- Automotive Components & Materials

- Automotive Pedestrian Protection System Market

Automotive Pedestrian Protection System Market Size, Share, Trends, Regional Forecasts 2026 - 2033

Automotive Pedestrian Protection System Market Product Type (Active Pedestrian Protection Systems, Passive Pedestrian Protection Systems), Component (Sensors & Cameras, Actuators, Control Units, Others), Vehicle Type (Passenger Vehicles, Light Commercial Vehicles, Heavy Commercial Vehicles, Electric Vehicles), Sales Channel (OEM, Aftermarket), and Regional Analysis from 2026 - 2033

Automotive Pedestrian Protection System Market Share and Trends Analysis

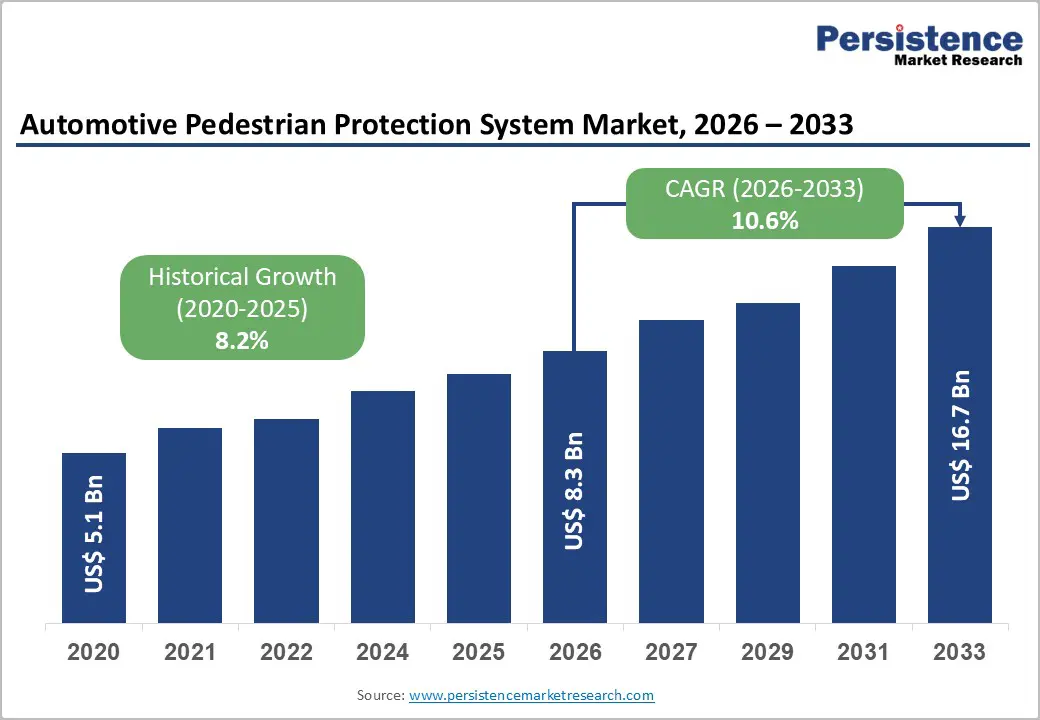

