- Automotive Components & Materials

- Automotive Wheel Market

Automotive Wheel Market Size, Share, and Growth Forecast, 2026 - 2033

Automotive Wheel Market by Material Type (Steel, Aluminum Alloy, Magnesium/Carbon Composite, Misc Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCV), Heavy Commercial Vehicles (HCV)), End User (OEM, Aftermarket), and Regional Analysis, 2026 - 2033

Automotive Wheel Market Size and Trends Analysis

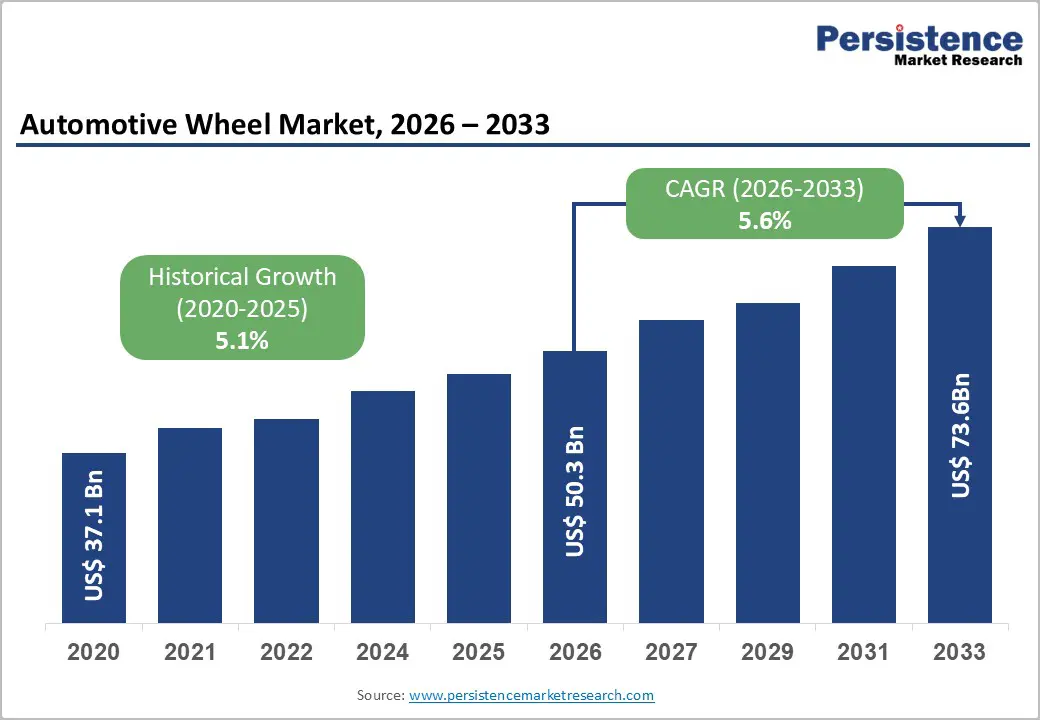

The global automotive wheel market size is likely to be valued at US$ 50.3 billion in 2026 and is projected to reach US$ 73.6 billion by 2033, growing at a CAGR of 5.6% between 2026 and 2033. This expansion reflects fundamental shifts in vehicle electrification, lightweight material adoption, and emerging market automotive expansion.

The market's acceleration from a historical CAGR of 5.1% to 5.6% signals intensifying demand for advanced wheel technologies that deliver weight reduction, performance optimisation, and manufacturing efficiency across diverse vehicle platforms. Steel wheels maintain foundational market dominance, while aluminum alloy and specialty composite wheel systems capture disproportionate growth reflecting EV adoption, regulatory decarbonization requirements, and customer preference for high-performance vehicle configurations.

