- Automotive Components & Materials

- Automotive Seats Market

Automotive Seats Market Size, Share, and Growth Forecast, 2026 - 2033

Automotive Seats Market: by Material Type (Genuine Leather, Synthetic Leather, Fabric, and Others), Technology (Standard (Manual) Seats, Powered Seats, Comfort and Others), Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Electric Vehicles) Seat Type, and Regional Analysis for 2026 - 2033

Automotive Seats Market Size and Trends Analysis

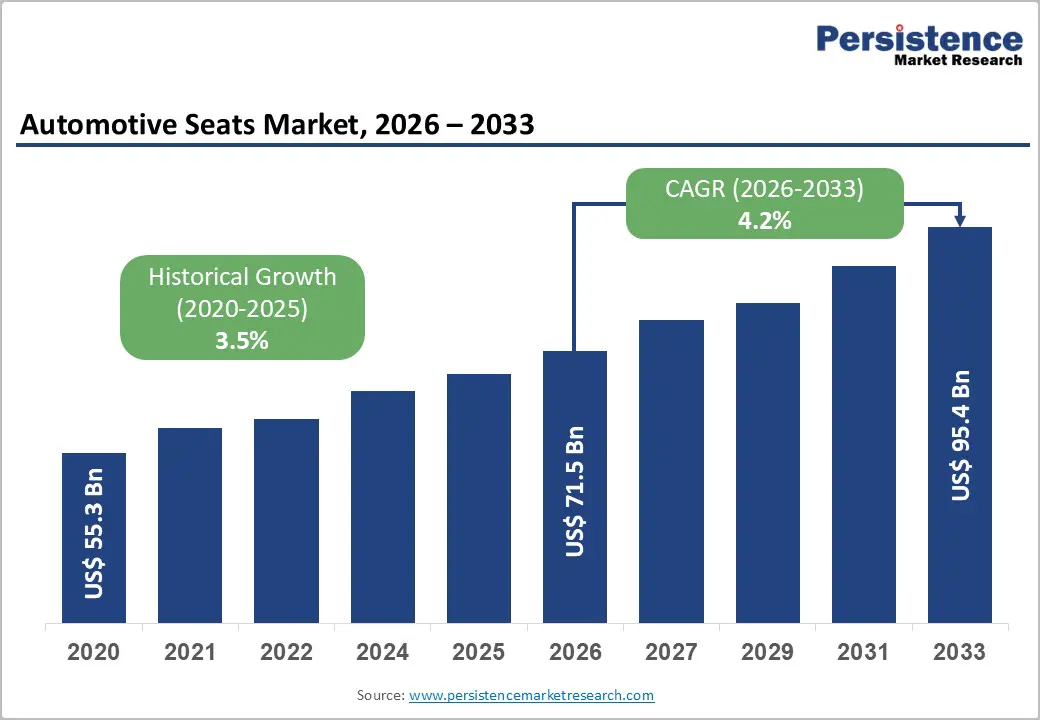

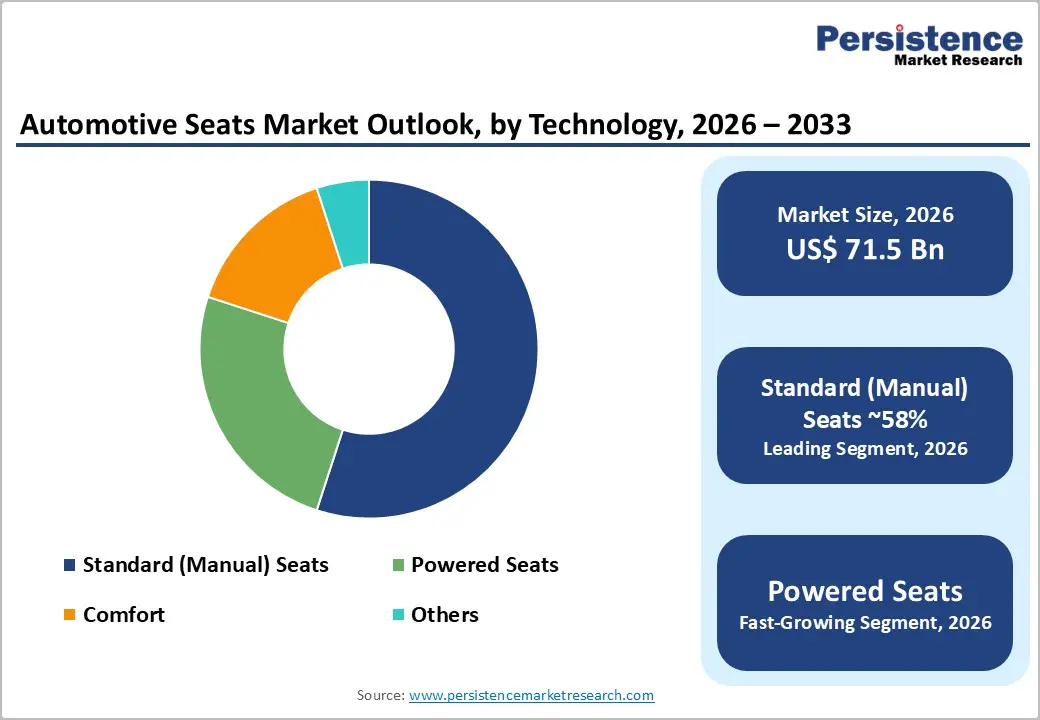

The global automotive seats market size is likely to be valued at US$ 71. billion in 2026 and is projected to reach US$ 95.4 billion by 2033, growing at a CAGR of 4.2% between 2026 and 2033.

The automotive seats market is experiencing sustained expansion driven by accelerating electric vehicle (EV) adoption, with 17 million units sold globally in 2024 and projections exceeding 20 million units in 2026, coupled with rising consumer demand for advanced comfort technologies, including heated, ventilated, and massage seats, and increasing vehicle production across developed and emerging markets.

Key Industry Highlights:

- Electric Vehicle Seating Dominance: EV seats segment expanding at 13.4% CAGR, substantially outpacing overall market growth, with 17 million EV units sold in 2024 establishing foundational demand for specialized EV seating architectures incorporating lightweight materials, thermal management, and premium comfort features.