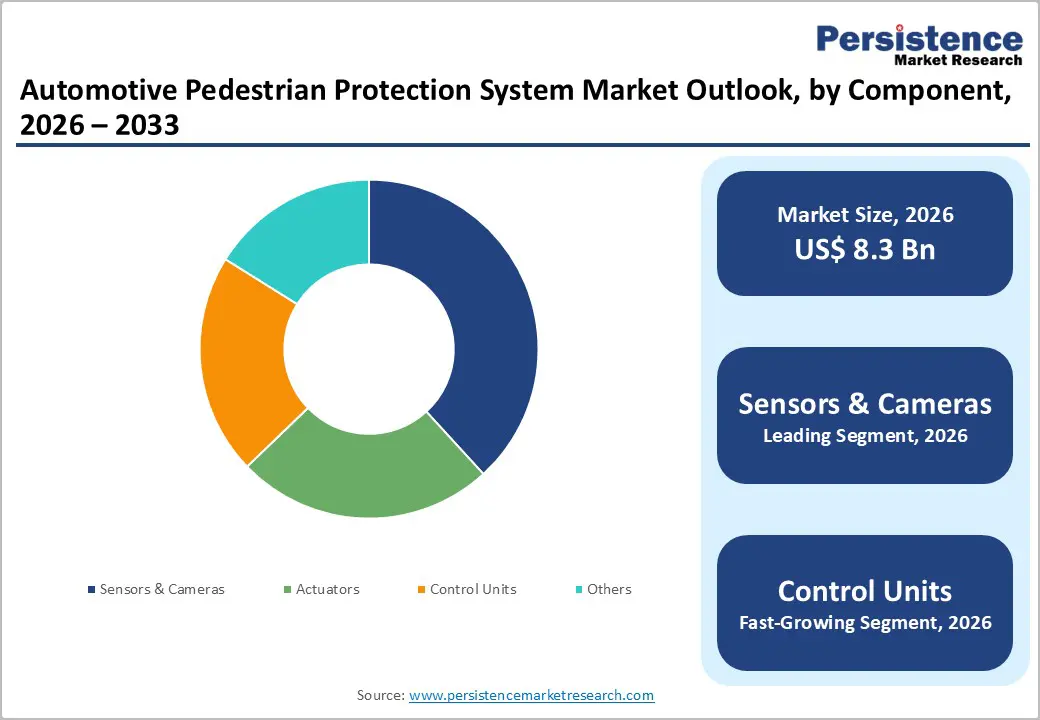

The global automotive pedestrian protection system market size is anticipated at US$ 8.3 billion in 2026 and is projected to reach US$ 16.7 billion by 2033, growing at a CAGR of 10.6% between 2026 and 2033.

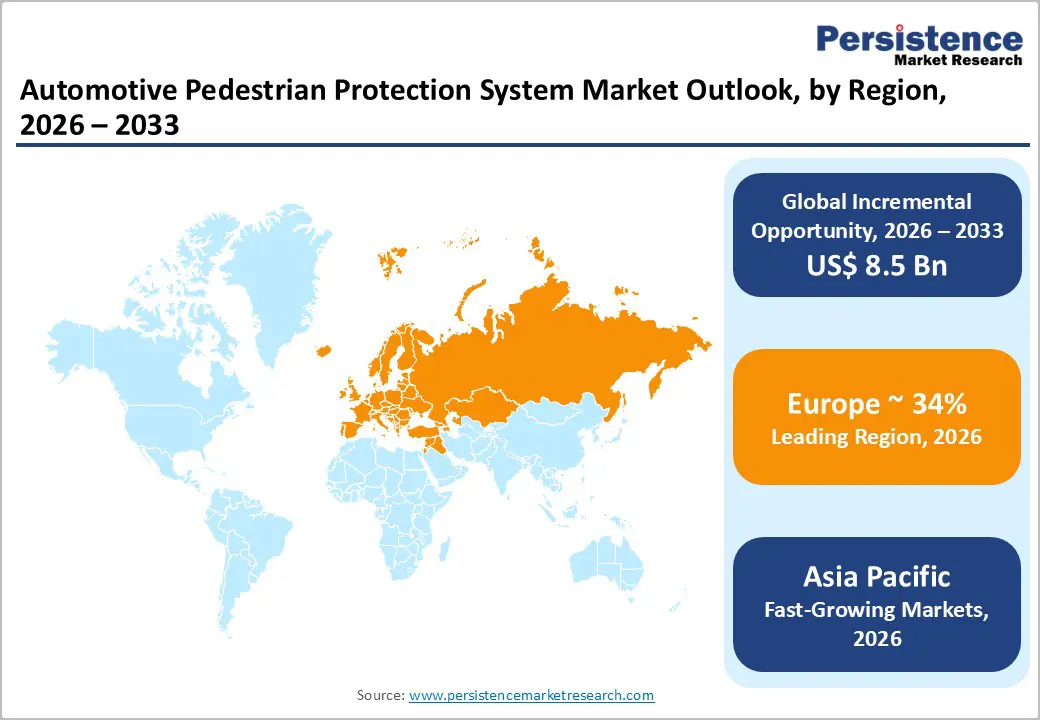

Market expansion is driven by stringent mandates, including US DOT pedestrian detecting AEB by September 2029, rising autonomous and semi-autonomous vehicle adoption, and AI-enabled multi-sensor fusion enabling real-time detection and collision prevention. North America grows at 9.4% CAGR, Europe holds 34% share via safety harmonization, while Asia Pacific expands 12.5% CAGR on vehicle growth and autonomy.