Key Industry Highlights:

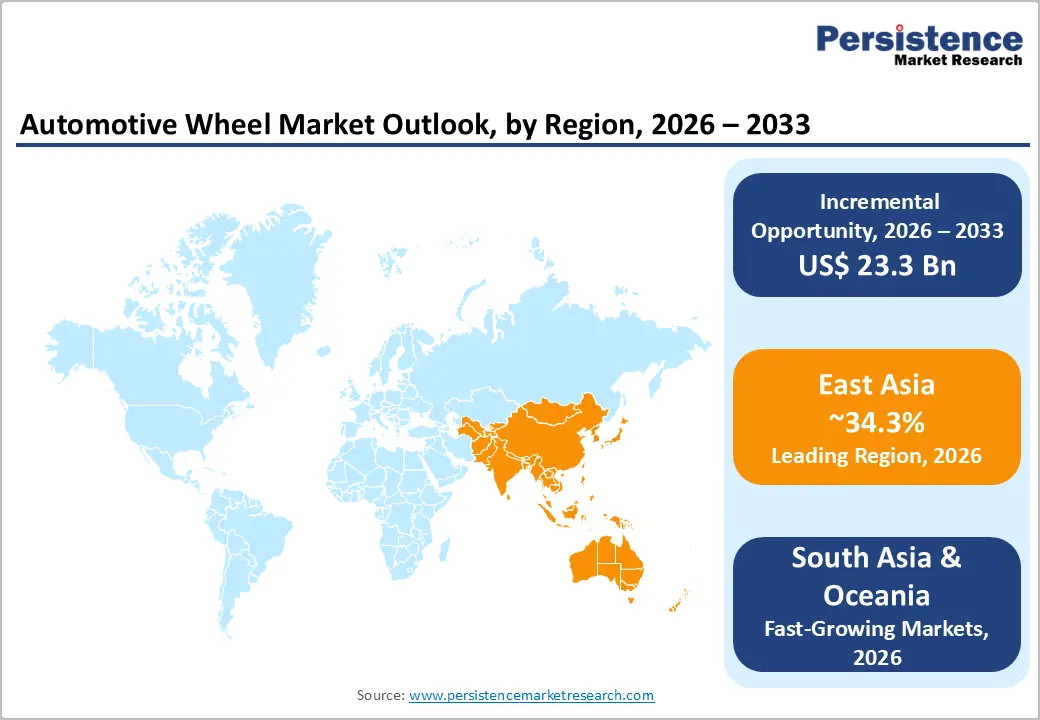

- Leading Region: East Asia leads the global automotive wheel market with 34.3% share, driven by China’s dominant vehicle manufacturing scale and accelerated EV ecosystem development.

- Fastest-Growing Regional Market: Europe accounts for ~24% market value, supported by stringent emission norms, premium vehicle production, and advanced alloy wheel adoption.

- Dominant Vehicle Segment: Passenger cars remain the dominant application category, 58.4% share, driven by rising vehicle ownership, SUV mix shift, and strong OEM production volumes.

- Fastest-Growing Vehicle Segment: Light Commercial Vehicles (LCVs) represent the fastest-growing segment, supported by booming last-mile logistics, e-commerce distribution, and urban fleet electrification.

- Material Innovation: Aluminum alloy wheels are the fastest-growing material category, driven by automotive lightweighting, EV battery efficiency requirements, and superior performance compared to steel.

- Electrification Growth Catalyst: EV adoption accelerates the development of high-strength alloy, magnesium, and carbon-composite wheels to reduce weight and improve aerodynamic efficiency.

- Manufacturing Expansion Opportunity: Automotive production growth across India, China, and Latin America boosts OEM demand, supported by industrialisation, infrastructure upgrades, and export-oriented vehicle programs.

| Key Insights | Details |

|---|---|

| Automotive Wheel Market Size (2026E) | US$ 50.3 Bn |

| Market Value Forecast (2033F) | US$ 73.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.1% |

Market Dynamics

Vehicle Electrification and Lightweight Material Adoption for Extended Driving Range

Vehicle electrification represents a transformative structural force reshaping the Automotive Wheel Market globally, requiring specialised wheel designs and materials that optimise energy efficiency and extend operating range. Global car registrations reached 74.6 million units in 2024, marking a 2.5 percent increase over 2023, with electric vehicle momentum accelerating substantially across regions. Battery-only electric cars reached nearly 5.9 million in 2024, reflecting a 32% year-on-year increase, though they accounted for only 2.3% of the total fleet.