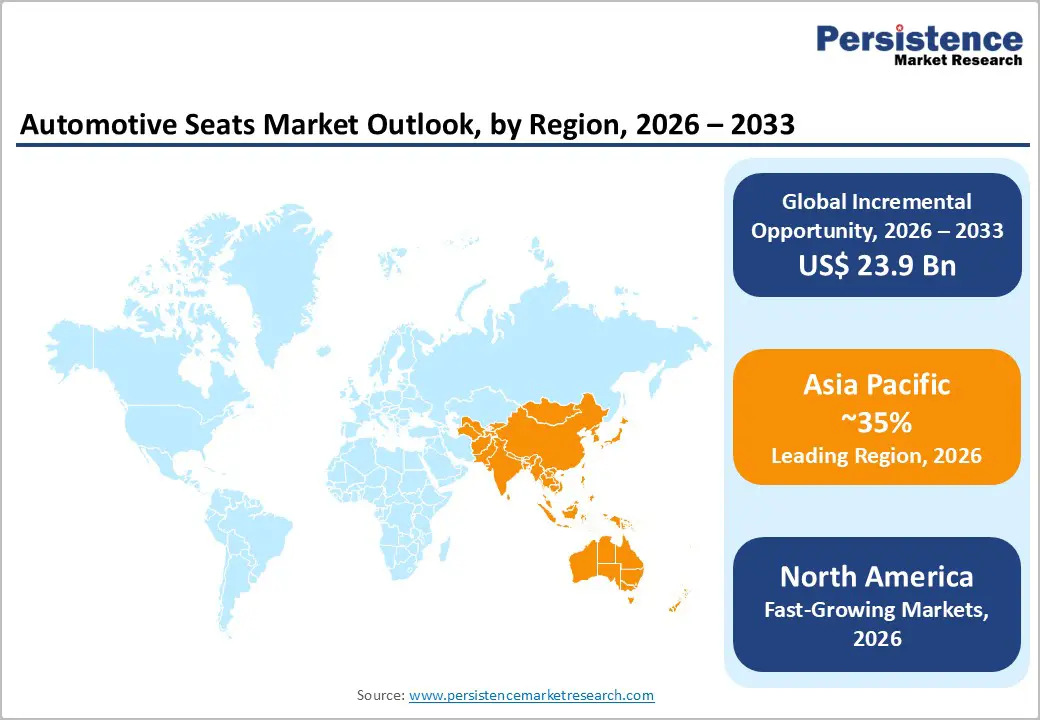

- Asia Pacific Regional Leadership: Asia Pacific commanding 35.4% market share with 3.8% CAGR, driven by China's EV market dominance at 45% EV penetration, India's rapid vehicle production growth, and emerging middle-class consumer expansion, creating the largest growth opportunity region through 2033.

- Powered Seating Technology Acceleration: Powered seats segment expanding at 8% CAGR, transitioning from luxury-exclusive to mid-range standard offering, with thermal comfort systems growing at 10.4% CAGR, representing the fastest-growing technology sub-segment driven by EV adoption, eliminating traditional engine waste heat.

- Sustainable Materials Transformation Opportunity: Vegan leather and bio-based materials expanding at 9% CAGR, with premium segment adoption driven by environmental consciousness and OEM decarbonization commitments, establishing USD 8 billion incremental market opportunity through sustainable seat material integration by 2033.

| Key Insights | Details |

|---|---|

|

Automotive Seats Market Size (2026E) |

US$ 71.5 Bn |

|

Market Value Forecast (2033F) |

US$ 95.4 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.5% |

Market Dynamics

Drivers - Rising Demand for Powered, Ventilated, and Comfort-Focused Seating Technologies

Consumer preference for advanced seat comfort features is expanding substantially, with 78% of Indian car owners surveyed identifying ventilated seats as must-have feature (April 2026 Park+ Research Labs survey), surpassing sunroofs, ADAS, and infotainment systems in consumer prioritization. Powered seat market expanding at 5.7% CAGR reflects growing OEM integration across mid-range and premium segments, with 6-way power adjustment, lumbar support, and memory functions becoming industry standards rather than luxury differentiators. Thermal comfort systems including heating, ventilation, and cooling (HVAC) functionality represent highest-growth segment with 10.4% CAGR, driven by EV adoption eliminating traditional waste heat from engines requiring active thermal management systems for cabin comfort. Seat massage systems projected to expand from USD 121.2 million in 2026 demonstrate premium segment growth trajectory with 15% CAGR for smart seat technologies, particularly in luxury and autonomous vehicle segments where extended occupancy durations justify advanced comfort investments.

Accelerating Electric Vehicle Adoption and Premium Interior Differentiation Requirements

Electric vehicle sales momentum, reaching 17 million units in 2024 with year-over-year growth of 25%, creates substantial demand for specialized seating architectures designed specifically for EV platforms. EV seats command price premiums of 15% compared to traditional internal combustion engine (ICE) vehicles due to integration of advanced features including thermal management systems, lightweight composite frames, and premium material finishes.

EV manufacturers including Tesla, BYD, Nio, and emerging OEMs prioritize seat quality as primary differentiator for consumer perception and premium positioning, establishing EV seats market growing at 13.4% CAGR (significantly above overall automotive seats market growth). Energy efficiency requirements mandate lightweight seat frame construction by reducing vehicle weight by 2-4 kg per seat, directly improving EV driving range by 5-7% and battery utilization efficiency.

