- Baby Care & Accessories

- Baby Food Packaging Products Market

Baby Food Packaging Products Market Size, Share, and Growth Forecast, 2025 - 2032

Baby Food Packaging Products Market by Material (Plastic, Paper, Metal, Glass, Others), Form Type (Liquid, Dried), Product (Bags & Pouches, Boxes & Cartons, Cups & Containers, Stick Pack, Cans, Others), and Regional Analysis for 2025 - 2032

Baby Food Packaging Products Market Size and Trend Analysis

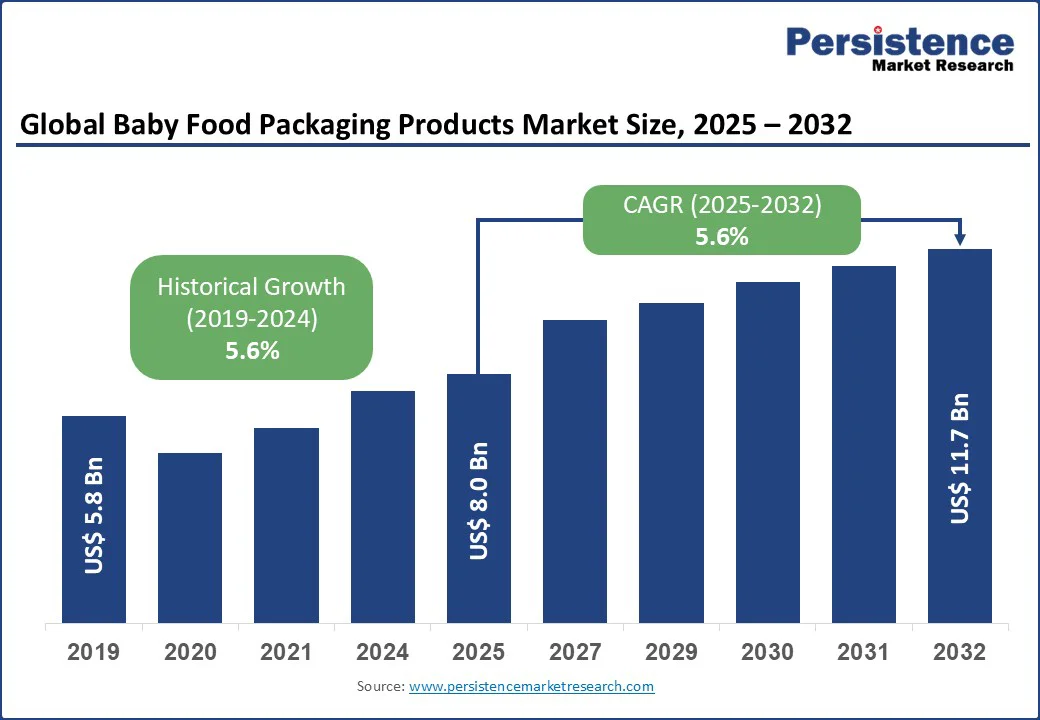

The global baby food packaging products market size is expected to be valued at US$8.0 billion in 2025 and is projected to reach US$11.7 billion by 2032, growing at a CAGR of 5.6% during the forecast period from 2025 to 2032.

The major growth factor is the rising demand for convenient, safe, and sustainable packaging solutions. Increasing awareness among parents about food safety and hygiene has fueled the adoption of high-quality, tamper-proof, and BPA-free materials.

Urbanization, busy lifestyles, and the emergence of advanced baby food supplements have increased the demand for ready-to-eat and portable baby food options. Furthermore, advancements in eco-friendly packaging, such as recyclable pouches and biodegradable containers, are supporting long-term market expansion.

Key Industry Highlights:

- Major Developments: In 2024, Initiative Foods adopted Surdry’s retort technology for sustainable pouches, while Tetra Pak partnered with Lactalis to launch a carton made with certified recycled polymers.