Emerging markets demonstrate particularly strong EV adoption momentum, with India's automotive production reaching 3.10 crore (31 million) vehicles in FY 2024-25, including significant growth in utility vehicle and three-wheeler segments. Research demonstrates that a 10% reduction in vehicle weight can yield 6-8% improvements in energy efficiency, making lightweight wheels critical for EV competitiveness.

The Automotive Wheel Market responds by adopting aluminum alloys, offering 30-40 percent weight reduction relative to traditional steel wheels, thereby extending EV driving range without requiring larger, more costly battery packs. Magnesium and carbon composite wheels further optimise weight efficiency, with specialised applications in high-performance EV segments. Manufacturers report battery cost reductions of approximately US$ 900-1,600 per vehicle for each kilogram of weight reduction, creating powerful economic incentives for lightweight wheel deployment.

Global Automotive Production Expansion and Regional Vehicle Manufacturing Growth

Automotive production and vehicle manufacturing expansion across emerging markets represents a critical growth vector for the Automotive Wheel Market, driven by infrastructure investment, rising middle-class vehicle ownership, and regional OEM supply chain localisation. Global car manufacturing reached 75.5 million units in 2024, though showing a slight 0.5 percent decline, reflecting demand normalisation after 2023 inventory backlogs.

Regional performance demonstrates substantial variation: North American production declined 3.2 percent, while South American production grew 1.7 percent, led by Brazil's 6.3 % expansion. India's automotive sector demonstrates exceptional momentum, with domestic passenger vehicle sales rising to 43.02 lakh units in FY 2024-25, driven primarily by utility vehicles (27.97 lakh units) and a strong export performance (7.70 lakh units, up from 6.72 lakh units). India's infrastructure expansion, including National Highways expansion to 1,46,204 km (60 percent increase), highway construction pace acceleration from 11.6 km/day to 34 km/day, and landmark projects like the Delhi-Mumbai Expressway and Atal Tunnel, directly correlate with increased vehicle ownership and commercial vehicle demand.

The automotive wheel market directly benefits from expansion in production volume, supply chain localisation investments, and OEM capacity establishment in high-growth regions. India's expansion of the 3PL and commercial logistics sectors drives demand for commercial vehicle wheels optimised for extended duty cycles and rough road conditions.

Restraint - Raw Material Cost Volatility and Supply Chain Tariff Pressures

Commodity price volatility for aluminum and steel, combined with escalating tariff policies, creates material cost pressures that constrain the Automotive Wheel Market's profitability and investment capacity. Superior Industries International, a leading global wheel manufacturer, reported that customer order cancellations stemming from tariffs could jeopardize 33% of projected 2025 revenues, thereby contributing to significant financial distress and debt-restructuring requirements.

Tariff escalation between the U.S. and trading partners has reduced industry growth forecasts by approximately 0.7-1.2 percent annually, with particular pressure on corrosion-resistant steel and advanced component imports from Asia. Supply chain fragmentation across multiple manufacturing regions creates logistical complexity and cost unpredictability that disproportionately affect smaller manufacturers, who are unable to absorb tariff shocks or maintain diversified sourcing. Rising input costs for speciality alloys, magnesium processing, and carbon composite manufacturing are elevating production costs, while customer pricing power remains constrained by competitive markets. Many OEM customers respond to tariff-driven cost increases by consolidating wheel supplier bases, deferring adoption of premium material technologies, or shifting procurement to tariff-advantaged sourcing regions.

Opportunity - Advanced Lightweight Materials and High-Performance Composite Wheel Development

The automotive wheel market presents substantial opportunities by accelerating the adoption of advanced lightweight materials, carbon fiber composites, magnesium alloys, and hybrid designs that address emerging customer requirements for performance optimisation and weight reduction. Borbet GmbH's acquisition of Dymag Technologies exemplifies this market opportunity, expanding Borbet's portfolio to include carbon and magnesium rims and targeting the OEM and aftermarket high-performance segments.