Restraint-Volatility in Raw Material Prices

The automotive seats market is significantly impacted by fluctuations in raw material prices, particularly steel, aluminum, polyurethane foam, plastics, and leather. Seat structures rely heavily on metal frames; while cushioning and trim materials are sensitive to petrochemical price movements. Sudden increases in input costs directly pressure supplier margins, especially as OEMs often operate under long-term contracts with limited pricing flexibility. While large Tier-1 suppliers can partially offset cost volatility through scale advantages and vertical integration, smaller suppliers face profitability challenges. Additionally, sustainability-driven shifts toward recycled and bio-based materials can initially increase costs due to limited supply and higher processing complexity. Persistent raw material volatility creates uncertainty in production planning and pricing strategies, restraining overall market growth and discouraging aggressive capacity expansion.

High Design Complexity and Development Costs

Modern automotive seats are among the most complex interior components, integrating mechanical, electrical, electronic, and safety systems. Features such as power adjustment, heating and ventilation, airbags, occupancy sensors, and memory modules significantly increase design and validation complexity. Meeting stringent crash safety, durability, and regulatory standards requires extensive testing, driving up development costs and lengthening time-to-market. This complexity is further amplified by OEM demands for model-specific customization and rapid platform refresh cycles. For suppliers, high upfront R&D investment and tooling costs raise entry barriers and limit participation to well-capitalized Tier-1 players, constraining competitive intensity and slowing innovation adoption across lower vehicle segments.

Opportunity - Sustainability and Lightweight Material Innovation

Sustainability is emerging as a major opportunity in the automotive seats market as OEMs face increasing pressure to reduce vehicle lifecycle emissions. Seat manufacturers are investing in lightweight structures, recycled materials, bio-based foams, and natural-fiber composites to meet environmental targets. Sustainable seating solutions not only reduce vehicle weight but also help OEMs comply with upcoming lifecycle and circular economy regulations.

Innovations such as mono-material seat designs, recyclable covers, and reduced foam usage improve end-of-life recyclability and lower carbon footprints. OEMs increasingly prefer suppliers that can demonstrate measurable sustainability benefits, creating competitive advantages for early adopters. While sustainable materials may initially increase costs, scale adoption and regulatory incentives are expected to improve economics over time.

Rising Demand for Smart and Wellness-Oriented Seating

Consumer interest in health, comfort, and personalization is creating strong growth opportunities for smart seating technologies. Features such as massage functions, posture monitoring, climate-controlled seating, active noise reduction, and integrated air-purification systems are gaining traction, particularly in premium and mid-segment vehicles. Advances in sensors, software, and connectivity enable seats to adapt dynamically to occupant preferences and driving conditions. As autonomous driving technologies progress, seats are expected to play an even greater role in passenger comfort and interior flexibility. This shift transforms seats into value-added systems rather than cost-driven components, allowing suppliers to command higher margins and strengthen strategic partnerships with OEMs.

Category-wise Analysis

Product Type Material Insights

Genuine Leather represents the dominant material segment commanding 43.4% market share, driven by premium vehicle segment concentration, superior durability characteristics, and luxury positioning. Genuine leather seats command price premiums of 40-60% versus synthetic alternatives, with premium OEMs including Mercedes-Benz, BMW, Audi, and Porsche standardizing leather interiors across vehicle lineups. Leather material advantage derives from aging characteristics improving aesthetic appeal over vehicle lifespan, superior tactile properties, and established consumer perception associating genuine leather.

Fabric segment emerges as fastest-growing material category with estimated 6% CAGR, driven by cost-effectiveness versus genuine leather, maintenance ease, and diverse aesthetic options particularly in economy and mid-range vehicle segments. Fabric seats offer manufacturer flexibility for rapid design, iteration, color customization, and pattern diversity supporting brand differentiation strategies.

