- Beauty & Personal Care

- Body Shaper Market

Body Shaper Market Size, Share, Trends, and Growth Forecast 2025 - 2032

Body Shaper Market by Product Type (Upper Wear Shapers, Bottoms Shapers, Shaping Bodysuits, Others), Material (Cotton, Spandex, Polyester, Nylon, Others), End-user (Female, Male), Regional Analysis, 2025 - 2032

Body Shaper Market Size and Trend Analysis

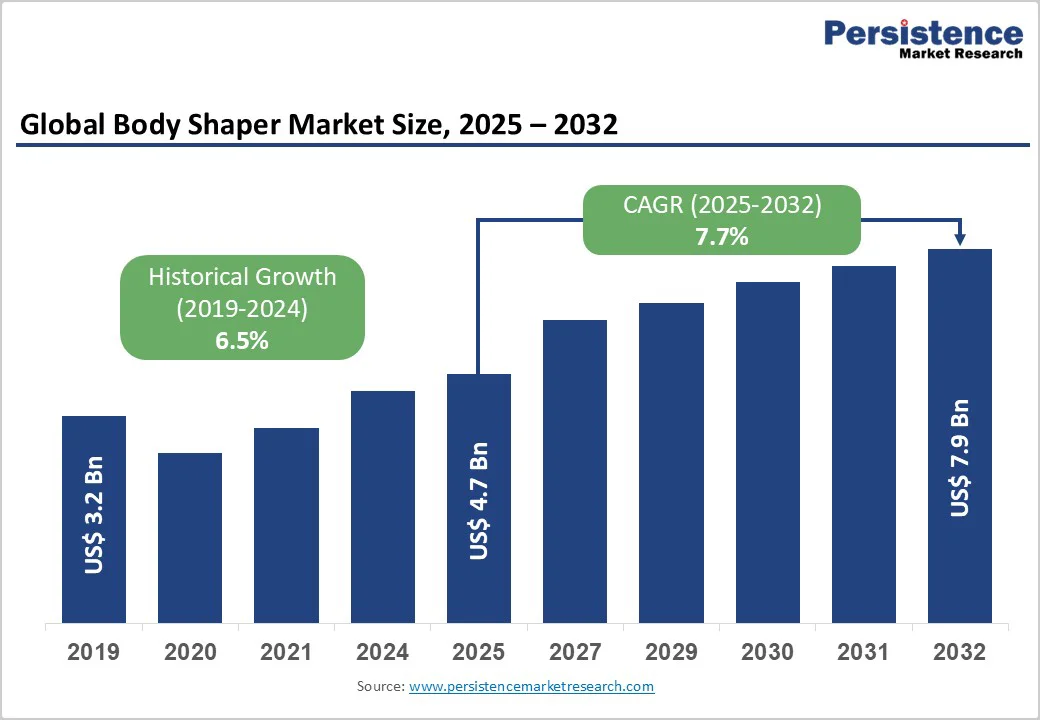

The global body shaper market size is likely to value at US$ 4.7 billion in 2025 and is projected to reach US$ 7.9 billion by 2032, growing at a CAGR of 7.7% between 2025 and 2032.

This growth is driven by rising health and fitness consciousness and the merging of athleisure with shapewear. The body positivity movement has redefined shapewear as confidence-boosting apparel offering posture support and muscle compression. According to industry data, 72.9 million fitness facility memberships were recorded in the United States in 2023, accounting for 23.7% of the population, significantly boosting demand for performance-oriented shapewear.

Key Industry Highlights:

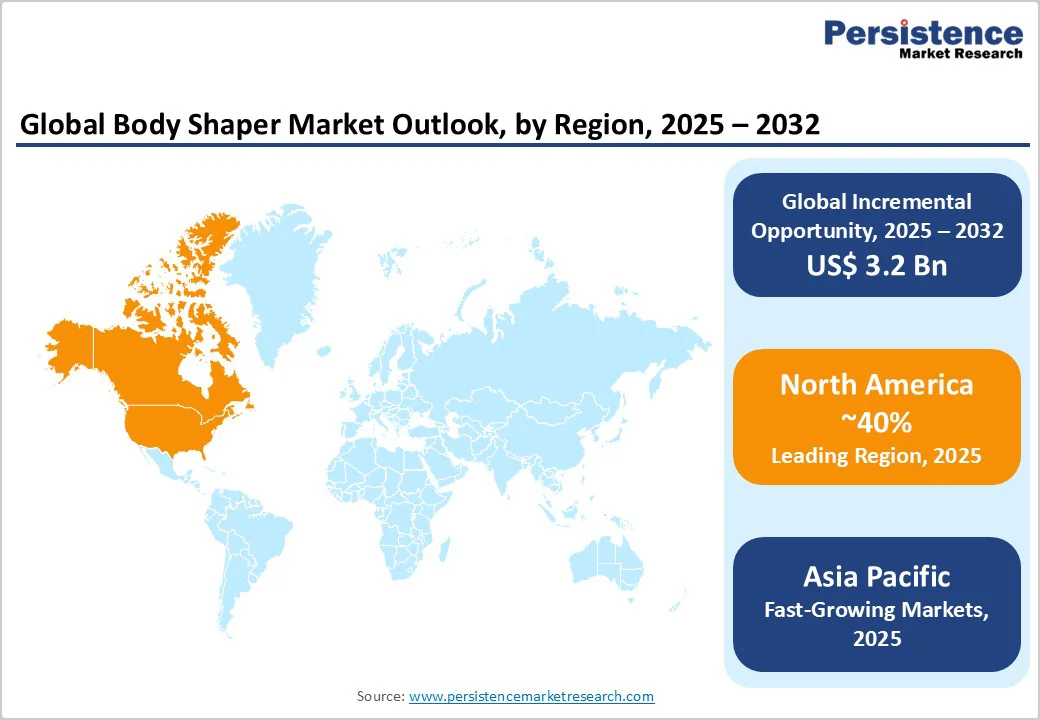

- Leading Region: North America leads the global body shaper market with over 40% market share, driven by strong U.S. sales growth and increasing preference for premium shapewear products.

- Fastest-Growing Region: Asia Pacific emerges as the fastest-growing market, supported by China’s dominant 25% regional contribution, India’s rising urban female workforce, and technology-driven shapewear innovations in Japan and South Korea.

- Dominant Segment: Shaping bodysuits account for nearly 38% of total sales, offering full-body contouring, seamless comfort, and versatility across both lifestyle and professional wear categories.

- Fastest-Growing Segment: The male shapewear segment is expanding rapidly, propelled by rising grooming awareness, body confidence trends, and growing product availability across online retail platforms.

- Key Opportunity: Medical-grade and postpartum compression shapewear present strong growth potential, witnessing nearly 10% CAGR as consumers seek recovery, comfort, and aesthetic support post-surgery or childbirth.

| Key Insights | Details |

|---|---|

| Body Shaper Market Size (2025E) | US$ 4.7 Bn |

| Market Value Forecast (2032F) | US$ 7.9 Bn |

| Projected Growth CAGR (2025 - 2032) | 7.7% |

| Historical Market Growth (2019 - 2024) | 6.5% |

Market Dynamics

Drivers - Rising Health and Fitness Consciousness Driving Functional and Performance-Oriented Shapewear Demand

Increasing global health awareness and fitness participation have significantly boosted the demand for shapewear that goes beyond aesthetic enhancement to deliver functional benefits.

Consumers now look for garments that support muscle recovery, improve posture, and enhance circulation during workouts or daily activities. According to the World Health Organization, nearly 69% of adults engage in regular physical activity, reflecting a strong potential market for performance-integrated shapewear designed for comfort and endurance.

This shift toward active lifestyles has led brands to innovate with high-performance features such as moisture-wicking, stretchable, and breathable materials. Advanced antimicrobial coatings, capable of reducing bacterial growth by up to 99%, ensure hygiene during extended wear. The fusion of fitness, recovery, and fashion continues to reposition shapewear as a staple in the global athleisure segment.

Technological Advancements in Fabric Engineering Enhance Comfort, Durability, and Performance in Modern Shapewear

Continuous innovation in textile science has revolutionized the body shaper industry, turning traditional compression garments into performance-driven, adaptive wear. Spandex-nylon blends now deliver superior elasticity and long-term shape retention, while moisture-wicking polyester ensures faster sweat evaporation and thermal regulation. These advancements enable shapewear to provide both sculpting support and day-long comfort, bridging the gap between fashion and functionality.

