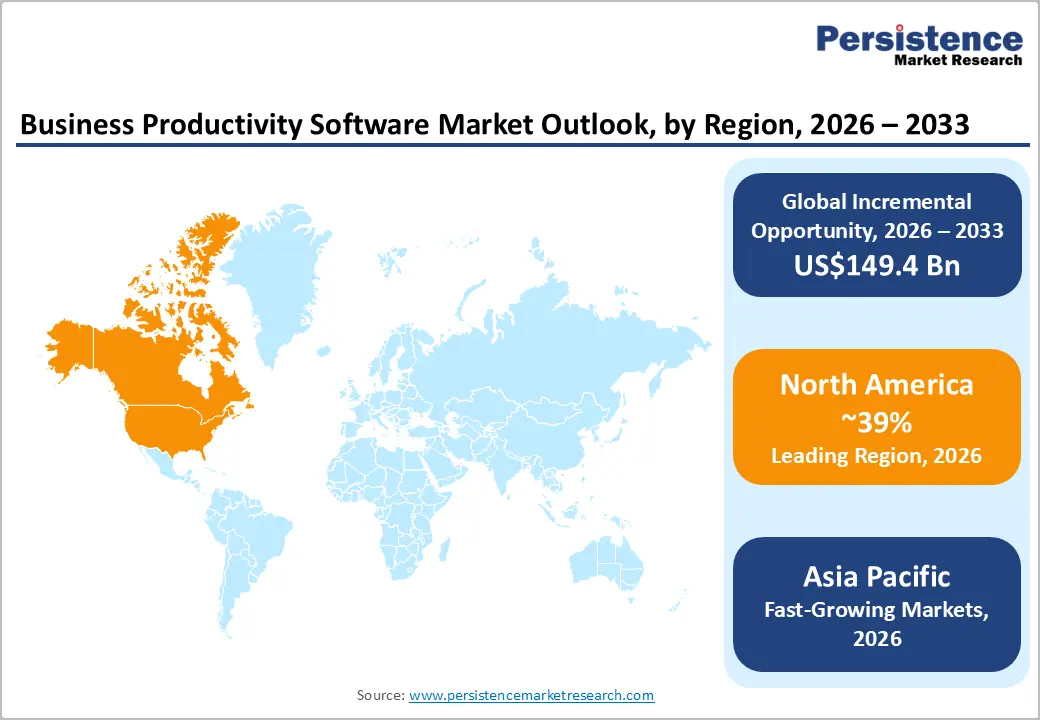

- Leading Region: North America currently leads the Business Productivity Software Market holding 39% share, supported by high cloud penetration, strong enterprise IT budgets, and an advanced innovation ecosystem centered on AI enabled collaboration and workflow automation tools.

- Fastest Growing Region: Asia Pacific is expected to be the fastest growing region with rising CAGR of 14.8%, driven by rapid SME digitization, large scale manufacturing transformation, and government backed digital economy programs across China, India, Japan, and key ASEAN markets.

- Dominant Segment: Among software types, Collaboration Tools form the dominant segment having 28% market share, acting as the central hub for communication, project coordination, and integration with document, workflow, and analytics applications across hybrid and remote work environments.

- Fastest Growing Segment: Cloud deployment is the fastest growing deployment segment with rising CAGR of 15%, as enterprises and SMEs prioritize scalable, subscription based productivity suites that simplify updates, enable AI features, and reduce infrastructure management overheads.

- Key Market Opportunity: AI driven productivity enhancements and intelligent automation capabilities embedded into everyday tools create a major opportunity for vendors and users, enabling significant time savings, higher quality output, and new value added subscription tiers.

| Key Insights | Details |

|---|---|

|

Business Productivity Software Market Size (2026E) |

US$ 100.5 Billion |

|

Market Value Forecast (2033F) |

US$ 249.9 Billion |

|

Projected Growth CAGR (2026–2033) |

13.9% |

|

Historical Market Growth (2020–2025) |

12.4% |

Market Dynamics

Market Growth Drivers

Rising Hybrid Work Models and Collaboration Intensity

The shift toward hybrid and remote work has fundamentally increased reliance on digital productivity ecosystems. According to Microsoft’s Work Trend Index, over 70% of employees globally prefer flexible remote or hybrid arrangements, pushing enterprises to standardize on tools such as Teams, Slack, and Google Workspace for persistent communication and project coordination.