Key Industry Highlights:

- Active pedestrian protection systems command 63% market share, supporting regulatory compliance and collision prevention, while Passive PPS expands at 8.8% CAGR, enabling cost-effective injury mitigation and broader vehicle segment adoption.

- Sensors & cameras lead at 38% component share, enabling pedestrian detection, while Control units expand at 11.2% CAGR, supporting AI integration and autonomous decision-making advancement.

- Passenger vehicles lead at 68% market share, while Electric vehicles expand at 15.2% CAGR, driving emerging autonomous vehicle development and technology integration requirements.

- Europe maintains 34% market share with a strict regulatory compliance emphasis, Asia Pacific expands at 12.5% CAGR with vehicle production dominance, and North America grows at 9.4% CAGR with regulatory mandate implementation.

- US DOT issues final rule for mandatory AEB with pedestrian detection by September 2029 (April 2024), Iteris and Sumitomo Electric form partnership for advanced pedestrian detection (2024), and Las Vegas implements AI pedestrian detection with USD 1.4M federal grant (2024) demonstrating regulatory momentum and technology advancement.

| Key Insights | Details |

|---|---|

|

Automotive Pedestrian Protection System Market Size (2026E) |

US$ 8.3 billion |

|

Market Value Forecast (2033F) |

US$ 16.7 billion |

|

Projected Growth CAGR (2026-2033) |

10.6% |

|

Historical Market Growth (2020-2025) |

8.2% |

Market Dynamics Analysis

Drivers - Stringent Regulatory Mandates and Government Safety Requirements Driving System Adoption

Regulatory mandates and government safety requirements are systematically driving pedestrian protection system adoption, with US DOT requiring automatic emergency braking with pedestrian detection on all new passenger vehicles and light trucks by September 1, 2029, UN regulations establishing harmonized requirements for vehicle-to-pedestrian AEBS at low speeds 0-60 km/h, and EU regulations mandating pedestrian safety improvements supporting sustained investment in advanced sensor and control systems across global automotive manufacturers. US DOT mandate (FMVSS 127) implementation. UN regulation requirements for AEBS pedestrian capability. EU General Safety Regulation compliance. Detection at speeds up to 62 mph. Daylight and nighttime pedestrian detection capability. Compliance deadline driving OEM investment. International regulatory harmonization support.

Pedestrian Safety Impact and Fatality Reduction Focus Supporting Consumer and Government Priority

Pedestrian safety and fatality reduction are systematically driving protective system adoption, with automatic emergency braking with pedestrian detection reducing pedestrian fatalities by approximately 27% according to European Commission research, AEB systems preventing 38% of rear-end crashes, and US NHTSA estimating 24,000+ annual injuries prevented and 360+ lives saved annually supporting sustained investment in safety-critical pedestrian protection technology across vehicle segments. Pedestrian accident statistics (70,000+ annually in US). Fatality reduction (27% with AEB+pedestrian detection). Injury mitigation focus (24,000+ annually). Government policy prioritization. Consumer safety consciousness. Insurance incentive support. Autonomous vehicle safety imperative.

Restraint - High System Integration Costs and Technical Complexity Limiting Adoption Across Vehicle Segments

Pedestrian protection system market expansion is constrained by high costs tied to sensor arrays, computing hardware, and complex integration, as active systems require multiple cameras, radar, lidar, and ultrasonic sensors adding USD 800–2000+ per vehicle, limiting adoption in mid-range and budget segments. Additional barriers include multi-sensor calibration challenges, platform integration with existing vehicle architectures, advanced software development and validation requirements, and increasingly sophisticated control units. Extensive testing, homologation, and certification expenses further elevate costs, while limited availability of skilled technical expertise and supply chain constraints for semiconductors and sensors restrict scalability, slow deployment timelines, and reduce penetration across price-sensitive markets.