The acquisition provides access to carbon-hybrid wheel technology, patent portfolios for advanced material integration, and production facilities that enable the scaling of lightweight wheel production. Dymag's BX-F™ carbon hybrid wheels represent next-generation technology, balancing performance, weight reduction, and manufacturing scalability for both automotive and motorcycle applications.

Subsequent strategic partnerships, including Dymag, Borbet, and Advanced International Multitech (AIM) collaboration, demonstrate market recognition of composite wheel demand. Partnership rationale emphasises DYMAG's carbon wheel expertise, BORBET's OEM positioning, and AIM's advanced manufacturing capabilities as Taiwan's largest carbon composite company, creating integrated supply solutions for global OEM integration. Research indicates carbon fiber composites deliver exceptional strength-to-weight ratios of 175 ± 25 kN·m/kg, five times stronger than steel, while substantially lighter, enabling ultra-lightweight performance wheels commanding premium pricing.

The automotive wheel market opportunity extends to magnesium wheels, which are the lightest structural metal and are particularly valuable for EV applications, reducing unsprung weight and improving handling and ride quality. Manufacturers developing cost-effective composite wheel manufacturing and achieving OEM validation will capture disproportionate margins and competitive differentiation.

Emerging Market EV Infrastructure and Commercial Vehicle Segment Expansion

Advanced manufacturing technologies and process innovations represent critical competitive opportunities, with manufacturers developing integrated production platforms delivering cost efficiency, quality consistency, and design flexibility. CITIC Dicastal's "Giga Casting" project demonstrated significant innovation potential by achieving the world's first heavy-duty integrated automotive wheel casting using China's largest two-plate high-pressure die-casting machine, thereby enabling the integration of nearly 100 components into a single casting. This transformation of traditional wheel manufacturing processes enables substantial cost reduction, weight optimisation, and production scalability. CITIC Dicastal's collaboration with major OEMs, including FAW and Leapmotor, reflects high-volume manufacturing demand for advanced casting technologies that support the scaling of EV production.

The automotive wheel market opportunity extends to aerodynamic wheel design and integrated efficiency optimisation. RONAL GROUP's collaboration with LEONHARD KURZ developed aerodynamic wheel inserts using an innovative hot-stamping process, creating lightweight, plastic-inserted wheels that enhance EV efficiency by reducing air resistance and noise. RONAL's subsequent R73 multi-spoke performance wheel launch features center-lock-style options, real carbon versions, and reduced unsprung mass, designed to improve handling, driving dynamics, and optimised performance.

Manufacturers developing integrated manufacturing platforms that combine advanced casting, hybrid material integration, aerodynamic optimisation, and digital design capabilities will achieve competitive differentiation and premium pricing power. Investment in automation, AI-enabled production optimisation, and Industry 4.0 technologies creates scalable competitive advantages.

