- Semiconductor Materials & Components

- Automotive Tuner ICs Market

Automotive Tuner ICs Market Size, Share, and Growth Forecast, 2026 – 2033

Automotive Tuner ICs Market by Tuner Type (AM/FM Tuners, DAB Tuners, Satellite Radio Tuners, Hybrid/SDR Tuners), Application (OEMs, Infotainment Systems, Aftermarket Radios, Navigation Units, In-Vehicle Entertainment), Vehicle Type (Passenger Cars, LCVs, HCVs, EVs), and Regional Analysis for 2026-2033

Automotive Tuner ICs Market Share and Trends Analysis

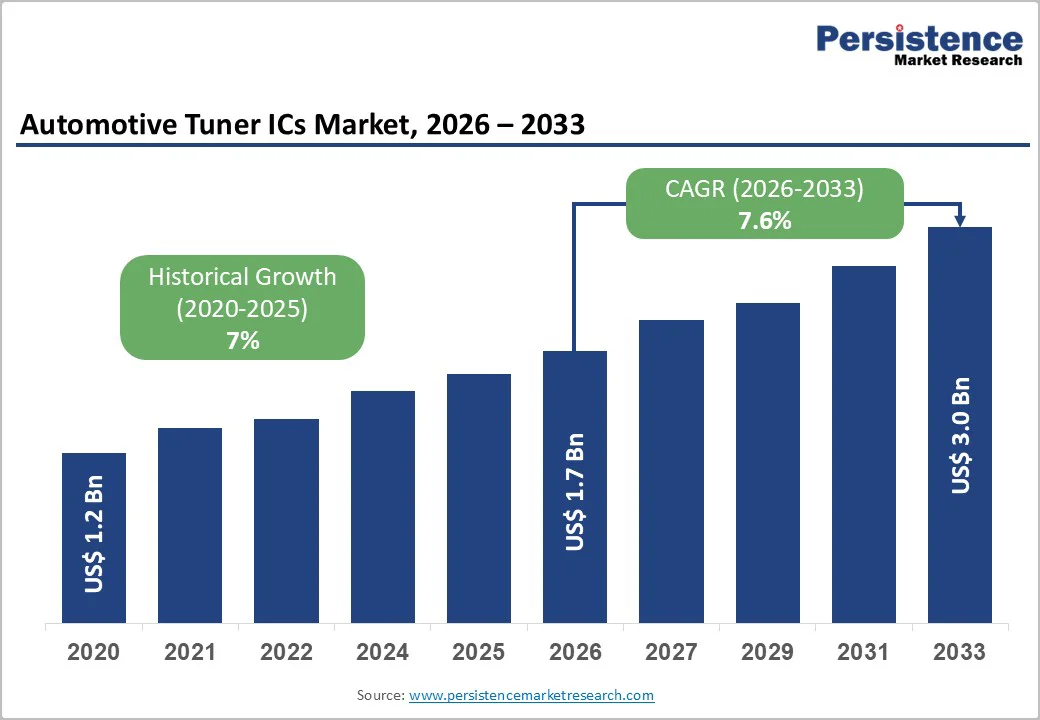

The global automotive tuner ICs market size is likely to be valued at US$ 1.7 billion in 2026 and is estimated to reach US$ 3.0 billion by 2033, growing at a CAGR of 7.6% during the forecast period 2026−2033. The expansion of the market is primarily propelled by the increasing integration of advanced infotainment systems into vehicles, a broad-based transition to digital broadcasting standards, and the accelerating adoption of electric vehicles (EVs), all of which demand more sophisticated electronic components.

This sustained growth is further underpinned by key technological advancements that enhance the capabilities and value of tuner ICs. Ongoing innovation in software-defined radio tuners provides automakers with greater flexibility and the ability to update system functionalities over time. Furthermore, the development of ICs that support multiple standards is crucial, as it enables a single component to function seamlessly across various regional broadcasting formats. These innovations are essential for meeting long-term volume demand and supporting the evolution of connected, feature-rich automotive platforms.

Key Industry Highlights

- Dominant Region: Asia Pacific is projected to capture a 45% market share by 2026, fueled by extensive automotive production and robust original equipment manufacturer (OEM) and supplier networks.