Technology Application Insights

Standard (Manual) Seats command dominant positioning representing 58.3% market share, reflecting cost-sensitive consumer segments and emerging market vehicle configurations where manual adjustment mechanisms remain economically optimal. Standard seat prevalence particularly concentrated in budget vehicle segments, commercial vehicle categories, and developing economy markets where feature-to-cost ratios justify simpler mechanical architectures.

Powered seats represent fastest-growing technology segment with estimated 7% CAGR, driven by increasing mid-range vehicle adoption of 6-way and multi-directional power adjustment mechanisms, lumbar support systems, and memory functions. Powered seat market expansion reflects consumer expectation evolution as advanced comfort features transition from luxury-exclusive to mid-range standard offerings. Growth trajectory accelerated by EV adoption where digital control integration facilitates advanced power seat functionality integration with vehicle electronics architecture.

Vehicle Type Insights

Passenger Vehicles maintain dominant positioning commanding 58.4% market share, driven by higher production volumes, premium feature content, and consumer comfort prioritization. Passenger car segment growth at 3.66% CAGR reflects sustained demand from SUV and crossover segment expansion, with SUVs representing 54% of total passenger vehicle sales, requiring enhanced seating architectures supporting multi-row configurations and increased per-vehicle seat content.

Electric Vehicles represent fastest-growing segment with 13.4% CAGR substantially exceeding overall market growth rate, driven by specialized EV seating requirements, premium customer expectations, and emerging OEM differentiation strategies. EV market expansion from 17 million units in 2024 to 20+ million units in 2026 establishes structural demand growth supporting incremental market opportunity of USD 4 billion by 2033.

Seat Type Configuration Insights

Bench/Split-Bench Seats command dominant positioning representing 48.5% market share, reflecting prevalence across passenger cars, commercial vehicles, and budget-segment vehicles where bench configurations optimize interior space utilization and manufacturing simplicity.

Bucket Seats emerge as fastest-growing segment with estimated 5.8% CAGR, driven by consumer preference for individual seating ergonomics, luxury aesthetic positioning, and enhanced comfort perception. Bucket adoption expanding particularly in premium vehicles, SUVs, and performance-oriented segments where lateral support, individual adjustment capabilities, and sporty positioning support premium brand differentiation strategies. Bucket seat growth acceleration reflects emerging consumer expectations for individualized seating experiences supporting market expansion opportunity.

Regional Insights

North America Automotive Seats Market Trends

North America, representing approximately 24.3% of global automotive seats market share, demonstrates highest regional growth rate at estimated 4.5% CAGR driven by strong consumer preference for premium seating features, advanced comfort technologies, and vehicle customization. United States market dominance, supported by major OEM headquarters including Ford, General Motors, Tesla, and automotive suppliers, establishes innovation ecosystem concentration supporting technology advancement and early feature adoption.

Consumer demand for heated, ventilated, and massage seats concentrated in North American market, reflecting climate diversity (cold winters requiring heating, hot/humid summers driving ventilation demand) and disposable income levels supporting premium feature adoption. Electric vehicle penetration in North America, reaching 8-12% of new vehicle sales in 2024, drives premium seating demand particularly from Tesla, Chevrolet (Bolt EV), and emerging EV manufacturers targeting premium consumer segments.

Europe Automotive Seats Market Trends

Europe commands approximately 21% global market share with sustained growth of 3.8% CAGR driven by strict vehicle emission regulations driving EV adoption, premium brand concentration, and consumer environmental consciousness. Germany, United Kingdom, France, and Spain collectively represent 75%+ of European market value, with German OEM concentration (Mercedes-Benz, BMW, Audi, Porsche) establishing premium seating content expectations across vehicle segments.