Category-wise Analysis

Material Type Insights

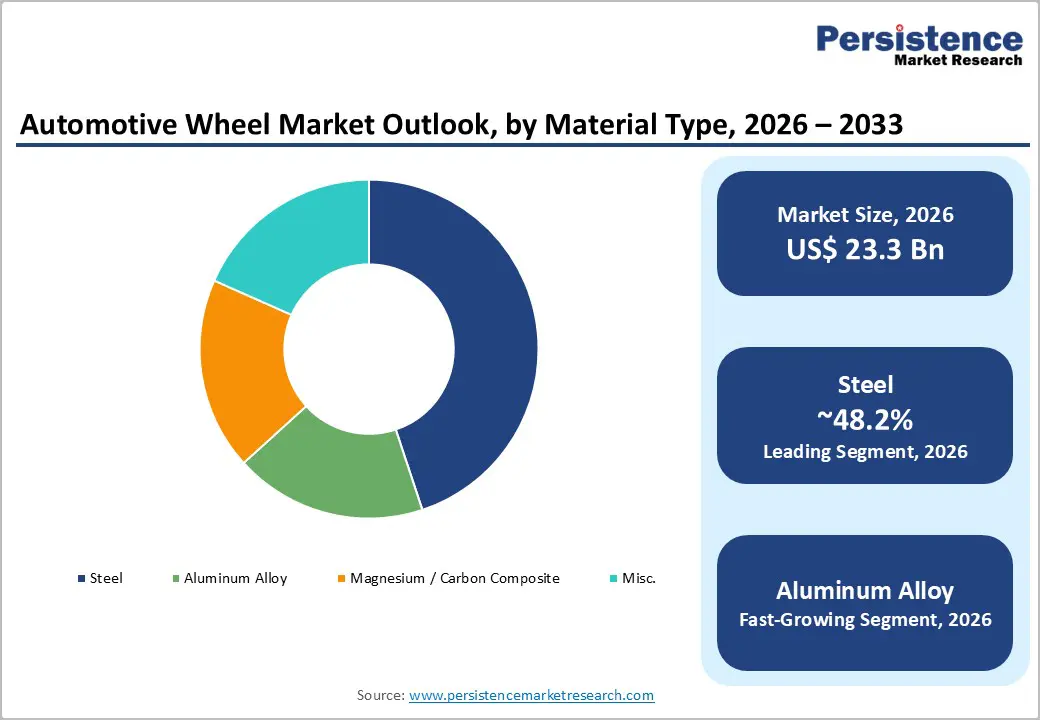

Steel wheels maintain a dominant market position, accounting for 48.2% of the global market share in 2026, reflecting a foundational cost advantage, established manufacturing infrastructure, and continued demand across the commercial vehicle, heavy-duty truck, and entry-level passenger vehicle segments. Steel wheels provide proven durability, repairability, and cost-effectiveness that are critical for price-sensitive vehicle segments and commercial fleet operators. Commercial vehicle applications, particularly heavy commercial vehicles, trucks, and buses, continue to prioritise steel wheels for towing capacity, load-bearing performance, and operational resilience across diverse road conditions.

Global commercial vehicle market dynamics support ongoing steel wheel demand, with the North America commercial vehicle market reaching 4 million units, Europe recording 2.5 million units, and Greater China maintaining 3 million units despite a 5.9% decline. Steel wheel manufacturing has achieved substantial automation and cost optimisation, enabling competitive pricing despite intensifying competition from aluminium. Regulatory decarbonization requirements and EV adoption growth are beginning to erode the steel wheel market share, as the adoption of lightweight materials becomes increasingly critical for fleet-average CO2 performance compliance.

Aluminum alloy wheels are the fastest-growing material segment, driven by EV adoption, regulatory weight-reduction incentives, and premium-vehicle segment expansion. Aluminum wheels offer 30-40 percent weight reduction versus steel, superior corrosion resistance, aesthetic appeal, and recyclability, collectively addressing emerging customer preferences and regulatory efficiency requirements. Research demonstrates that aluminum alloys 6000 and 7000 series offer excellent formability, enabling complex geometric designs supporting aerodynamic efficiency and performance optimisation critical for EV applications.

Vehicle Type Insights

Passenger cars constitute the Automotive Wheel Market's dominant end-use segment, accounting for 58.4% of the market in 2026, reflecting widespread vehicle ownership aspirations, established manufacturing infrastructure, and sustained replacement demand. Global passenger car market dynamics demonstrate resilience despite cyclical pressures, with the EU passenger car fleet reaching over 259 million registered vehicles by the end of 2024, representing a 5.9% increase since 2019.

Germany, Italy, and France remain Europe's largest markets, with over 49 million, 41 million, and 39 million cars respectively. Battery-only electric cars reached 5.9 million in 2024 across global markets, reflecting 32 percent year-over-year growth and signaling material transition intensity within passenger vehicle segments. Passenger-car electrification drives disproportionate adoption of aluminum wheels, as these wheels directly optimize EV performance, range, and operational efficiency. Premium passenger car segments, luxury brands, sports cars, and high-performance variants prioritise advanced wheel materials, including carbon composites and specialty alloys, commanding premium pricing and superior margins. This market leadership reflects sustained global passenger demand, demographic expansion in emerging markets, and continuous technology transition toward electrification.