- Fastest-growing Regional Market: Asia Pacific is positioned to be the fastest-growing market through 2033, driven by widespread EV adoption and supportive policies for clean mobility.

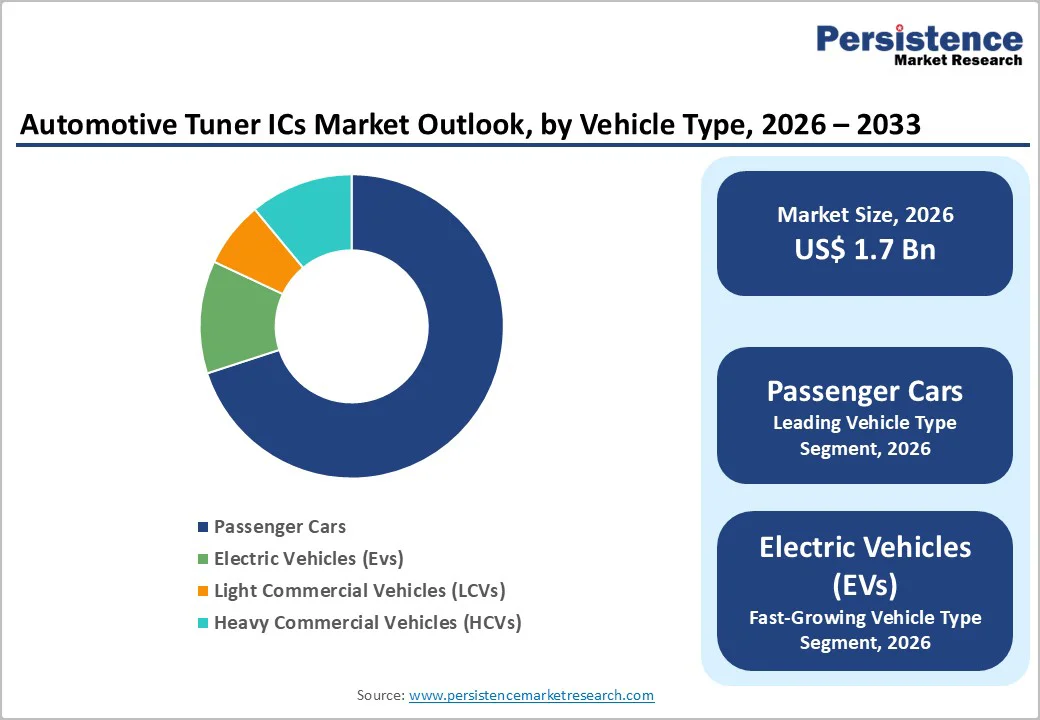

- Leading Vehicle Type: Passenger cars are likely to hold a 70% market share by 2026, driven by high sales, urban mobility trends, and premium infotainment features.

- Fastest-growing Vehicle Type: EVs are expected to grow the fastest through 2033, owing to rising EV adoption and expanding charging infrastructure.

| Key Insights | Details |

|---|---|

| Automotive Tuner ICs Market Size (2026E) | US$ 1.7 Bn |

| Market Value Forecast (2033F) | US$ 3.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 7% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growing Demand for Advanced Infotainment Systems

Drivers today expect vehicles to deliver sophisticated entertainment and connectivity experiences, and this preference is fundamentally reshaping demand for advanced tuner integrated circuits (ICs). Modern infotainment systems consolidate radio reception, music streaming, navigation, and voice control into seamless platforms that demand ICs capable of processing multiple signals concurrently without compromising audio fidelity or network reliability. As consumer expectations for frictionless in-car digital interactions continue to rise, automakers increasingly adopt high-performance tuner ICs that deliver crystal-clear sound, actively suppress background noise, and operate across diverse frequency bands. This shift reflects a strategic recognition that infotainment quality has become a meaningful differentiator in how buyers evaluate vehicle sophistication and overall value proposition.