European regulatory focus on sustainability including EU General Safety Regulation (GSR) mandates and circular economy initiatives drives adoption of recyclable and bio-based seat materials, with major OEMs committing to 100% recyclable seat content by 2030. Electric vehicle adoption in Europe reaching 22% of new vehicle sales in 2024, highest globally among major regions, creates concentrated demand for premium EV seating solutions. Regulatory harmonization across EU member states enables efficient manufacturing scale supporting competitive cost structures despite premium material specifications.

Asia Pacific Automotive Seats Market Trends

Asia Pacific dominates global automotive seats market commanding 35.4% market share, with strongest regional growth projection of 4.0% CAGR, driven by massive vehicle production concentration in China, Japan, and India, rapid middle-class population expansion, and rising disposable income enabling premium feature adoption. China's automotive market, comprising 28% of global production, demonstrates EV leadership with 45% projected EV penetration in new vehicle sales by 2026, creating concentrated demand for specialized EV seating architectures.

India's emerging automotive sector, experiencing 8-10% annual vehicle production growth, drives demand from budget and mid-range vehicle segments with increasing comfort feature adoption as consumer purchasing power expands. Japan's sustained automotive leadership, featuring Toyota, Honda, Nissan, and Suzuki, maintains technology-intensive seat development supporting global premium and hybrid vehicle platforms. ASEAN growth dynamics including Thailand, Indonesia, and Vietnam establish manufacturing hubs supporting regional vehicle production expansion with projected 5% CAGR.

Competitive Landscape

The automotive seat market is highly oligopolistic, with Adient, Lear, Forvia, and Toyota Boshoku supplying most global vehicle programs. Their large scale provides advantages such as strong purchasing power, vertically integrated metal processing, and global program management capabilities, enabling pricing stability and margin protection during raw-material cost volatility. However, competitive pressure is intensifying as EV manufacturers and new mobility entrants demand lighter, smarter, and more integrated seating systems, often within shorter development timelines.

Tier-1 suppliers are responding with dual-track strategies that combine operational efficiency in high-volume structural components with technological differentiation in premium and value-added modules. Lear, through its IDEA (Innovate, Digitize, Engineer, Automate) roadmap, has strengthened automation capabilities with the acquisition of WIP Industrial Automation, integrating robotics and digital twin technologies into seat cushion assembly to reduce defects and accelerate model changeovers. Forvia is advancing lightweight and sustainability objectives by deploying NAFILean natural-fiber composite materials, helping OEMs meet emerging lifecycle and environmental regulations.

Key Industry Developments

- In February 2025, Lear Corporation confirmed ComfortMax integration on General Motors vehicles starting Q2 2025, offering 40% faster thermal response and 50% lower assembly complexity.

- In October 2024, Yanfeng introduced XiM25 smart cabin for Generation Z with adaptive zero-gravity seats and integrated SafeUnit™ protection.

- In September 2024, FORVIA unveiled a lightweight truck seat portfolio at IAA Transportation 2024 that achieves up to 40% CO2 reduction.

Companies Covered in Automotive Seats Market

- Adient PLC

- Faurecia SA

- Lear Corporation

- Toyota Boshoku Corporation

- TS Tech Co., Ltd.

- Magna International Inc.

- Aisin Seiki Co., Ltd.

- Tachi-S Co., Ltd.

- NHK Spring Co., Ltd.

- Guelph Manufacturing Group

- Futuris Group

- Others Key Players

Frequently Asked Questions

The Automotive Seats market is estimated to be valued at US$ 71.5 Bn in 2026.

The key demand driver for the Automotive Seats market is the rising consumer and OEM focus on comfort, safety, and interior differentiation, combined with the increasing content value of seats in modern vehicles.

In 2026, the Asia Pacific region will dominate the market with an exceeding 35% revenue share in the global Automotive Seats market.

Among the Technology, Standard (Manual) Seats hold the highest preference, capturing beyond 58.3% of the market revenue share in 2026, surpassing other Technology.

The key players in Automotive Seats are Adient PLC, Faurecia SA, Lear Corporation and Toyota Boshoku Corporation.