False Positive Rates and Real-World Performance Variability Affecting Consumer Confidence

Pedestrian protection system market expansion is constrained by sensor accuracy limitations across diverse environmental conditions including adverse weather, low visibility lighting, and dense urban traffic, increasing false positive and false negative risks that undermine consumer trust and regulatory compliance. Rain, fog, and snow degrade sensor performance, while night driving and glare affect camera reliability. Crowded city environments with overlapping pedestrian and vehicle movements complicate object classification and tracking. Detection accuracy variability elevates false alarm frequency concerns, demanding extensive validation. As a result, system reliability verification, scenario-based testing, and regulatory certification become more complex, time-intensive, and costly, slowing large-scale deployment globally.

Opportunity- Emerging Market Vehicle Proliferation and Government Infrastructure Investment Supporting Growth

Emerging market vehicle proliferation and expanding government safety infrastructure investment create a substantial growth opportunity, led by Asia Pacific advancing at 12.5% CAGR as rapid urbanization and rising vehicle ownership accelerate pedestrian protection system adoption across personal and commercial fleets. Increasing urban traffic density heightens pedestrian safety concerns, prompting governments to strengthen road safety programs and enforcement. Infrastructure development initiatives, including smart roads and monitoring systems, support technology integration. Manufacturing cost advantages and scalable supply chains enable competitive pricing, while local production facility development improves availability and compliance. Government incentive programs, localization mandates, and public–private partnerships further encourage OEM adoption, allowing pedestrian protection solutions to penetrate price-sensitive markets and extend growth beyond mature developed automotive regions and long-term market sustainability.

Smart City Integration and Infrastructure-Based Pedestrian Detection Systems

Smart city infrastructure integration and infrastructure-based pedestrian detection present a strong emerging opportunity, as cities deploy smart crossings equipped with sensors, cameras, and communication devices enabling coordinated safety responses. Las Vegas exemplifies this trend through a USD 1.4 million federal grant supporting AI-powered pedestrian detection along the Fremont Street corridor. These initiatives enable vehicle-to-infrastructure communication, traffic signal optimization, and pedestrian alert systems delivering real-time warnings to drivers and vulnerable road users. City-level safety strategies increasingly prioritize data-driven accident reduction, encouraging adoption of connected detection platforms. Public investment programs, smart mobility policies, and urban digitization efforts accelerate ecosystem development linking vehicles, infrastructure, and pedestrians, expanding pedestrian protection solutions beyond vehicle-based systems into integrated urban safety frameworks globally across modern cities worldwide.

Category-wise Analysis

Product Type Insights

Active pedestrian protection systems command 63% of market share, representing dominant product type with real-time pedestrian detection, warning systems, and automatic emergency braking capabilities supporting regulatory compliance and collision prevention across diverse driving scenarios. Real-time detection capability. Automatic braking activation. Warning systems implementation. Collision prevention focus. Complex algorithms utilization. Multi-sensor integration. Regulatory compliance leadership.

Passive pedestrian protection systems expand at 8.8% CAGR, driven by cost-effective pop-up bonnets, external airbags, and deformable hood structures supporting injury mitigation and collision energy absorption providing low-cost safety enhancement for broader vehicle segments. Pop-up hood technology. External airbags deployment. Deformable structures integration. Cost-effectiveness advantage. Energy absorption capability. Broad adoption potential. Injury mitigation focus.

Component Insights

Sensors and cameras command 38% of component market share, representing critical sensing infrastructure with cameras, radar, lidar, and ultrasonic sensors enabling pedestrian detection and tracking across diverse environmental conditions. Control units expand as a prominently growing component at 11.2% CAGR, driven by increasing computational requirements for real-time data processing and decision-making supporting emerging demand for advanced processors and AI integration enabling autonomous decision-making and emergency response initiation.

Vehicle Type Insights

Passenger vehicles command 68% of market share, representing dominant segment reflecting highest production volume and regulatory compliance requirements with broad consumer base supporting sustained market growth and technology advancement. Volume production leadership. Consumer focus prioritization. Regulatory compliance mandate. Technology standardization. Global distribution networks. Premium and budget segments. Market leadership positioning.

Electric vehicles expand as fastest-growing segment at 15.2% CAGR, driven by EV adoption acceleration requiring integrated safety systems and advanced sensor compatibility supporting emerging high-growth niche with specialized requirements for quiet vehicle operation and precise pedestrian detection.