Light commercial vehicles represent the fastest-growing vehicle end-use segment for the Automotive Wheel Market, driven by e-commerce logistics expansion, last-mile delivery requirements, and emerging market commercial vehicle adoption. Global LCV demand reflects sustained growth across regional markets, with particular strength in Asia and Latin America. India's automotive exports demonstrate particular momentum in LCVs, with two-wheeler exports surging from 34.58 lakh to 41.98 lakh units in FY 2024-25, and three-wheeler exports expanding to 3.07 lakh units, reflecting the growth of e-commerce delivery infrastructure and last-mile transport solutions. LCV electrification represents an emerging trend, with manufacturers developing electric light commercial vehicles optimised for urban delivery and short-haul logistics operations.

Regional Insights and Trends

North America Automotive Wheel Market Trends

North America represents a mature, technologically advanced market, commanding approximately 20% of the global Automotive Wheel Market share in 2026, characterised by established OEM supply chain networks, stringent regulatory requirements, and substantial investment in automotive innovation. North America's commercial vehicle market dominance demonstrates particular market significance, with 4 million units reflecting robust freight logistics, commercial transportation, and fleet modernisation investments. U.S. automotive production and sales demonstrate resilience, with U.S. car registrations reaching 12.7 million units in 2024, growing 3.1 percent from 2023 and reflecting year-end demand shifts linked to policy changes around EV incentives.

The U.S. transportation sector's US$ 2.5 trillion GDP contribution underscores automotive's economic centrality. North America's regulatory environment emphasises CO2 emissions reduction and EV adoption, with EPA Phase 3 HDV standards and multi-pollutant emissions regulations driving lightweight wheel adoption to support fleet efficiency compliance. Superior Industries' debt restructuring, converting approximately US$ 550 million of term loans into equity and reducing funded debt to US$ 125 million, reflects North American wheel market consolidation and competitive pressures.

East Asia Automotive Wheel Market Trends

East Asia represents the global Automotive Wheel Market's largest and fastest-growing region, commanding approximately 34.3% regional market share in 2026 and demonstrating exceptional growth momentum driven by manufacturing-intensive expansion, EV deployment acceleration, and emerging market vehicle ownership growth. China's automotive dominance is particularly significant: it remains the largest market, with nearly 23 million units sold, accounting for 31 percent of global car sales in 2024, and it achieved 2.6 percent growth, supported by tax incentives. CITIC Dicastal's market leadership position as China's largest aluminium wheel manufacturer and one of the largest globally underscores Asia's manufacturing capability and supply chain concentration.

The "Giga Casting" project demonstrates advanced manufacturing momentum, with integration of nearly 100-wheel components into single castings, transforming production efficiency and cost structure.

East Asia's estimated annual growth rates range from 7-10 percent, substantially exceeding global averages, reflecting structural manufacturing expansion, emerging market vehicle ownership democratisation, and EV adoption acceleration, particularly in Chinese and Indian markets.

Europe Automotive Wheel Market Trends

Europe represents a mature, technologically sophisticated market commanding approximately 24% of the global Automotive Wheel Market share in 2026, characterised by stringent environmental regulations, advanced manufacturing standards, and substantial renewable energy and EV infrastructure investment. The EU passenger car fleet expanded to 259 million registered vehicles by the end of 2024, representing 5.9 percent growth since 2019, with Germany, Italy, and France accounting for the largest markets. EU regulatory frameworks establish particularly stringent CO2 reduction mandates, with Fit for 55 standards requiring 55 percent CO2 reductions for new cars and zero-carbon sales mandates beginning in 2035.