The global spandex market reflects this technological shift, expected to grow from US$ 7.9 billion in 2025 to US$ 14.8 billion by 2032 at a 9.4% CAGR. Leading sportswear and apparel brands, including Nike and Adidas, integrate patented technologies such as Dri-FIT and Primegreen into compression lines, reinforcing shapewear’s evolution toward sustainable, high-performance, and lifestyle-centric apparel.

Restraints - Counterfeit and Low-Quality Products Undermining Brand Credibility and Consumer Trust

The growing prevalence of counterfeit shapewear, particularly on major e-commerce platforms, poses a serious challenge to legitimate manufacturers and established brands. These imitation products often mimic branded designs but use substandard materials and poor stitching, leading to discomfort, skin irritation, and dissatisfaction. According to the OECD, counterfeit apparel accounts for an increasing share of global online fashion sales, directly impacting brand equity and long-term consumer confidence.

To mitigate these risks, companies are investing heavily in anti-counterfeiting technologies such as QR code authentication, blockchain-enabled supply tracking, and awareness campaigns. While these initiatives help protect consumers, they also increase operational costs, making it harder for genuine players to maintain competitive pricing in a crowded marketplace.

High Product Pricing and Cost Sensitivity Restricting Adoption in Emerging Economies

Premium shapewear products require specialized fabrics, precision manufacturing, and advanced design processes, all of which elevate production costs. As a result, brands often position their offerings in higher price brackets, which limits accessibility in developing regions where disposable incomes remain modest. For instance, the average shapewear price in the UK reached £46.16 in 2023, marking a rise of £6.90 since 2021, reflecting global inflationary pressures on apparel manufacturing.

Fluctuating raw material costs for spandex, nylon, and polyester further constrain pricing flexibility, compelling brands to balance affordability with quality. This sensitivity to price hampers widespread adoption in emerging economies such as India, Indonesia, and Brazil, where consumers often prioritize cost efficiency over premium performance features in apparel purchases.

Opportunity- Expanding Demand for Medical-Grade and Post-Surgical Compression Shapewear in Recovery and Therapeutic Applications

Medical-grade compression shapewear is emerging as a key high-growth segment within the apparel industry. These garments, designed with compression levels between 17-20 mmHg, help minimize swelling, enhance blood circulation, and speed up healing after cosmetic surgeries such as liposuction, abdominoplasty, and tummy tucks. The postpartum shapewear segment is growing at nearly 10% CAGR, supported by rising awareness of body recovery and comfort among new mothers.

Brands such as Marena Recovery and MACOM Medical are introducing adjustable, antimicrobial garments distributed through medical and wellness channels. The integration of breathable, ergonomic fabrics further boosts patient compliance. As aesthetic procedures and post-surgery recovery awareness increase globally, medical-grade shapewear continues to gain traction in both healthcare and retail markets.

Smart Technology Integration and Sustainability Advancements Redefining Shapewear Performance and Appeal

The incorporation of smart textiles and sustainable materials is transforming the global body shaper market. Emerging wearable technologies enable posture correction, fitness tracking, and adaptive compression for enhanced comfort and performance. Companies such as Hexoskin have developed FDA-cleared smart garments for monitoring physiological parameters, opening new possibilities in both medical and lifestyle applications.

Simultaneously, sustainability has become a critical purchase driver, with 75% of consumers willing to pay more for eco-friendly apparel. Recycled polyester, organic cotton, and Tencel made via closed-loop production are increasingly used by leading brands. Europe remains at the forefront, with GOTS-certified sustainable textile facilities expanding by nearly 300% between 2017 and 2023, reinforcing a global shift toward ethical manufacturing.

Category-Wise Insights

Product Type Analysis

Shaping bodysuits hold the largest share of the global body shaper market at approximately 38%, owing to their all-in-one, seamless construction that delivers comprehensive torso sculpting. Unlike separate top and bottom garments, bodysuits eliminate overlapping and bulging issues, ensuring smoother contours under clothing. Their convenience, comfort, and aesthetic appeal make them a preferred choice among consumers seeking everyday shaping solutions and special-occasion wear alike.

Brands such as Spanx and Skims have revolutionized this category with inclusive sizing options ranging from XXS to 4X, and innovative designs like thong bodysuits, open-bust variants, and adjustable straps. Their modern silhouettes cater to comfort, mobility, and confidence, driving rapid adoption across global retail and online fashion platforms.