Sales Channel Insights

Original equipment manufacturer channel commands 82% of market share, representing a dominant sales channel with direct vehicle manufacturer integration supporting factory-installed systems ensuring quality control and regulatory compliance across new vehicle production. Aftermarket channel is likely to expand at a positive CAGR, driven by retrofit demand from existing fleet owners and safety-conscious consumers supporting complementary market development enabling fleet modernization and safety enhancement for non-OEM integrated vehicles.

Regional Insights

North America Automotive Pedestrian Protection System Market Share

North America expands at 9.4% CAGR, driven by regulatory mandate leadership, technology innovation focus, automotive OEM concentration, and safety-conscious consumer base supporting market development and premium technology adoption. North American market characterized by regulatory compliance focus and technology leadership with US DOT mandate driving sustained investment. Strong emphasis on pedestrian fatality reduction and injury prevention.

Europe Automotive Pedestrian Protection System Market Share

Europe maintains its leading presence with 34% market share and is growing at a considerable pace, driven by stringent EU regulations, pedestrian-centric urban planning, automotive technology leadership, and regulatory harmonization supporting advanced technology adoption and compliance focus. European market characterized by strict regulatory compliance and sustainability emphasis with manufacturers focusing on advanced safety technologies. Strong emphasis on urban pedestrian safety and vulnerable road user protection. Established technical standards supporting reliability and consistency.

Asia Pacific Automotive Pedestrian Protection System Market Trends

Asia Pacific expands as the fastest-growing region with 12.5% CAGR, driven by vehicle production dominance, rapid urbanization, autonomous vehicle development, and emerging market technology adoption, supporting market growth exceeding global averages. The market growth in Asia Pacific is characterized by rapid growth and emerging market opportunities with China leading through massive vehicle production and autonomous vehicle development. India emerging as high-growth market with vehicle proliferation. Cost-competitive production attracting global supply chain development. Government focus on road safety and infrastructure investment accelerating adoption.

Competitive Landscape

The global pedestrian protection system market shows consolidation, led by multinational players such as Robert Bosch GmbH, Continental AG, and Valeo SA through integrated sensors, control units, and software platforms. Specialized suppliers including Mobileye, Denso, Autoliv, and Aptiv strengthen positioning via technology focus, while emerging Chinese manufacturers and technology firms capture growth through innovation, localization, and cost competitive solutions, sustaining environment.

Strategic Developments:

- In October 2024, Volvo announced 2025 EX90 SUV featuring groundbreaking Luminar LiDAR safety system utilizing laser technology creating detailed 3D surroundings mapping, detecting pedestrians at distances up to 250 meters, significantly enhancing collision avoidance capability and advancing automotive safety technology.

- In May 2025, Mobileye announced breakthrough Imaging Radar selection by leading global automaker for SAE Level 3 automated highway driving starting 2028, detecting pedestrians, motorcycles, cyclists at 315 meters with exceptional performance in fog, rain, and complex environments, advancing autonomous vehicle safety.

- In October 2025, Autoliv announced intention to establish joint venture with Hangsheng Electric, Chinese EV electronics specialist, targeting first quarter 2026 formation with 40% Autoliv stake, producing safety electronics tailored for Chinese market while extending advanced solutions to markets beyond China.

Companies Covered in Automotive Pedestrian Protection System Market

- Robert Bosch GmbH

- Continental AG

- Valeo SA

- Denso Corporation

- Mobileye (Intel)

- ZF Friedrichshafen AG

- Autoliv Inc.

- Aptiv PLC

- FLIR Systems

- Hyundai Mobis

- Magna International

- BMW AG

Frequently Asked Questions

The global automotive pedestrian protection system market size is anticipated at US$ 8.3 billion in 2026 and is projected to reach US$ 16.7 billion by 2033.

The automotive pedestrian protection system market growth is driven by mandatory pedestrian-detecting AEB regulations, rising pedestrian safety priorities reducing fatalities, and expanding autonomous and semi-autonomous vehicle deployment requiring advanced detection and collision-avoidance systems.

The market is projected to expand at a 10.6% CAGR between 2026 and 2033.

Key opportunities include rapid APAC vehicle growth, smart-city and vehicle-to-infrastructure pedestrian detection deployments, and rising demand for aftermarket retrofit solutions to modernize existing vehicle fleets.

The market is led by Bosch, Continental, Valeo, Denso, Mobileye (Intel), and ZF Friedrichshafen, supported by regulatory mandates and recent AI-based pedestrian detection partnerships and smart-city deployments.