- Automotive Components & Materials

- Automotive Hypervisor Market

Automotive Hypervisor Market Size, Share, and Growth Forecast 2026 2033

Automotive Hypervisor Market by Product Type (Type 1, Type 2), by Mode of Operation (Semi Autonomous, Fully Autonomous), by Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles), by End User (Economy, Mid Priced, Luxury), by Regional Analysis, 2026 2033

Automotive Hypervisor Market Size and Trend Analysis

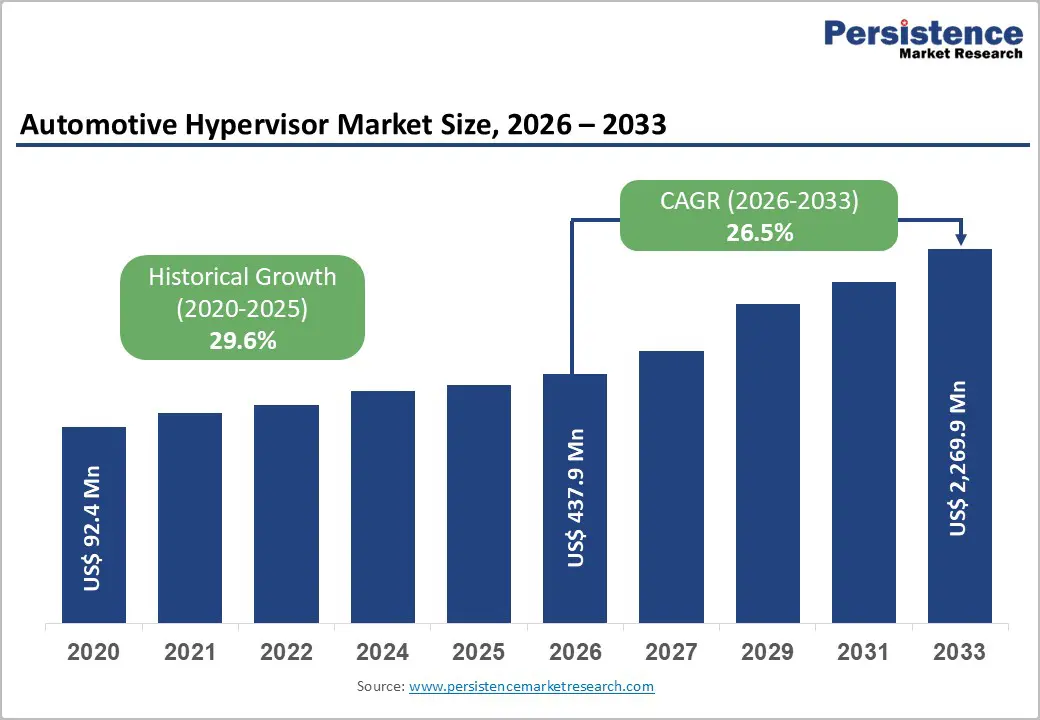

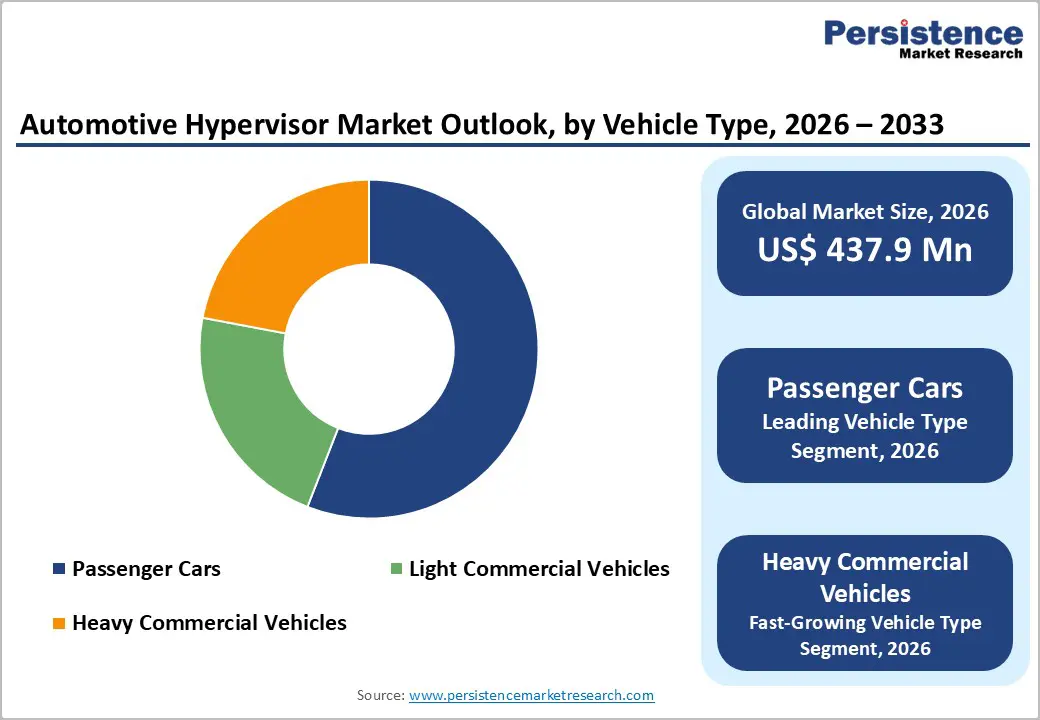

The global Automotive Hypervisor market size is expected to be valued at US$ 437.9 million in 2026 and projected to reach US$ 2,269.9 million by 2033, growing at a CAGR of 26.5% between 2026 and 2033.

Market expansion is fundamentally driven by accelerating adoption of software defined vehicle architectures, escalating demand for autonomous driving capabilities requiring sophisticated virtualization infrastructure, and growing emphasis on cybersecurity and functional isolation across multiple vehicle domains. The rapid transition from distributed electrical architectures to centralized computing platforms necessitates advanced hypervisor technologies enabling consolidation of multiple electronic control units into unified domain controllers.