The International Labour Organization (ILO) has highlighted that remote work adoption surged several-fold during and after 2020, embedding long term demand for always on collaboration, secure file sharing, and real time document co editing. These patterns directly expand the user base for office suites, collaboration tools, and project & task management software, driving recurring subscription revenues and cross sell of advanced analytics and security add ons across industries and regions.

Digital Transformation and Automation for Operational Efficiency

Enterprises are increasingly turning to workflow automation software, business intelligence & reporting tools, and integrated document management software to reduce manual work and improve process consistency. The World Economic Forum and OECD note that organizations deploying advanced digital tools can enhance labor productivity by 10–30% through streamlined workflows, reduced rework, and faster decision cycles.

In parallel, industry surveys indicate that more than 60% of large enterprises are investing in automation platforms for functions such as finance, HR, customer service, and supply chain management, with adoption particularly strong in BFSI and manufacturing. As automation and analytics are embedded into everyday productivity applications, the value proposition of unified business productivity software stacks strengthens, supporting higher spending per seat and multi year growth.

Market Restraints

Data Security, Privacy, and Compliance Concerns

Despite strong demand, enterprises remain cautious about exposing sensitive information through cloud based productivity suites, especially in regulated sectors. Data breaches and ransomware incidents reported by organizations such as ENISA and national cybersecurity agencies have highlighted vulnerabilities linked to misconfigured collaboration platforms and document repositories.

Stricter data protection regimes such as GDPR in Europe and regulations like CCPA in the U.S. require robust encryption, access controls, and audit trails, increasing deployment complexity and compliance cost. For risk averse sectors such as BFSI and public administration, these concerns can slow full scale migration to cloud deployments and limit experimentation with new AI driven productivity capabilities.

Integration Complexity and Legacy System Constraints

Many organizations still run mission critical workloads on legacy on premise systems and custom business applications that are difficult to integrate with modern productivity suites. Fragmented IT stacks, overlapping tools, and lack of standardized APIs often result in data silos and low user adoption.

Industry assessments indicate that a significant share of digital transformation projects either underperform or are delayed due to integration challenges and change management issues. Enterprises with constrained IT budgets, particularly SMEs and micro businesses, may struggle to justify complex multi year rollouts when immediate productivity gains are not visible, which can moderate the pace of new license adoption and expansion in some markets.

Market Opportunities

AI Enabled Productivity, Copilots, and Intelligent Automation

The integration of generative AI and intelligent copilots into office suites, collaboration platforms, and project & task management software creates a major upside for vendors and users. Large technology players such as Microsoft, Google, and Salesforce are embedding AI features that summarize meetings, auto generate documents, draft emails, and surface insights from enterprise knowledge bases.

Early pilots suggest that AI augmented workers can save several hours per week on routine tasks, with some studies from leading vendors and academic institutions indicating productivity gains exceeding 20% in knowledge work scenarios. As pricing models evolve to include AI add ons per user, vendors can expand average revenue per account, while customers unlock higher value from existing data and workflows. This AI wave offers compelling opportunities for both established participants and specialized startups focusing on niche vertical workflows.

SME Digitization and Cloud First Adoption in Emerging Markets

Small & medium sized enterprises and micro businesses in emerging regions are rapidly adopting cloud based productivity suites, often via subscription models that avoid upfront capital expenditure. Initiatives such as India’s Digital India, various ASEAN digital economy blueprints, and Latin American SME digitization programs encourage cloud software use for invoicing, collaboration, and workforce management. The World Bank and regional development agencies highlight that SMEs adopting digital tools can increase sales and export orientation while formalizing operations.

Lightweight time tracking & workforce management tools, entry level office suites, and integrated retail & e commerce plugins provide a low barrier entry into the business productivity software ecosystem. As these businesses scale, they tend to add workflow automation and business intelligence & reporting tools, creating a long term growth runway for vendors addressing the SME segment with localized, affordable, and mobile first offerings.

Category wise Insights

Software Type Analysis

Within Software Type, Collaboration Tools account for an estimated leading share of around 28% of global business productivity software revenues, ahead of traditional office suites and standalone project & task management software. Platforms such as Slack, Microsoft Teams, and Google Chat anchor daily communication, integrating messaging, video conferencing, file sharing, and app integrations.

During the pandemic period and beyond, daily active users on major collaboration platforms scaled into the tens of millions, reflecting a structural shift in how teams coordinate work. These tools increasingly serve as hubs that connect document management software, workflow automation, CRM, and developer tools via APIs and bots. Their central role in hybrid work environments and their ability to aggregate digital workflows justify their dominant market share and underpin stickiness across enterprise and SME segments.

