- Hardware & Software IT Services

- Business Intelligence Platform Market

Business Intelligence Platform Market Size, Share, and Growth Forecast, 2026 - 2033

Business Intelligence Platform market by Component (Software/Platform, Services), Organisation Size (Small & Medium Enterprises (SMEs), Large Enterprises), Deployment Mode (Cloud, On-Premises, Hybrid), Industry (Small & Medium Enterprises (SMEs), Large Enterprises), and Regional Analysis for 2026 - 2033

Business Intelligence Platform Market Size and Trends Analysis

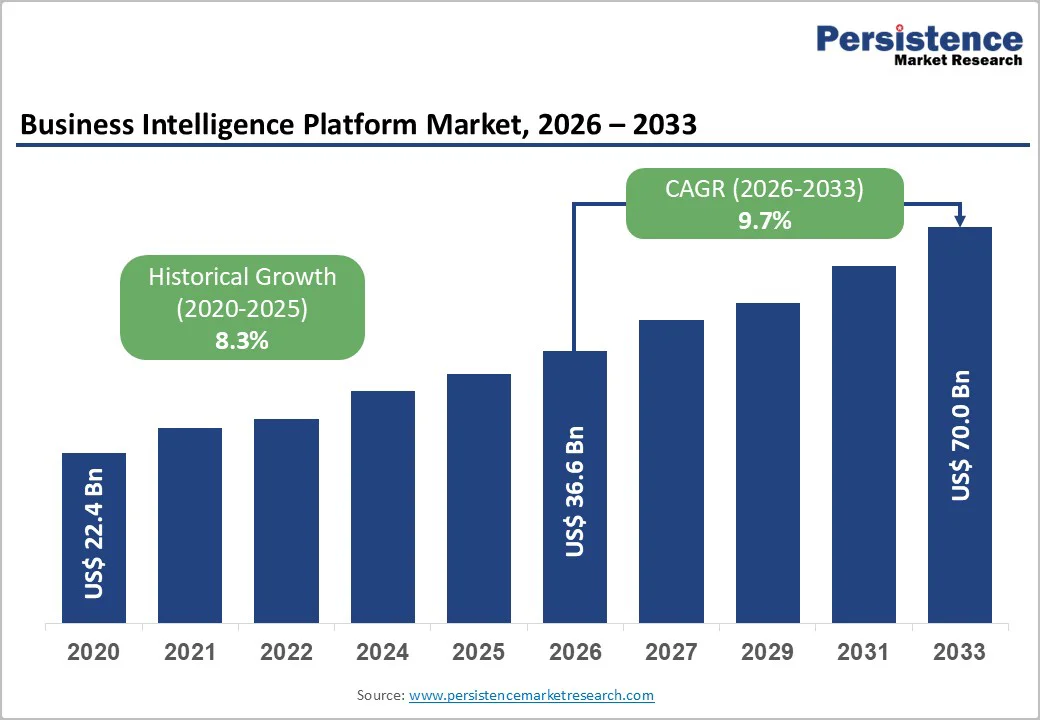

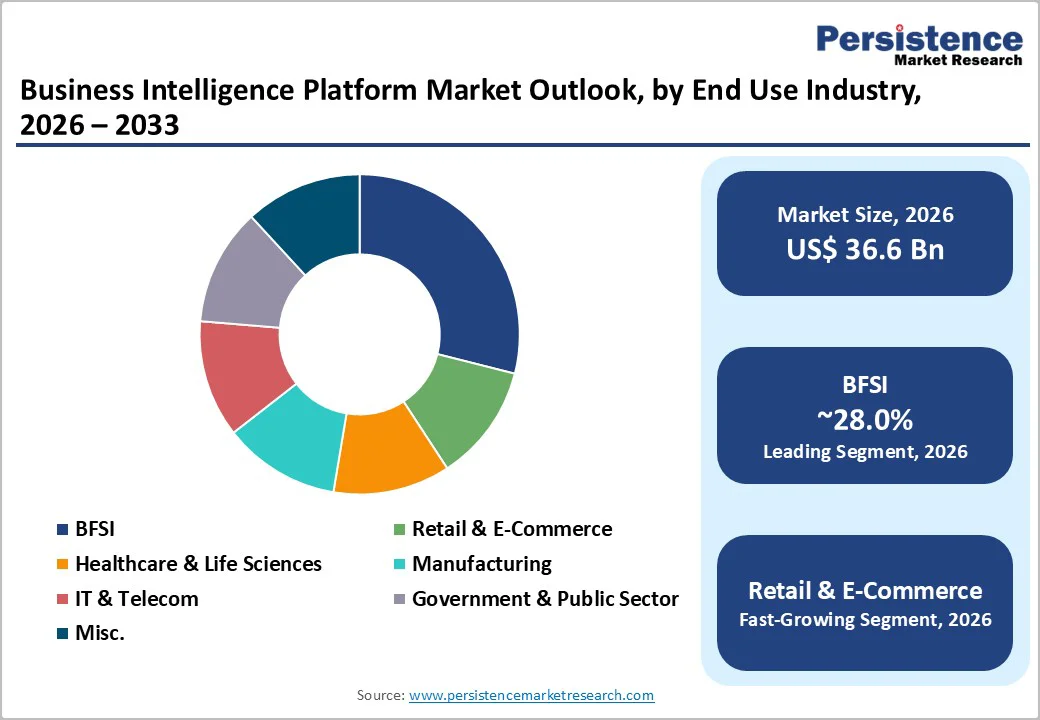

The global business intelligence platform market is projected to reach US$70.0 billion by 2033, growing at a CAGR of 9.7% between 2026 and 2033. The market is likely to be valued at US$36.6 billion in 2026. The market is driven by enterprise adoption of AI-augmented analytics, cloud-based deployment architectures, and regulatory compliance requirements across financial services, healthcare, and retail sectors.

Primary growth catalysts include the integration of generative AI into analytics platforms, the imperative for real-time decision-making, and government-mandated digital transformation initiatives across developed and emerging economies. The business intelligence platform market is characterised by rapid technological convergence between semantic modelling, agentic AI, and multi-cloud deployment paradigms, supported by substantial organisational capital allocation targeting data-driven competitive differentiation.

Key Industry Highlights:

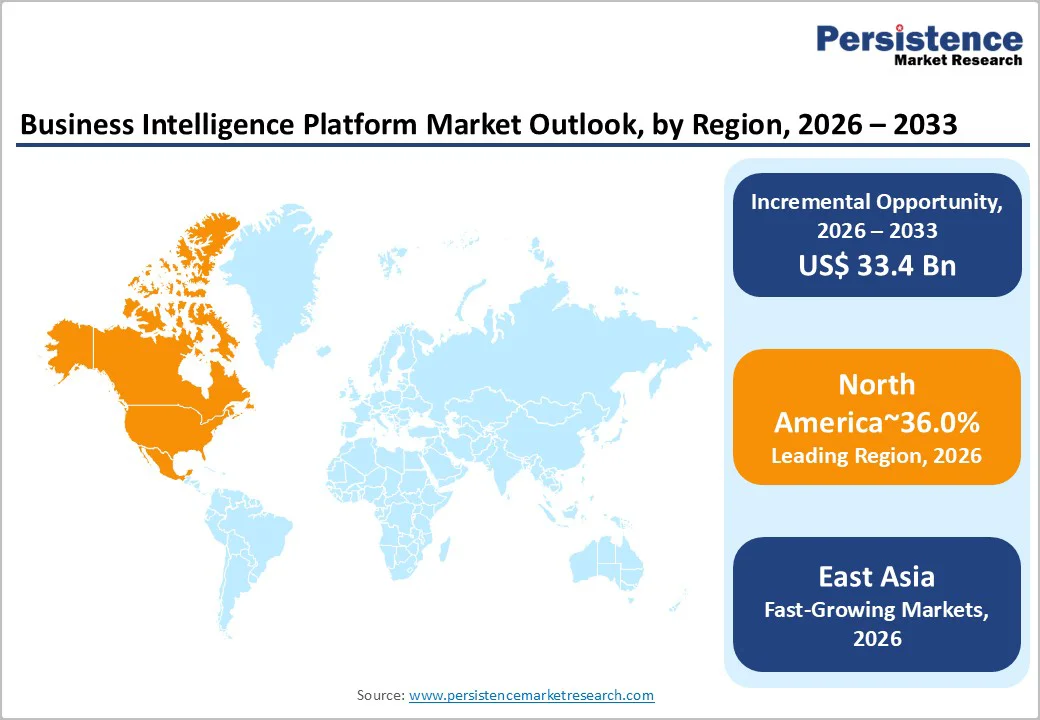

- Regional Leadership: North America leads the global Business Intelligence Platform market with an estimated 36% share in 2025, supported by strong enterprise digital-transformation spending and the dominance of major platform vendors such as Microsoft, Salesforce, and Tableau.

- Fastest-Growing Market: East Asia captures around 13% share in 2025 and is the fastest-growing region, driven by large-scale cloud adoption in China, acceleration of Industry 4.0, and government-backed digital-infrastructure programs.

- Component Dominance: Software/Platform remains the leading component category with an estimated 68% market share in 2025, strengthened by the rapid adoption of generative-AI analytics, semantic modelling, and natural-language query engines.

- Fastest-growing Component: Services emerge as the fastest-growing segment, fuelled by rising demand for implementation consulting, data-governance setup, and enterprise-wide BI optimisation across global organisations.

- Top end-user segment: BFSI leads the global market with an estimated 28% share in 2025, anchored by strong demand for compliance analytics, fraud detection, risk scoring, and DORA/GDPR/HIPAA-aligned reporting frameworks.

- Fastest-Growing End-user: Retail & E-commerce is the fastest-growing segment, driven by adoption of omnichannel analytics, customer-journey intelligence, and AI-driven personalisation for high-velocity digital commerce.

- AI-Driven Growth Opportunity: Generative AI, agentic analytics, and unified semantic-intelligence layers exemplified by Microsoft Fabric IQ and Tableau Next create a major market opportunity by transforming BI platforms into autonomous decision-intelligence engines.

| Key Insights | Details |

|---|---|

|

Business Intelligence Platform Market Size (2026E) |

US$ 36.6 Bn |

|

Market Value Forecast (2033F) |

US$ 70.0 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

9.7% |

|

Historical Market Growth (CAGR 2020 to 2025) |

8.3% |

Market Dynamics

Drivers - Generative AI Integration and Agentic Analytics Functionality Enhancement

Generative AI integration within Business Intelligence platforms represents a fundamental structural driver reshaping platform architectures and accelerating enterprise adoption velocity. Microsoft Power BI was recognised as a Leader in the Forrester Wave™: Business Intelligence Platforms Q2 2025, achieving the highest scores in generative AI functionality and securing top marks in 17 additional evaluation criteria, reinforcing market-wide recognition of AI-driven analytics capability differentiation. Microsoft's November 2025 announcement of Fabric IQ marked a major platform evolution, introducing a unified semantic intelligence layer integrated with Power BI and Microsoft Fabric, incorporating ontology-driven semantic modelling, real-time intelligence, graph-based insights, and autonomous operations agents, enabling enterprises to convert unified data into automated decision-making architectures.

Tableau's April 2025 introduction of Tableau Next demonstrated agentic analytics maturation, allowing users to collaborate with AI agents across entire data-to-action workflows through intelligent semantic layers, automated data preparation, and natural language querying. These generative AI advancements are expanding the addressable use cases in the Business Intelligence Platform Market beyond traditional reporting and dashboarding, enabling self-service analytics for non-technical business users while automating routine analytical workflows that previously required specialised data-science competencies.