Key Market Highlights

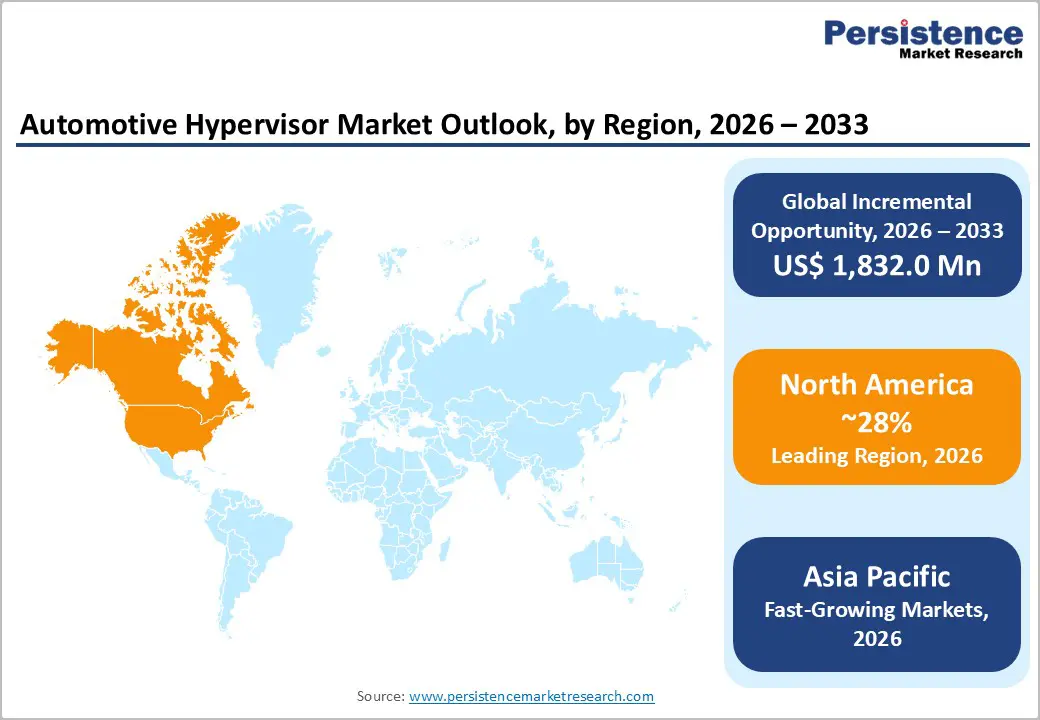

- Leading Region: North America leads the global Automotive Hypervisor Market with approximately 28% share in 2025, supported by substantial automotive manufacturing base, major original equipment manufacturer presence, and regulatory emphasis on safety systems requiring virtualization.

- Fastest Growing Region: Asia Pacific is the fastest growing region, expected to post approximately 31.7% CAGR through 2032, driven by rapid autonomous vehicle development, software-defined architecture adoption by Chinese manufacturers, and expanding semiconductor capabilities.

- Dominant Segment from Product Type: Type 1 Hypervisors dominate with roughly 67% share in 2025, reflecting superior performance, lower latency, and proven deployment across automotive safety-critical applications.

- Fastest Growing Segment from Mode of Operation: Fully Autonomous is the fastest growing segment, with estimated 29.7% CAGR through 2033, fueled by accelerating autonomous vehicle platform development and emerging regulatory frameworks supporting Level 3+ operations.

- Key Market Opportunity: Development of advanced real-time hypervisors for autonomous vehicle platforms managing complex computational requirements and sensor fusion represents a significant opportunity for establishing competitive differentiation.

| Key Insights | Details |

|---|---|

| Automotive Hypervisor Market Size (2026E) | US$ 437.9 million |

| Market Value Forecast (2033F) | US$ 2,269.9 million |

| Projected Growth (CAGR 2026 to 2033) | 26.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 29.6% |

Market Dynamics

Market Growth Drivers

Accelerating Transition to Software Defined Vehicle Architectures and Domain Consolidation

The automotive industry’s fundamental shift toward software defined vehicle architectures represents the most significant growth driver for automotive hypervisor adoption. Traditional vehicle electrical architectures featured distributed electronic control units managing isolated functions, creating complexity, cost, and maintenance challenges. Modern vehicle architecture consolidates multiple control domains, including infotainment, advanced driver assistance systems, and powertrain management, onto unified computing platforms utilizing hypervisor-based virtualization.

According to Siemens Digital Industries Software, hypervisor consolidation reduces the total number of ECU by approximately 20%, substantially lowering hardware costs while improving system efficiency. Major original equipment manufacturers, including Tesla, BMW, and Volkswagen, are actively standardizing on hypervisor-based architectures to future-proof vehicle platforms against evolving software requirements. The consolidation strategy enables independent teams developing specialized software for distinct domains to integrate seamlessly onto shared hardware platforms without software conflicts, accelerating development timelines and reducing integration complexity.

Rapid Expansion of Autonomous Driving Capabilities and ADAS System Adoption

The exponential growth in autonomous vehicle development and advanced driver assistance system deployment represents a transformational growth driver for sophisticated hypervisor technologies. Level 2+ autonomous systems require management of multiple parallel computational tasks, including sensor fusion from LiDAR, radar, and camera systems, real-time path planning, obstacle detection, and vehicle control coordination operating simultaneously on resource-constrained automotive hardware.