The competitive landscape reinforces the importance of tuner ICs as a technology linchpin for automotive differentiation. Vehicles featuring advanced infotainment systems command premium positioning in consumer perception and directly influence purchase intent, compelling manufacturers to prioritize IC capabilities that handle intricate signal processing, function flawlessly with next-generation software architectures, and embrace emerging wireless communication standards. This technical elevation transforms tuner ICs from commodity components into strategic assets within the broader vehicle electronics ecosystem. The market operates within a self-reinforcing dynamic: consumer demand drives automakers to implement more sophisticated infotainment architecture, which in turn creates sustained demand for dependable, feature-rich tuner solutions that can evolve alongside rapidly changing in-car entertainment ecosystems and connectivity requirements.

High Development and Integration Costs

High development and integration costs stem from the complexity of designing tuner integrated circuits that can reliably handle multiple frequency bands, signal types, and interference conditions. The engineering process demands advanced semiconductor materials, precision circuit design, and rigorous testing to ensure compatibility with various automotive systems. Achieving high sensitivity, minimal noise, and robust performance under varying environmental conditions requires substantial investment in research, prototyping, and validation. Integration into the vehicle’s broader electronic architecture further increases costs, as it necessitates custom interfaces, firmware development, and compliance with stringent automotive safety and electromagnetic compatibility standards.

The financial burden extends to the production and deployment stages, where low defect tolerance and high-quality requirements increase manufacturing costs. Automakers and suppliers face trade-offs between functionality, reliability, and cost efficiency, which can limit adoption in cost-sensitive vehicle segments. Scaling production without compromising performance demands specialized manufacturing processes and quality control measures, reinforcing the high entry barriers for new entrants. These factors constrain profitability and slow widespread implementation, making cost management a critical consideration for stakeholders aiming to deliver sophisticated yet economically viable solutions.

Hybrid and Software-Defined Radio (SDR) Tuners

Hybrid and software-defined radio (SDR) tuners represent a transformative opportunity because they integrate multiple radio standards into a single, flexible platform. Traditional tuners rely on fixed hardware for specific frequency bands, limiting adaptability as new standards emerge. Hybrid and SDR tuners allow seamless reception of AM, FM, DAB, and satellite signals through programmable software, reducing the need for multiple discrete components. This flexibility enhances vehicle infotainment experiences, enabling manufacturers to deliver richer audio, data services, and connected features that align with evolving consumer expectations.

The shift toward hybrid and SDR tuners also supports cost efficiency and scalability. By consolidating functionality into fewer integrated circuits, vehicle manufacturers can streamline design, reduce weight, and lower production complexity. Software updates can extend the system's lifecycle, allowing vehicles to support future communication protocols without hardware changes. This capability aligns with the automotive industry's push toward smarter, connected vehicles and enhances brand differentiation. The combination of adaptability, efficiency, and future readiness positions hybrid and SDR tuners as a strategic lever for automotive electronics innovation.

Category-wise Analysis

Tuner Type Insights

AM/FM tuners are projected to hold a 55% market share in 2026, marking their leading position. Their widespread compatibility across all vehicle types and cost-effective implementation drive this dominance. They provide reliable performance even in challenging environments with signal interference, making them a preferred choice for OEMs. Legacy vehicle fleets continue to rely on AM/FM tuners, ensuring sustained demand. Mainstream automakers such as Toyota and Ford integrate these tuners into economy and mid-range models for dependable audio functionality.

Hybrid and software-defined tuners are set to emerge as the fastest-growing segment between 2026 and 2033, driven by the shift toward connected and electric vehicles. Their adaptability to advanced software architectures and 5G-enabled infotainment systems allows automakers to offer seamless digital experiences. Premium carmakers, including BMW and Tesla, are increasingly adopting these tuners to enhance connectivity, streaming, and in-car intelligence. The segment’s growth is also supported by reductions in production costs and the ability to scale across multiple vehicle platforms, making hybrid tuners an attractive option for innovation-focused OEMs.

Application Insights

OEM infotainment systems are projected to hold 65% of the revenue share of the automotive tuner ICs market in 2026, driven by growing demand for connected and smart vehicle experiences. Their widespread integration in new vehicles ensures strong market presence and stable revenue through high-volume OEM contracts. These systems provide seamless connectivity, intuitive user interfaces, and enhanced safety integration. For example, combining infotainment with advanced driver-assistance systems (ADAS) improves reliability and overall system performance. Automakers leverage OEM platforms to deliver consistent, high-quality in-car experiences across multiple vehicle models.