Qlik Cloud Analytics® delivers natural-language data exploration and GenAI-powered explanations on in-memory analytics engines, enabling organisations to accelerate decision-making from weeks to hours. The convergence of semantic-layer governance with agentic AI is fundamentally reshaping Business Intelligence platform value propositions, driving sustained premium pricing and expanding enterprise willingness to deploy comprehensive, enterprise-wide analytics infrastructures despite intensifying competitive pressure.

Regulatory Compliance Frameworks and Data Governance Mandates

Regulatory complexity across financial services, healthcare, and emerging data-protection jurisdictions is driving substantial Business Intelligence Platform market demand for governance-embedded analytics architectures. The European Union's AI Act entered force in August 2024 with phased compliance timelines through August 2026, mandating risk-assessment frameworks, transparency measures, data governance practices, and human oversight mechanisms that directly impact analytics platform design and deployment.

The EU Data Act, effective September 12, 2025, introduced new rules for data access, sharing, and portability across connected devices and Internet of Things infrastructure, extending data-governance scope beyond personal data into non-personal industrial and operational data. The Digital Operational Resilience Act (DORA), effective January 17, 2025, imposes comprehensive information and communication technology risk management frameworks on financial-sector institutions, with non-compliance penalties of up to 10 million euros or 2% of annual global turnover, driving substantial regulatory-compliance analytics investment within BFSI segments.

Healthcare organisations implementing AI-driven analytics alongside robust HIPAA compliance frameworks have demonstrated 23% improvement in clinical outcomes, with early-intervention protocols guided by predictive algorithms reducing hospital readmissions by up to 31%, validating compliance-first analytics architectures within regulatory-sensitive sectors.

The Business Intelligence Platform Market benefits directly from these regulatory mandates, as enterprise IT departments allocate capital toward governance-embedded analytics solutions capable of demonstrating audit-trail transparency, access controls, and algorithmic explainability required for regulatory certification and third-party compliance verification. Governance complexity creates switching costs and customer lock-in, supporting sustained revenue expansion even as competitive intensity increases across platform vendors.

Restraint - Data Quality and Integration Complexity Within Heterogeneous Enterprise Environments

Enterprise data environments remain fragmented across legacy on-premises systems, cloud-based SaaS applications, and emerging data-lake architectures, creating substantial integration complexity that constrains Business Intelligence Platform deployment velocity. Most enterprises operate across 6–12 distinct data sources, including ERP, CRM, financial systems, and operational databases, each utilising proprietary data formats, authentication mechanisms, and synchronisation protocols that require custom integration development.

Data quality challenges persist within these heterogeneous environments, with 40–50% of enterprise data characterised as low-quality, incomplete, or inconsistent, requiring substantial data-preparation investment upstream of analytics deployment. Custom integration projects typically require 6–12 months of development effort and significant ongoing maintenance costs to maintain data currency and consistency across source systems, creating deployment delays and limiting Business Intelligence Platform penetration within cost-sensitive segments.

These integration barriers are particularly acute for small and medium-sized enterprises lacking dedicated data-engineering resources, constraining adoption of SaaS analytics platforms despite reduced capital barriers relative to on-premises deployments. The technical complexity of data governance, metadata management, and lineage tracking introduces specialised skill requirements that remain scarce within manufacturing and retail segments, further constraining Business Intelligence Platform market expansion beyond sophisticated technology and financial services organisations.

Opportunity - Vertical-Specific Analytics and Industry-Tailored BI Solution Development

The heterogeneous analytical requirements across healthcare, retail & e-commerce, manufacturing, and financial services are creating substantial opportunities for specialised Business Intelligence Platform vendors developing industry-specific analytics solutions with embedded domain knowledge and regulatory compliance architectures.