The computational complexity of autonomous vehicle platforms necessitates hypervisor-enabled resource allocation across multiple AI accelerators, specialized sensor processing units, and safety-critical monitoring systems. Regulatory clarity emerging in major markets, including Germany’s Level 4 legalization and Japan’s targeted nationwide Level 4 deployment by 2027, is accelerating the development of commercial autonomous vehicle platforms and driving substantial hypervisor demand.

Market Restraints

Complex System Integration and Cybersecurity Requirements

Automotive hypervisor deployment is highly complex, integrating virtualization technologies with safety-critical vehicle systems subject to stringent ISO 26262 functional safety standards. Hypervisors must provide complete isolation between virtual machines running safety-critical applications and non-safety infotainment systems while ensuring real-time performance for time-sensitive vehicle functions. The requirement for comprehensive security frameworks protecting against cyber threats, combined with strict regulatory compliance requirements, necessitates specialized expertise constraining widespread adoption among smaller manufacturers. Legacy vehicle platforms designed without virtualization considerations require substantial rearchitecture efforts for hypervisor integration, elevating implementation costs and development timelines.

High Development Costs and Limited Specialized Expertise

Automotive hypervisor development requires substantial research and development investment in microkernel architecture design, real-time scheduling optimization, and safety certification processes. The limited availability of engineers with specialized expertise in embedded virtualization, real time systems, and automotive safety standards creates talent constraints constraining rapid market expansion. Smaller automotive suppliers and emerging vehicle manufacturers struggle to justify investments in hypervisor development due to limited production volumes and uncertain returns on development expenditures. The requirement for comprehensive testing, validation, and certification across diverse hardware platforms and vehicle configurations further elevates development costs and implementation timelines.

Market Opportunities

Development of Advanced Real-Time Hypervisors for Complex Autonomous Systems

Significant growth opportunities exist for hypervisor manufacturers developing specialized solutions optimized for autonomous vehicle platforms managing extensive computational complexity and real time performance requirements. Autonomous vehicle hypervisors represent the fastest growing market segment at 20% CAGR, driven by computational demands of Level 3+ autonomous systems. Manufacturers investing in hypervisor technology advancement optimized for heterogeneous hardware architectures, artificial intelligence workload management, and advanced sensor fusion capabilities can establish competitive differentiation in premium autonomous vehicle segments. The integration of AUTOSAR Adaptive standard compliance with advanced hypervisor capabilities supports seamless software ecosystem integration while addressing safety and real-time performance requirements essential for autonomous vehicle platforms.

Expansion into Emerging Markets and Cost Optimized Solutions for Lower Priced Vehicle Segments

Substantial growth opportunities exist for hypervisor manufacturers developing cost effective solutions optimized for emerging market requirements across mid priced and economy vehicle segments. Asia Pacific regions demonstrate exceptional growth potential, with 38% regional market share in 2024 and a 15% CAGR. Chinese original equipment manufacturers are rapidly adopting software-defined architectures and localizing silicon solutions, with approximately one-third of vehicles built in China for the 2025 model year featuring domain controllers incorporating hypervisor instances. Manufacturers developing simplified, cost-optimized hypervisor solutions meeting the requirements of emerging market vehicle platforms can establish strong competitive positions. Strategic partnerships with regional semiconductor manufacturers, supply chain integration, and localized customer support facilitate market penetration in high-growth emerging economies.

Category wise Insights

Product Type Analysis

Within product type category, Type 1 Hypervisors command the dominant market position with approximately 67% market share in 2025, reflecting their establishment as the standard virtualization approach in automotive applications. Type 1 hypervisors operate directly on hardware without requiring an underlying operating system, providing superior performance, lower latency, and minimal resource overhead essential for automotive real-time systems. The direct hardware access, exceptional reliability, and proven performance across decades of deployment support Type 1 hypervisor dominance in safety-critical automotive environments. Major automotive suppliers, including Wind River, QNX, and Siemens, extensively use Type 1 hypervisor architectures to optimize performance for automotive-specific requirements.