In-vehicle entertainment systems are estimated to be the fastest-growing segment from 2026 to 2033, powered by rising consumer demand for rear-seat multimedia and streaming experiences in family and electric vehicles. Automakers are equipping vehicles with advanced rear-seat displays, connectivity solutions, and scalable software platforms to enhance passenger engagement and comfort. Premium carmakers are rapidly adopting these systems to differentiate their offerings and improve the in-car experience. Integration with vehicle networks, flexible content delivery, and adaptable hardware accelerate adoption, positioning in-vehicle entertainment as a key innovation and growth driver in automotive infotainment.

Vehicle Type Insights

Passenger cars are expected to hold a 70% market share in 2026. Their dominance is boosted by strong urban mobility trends and high annual sales volumes. Feature-rich trims and enhanced infotainment packages further drive the uptake of premium tuners in this segment. Automakers continue to integrate advanced audio and connectivity solutions in passenger cars to meet consumer expectations for comfort, convenience, and entertainment, ensuring sustained demand and stable revenue streams across global markets.

Electric vehicles are expected to be the fastest-growing segment through 2033, driven by increasing EV adoption and the integration of advanced infotainment systems. As automakers expand EV lineups, consumers demand connected, feature-rich audio and tuner solutions to complement smart vehicle technologies. Premium EV models are increasingly equipped with hybrid and software-defined tuners to enhance in-car experiences. Policy support, infrastructure growth, and declining battery costs further accelerate EV penetration, positioning this segment as a key driver of future growth and innovation in the automotive tuner market.

Regional Insights

North America Automotive Tuner ICs Market Trends

Tuner IC deployment in North America's automotive sector prioritizes harmonized standards, environmental sustainability, and operational reliability. OEMs and tier-1 suppliers develop highly modular, software-defined architectures for connected and autonomous vehicles that require advanced tuner and radio-frequency (RF) components. Dense networks of semiconductor designers, telematics specialists, and automotive engineers collaborate to create bespoke infotainment and V2X (vehicle-to-everything) solutions. Strong intellectual property regimes and robust R&D ecosystems enable iterative optimization of components, allowing rapid adaptation to evolving regulatory frameworks and multi-standard communication protocols. This synergy of engineering rigor and platform-level design precision drives technological leadership in automotive electronics.

Operational complexity and strategic cost management shape market dynamics in North America. Elevated manufacturing costs, rigorous certification processes, and multi-layered compliance requirements create challenges for the mass deployment of advanced components. Close collaboration with foundries, software developers, and systems integrators ensures performance, interoperability, and scalability. Prioritization of advanced customization and ecosystem-driven co-engineering sustains technological differentiation. Meticulous engineering, regulatory agility, and strategic partnerships support the delivery of high-value, technically sophisticated vehicle electronic solutions.

Europe Automotive Tuner ICs Market Trends

The European automotive tuner IC market is shaped by standardization, sustainability, and high reliability in tuner IC deployment. OEMs and tier-1 suppliers focus on integrating multi-band tuners that support diverse radio standards and advanced connectivity protocols, meeting the needs of both legacy fleets and modern connected vehicles. Research clusters in Germany, France, and the Nordics optimize tuner IC architectures for electromagnetic compatibility, thermal stability, and interference resilience. Policy initiatives promoting digital radio adoption, low-emission mobility, and smart transportation infrastructure create a favorable environment for innovation. Collaboration between manufacturers and semiconductor firms accelerates development cycles and deployment of advanced tuner IC solutions across vehicle segments.

Market dynamics in Europe are shaped by regulatory rigor, quality assurance, and cross-border coordination. Certification procedures, strict safety standards, and harmonized communication protocols require highly reliable and future-proof tuner IC designs. Investment in modular and scalable IC architectures supports adoption across electric, hybrid, and conventional vehicles. Alignment with standardization bodies ensures interoperability and compliance, while advanced testing frameworks mitigate operational risks. Precision engineering, regulatory alignment, and structured innovation networks enable the delivery of technically sophisticated and performance-driven tuner IC solutions.