These regulations directly drive the adoption of lightweight wheels, with aluminium and specialty composite materials capturing a larger market share. EU new car registrations reached 10.6 million units in 2024, up 0.8 percent from 2023, with Spain demonstrating the strongest regional performance (+7.1 percent), while Germany (-1 percent), France (-3.2 percent), and Italy (-0.5 percent) experienced declines. Van registrations increased 8.3% to 1.6 million units, driven by e-commerce logistics expansion and commercial delivery optimisation.

The European Union's emphasis on circular economy and environmental compliance requirements create market preference for aluminium wheels that offer superior recyclability, corrosion resistance, and sustainability performance. European regional growth projections range from 5.1 to 6.2 percent annually, reflecting market maturity, strong EV adoption momentum, regulatory decarbonisation requirements, and commercial vehicle segment expansion, which support logistics infrastructure modernisation.

Competitive Landscape

The global automotive wheel market is moderately consolidated, dominated by a few large multinational manufacturers while still having numerous smaller regional players. Leading companies such as Enkei Corporation, Ronal Group, BBS GmbH, Iochpe-Maxion SA, CITIC Dicastal (CITIC Group), and Alcoa Wheels (Howmet Aerospace) hold significant market share, supplying both OEMs and the aftermarket globally. These top players compete on material innovation, lightweight designs, and cost efficiency, especially for passenger cars, commercial vehicles, and electric vehicles. While the top tier exhibits oligopolistic characteristics, the market remains fragmented at regional and niche levels, with smaller firms catering to specialised demands. Strategic collaborations, acquisitions, and global supply networks further strengthen the position of the leading manufacturers.

Key Developments

- On 3 November 2025, Iochpe-Maxion (Maxion Wheels) announced a strategic expansion of its light vehicle aluminum wheels business in South America. The company redeployed existing global assets to its Brazilian plants and acquired a 50.1% stake in Polimetal, Argentina, to increase production capacity. This initiative addresses the growing demand for aluminum wheels in the Mercosur region, strengthens OEM supply chains, and positions Maxion Wheels to capture rising market share in the South American passenger car segment.

- On 8 December 2025, Superior Industries International, Inc. completed an acquisition by a group of its term loan investors, including Oaktree Capital Management, converting a portion of debt into equity and strengthening its balance sheet. The transaction positions Superior for long-term growth in the global wheel industry, allowing increased investment in operations, customer relationships, and regional supply capabilities, while also appointing Michael Dorah as the new CEO to lead the company’s strategic expansion.

Companies Covered in Automotive Wheel Market

- Enkei Corporation

- Ronal Group

- BBS GmbH

- Iochpe-Maxion SA

- CITIC Dicastal (CITIC Group)

- Superior Industries International Inc.

- Accuride Corporation

- Maxion Wheels

- Steel Strips Wheels Ltd.

- Alcoa Wheels (Howmet Aerospace)

- Carbon Revolution Ltd.

- RAYS Co., Ltd.

- Central Motor Wheel of America, Inc.

- Topy Industries Ltd.

- Euromax Wheel

Frequently Asked Questions

The global automotive wheel market is projected to be valued at US$ 50.3 Bn in 2026.

The steel segment is expected to account for approximately 48.2% of the global automotive wheel market by Material Type in 2026.

The automotive wheel market is expected to witness a CAGR of 5.6% from 2026 to 2033.

The automotive wheel market growth is driven by global vehicle electrification and lightweight material adoption to improve EV range, coupled with expanding automotive production, regional manufacturing growth, and rising vehicle ownership in emerging markets.

Key opportunities in the automotive wheel market lie in advanced lightweight and composite material adoption (carbon fiber, magnesium, hybrid designs), OEM-focused high-performance wheel development, aerodynamic efficiency solutions for EVs, and manufacturing innovations such as giga-casting and automated composite production.

Key players in the automotive wheel Market include Enkei Corporation, Ronal Group, BBS GmbH, Iochpe‑Maxion SA, CITIC Dicastal (CITIC Group), and Alcoa Wheels (Howmet Aerospace).