Mode of Operation Analysis

By mode of operation, semi-autonomous dominates the market with approximately 64% market share in 2025, reflecting widespread deployment of Level 2 advanced driver assistance systems mandated across major automotive markets. Semi-autonomous systems require functional isolation between safety-critical perception algorithms and non-safety infotainment components, with hypervisors providing essential domain separation. The mature supply chain infrastructure, established safety certification processes, and proven technology deployment across millions of vehicles support semi-autonomous segment dominance.

Vehicle Type Analysis

By vehicle type, Passenger Cars represent the leading segment, commanding approximately 58% market share in 2025, driven by the segment’s volume production scale and emphasis on differentiating vehicles through advanced infotainment and autonomous driving capabilities. Passenger vehicle manufacturers extensively use hypervisors to consolidate multiple domains, reducing hardware complexity and enhancing software flexibility, thereby supporting consumer-focused features. Light and heavy commercial vehicle segments demonstrate growing interest in hypervisor-enabled fleet management and predictive telematics applications.

The fastest growing vehicle type segment is Heavy Commercial Vehicles, projected to expand at approximately 28.3% CAGR through 2033, driven by the adoption of advanced fleet management systems, autonomous driving for long haul operations, and regulatory emphasis on safety systems requiring sophisticated virtualization architectures.

End User Analysis

By end user, Luxury Vehicles commands the leading position with approximately 51% market share in 2025, reflecting premium vehicle manufacturers’ emphasis on advanced autonomous driving capabilities, sophisticated infotainment systems, and consumer preference for feature-rich platforms. Luxury vehicle segments prioritize cutting-edge technology adoption, enabling early deployment of advanced hypervisor-enabled vehicle architectures. The fastest growing end user segment is Economy Vehicles, expected to expand at approximately 27.4% CAGR through 2033, driven by cost effective hypervisor solutions enabling feature differentiation across price sensitive segments while maintaining manufacturing margins.

Regional Insights

North America Automotive Hypervisor Market Trends and Insights

North America commands approximately 28% global market share in 2025, supported by substantial automotive manufacturing base, established innovation ecosystem, and regulatory emphasis on safety systems and emissions reduction. The United States dominates North American markets with major original equipment manufacturers, including Tesla, General Motors, and Ford, aggressively deploying hypervisor-based software-defined vehicle architectures. Qualcomm Technologies Inc. and NXP Semiconductor maintain significant automotive semiconductor operations supporting hypervisor-enabled platform development and deployment across North American manufacturers.

The region’s regulatory framework, including NHTSA guidelines for autonomous vehicle safety, drives adoption of advanced virtualization platforms enabling functional isolation and safety-critical workload management. According to industry sources, Tesla’s Autopilot, BMW’s iDrive, and emerging autonomous vehicle platforms extensively utilize hypervisor technologies, consolidating multiple vehicle domains. North American manufacturers emphasize software-defined vehicle development, supporting competitive differentiation through advanced autonomous capabilities and connected vehicle features requiring sophisticated hypervisor infrastructure.

Europe Automotive Hypervisor Market Trends and Insights

Europe represents a significant market, commanding approximately 26% global share in 2025, characterized by emphasis on regulatory compliance, sustainability focus, and automotive engineering excellence. Germany, the United Kingdom, France, and Spain host major automotive manufacturers, including BMW, Mercedes-Benz, Volkswagen, and Audi, actively deploying hypervisor-enabled software-defined architectures. Siemens AG and Continental AG leverage advanced technology capabilities supporting hypervisor development and automotive platform integration across European manufacturers.

European regulatory frameworks emphasizing GDPR data protection, cybersecurity standards, and autonomous vehicle safety guidelines drive adoption of advanced hypervisor technologies enabling secure virtual machine isolation. According to industry announcements, major European automotive manufacturers are transitioning to centralized computing architectures utilizing hypervisor virtualization, consolidating infotainment, ADAS, and powertrain domains. The region’s emphasis on safety standards and functional isolation between vehicle domains supports premium positioning for advanced hypervisor solutions.