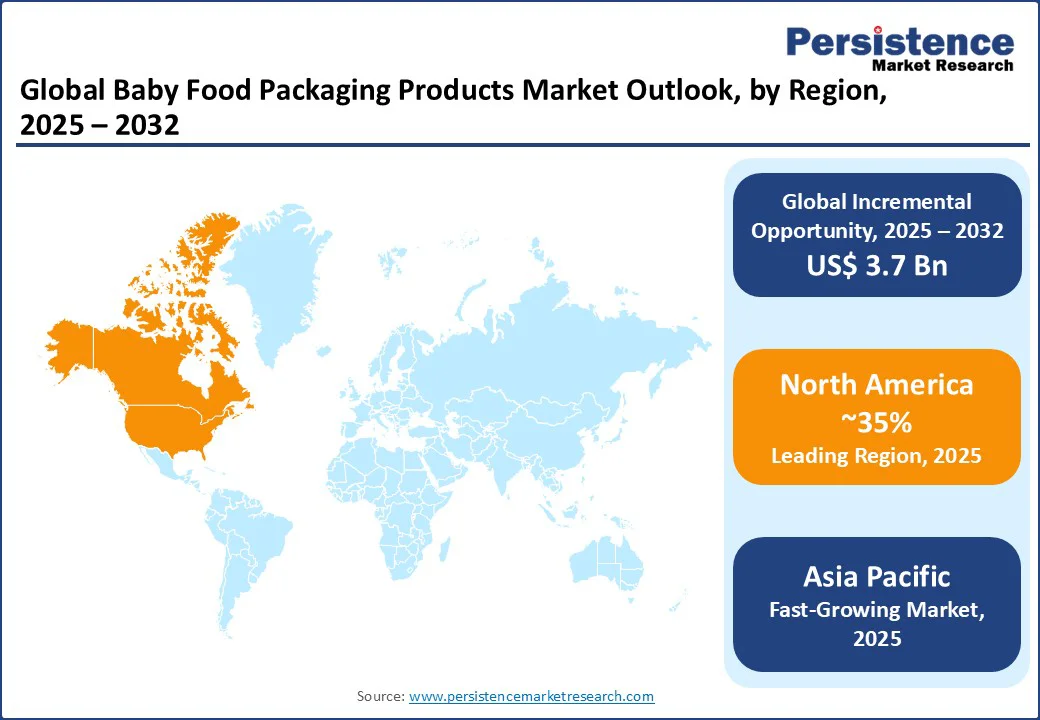

- Leading Region: North America dominates the global baby food packaging products market with a 35% share in 2025, driven by strong demand for convenience-driven packaging and stringent safety standards that ensure product quality.

- Fastest-Growing Region: Asia Pacific emerges as the fastest-expanding market in 2025, driven by rising birth rates, urbanization, and growing preference for safe, portable, and affordable baby food packaging solutions.