Deployment Analysis

In the Deployment category, Cloud deployment models account for an estimated 63% share of the global business productivity software market, significantly outpacing onpremise installations. Public and hybrid cloud architectures enable elastic scaling, rapid feature delivery, and easier integration with AI and analytics services. Major productivity vendors report that a majority of new customer sign ups and renewals involve cloud first or cloud preferred options, while many existing on premise customers are transitioning to SaaS subscriptions as part of broader cost optimization and modernization efforts.

Regulatory advances, including clearer guidance on data residency and industry specific compliance certifications, have also improved enterprise confidence in cloud deployments. Consequently, cloud delivered productivity suites and collaboration platforms are expected to sustain their leadership as the de facto standard in both developed and emerging markets.

Enterprise Size Analysis

By Enterprise Size, Large Enterprises currently command an estimated 55% share of global revenues, reflecting their extensive user bases, complex workflows, and higher spending on advanced security, compliance, and integration features. Large organizations often deploy full stack productivity ecosystems that encompass office suites, collaboration tools, workflow automation, business intelligence, and time tracking & workforce management tools.

SMEs and micro businesses represent the fastest growing cohorts as they adopt cloud native solutions to compete with larger peers. Several industry studies show that SME adoption of cloud productivity tools has risen sharply since 2020, with penetration rates in some advanced economies surpassing 60% of small firms. This dual structure—large enterprises as stable, high value accounts and SMEs as dynamic growth drivers—shapes vendor go to market strategies, pricing, and product bundling.

End Use Analysis

Within End Use, the IT & Telecom segment holds an estimated leading share of about 24%, ahead of BFSI, retail & e commerce, and manufacturing. IT and technology service providers rely heavily on project & task management software, agile planning tools, and collaboration platforms to coordinate distributed development teams, manage sprints, and support clients across time zones.

Telecom operators, meanwhile, use workflow automation and business intelligence & reporting tools to streamline network operations, customer support, and marketing campaigns. The sector’s high digital maturity, continuous innovation cycles, and reliance on remote and distributed teams make it an early adopter and heavy user of integrated productivity stacks. As 5G, edge computing, and cloud services expand, IT & Telecom firms are expected to remain at the forefront of advanced productivity software implementation.

Regional Insights

North America Business Productivity Software Market Trends

North America is one of the most mature markets for business productivity software, characterized by early cloud adoption, a dense technology ecosystem, and high digital readiness among enterprises. The U.S. leads regional demand, supported by large technology companies, advanced BFSI institutions, and dynamic startups that rely on cloud collaboration tools, workflow automation, and business intelligence platforms as core infrastructure. Regulatory frameworks such as CCPA and sector specific guidelines in healthcare and finance push vendors to invest heavily in security, compliance, and data governance features.

The region also pioneers AI enabled productivity through offerings from Microsoft, Google, Salesforce, and others that integrate generative AI into email, documents, and collaboration channels. Venture funding into SaaS and productivity startups in the U.S. remains robust, catalyzing innovation in vertical specialized tools for legal, marketing, and engineering workflows. Canada’s federal and provincial digital strategies, along with strong broadband penetration, further support adoption among mid market organizations. Overall, North America sets benchmarks in feature richness and usage intensity, with enterprises frequently operating multi vendor productivity stacks optimized for hybrid work and advanced analytics.

Europe Business Productivity Software Market Trends

Europe represents a sizeable and sophisticated market shaped strongly by regulatory harmonization and data sovereignty priorities. Countries such as Germany, the U.K., France, and Spain have seen widespread adoption of office suites, team collaboration tools, and document management software to support manufacturing, public services, and knowledge intensive industries. The GDPR framework, along with sector specific regulations in finance and healthcare, has driven demand for solutions that embed privacy by design, granular consent management, and robust audit logging. Vendors increasingly offer EU hosted data centers and sovereign cloud options to address compliance requirements and build customer trust.

At the same time, initiatives under the EU’s Digital Europe Programme and national Industry 4.0 and e government strategies are accelerating the digitalization of SMEs and public sector entities. This catalyzes uptake of cloud collaboration, workflow automation, and business intelligence & reporting tools that integrate with ERP and CRM platforms. The U.K., as a leading services economy, exhibits strong adoption in professional services and financial institutions, while Germany and France drive manufacturing linked deployments. Overall, Europe’s market growth is underpinned by a combination of productivity imperatives, regulatory clarity, and continued investment in secure, interoperable digital workplaces.