Material Analysis

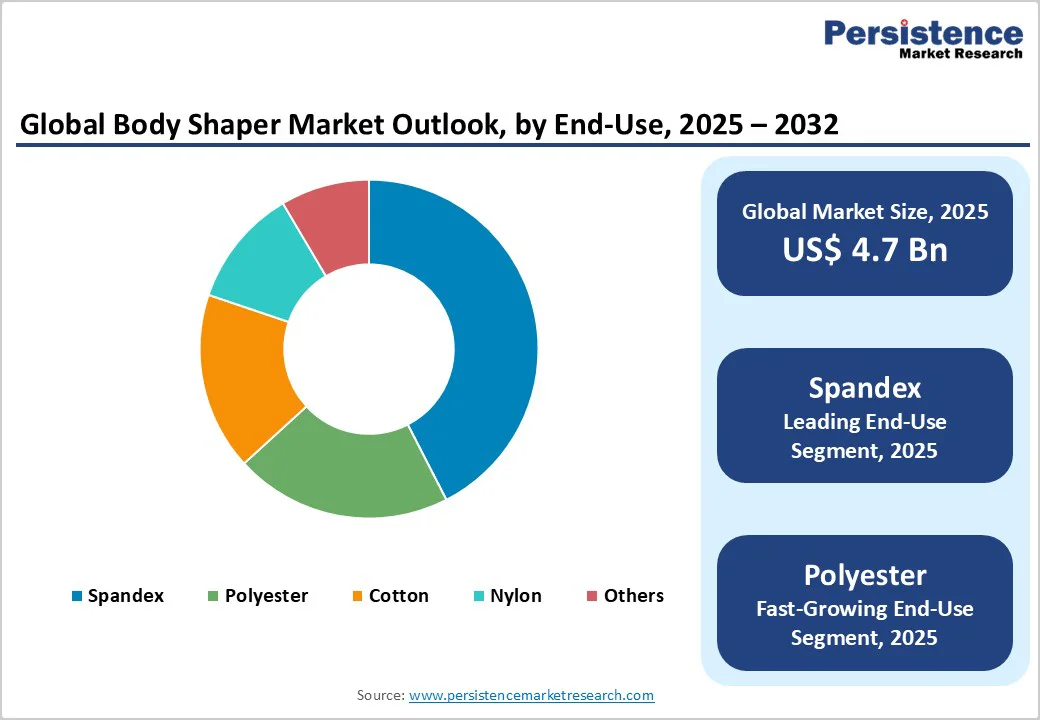

Spandex continues to dominate the shapewear material segment, commanding nearly 42% of the market. Its superior elasticity, recovery, and adaptability to body contours provide an ideal balance between compression and comfort. Nylon follows as the second most utilized material, valued for its durability, flexibility, and compressibility, ensuring lasting shape retention even with regular use. These fabrics together define the technical foundation of modern shapewear.

Polyester’s moisture-wicking properties have also gained traction, especially in sports-inspired compression garments that double as activewear. Meanwhile, eco-conscious consumers are increasingly driving demand for sustainable fibers such as organic cotton, bamboo, and Tencel. This sustainability shift is prompting leading brands to adopt recyclable or plant-based materials, aligning shapewear manufacturing with global green apparel trends.

End User Analysis

The female segment continues to dominate the global shapewear market, accounting for around 96% of total demand. Women’s shapewear enjoys widespread adoption due to product diversity, established retail availability, and deep cultural association with body contouring. From slimming slips to high-waist shapers, female consumers benefit from extensive product choices and fit innovations tailored to daily, professional, and special-event wear.

The male shapewear segment is expanding rapidly, recording a positive CAGR compared with female products. Increasing acceptance of male grooming, body toning, and fitness-oriented compression wear has broadened the consumer base. Brands such as Under Armour and 2XU are introducing purpose-built men’s shapers designed for both athletic performance and everyday comfort.

Regional Insights

North America Body Shaper Market Trends

In 2024, North America maintained its leadership in the shapewear industry, fueled by product innovation, celebrity-led branding, and strong retail integration. The U.S. remained the core hub for premium shapewear, with high consumer spending on comfort-driven, multifunctional apparel. Brands leveraged social media and influencer marketing to redefine shapewear as both lifestyle and fashion.

Skims’ October 2024 “Ultimate Bush” faux-hair thong launch exemplified the region’s bold marketing and inclusivity trend, while Spanx expanded its AirEssentials activewear line across major retail platforms. Premium quality, breathable compression fabrics, and body-positive messaging strengthened brand loyalty, positioning North America as the global trendsetter in next-generation shapewear design.