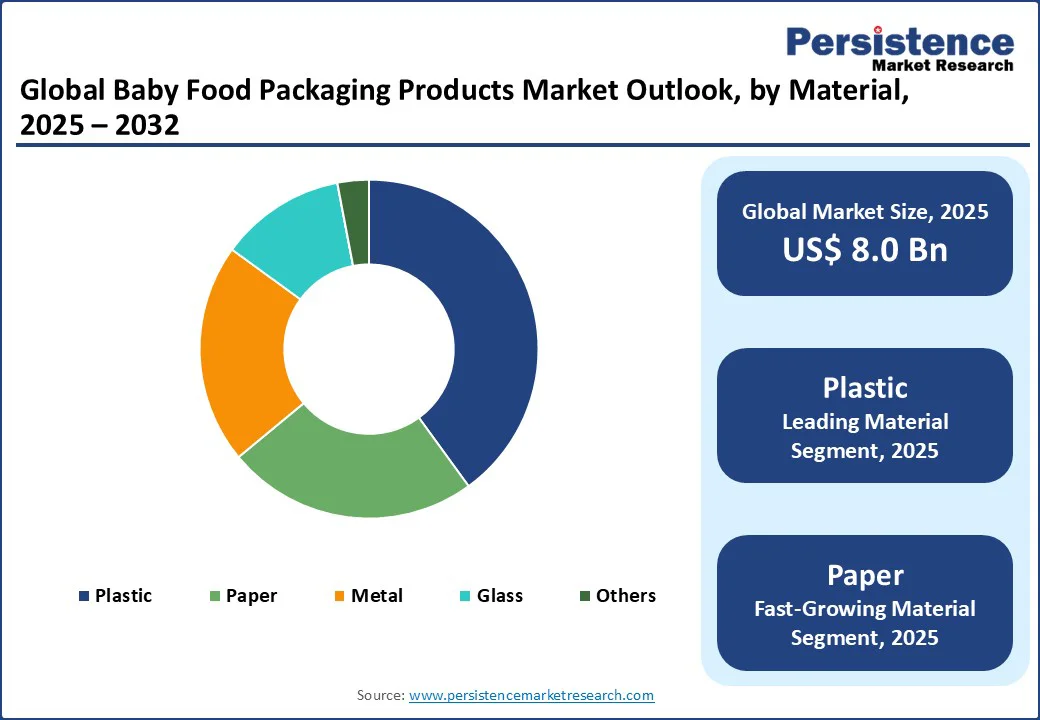

- Dominant Material: Plastic leads this segment with a 40% share in 2025, valued for its durability, lightweight design, extended shelf life, and 20% lower production costs than glass.

- Leading Form Type: Liquid form holds a 55% share in 2025, boosted by strong demand for milk formulas and ready-to-feed products, which are preferred by nearly 70% of urban parents globally.

- Leading Product: Bags and pouches capture a 45% share in 2025, favored for their lightweight, resealable, and portable designs, which reduce transport costs by almost 30% compared to glass jars.

|

Global Market Attribute |

Key Insights |

|

Baby Food Packaging Products Market Size (2025E) |

US$8.0 Bn |

|

Market Value Forecast (2032F) |

US$11.7 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.1% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.6% |

Market Dynamics

Driver - Consumer & Lifestyle Factors Creates the Need for Robust Food Solutions For Babies

Consumer lifestyles are evolving rapidly, with urbanization, dual-income households, and increasingly busy routines shaping purchasing behavior. Parents are increasingly opting for baby food packaging that ensures safety, convenience, and portability, such as resealable pouches and single-serve containers. Rising health awareness is also driving demand for BPA-free, tamper-proof, and hygienic solutions that cater to modern parenting needs. With more families seeking ready-to-feed options, packaging innovation has become central to meeting these lifestyle-driven demands.

Environmental awareness is another factor influencing consumer choices, as parents tend to opt for biodegradable and recyclable packaging that aligns with their sustainable living values. For instance, India’s Plastic Waste Management Rules, strengthened with Extended Producer Responsibility (EPR) guidelines, mandate recycling targets and restrict the use of non-recyclable multi-layer plastics, directly driving manufacturers to innovate eco-friendly packaging.

Such regulations not only support sustainability but also empower eco-conscious consumers to select baby food products packaged in safer, environmentally responsible formats, reinforcing long-term market growth.

Restraint - Environmental Concerns and Sustainability

One of the major restraints affecting the baby food packaging products market is the rising concern over environmental sustainability. Conventional packaging materials, particularly single-use plastics and non-biodegradable components, significantly contribute to global waste generation. As baby food often relies on flexible pouches, plastic containers, and multilayer laminates for durability and convenience, disposal challenges create long-term environmental burdens. This growing concern is prompting regulators, advocacy groups, and eco-conscious consumers to scrutinize the environmental impact of packaging, prompting manufacturers to reassess their strategies.

Strict regulations on plastic usage and waste management in several countries are compelling companies to invest in sustainable packaging innovations, which often involve higher production costs.