Healthcare organisations require HIPAA-compliant data governance frameworks, patient-privacy protections, and clinical analytics capabilities to support longitudinal patient-outcome assessment and population-health management, which generic Business Intelligence platforms inadequately address. Retail & e-commerce enterprises require customer analytics capabilities, including real-time segmentation, predictive recommendation engines, and omnichannel customer-journey analysis aligned with emerging customer-data-platform and marketing-analytics integrations. Manufacturing sectors require supply-chain visibility, production-optimisation analytics, and predictive maintenance capabilities embedded within product-lifecycle and enterprise-asset-management frameworks.

The financial services regulatory environment requires specialised compliance reporting, anti-money laundering transaction surveillance, and advanced fraud detection analytics, which demand sector-specific data models and regulatory knowledge integration. Specialised Business Intelligence Platform vendors developing vertical solutions, such as Domo's recognition as a Strong Performer in The Forrester Wave™: Business Intelligence Platforms Q2 2025, for cloud-native, full-stack BI integration with specialised data-governance capabilities, are capturing premium pricing and higher customer retention than horizontal, generic platforms.

The business intelligence platform market will expand through vertical-solution proliferation, addressing unmet analytical requirements within specialised industries, enabling smaller vendors to establish market leadership within niche segments. In comparison, larger vendors acquire specialised capabilities through partnerships or acquisitions to maintain comprehensive industry coverage.

Strategic Partnerships and Ecosystem Integration Expanding Business Intelligence Market Addressability

Strategic partnerships between business intelligence platform vendors and complementary software and infrastructure providers are expanding market addressability through integrated, end-to-end analytics ecosystems. Microsoft's June 2025 multi-year early extension of its Databricks partnership, with native integrations between Azure Databricks, Azure AI Foundry, Microsoft Power Platform, and SAP Databricks on Azure, exemplifies strategic alignment, enabling organisations to harness unified data for analytics, AI, and machine learning.

Vena's November 2022 integration of its Complete Planning platform with Microsoft Power BI Embedded enhanced Insights and Analysis capabilities with advanced analytics and AI-powered business intelligence, enabling organisations to leverage real-time analytics, predictive modelling, and interactive dashboards within planning workflows. These strategic partnerships create ecosystem effects that increase switching costs, expand platform functionality, and accelerate adoption velocity by simplifying organisational data-infrastructure consolidation.

Regional business intelligence vendors are achieving market leadership through partnership strategies aligned with regional government-supported digital-transformation initiatives; the India cloud computing market is projected at around 18-20% CAGR through FY 2033, driven by state-program initiatives including Digital India and government support for cloud-based Business Intelligence adoption across BFSI, healthcare, and manufacturing sectors. The business intelligence platform market is likely to expand through ecosystem-partnership proliferation, enabling horizontal platforms to address vertical-specific requirements through specialised integrations while reducing customer infrastructure complexity and total cost of ownership.

Category-wise Analysis

Component Insights

Software and platform components represent the dominant component-segment revenue within the Business Intelligence Platform Market in 2026, capturing 68.0% of global sales. This revenue concentration reflects the primary value concentration within analytics software, semantic layers, query optimisation engines, and visualisation capabilities constituting the core Business Intelligence Platform architecture. Differentiation across competing vendors, including Microsoft Power BI, Tableau, Qlik, Domo, and Looker, centres on platform capabilities, including generative AI integration, natural-language querying, semantic modelling, and real-time analytics performance rather than professional-services or consulting differentiation.

Services revenue encompassing professional consulting, custom-development services, managed analytics operations, and ongoing platform optimisation represents the fastest-growing component segment within the Business Intelligence Platform Market. Service revenue typically accounts for 20–30% of total deployment value, reflecting the complexity of platform implementation, organisational change management, and ongoing analytical capability optimisation.

As organisations expand Business Intelligence Platform deployments from single-department pilots to enterprise-wide multi-application implementations, professional services for requirements analysis, data modelling, implementation management, and user training accelerate.