Europe Body Shaper Market Trends

Europe’s shapewear market in 2024 centered on sustainability, material innovation, and inclusivity. Growing consumer preference for ethical, eco-certified apparel encouraged brands to use recycled nylon, Tencel, and organic cotton. Regulatory frameworks promoting circular fashion and waste reduction further reinforced this shift toward responsible production.

Body positivity campaigns across the U.K., Germany, and France redefined shapewear as empowerment apparel rather than restrictive wear. Premium labels such as Triumph, H&M, and Chantelle expanded collections featuring adaptive sizing and biodegradable materials. European consumers prioritized transparency in sourcing and manufacturing, driving collaborations with certified textile producers under GOTS and OEKO-TEX standards.

Asia Pacific Body Shaper Market Trends

In 2024, the Asia Pacific emerged as the fastest-evolving shapewear market, propelled by rising digital retail adoption and beauty-focused consumer culture. China’s e-commerce giants introduced dedicated shapewear segments targeting millennials and Gen Z, emphasizing fit, comfort, and affordability. Urban professionals across India and Southeast Asia increasingly embraced shapewear for both fitness and daily wear.

Japan and South Korea led in fabric technology, developing lightweight, anti-sweat compression garments suited for humid climates. The fusion of shapewear with athleisure aesthetics gained traction through online fashion brands and regional influencers. Local manufacturers invested in seamless knitting and sustainable fiber technologies, enhancing product comfort and longevity to meet evolving lifestyle needs.

Competitive Landscape

The global body shaper market is moderately consolidated, marked by a blend of established apparel innovators and fast-emerging fashion-tech brands. Competition revolves around design innovation, advanced fabric engineering, and inclusive product offerings that cater to diverse body types. Many brands are diversifying into athleisure and recovery wear while investing in adaptive sizing, seamless construction, and smart compression technology to enhance comfort and performance.

Digital transformation remains central to competitive strategy, with virtual fitting tools, subscription-based models, and omnichannel retail strengthening customer engagement. Sustainability certifications, eco-friendly materials, and transparency in sourcing are key differentiators, positioning brands to appeal to both wellness-oriented and environmentally conscious consumers.

Key Market Developments

- In October 2024, Skims unveiled its “Ultimate Bush” faux-hair thong collection, generating significant social media attention and influencer engagement. The launch strengthened brand visibility, promoted body inclusivity, and reinforced Skims’ market valuation of US$4 billion, highlighting its continued influence in shaping contemporary shapewear trends.

- In January 2024, Spanx strategically expanded its portfolio in January 2024 with the launch of AirEssentials activewear, integrating performance-focused fabrics and ergonomic compression. This move positioned the brand within the active lifestyle segment, attracting fitness-conscious consumers and broadening its market reach beyond traditional shapewear offerings.

- In April 2024, Shapellx introduced INNER ARMOR medical-grade compression shapewear, while Knix Wear debuted leakproof postpartum designs. Both launches emphasized functional recovery, hygiene, and comfort, addressing niche healthcare and maternal needs. These innovations highlight the industry’s growing focus on medical applications and postpartum support solutions.

Companies Covered in Body Shaper Market

- Skims

- Maidenform

- Wacoal America

- Honeylove

- Nike

- PUMA

- Ann Chery

- Hanesbrands

- Marks & Spencer

- Rago Shapewear

- Body Hush

- Adidas

- Triumph International

- Leonisa

- Under Armour

- Wacoal Holdings Corp

- Shapellx, Commando

- Miraclesuit

Frequently Asked Questions

The global body shaper market is projected to reach US$ 7.9 Bn by 2032, up from US$ 4.7 Bn in 2025 at a 7.7% CAGR.

Key drivers include rising fitness facility memberships such as 72.9 million in the US (23.7% of population), advancements in antimicrobial fabrics reducing bacteria by 99%, and the body positivity movement reframing shapewear as empowerment apparel.

Shaping Bodysuits lead with 38% share, offering all-in-one torso contouring, popularized by inclusive sizing ranges (XXS-4X) from brands like Spanx and Skims.

North America leads with over 40% share in 2025.

Medical-grade post-surgical compression wear, with the postpartum shapewear segment growing at 10% CAGR, offers premium pricing potential.

Major players include Skims, Hanesbrands, Wacoal, Triumph International, and athletic brands Nike, Adidas, Puma.