For instance, the push toward recyclable or biodegradable materials requires redesigning supply chains and adopting new technologies, adding financial pressure on manufacturers. These sustainability-related constraints may slow market growth, as balancing cost efficiency with eco-friendly solutions remains a significant challenge for industry players.

Opportunity - Growth in Eco-Friendly Packaging and E-Commerce Expansion

The rising shift toward eco-friendly packaging presents a significant growth opportunity for the baby food packaging market. Parents are increasingly seeking sustainable solutions that ensure food safety while reducing environmental impact. Demand for biodegradable containers, recyclable pouches, and BPA-free packaging is increasing as consumers align their purchasing decisions with their ecological values. Manufacturers focusing on innovative green materials not only meet regulatory compliance but also gain consumer trust, positioning themselves as leaders in responsible packaging practices. This shift is transforming the competitive landscape and fostering long-term brand loyalty.

Alongside sustainability, the rapid expansion of e-commerce is creating new avenues for growth. Online platforms are becoming a primary channel for baby food purchases, particularly among tech-savvy and urban parents. This trend demands durable, lightweight, and secure packaging that can withstand shipping and handling while maintaining product integrity. By integrating eco-friendly designs with e-commerce-friendly formats, manufacturers can capitalize on both evolving consumer values and expanding digital marketplaces.

Category-wise Analysis

Material Insights

Plastic continues to dominate the baby food packaging products market, holding nearly 40% of the share in 2025. Its popularity is attributed to being lightweight, durable, and highly cost-effective compared to alternatives. High-density polyethylene (HDPE) accounts for around 60% of plastic-based packaging, offering strong barrier protection that ensures food safety and extends shelf life. This makes it the preferred choice for liquid milk formula and ready-to-eat baby food products. Additionally, its production cost is approximately 20% lower than that of glass, further strengthening its market leadership.

Paper packaging, however, is emerging as the fastest-growing material segment, supported by rising consumer demand for biodegradable and recyclable options. By 2032, the paper segment is expected to surpass $ 3.5 billion in value. Innovations, such as Tetra Pak’s paper-based cartons, which reduce environmental impact by nearly 50% compared to traditional plastic packaging, are driving this growth. Regulatory backing and a reported 30% rise in eco-conscious purchasing in 2024 further accelerate adoption.

Form Type Insights

The liquid form leads the baby food packaging products market, holding approximately 55% of the share in 2025. This dominance is largely fueled by strong demand for liquid milk formula and ready-to-consume baby food, which cater to the fast-paced lifestyles of urban families. Around 70% of urban parents prefer liquid products packaged in pouches and containers due to their convenience in feeding and portability. Globally, sales of liquid baby food products exceed 80 million units annually, highlighting their widespread adoption and trust among caregivers.

Dried form, however, is emerging as the fastest-growing category, supported by its longer shelf life and high portability. Powdered milk formula and baby cereals remain particularly popular in developing nations, where storage and affordability are key factors influencing purchasing decisions. In 2024, sales in the Asia Pacific rose by nearly 25%, driven by working parents’ preference for lightweight, easy-to-store options that ensure nutrition while minimizing waste and cost.

Product Insights

Bags and pouches dominate the baby food packaging products market, holding nearly 45% of the share in 2025. Their popularity is driven by lightweight, resealable, and portable designs that make feeding easier for parents. These formats are used in approximately 60% of prepared baby food packaging, resulting in a nearly 30% reduction in transportation costs compared to glass jars. Added features such as spout tops and tamper-evident seals further enhance safety and convenience, strengthening their position as the preferred packaging choice among busy families.

Cups and containers are emerging as the fastest-growing packaging type, fueled by innovations in recyclable, re-sealable, and travel-friendly formats. Nearly 40% of parents favor these products for on-the-go feeding, reflecting the changing needs of their lifestyle. In 2024, Tetra Pak introduced a new line of recyclable baby food containers, which drove segment adoption by almost 20%. This emphasis on sustainability and convenience is expected to drive up demand for cups and containers in the years to come.