Asia Pacific Automotive Tuner ICs Market Trends

By 2026, the Asia Pacific is expected to lead with an estimated 45% of the automotive tuner ICs market share, propelled by its vast automotive manufacturing base in China, Japan, South Korea, and India. High vehicle volumes, advanced infotainment integration, and a strong presence of both OEMs and domestic suppliers create an efficient ecosystem for design, prototyping, and production. Rising urbanization, growing middle-class demand for connected vehicles, and supportive government policies for digital broadcasting and smart mobility are accelerating the adoption of tuner ICs across passenger and commercial vehicles, reinforcing the region’s dominant market position.

Asia Pacific is also poised to be the fastest-growing market for automotive tuner ICs during the 2026-2033 forecast period, driven by strategic factors beyond production scale. Aggressive electrification in China and high EV adoption increase demand for advanced electrical/electronic (E/E) architectures, requiring sophisticated tuner ICs for infotainment, telematics, and V2X communications. Supportive government policies for digital radio, smart mobility, and 5G connectivity accelerate IC adoption across vehicle platforms. Advanced semiconductor ecosystems, including wafer fabs, packaging, and R&D centers, enable cost-efficient production and customization for regional OEMs. Software-defined automotive systems and connected vehicle technologies enhance in-car experiences and future-proof vehicles.

Competitive Landscape

The global automotive tuner ICs market landscape is characterized by moderate concentration, with major players such as NXP Semiconductors, Texas Instruments, Infineon Technologies, and STMicroelectronics commanding approximately 60% of total revenue. These leaders achieve their position through robust partnerships with OEMs and by delivering multi-standard tuner platforms, advanced digital broadcast capabilities, and software-defined solutions. Their continued investment in innovation, distinctive feature sets, and responsiveness to shifting vehicle connectivity needs allows them to maintain a strong competitive edge and shape market trends.

Beyond the leading suppliers, a range of regional and specialized manufacturers meets aftermarket requirements, ensuring broad coverage across various vehicle segments. The industry faces high barriers to entry, including the necessity for automotive-grade qualification, stringent testing protocols, and large-scale supply chain capabilities. These factors reinforce market concentration but also open doors for strategic collaborations and regionally focused approaches. As a result, the market environment continues to reward technological differentiation and close alignment with OEM priorities, shaping a landscape where both global and regional players contribute to advancing automotive tuner IC solutions.

Key Industry Developments

- In December 2025, Infineon Technologies extended its CoolSiC™ MOSFET 750 V G2 family with new packages (Q-DPAK and D2PAK) featuring ultra-low on-state resistance (RDS(on)) values ranging from 4 milliohms to 60 milliohms, designed for automotive onboard chargers, high-voltage DC-DC converters, and industrial power applications. The technology delivers superior efficiency and power density through optimized thermal performance, reduced switching losses, and enhanced gate driving capabilities.

- In October 2025, Tesla announced that its 2026 entry-level Model Y Standard and Model 3 Standard trims will eliminate both AM and FM radio tuners entirely, making Tesla the first mainstream automaker to remove terrestrial radio completely from base models. The decision reflects Tesla's strategy to rely on Bluetooth connectivity for mobile device pairing and premium connectivity for cellular-enabled music streaming through native applications.

- In April 2025, Texas Instruments introduced new automotive semiconductor solutions, including the LMH13000 integrated lidar laser driver featuring an 800-picosecond rise time that extends detection distance by up to 30% while reducing system size by four times and costs by approximately 30%. The company also launched the AWR2944P mmWave radar sensor with enhanced signal-to-noise ratio, memory capacity, and integrated hardware acceleration for advanced edge AI processing, alongside industry-first bulk acoustic wave (BAW)-based automotive clocks.

Frequently Asked Questions

The global automotive tuner ICs market is projected to reach US$ 1.7 billion in 2026.

Increasing demand for connected infotainment systems, multi-standard radio support, and integration with advanced vehicle communication technologies are driving the market.

The market is poised to witness a CAGR of 7.6% from 2026 to 2033.

Growing adoption of connected and autonomous vehicles, rising demand for multi-standard and software-defined tuner ICs, and expansion into emerging automotive markets are key opportunities.

Some of the key market players include NXP Semiconductors, Texas Instruments, Infineon Technologies, STMicroelectronics, and Analog Devices.