Industry Insights

Financial services institutions represent the largest end-use industry segment for Business Intelligence Platform Market revenue in 2026, capturing 28.0% of global sales. BFSI sector dominance reflects regulatory compliance requirements, customer-risk assessment imperatives, fraud-detection priorities, and operational-efficiency optimisation across banking, insurance, and capital-markets institutions globally. Regulatory complexity, including DORA, anti-money-laundering transaction surveillance, know-your-customer customer-assessment, and anti-fraud-detection mandates, drives substantial analytics investment within financial-services institutions competing on risk-adjusted returns and compliance excellence.

Retail and e-commerce enterprises represent the fastest-expanding end-use industry segment within the Business Intelligence Platform Market, driven by digital-transformation mandates and customer analytics competition for omnichannel customer-experience optimisation.

Deployment Mode

Cloud deployment represents the dominant deployment-mode segment within the Business Intelligence Platform Market in 2026, commanding 60.0% of global revenue. Cloud-based analytics platforms eliminate heavy upfront capital expenditure requirements, enable continuous feature releases and capability updates, and reduce infrastructure-management overhead, driving organisational preference for SaaS analytics solutions over on-premises deployments. Cloud-based Business Intelligence platforms provide standardised compliance controls, automated backup and disaster-recovery capabilities, and secure multi-tenant architecture enabling rapid deployment and scalability without requiring dedicated IT infrastructure investment.

Microsoft Azure, Amazon Web Services, and Google Cloud Platform have established cloud-computing infrastructure dominance, with SaaS-based Business Intelligence platforms leveraging cloud-provider capabilities to deliver scalable, resilient, and cost-effective analytics deployments. Cloud deployment enables rapid internationalization and multi-region deployment, supporting organizations expanding into emerging markets without requiring local infrastructure capital investment.

Regional Insights and Trends

North America Business Intelligence Platform Market Trends

North America represents the largest geographic Business Intelligence Platform Market region, commanding approximately 36% of global revenue. The United States dominates the region, driven by advanced technology infrastructure, substantial enterprise capital allocation toward digital transformation, and leading-position market concentration among major Business Intelligence Platform vendors, including Microsoft, Salesforce, and Tableau. North American technology spending reached USD 2.7 trillion in 2025, with digital-transformation investments growing at 6.1% annually, establishing North America as the globally dominant digital-transformation investment region.

North American enterprises demonstrate the highest Business Intelligence Platform adoption maturity, with large organisations utilising sophisticated analytics across finance, marketing, operations, and customer-facing applications. Microsoft Power BI recognition as a Leader in Forrester Wave Q2 2025 reflects North American market dominance. Forrester serves a primarily North American analyst and vendor base, indicating platform strength within the region. U.S. regulatory framework complexity, including SEC reporting requirements, SOX compliance, and anti-fraud detection mandates, drives substantial BFSI analytics investment.

East Asia Business Intelligence Platform Market Trends

East Asia represents the second-largest Business Intelligence Platform Market region, accounting for approximately 13% of global revenue with the fastest projected growth rates through 2033. China dominates the region, driven by massive domestic-market scale, government-backed digital transformation mandates, and rapid expansion of cloud computing infrastructure. China's manufacturing sector accounts for approximately 31.7% of China's GDP, with the "Made in China 2025" strategic initiative directly supporting advanced-technology development, including AI, cloud computing, and big-data analytics. Government support for cloud adoption and digital-infrastructure investment is accelerating SaaS Business Intelligence Platform deployment within Chinese enterprises competing across manufacturing, e-commerce, and financial services.

Japan maintains critical technology-infrastructure roles within East Asia through advanced cloud-computing capabilities and enterprise-software leadership. Southeast Asia's emerging manufacturing positioning, with China investing around USD 25 billion in Southeast Asian FDI for manufacturing expansion, is creating incremental Business Intelligence Platform demand within regional manufacturing enterprises transitioning to Industry 4.0 manufacturing paradigms requiring advanced production analytics and supply-chain visibility.