Asia Pacific Automotive Hypervisor Market Trends and Insights

Asia Pacific emerges as the fastest-growing regional market, projected to expand at approximately 31.7% CAGR through 2033, driven by rapid automotive platform electrification, aggressive autonomous vehicle development by Chinese manufacturers, and emerging regulatory frameworks supporting advanced vehicle technologies. China represents the largest regional market with domestic original equipment manufacturers, including BYD, NIO, and XPeng, aggressively adopting software-defined vehicle architectures. According to regional analysis, approximately one-third of vehicles built in China for the 2025 model year feature domain controllers incorporating hypervisor instances, reflecting accelerated hypervisor adoption across Chinese automotive manufacturers.

Japan maintains technological leadership with manufacturers including Toyota, Honda, and Nissan deploying hypervisor-enabled platforms across autonomous and connected vehicle initiatives. The region’s manufacturing cost advantages, expanding semiconductor design capabilities, and government emphasis on autonomous vehicle development create substantial opportunities for hypervisor technology providers. Renesas Electronics Corp. and Panasonic Corporation leverage their strong regional automotive supplier positions to support hypervisor deployment across Asian vehicle platforms.

Competitive Landscape

The global automotive hypervisor market is characterized by a fragmented yet rapidly maturing competitive structure, shaped by the presence of specialized software vendors and established automotive technology suppliers. Market participants primarily compete on software robustness, long-term reliability, and the ability to support mixed-criticality workloads within increasingly centralized vehicle architectures. Business strategies focus on deep integration with automotive operating systems, seamless compatibility with vehicle electronic architectures, and close collaboration with OEMs and Tier-1 suppliers early in the vehicle development cycle.

Standardization plays a central role in competitive positioning, with strong emphasis on compliance with adaptive automotive software frameworks, functional safety requirements, and cybersecurity regulations. Performance optimization for real-time workloads, efficient resource isolation, and scalability across heterogeneous computing platforms are key differentiators. Additionally, ecosystem partnerships with semiconductor platform providers enable tighter hardware–software co-design. As software-defined and autonomous vehicles gain traction, vendors are prioritizing continuous software upgrades, certification readiness, and platform flexibility to secure long-term design wins.

Key Market Developments

- May 2025: BlackBerry QNX launched QNX Hypervisor 8.0, enabling multiple operating systems including Android, Linux, and QNX to operate simultaneously on unified system on chip platforms with enhanced security and performance characteristics.

- September 2024: NXP Semiconductor announced expanded S32 CoreRide platform integration with advanced hypervisor capabilities, facilitating domain controller consolidation across

Companies Covered in Automotive Hypervisor Market

- Qualcomm Technologies Inc.

- Panasonic Corp.

- Siemens

- Green Hills Software

- Sysgo GmbH

- Wind River Systems Inc.

- Renesas Electronic Corp.

- Denso Corp.

- Visteon

- Harman International

- KPIT

- OpenSynergy GmbH

- BlackBerry Limited

- Continental AG

- NXP Semiconductor N.V.

- Elektrobit

- Mentor Graphics

Frequently Asked Questions

The global Automotive Hypervisor Market is projected to reach US$ 437.9 million in 2026, up from US$ 92.4 million in 2020.

Key demand drivers include accelerating transition to software defined vehicle architectures, rapid expansion of autonomous driving capabilities and ADAS system adoption.

North America currently leads with approximately 28% market share in 2025, supported by substantial automotive manufacturing base, major original equipment manufacturer presence, and established innovation ecosystem.

Advanced real time hypervisor development optimized for autonomous vehicle platforms represents the most attractive opportunity area.

Key players include QNX (BlackBerry), Wind River, Siemens, Green Hills Software, Qualcomm, NXP Semiconductor, Renesas, Sysgo, and Continental AG, among others.