Regional Insights

North America Baby Food Packaging Products Market Trends

North America dominates the baby food packaging products market, accounting for 35% market share in 2025. The region’s leadership is fueled by strong demand for convenience-focused packaging and strict safety regulations. The United States leads with revenue of around US$2.19 billion in 2024, supported by major players such as Gerber and Nestlé, alongside FDA guidelines ensuring BPA-free and tamper-proof packaging.

Canada also contributes significantly through government-backed initiatives that promote sustainable materials, as reflected in a 20% rise in recyclable pouch adoption in 2024. These factors reinforce North America’s position as a leader in safe, innovative, and eco-friendly packaging solutions

Europe Baby Food Packaging Products Market Trends

Europe holds a significant share of the baby food packaging products market, driven by strong consumer preference for eco-friendly and recyclable materials. In 2025, the region accounts for nearly 30% of global revenue, supported by strict EU regulations on plastic reduction and packaging sustainability. Countries such as Germany, France, and the UK lead the adoption of paper-based cartons and recyclable pouches, with sales of eco-conscious packaging rising by over 25% in 2024.

Major players such as Danone and Nestlé are investing in biodegradable and paper-based innovations, reinforcing Europe’s position as a hub for sustainable packaging trends and technological advancements.

Asia Pacific Baby Food Packaging Products Market Trends

Asia Pacific is the fastest-growing market for baby food packaging products, fueled by rising birth rates, urbanization, and increasing disposable incomes. In 2025, the region is projected to account for over 28% of global demand, with countries such as China, India, and Japan driving growth.

The preference for portable, affordable, and safe packaging solutions is accelerating the adoption of pouches, containers, and paper-based cartons. In 2024, the Asia Pacific region recorded a 25% surge in sales of dried baby food packaging, reflecting the demand of working parents for convenient and long-shelf-life products. Government support for sustainable materials further positions the region as a key hub for growth.

Competitive Landscape

The competitive landscape of the global baby food packaging products market is highly consolidated, with leading manufacturers collectively accounting for nearly 65–70% of global revenue in 2025. Competition centers on innovation, with a strong focus on sustainable, recyclable, and BPA-free packaging solutions to meet rising consumer and regulatory demands.

Companies are investing in advanced materials such as biodegradable cartons and lightweight pouches that reduce transportation costs by up to 30%. Strategic collaborations, regional expansions, and product diversification remain core strategies, while ongoing investments in eco-friendly packaging are expected to drive market differentiation and long-term competitiveness.

Key Developments

- July 2024: Initiative Foods adopted Surdry’s oscillating Steam Water Spray (SWS) retort technology to produce sustainable cups and pouches. This innovation enhanced energy and water efficiency while enabling safer, high-quality packaging formats that surpass traditional glass jars.

- October 2024: Tetra Pak partnered with Lactalis to introduce a carton package made with certified recycled polymers sourced from used beverage cartons. The launch, certified under the ISCC PLUS program, supported circular economy goals while maintaining product safety and performance standards.

Companies Covered in Baby Food Packaging Products Market

- Gerber Packaging

- Heinz Baby Food

- Nestle S.A.

- Piramal Glass

- Amcor

- AptarGroup

- Ball Corporation

- Owens-Illinois, Inc.

- Tetra Pak International S.A.

- Berlin Packaging

- Others

Frequently Asked Questions

The baby food packaging products market is projected to reach US$8.0 Bn in 2025, driven by demand for convenient and sustainable packaging.

Key drivers include rising birth rates, urbanization, consumer demand for eco-friendly packaging, and e-commerce growth.

The baby food packaging products market is expected to grow at a CAGR of 5.6% from 2025 to 2032, reaching US$11.7 Bn.

Opportunities include sustainable packaging innovations, e-commerce expansion, and increasing demand in emerging markets.

Leading players include Gerber Packaging, Heinz Baby Food, Nestlé S.A., Piramal Glass, Amcor, AptarGroup, Ball Corporation, Owens-Illinois, Inc., Tetra Pak International S.A., and Berlin Packaging.