Europe Business Intelligence Platform Market Trends

Europe represents approximately 27% of the global business intelligence platform market revenue, with distinct emphasis on regulatory compliance, data-governance excellence, and privacy-protection frameworks. The European Union's GDPR, AI Act, Data Act, and DORA regulatory framework create stringent data-governance and compliance requirements, driving substantial Business Intelligence Platform investment in security, encryption, and compliance-control capabilities. Organisations operating across EU jurisdictions must implement comprehensive data-protection and governance architectures, establishing Business Intelligence as essential infrastructure supporting regulatory compliance and organisational governance effectiveness.

The European digital-strategy framework, emphasizing data-governance excellence, public-dataset reuse, and federated cloud infrastructure, is accelerating Business Intelligence Platform adoption within public-sector organisations and regulated enterprises.

Germany's Industrie 4.0 initiative and European Union data-sovereignty strategy emphasizing European cloud-infrastructure development, are driving adoption of regionally hosted Business Intelligence solutions and European-based vendor alternatives to North American platform dominance. The EU's planned investment of EUR 2 billion in European High-Impact Projects supporting data-processing infrastructures and governance mechanisms is directly supporting European Business Intelligence Platform development and deployment capacity.

Competitive Landscape

The global business intelligence platform market reflects a consolidated and moderately oligopolistic structure, driven by the strong presence of major technology companies that dominate enterprise analytics adoption worldwide.

Leading players such as Microsoft Corporation, Salesforce, SAP SE, Oracle Corporation, IBM Corporation, and Qlik hold substantial market influence due to their extensive product ecosystems, global customer bases, and continuous investments in AI-driven analytics capabilities. These companies set competitive benchmarks through integrated cloud-based BI suites, advanced data visualisation tools, and predictive analytics features.

Although several emerging and mid-tier vendors like DOMO, Inc., Google, Sisense Ltd, and Yellowfin contribute to innovation, their market share remains comparatively limited. The high entry barriers created by technological complexity, customer switching costs, and strong enterprise partnerships further reinforce the dominance of top-tier players, keeping the competitive landscape concentrated with a few leaders shaping overall market direction.

Key Industry Developments

- April 21, 2025, Microsoft Power BI was recognised as a Leader in the Forrester Wave™: Business Intelligence Platforms, Q2 2025. The platform achieved the highest score among all vendors in generative AI functionality and secured top scores in 17 additional evaluation criteria. Forrester highlighted Microsoft’s continuous innovation, strong partner ecosystem, and the ability of Power BI to meet nearly all enterprise BI requirements, reinforcing its leadership position in the global Business Intelligence Platform market.

- November 18, 2025, Microsoft announced Fabric IQ at Microsoft Ignite 2025, marking a major evolution of its Business Intelligence Platform by introducing a unified semantic intelligence layer integrated with Power BI and Microsoft Fabric. Fabric IQ enhances BI capabilities with ontology-driven semantic modelling, real-time intelligence, graph-based insights, and autonomous Operations Agents, enabling enterprises to convert unified data into real-time business understanding and automated decision-making.

Companies Covered in Business Intelligence Platform Market

- STMicroelectronics

- ABB Ltd. / ABB (considered the same, kept as ABB Ltd.)

- Endress+Hauser Management AG

- Banner Engineering Corp.

- Schneider Electric

- Emerson Electric Co.

- Yokogawa Electric Corporation

- NXP Semiconductors

- Cisco Systems, Inc.

- Huawei Technologies Co., Ltd.

- Advantech Co., Ltd.

- Analog Devices, Inc.

- Texas Instruments Incorporated

- Intel Corporation

Frequently Asked Questions

The global Business Intelligence Platform market is projected to be valued at US$ 7.2 Bn in 2026.

The BFSI segment is expected to account for approximately 28.0% of the global Business Intelligence Platform market by End Use Indsutry in 2026.

The market is expected to witness a CAGR of 9.7% from 2026 to 2033.

Generative AI integration, agentic analytics enhancement, and expanding regulatory-driven data-governance requirements are the core forces accelerating Business Intelligence Platform market growth.

Vertical-specific analytics expansion and ecosystem-driven BI platform integrations are creating the strongest market opportunities in the Business Intelligence Platform market.