Asia Pacific Business Productivity Software Market Trends

Asia Pacific is among the fastest growing regions for business productivity software, fueled by rapid economic expansion, manufacturing strength, and aggressive digital transformation programs. China, Japan, and India are key demand centers, while ASEAN economies such as Singapore, Indonesia, and Vietnam display strong adoption momentum. Governments across the region promote cloud computing, SME digitization, and e governance, leading to increased deployment of cloud based office suites, collaboration tools, and mobile first productivity applications. In manufacturing intensive economies, integration of workflow automation software and business intelligence into factory operations and supply chains improves visibility and efficiency.

India’s growing IT services sector and startup ecosystem, for example, relies heavily on project & task management software, time tracking & workforce management tools, and collaboration platforms to serve global clients. Japan and South Korea, with their focus on advanced manufacturing and innovation, combine productivity tools with IoT and robotics initiatives. Meanwhile, a large and expanding SME base across the region is adopting affordable SaaS productivity solutions, often via local cloud marketplaces and telecom partners. This combination of top down policy support and bottom up entrepreneurial adoption positions Asia Pacific as a key engine of future growth for the global business productivity software market.

Competitive Landscape

Market Structure Analysis

The business productivity software market is moderately concentrated at the platform layer, with global leaders such as Microsoft, Google, Salesforce, Oracle, Cisco, and Atlassian providing broad suites that span communication, collaboration, content, and analytics. At the same time, the ecosystem is highly dynamic and fragmented at the application level, with specialized vendors like Slack Technologies, Asana, Freshworks, Slab, Trello, Monday.com, ClickUp, Zoho, and Todoist differentiating through user experience, vertical focus, and workflow depth.

Competitive strategies revolve around expanding integrated suites, embedding AI copilots, deepening third party integrations, and offering flexible pricing for SMEs and large enterprises alike. Mergers, acquisitions, and ecosystem partnerships are common as firms seek to consolidate capabilities, enhance security and compliance, and deliver end to end digital workplace experiences.

Key Market Developments

- February, 2024: Microsoft expanded its AI enhanced productivity offerings by rolling out advanced Copilot capabilities across its Microsoft 365 suite, including deeper integration with Teams and Power Platform to automate complex workflows.

- June, 2024: Slack Technologies (part of Salesforce) introduced new AI features for channel summarization and knowledge discovery, aimed at reducing information overload and improving decision speed across distributed teams.

- September, 2023: Atlassian launched enhanced integrations between Jira, Confluence, and third party collaboration tools, along with new analytics features to optimize project delivery and cross team coordination.

Companies Covered in Business Productivity Software Market

- Slack Technologies

- Microsoft

- Cisco

- Asana

- Freshworks

- Slab

- Atlassian

- Trello

- Monday.com

- ClickUp

- Zoho

- Todoist

- Salesforce

- Oracle

Frequently Asked Questions

The global Business Productivity Software Market is projected to reach around US$ 249.9 Billion by 2033, up from US$ 100.5 Billion in 2026, reflecting a robust forecast CAGR of 13.9% over 2026–2033.

Demand is propelled by the widespread adoption of hybrid and remote work, accelerated digital transformation, and the need to streamline workflows using collaboration tools, workflow automation software, and business intelligence & reporting tools, which together enhance operational efficiency and decision‑making.

Among software types, Collaboration Tools form the leading segment, capturing the largest share as they serve as central hubs for communication, project coordination, and integration with document management, automation, and analytics applications across organizations.

North America dominates the market, supported by strong enterprise IT spending, high cloud adoption, a sophisticated innovation ecosystem, and early deployment of AI‑enabled productivity capabilities across sectors such as IT & Telecom and BFSI.

A major opportunity lies in embedding AI‑driven copilots and intelligent automation into everyday productivity tools, enabling workers to offload repetitive tasks, generate content faster, and surface insights from organizational data, thereby supporting new premium subscription models and higher value realization.

Leading players include Slack Technologies, Microsoft, Google, Cisco, Asana, Freshworks, Slab, Atlassian, Trello, Monday.com, ClickUp, Zoho, Todoist, Salesforce, and Oracle, alongside other ecosystem participants such as Adobe, SAP, HubSpot, ServiceNow, Notion Labs, and Smartsheet.